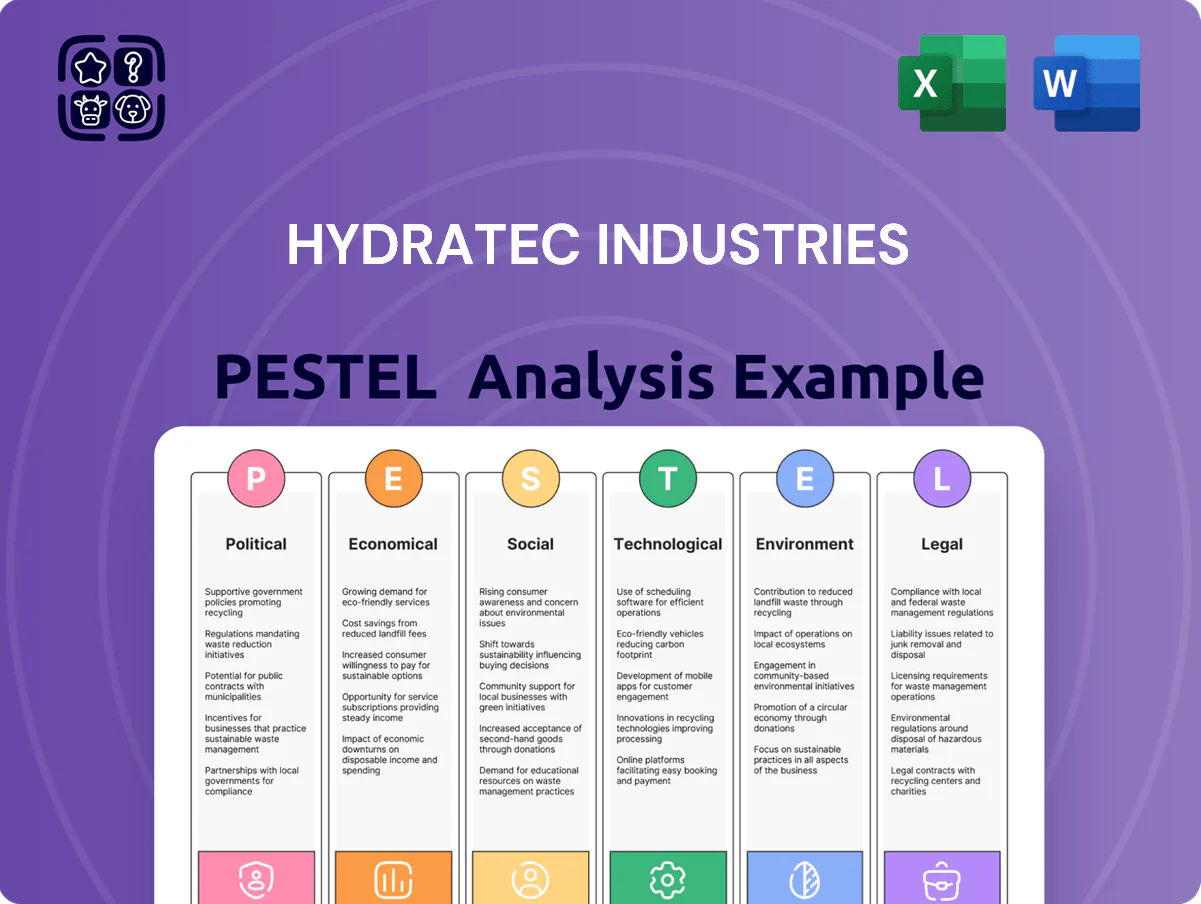

Hydratec Industries PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and advancing water technologies influence Hydratec Industries’ growth and risks—our concise PESTLE snapshot highlights opportunities and vulnerabilities you need to know; purchase the full PESTLE for a detailed, actionable roadmap to strengthen strategy and investment decisions.

Political factors

EU Green Deal and Industrial Strategy

The EU Green Deal’s goal of climate neutrality by 2050 shapes Hydratec’s strategy, with EU industry emissions targets cutting 55% by 2030 from 1990 levels influencing supply-chain decarbonization investments.

Policies promoting circularity and the 2021 Plastics Strategy, targeting a 10 million tonne annual increase in recycled plastics use by 2030, boost demand for Hydratec’s recycling-ready components.

Aligning with these objectives secures market access across the EU’s €15 trillion single market and reduces risk of non-compliance fines and trade barriers.

Geopolitical Supply Chain Stability

As of late 2025, ongoing geopolitical tensions have driven a 12–18% rise in prices for key raw materials and a 22% shortage in industrial-grade semiconductors, increasing Hydratec Industries’ component procurement costs by an estimated $8–12 million annually.

Hydratec must navigate evolving trade policies and tariffs—notably 2024–25 tariff adjustments between the US, EU and Southeast Asia—that can add 3–6% to landed costs and complicate global sourcing and distribution.

Political instability in manufacturing hubs such as Taiwan and parts of Southeast Asia heightens risk to assembly timelines, with 2025 supply disruptions causing average lead-time extensions of 4–7 weeks critical to Hydratec’s service-level agreements.

Dutch Government Innovation Subsidies

The Dutch government allocated about EUR 6.8bn in 2024 to innovation grants and R&D tax incentives (WBSO, R&D credit) targeting high-tech manufacturing and sustainable solutions, which Hydratec can tap to reduce automation and healthcare systems development costs by up to 30% of eligible spend.

Global Trade Agreements

Changes in EU-US-China trade relations affect Hydratec’s export capacity; EU goods exports to the US totaled €524bn in 2024 and to China €383bn, shifts that can alter tariff exposure for Hydratec’s automotive and food-processing components.

The group monitors rising protectionist measures—global tariff spikes averaged 7.2% in 2024—and sector-specific barriers that could reduce margins or restrict market access.

Favorable agreements (e.g., EFTA, EU trade deals) are critical to sustain Hydratec’s presence across 12+ export markets and protect ~28% of 2025 forecasted revenues from international sales.

- EU exports to US €524bn (2024)

- EU exports to China €383bn (2024)

- Global tariff spike average 7.2% (2024)

- ~28% of Hydratec’s 2025 forecasted revenue from exports

Labor Market Policy and Migration

Political decisions on labor migration and technical education in the Netherlands directly affect Hydratec Industries’ access to skilled engineers; Netherlands issued 78,000 highly skilled migrant permits in 2024, easing shortages in engineering roles.

With the industrial sector facing a 12% talent gap in STEM roles (2024 Netherlands Labor Market Monitor), policies promoting STEM education and skilled mobility are critical for Hydratec’s growth and project delivery.

Hydratec depends on a stable political framework for long-term workforce planning, hiring forecasts, and maintaining operational efficiency amid an aging technician workforce (median age ~45 in 2024).

- 78,000 highly skilled migrant permits issued in 2024

- 12% STEM talent gap reported in 2024

- Median technician age ~45 in 2024 affects succession planning

EU Green Deal, tariffs & shortages: €6.8bn R&D offsets €8–12m cost hit

Political factors: EU Green Deal and Plastics Strategy drive demand for recycling-ready components and compliance costs; 2024–25 trade tensions, tariff shifts (avg +7.2% in 2024) and raw material/semiconductor shortages raised procurement costs ~$8–12m and extended lead times 4–7 weeks; Dutch R&D support (~€6.8bn 2024) and 78,000 skilled-migrant permits (2024) mitigate a 12% STEM talent gap.

| Metric | Value (year) |

|---|---|

| EU→US exports | €524bn (2024) |

| EU→China exports | €383bn (2024) |

| Global tariff spike | 7.2% (2024) |

| Hydratec export share | ~28% (2025 forecast) |

| Raw material cost impact | $8–12m pa (late 2025) |

| Dutch R&D funds | €6.8bn (2024) |

| Skilled migrant permits | 78,000 (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hydratec Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

Concise, category-segmented PESTLE summary of Hydratec Industries designed for quick reference in meetings and presentations—editable for regional or business-line notes and easily dropped into slides or shared for rapid team alignment.

Economic factors

Eurozone Interest Rate Environment

By end-2025 the Eurozone policy rate settled near 3.25% after cuts from 2024 peak levels, keeping cost of capital elevated for capital-intensive firms like Hydratec; higher rates compress NPV on factory automation investments and slow client CAPEX. ECB rate volatility directly alters project IRRs and financing costs, so a stable or falling trend—seen in 2024–25 easing—supports larger automation orders and an expanding order book for Hydratec.

Energy Price Volatility in Europe

Energy-intensive plastic component production leaves Hydratec highly exposed to European gas and electricity swings; EU industrial electricity prices averaged about 190 EUR/MWh in 2023 vs 60 EUR/MWh pre-2021 shocks, and 2024-25 volatility continued with winter 2024 spikes up to 350 EUR/MWh in parts of Central Europe, risking margin compression if not passed to customers.

Inflationary Pressure on Raw Materials

Inflation pushed global polymer prices up about 18% and base metal prices 12% year-over-year into 2025, while specialty electronic component lead times and premiums rose 20%, pressuring input costs for Hydratec Industries.

Hydratec offsets volatility via hedging, multi-sourcing and long-term supplier contracts covering roughly 60% of annual polymer needs, reducing spot exposure and smoothing COGS.

Maintaining pricing power in food and automotive end-markets—which account for ~55% of revenue—allowed Hydratec to pass through cost increases selectively, preserving gross margins near 28% despite inflationary headwinds.

Automotive and Healthcare Sector Growth

Automotive cycles heavily affect Hydratec’s revenues: global auto production fell 2.1% in 2024 to ~79.7M units, trimming demand for specialized plastic components tied to vehicle output and EV adoption rates.

Healthcare offers resilience—global medical device spending grew ~5.6% in 2024 to $520B, buffering Hydratec with stable demand for medical-grade plastics during downturns.

Diversification across automotive and healthcare balances cyclical exposure, with healthcare reducing revenue volatility and improving margin stability.

- Automotive: -2.1% production (2024) ~79.7M units

- Healthcare: +5.6% medical device spend (2024) ~$520B

- Diversification mitigates cyclical risk, supports steady cash flow

Labor Cost Inflation

Rising wages in the Netherlands and EU pushed labor costs up ~4.5% YoY in 2024, increasing Hydratec’s engineering and assembly expenses; the company is accelerating internal automation to protect margins and offset higher payroll.

Wage pressure drives client demand for automation—EU industrial automation sales grew ~6% in 2024—supporting Hydratec’s service and equipment uptake.

- Netherlands wage growth ~4–5% (2024)

- Hydratec invests in process automation to sustain margins

- EU industrial automation market +6% (2024), boosting demand

Hydratec margins squeezed by rates, energy spikes and input inflation—hedges & automation buffer

Eurozone rates near 3.25% (end-2025) keep Hydratec financing costs elevated, moderating CAPEX by clients; energy price volatility (2023 avg €190/MWh; spikes to €350/MWh winter 2024) and input inflation (polymers +18%, metals +12% into 2025) pressure margins, offset by 60% hedged polymer coverage, pricing power in food/auto (~55% revenue) and automation-driven demand (EU automation +6% 2024).

| Metric | Value |

|---|---|

| ECB policy rate (end-2025) | ≈3.25% |

| EU industrial electricity (2023 avg) | €190/MWh |

| Winter 2024 spike | €350/MWh |

| Polymer price change | +18% (to 2025) |

| Polymer hedged | ~60% of needs |

| Gross margin | ~28% |

Preview the Actual Deliverable

Hydratec Industries PESTLE Analysis

The preview shown here is the exact Hydratec Industries PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and headings visible in this preview are the same final file you’ll download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and advancing water technologies influence Hydratec Industries’ growth and risks—our concise PESTLE snapshot highlights opportunities and vulnerabilities you need to know; purchase the full PESTLE for a detailed, actionable roadmap to strengthen strategy and investment decisions.

Political factors

EU Green Deal and Industrial Strategy

The EU Green Deal’s goal of climate neutrality by 2050 shapes Hydratec’s strategy, with EU industry emissions targets cutting 55% by 2030 from 1990 levels influencing supply-chain decarbonization investments.

Policies promoting circularity and the 2021 Plastics Strategy, targeting a 10 million tonne annual increase in recycled plastics use by 2030, boost demand for Hydratec’s recycling-ready components.

Aligning with these objectives secures market access across the EU’s €15 trillion single market and reduces risk of non-compliance fines and trade barriers.

Geopolitical Supply Chain Stability

As of late 2025, ongoing geopolitical tensions have driven a 12–18% rise in prices for key raw materials and a 22% shortage in industrial-grade semiconductors, increasing Hydratec Industries’ component procurement costs by an estimated $8–12 million annually.

Hydratec must navigate evolving trade policies and tariffs—notably 2024–25 tariff adjustments between the US, EU and Southeast Asia—that can add 3–6% to landed costs and complicate global sourcing and distribution.

Political instability in manufacturing hubs such as Taiwan and parts of Southeast Asia heightens risk to assembly timelines, with 2025 supply disruptions causing average lead-time extensions of 4–7 weeks critical to Hydratec’s service-level agreements.

Dutch Government Innovation Subsidies

The Dutch government allocated about EUR 6.8bn in 2024 to innovation grants and R&D tax incentives (WBSO, R&D credit) targeting high-tech manufacturing and sustainable solutions, which Hydratec can tap to reduce automation and healthcare systems development costs by up to 30% of eligible spend.

Global Trade Agreements

Changes in EU-US-China trade relations affect Hydratec’s export capacity; EU goods exports to the US totaled €524bn in 2024 and to China €383bn, shifts that can alter tariff exposure for Hydratec’s automotive and food-processing components.

The group monitors rising protectionist measures—global tariff spikes averaged 7.2% in 2024—and sector-specific barriers that could reduce margins or restrict market access.

Favorable agreements (e.g., EFTA, EU trade deals) are critical to sustain Hydratec’s presence across 12+ export markets and protect ~28% of 2025 forecasted revenues from international sales.

- EU exports to US €524bn (2024)

- EU exports to China €383bn (2024)

- Global tariff spike average 7.2% (2024)

- ~28% of Hydratec’s 2025 forecasted revenue from exports

Labor Market Policy and Migration

Political decisions on labor migration and technical education in the Netherlands directly affect Hydratec Industries’ access to skilled engineers; Netherlands issued 78,000 highly skilled migrant permits in 2024, easing shortages in engineering roles.

With the industrial sector facing a 12% talent gap in STEM roles (2024 Netherlands Labor Market Monitor), policies promoting STEM education and skilled mobility are critical for Hydratec’s growth and project delivery.

Hydratec depends on a stable political framework for long-term workforce planning, hiring forecasts, and maintaining operational efficiency amid an aging technician workforce (median age ~45 in 2024).

- 78,000 highly skilled migrant permits issued in 2024

- 12% STEM talent gap reported in 2024

- Median technician age ~45 in 2024 affects succession planning

EU Green Deal, tariffs & shortages: €6.8bn R&D offsets €8–12m cost hit

Political factors: EU Green Deal and Plastics Strategy drive demand for recycling-ready components and compliance costs; 2024–25 trade tensions, tariff shifts (avg +7.2% in 2024) and raw material/semiconductor shortages raised procurement costs ~$8–12m and extended lead times 4–7 weeks; Dutch R&D support (~€6.8bn 2024) and 78,000 skilled-migrant permits (2024) mitigate a 12% STEM talent gap.

| Metric | Value (year) |

|---|---|

| EU→US exports | €524bn (2024) |

| EU→China exports | €383bn (2024) |

| Global tariff spike | 7.2% (2024) |

| Hydratec export share | ~28% (2025 forecast) |

| Raw material cost impact | $8–12m pa (late 2025) |

| Dutch R&D funds | €6.8bn (2024) |

| Skilled migrant permits | 78,000 (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hydratec Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

Concise, category-segmented PESTLE summary of Hydratec Industries designed for quick reference in meetings and presentations—editable for regional or business-line notes and easily dropped into slides or shared for rapid team alignment.

Economic factors

Eurozone Interest Rate Environment

By end-2025 the Eurozone policy rate settled near 3.25% after cuts from 2024 peak levels, keeping cost of capital elevated for capital-intensive firms like Hydratec; higher rates compress NPV on factory automation investments and slow client CAPEX. ECB rate volatility directly alters project IRRs and financing costs, so a stable or falling trend—seen in 2024–25 easing—supports larger automation orders and an expanding order book for Hydratec.

Energy Price Volatility in Europe

Energy-intensive plastic component production leaves Hydratec highly exposed to European gas and electricity swings; EU industrial electricity prices averaged about 190 EUR/MWh in 2023 vs 60 EUR/MWh pre-2021 shocks, and 2024-25 volatility continued with winter 2024 spikes up to 350 EUR/MWh in parts of Central Europe, risking margin compression if not passed to customers.

Inflationary Pressure on Raw Materials

Inflation pushed global polymer prices up about 18% and base metal prices 12% year-over-year into 2025, while specialty electronic component lead times and premiums rose 20%, pressuring input costs for Hydratec Industries.

Hydratec offsets volatility via hedging, multi-sourcing and long-term supplier contracts covering roughly 60% of annual polymer needs, reducing spot exposure and smoothing COGS.

Maintaining pricing power in food and automotive end-markets—which account for ~55% of revenue—allowed Hydratec to pass through cost increases selectively, preserving gross margins near 28% despite inflationary headwinds.

Automotive and Healthcare Sector Growth

Automotive cycles heavily affect Hydratec’s revenues: global auto production fell 2.1% in 2024 to ~79.7M units, trimming demand for specialized plastic components tied to vehicle output and EV adoption rates.

Healthcare offers resilience—global medical device spending grew ~5.6% in 2024 to $520B, buffering Hydratec with stable demand for medical-grade plastics during downturns.

Diversification across automotive and healthcare balances cyclical exposure, with healthcare reducing revenue volatility and improving margin stability.

- Automotive: -2.1% production (2024) ~79.7M units

- Healthcare: +5.6% medical device spend (2024) ~$520B

- Diversification mitigates cyclical risk, supports steady cash flow

Labor Cost Inflation

Rising wages in the Netherlands and EU pushed labor costs up ~4.5% YoY in 2024, increasing Hydratec’s engineering and assembly expenses; the company is accelerating internal automation to protect margins and offset higher payroll.

Wage pressure drives client demand for automation—EU industrial automation sales grew ~6% in 2024—supporting Hydratec’s service and equipment uptake.

- Netherlands wage growth ~4–5% (2024)

- Hydratec invests in process automation to sustain margins

- EU industrial automation market +6% (2024), boosting demand

Hydratec margins squeezed by rates, energy spikes and input inflation—hedges & automation buffer

Eurozone rates near 3.25% (end-2025) keep Hydratec financing costs elevated, moderating CAPEX by clients; energy price volatility (2023 avg €190/MWh; spikes to €350/MWh winter 2024) and input inflation (polymers +18%, metals +12% into 2025) pressure margins, offset by 60% hedged polymer coverage, pricing power in food/auto (~55% revenue) and automation-driven demand (EU automation +6% 2024).

| Metric | Value |

|---|---|

| ECB policy rate (end-2025) | ≈3.25% |

| EU industrial electricity (2023 avg) | €190/MWh |

| Winter 2024 spike | €350/MWh |

| Polymer price change | +18% (to 2025) |

| Polymer hedged | ~60% of needs |

| Gross margin | ~28% |

Preview the Actual Deliverable

Hydratec Industries PESTLE Analysis

The preview shown here is the exact Hydratec Industries PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and headings visible in this preview are the same final file you’ll download immediately after checkout.