Norsk Hydro PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Explore how geopolitical shifts, regulatory pressures, and decarbonization trends are reshaping Norsk Hydro’s outlook—our concise PESTLE highlights the most consequential external forces and their strategic implications. Purchase the full PESTLE for a complete, actionable analysis that investors, strategists, and consultants can use immediately to inform decisions and mitigate risks.

Political factors

Geopolitical Trade Barriers and Tariffs

Geopolitical trade protectionism—notably US Section 232 tariffs and recent EU anti-dumping measures—reshapes global aluminum flows and can raise input costs; US tariffs on aluminum (2018) remain active while the EU imposed duties of up to 48.5% on some imports in 2023-24. Norsk Hydro must adapt to shifting trade alliances and regional blocs that affect bauxite and primary metal movement, risking margin pressure. Political stability in Brazil is critical, where Hydro’s Alunorte refinery and Paragominas mine supply a significant share of its alumina; disruptions there could impact roughly 20–25% of its upstream volumes.

European Green Deal and Carbon Border Adjustment Mechanism

As an EU-based producer, Hydro benefits from the Carbon Border Adjustment Mechanism (CBAM) in force from late 2025, which taxed high-carbon imports and increased demand for low-carbon aluminum; Hydro reported 2025 low-carbon premium volumes up ~18% YoY, supporting a 2025 EBITDA margin uplift of ~1.2 percentage points. Political shifts in Brussels on industrial subsidies and green aid—including €20–30 billion/state aid frameworks in 2024–25—directly affect Hydro's investment capacity for decarbonization projects. Continued EU support for energy transition reduces financing costs for Hydro's €1.1bn planned green smelter upgrades through 2026, while potential subsidy retrenchment could raise capital costs and delay projects.

Norwegian State Ownership and Energy Policy

The Norwegian state holds a 34.3% direct stake in Norsk Hydro ASA (2025), anchoring strategic alignment and governance stability; state control aids access to favorable long-term financing and policy influence. Government rulings on hydropower concessions and regulated domestic industrial power prices directly affect smelting margins—Hydro reported NOK 12.6 billion power-related costs in 2024. Political pressure to preserve roughly 7,000 Norwegian jobs often tempers shutdowns despite global cost pressures.

Resource Nationalism in Emerging Markets

Resource nationalism elevates risk for Hydro’s upstream operations: 2024 saw 15% of global mining policy reforms target royalties and local processing, affecting Hydro’s sourcing in South America and Africa where metals contributed ~22% of its raw-material spend in 2023.

Political shifts can trigger higher taxes or local-processing mandates—Argentina, Peru and Zambia introduced tougher mineral codes between 2022–2024—putting pressure on margins and CAPEX planning.

Maintaining diplomatic ties, stakeholder engagement and local investments reduces expropriation/operational-halt risk; Hydro’s 2024 community and license-related provisions equaled ~0.4% of revenue.

- Upstream exposure: metals ~22% of raw-material spend (2023)

- 2022–2024: >15% of mining-policy reforms increased royalties/processing rules

- 2024 community/license provisions ≈0.4% of Hydro revenue

Global Defense and Infrastructure Spending

Rising NATO and EU defense budgets—NATO allies plan collective defense spending above 2% of GDP, with EU green infrastructure investment targets of €312 billion (2024–2027)—increase demand for lightweight aluminum, favoring Hydro’s products in aerospace and transport.

Political mandates for onshore supply chains in Europe and North America align with Hydro’s localized production, supporting revenue resilience as governments prioritize domestic sourcing.

Friend-shoring trends and government procurement programs create opportunities for Hydro to win multi-year, government-backed contracts, strengthening long-term order books and cash flow visibility.

- EU green investment target €312bn (2024–27) boosts aluminum demand

- NATO 2% GDP defense spending raise supports aerospace aluminum

- Local sourcing mandates favor Hydro’s Europe/North America footprint

- Friend-shoring opens path to long-term government contracts

Tariffs, resource nationalism and power costs squeeze margins despite state backing

Trade barriers (US tariffs active since 2018; EU duties up to 48.5% in 2023–24) and resource-nationalism (2022–24: >15% mining-policy reforms) risk margin pressure; Brazil supplies ~20–25% upstream volumes. Norwegian state 34.3% stake (2025) supports financing; Hydro reported NOK 12.6bn power costs (2024) and 2024 community provisions ≈0.4% revenue.

| Metric | Value |

|---|---|

| Norwegian state stake (2025) | 34.3% |

| Brazil upstream share | 20–25% |

| Power costs (2024) | NOK 12.6bn |

| Community provisions (2024) | ≈0.4% revenue |

| EU duties peak | up to 48.5% |

What is included in the product

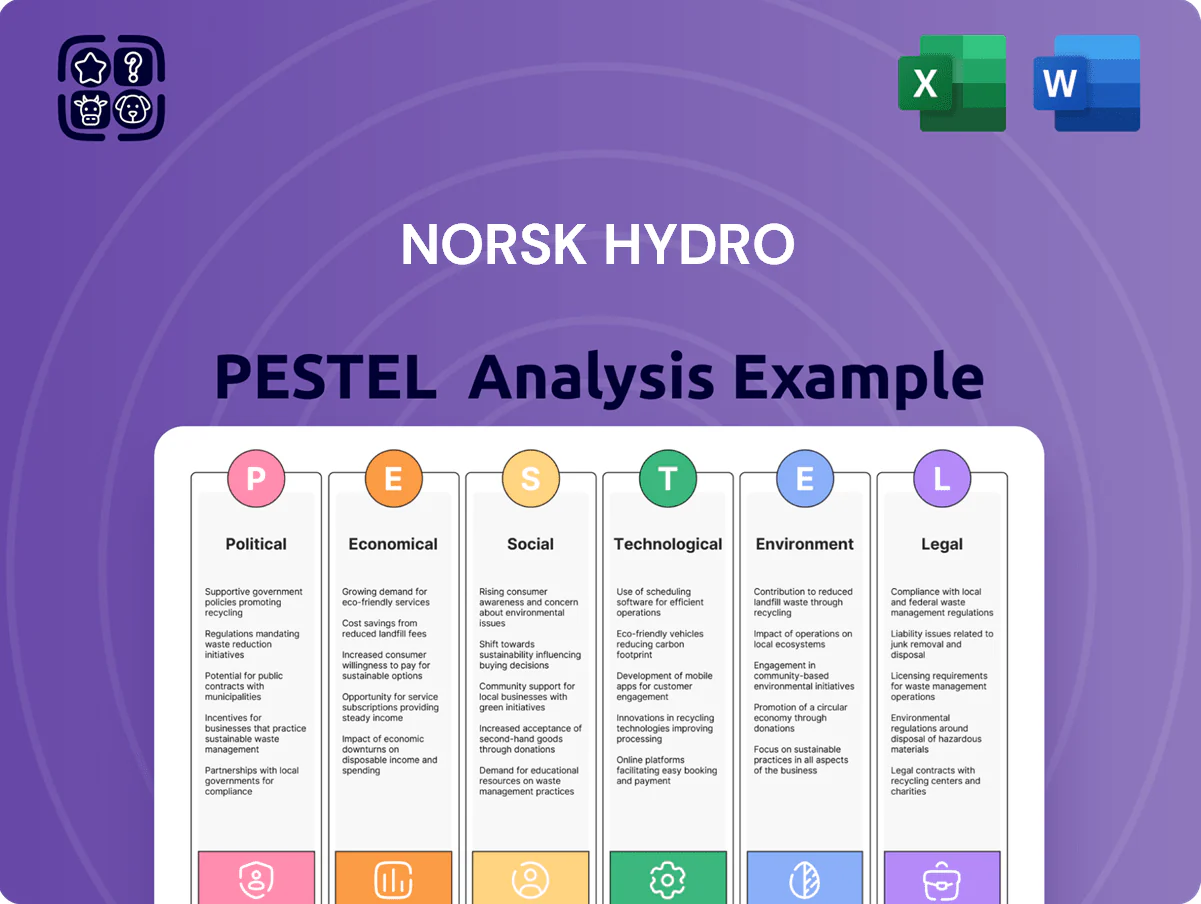

Explores how external macro-environmental factors uniquely affect Norsk Hydro across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current market and regulatory dynamics relevant to its industry and regions.

A concise, shareable PESTLE summary tailored to Norsk Hydro that highlights regulatory, market, and geopolitical risks and opportunities for quick inclusion in presentations or team planning sessions.

Economic factors

Volatility in LME Aluminum Prices

Norsk Hydro's revenue closely tracks LME aluminum prices, which swung between $1,900–$2,600/ton in 2024 amid supply tightness and Chinese demand shifts, directly affecting top-line performance.

Demand from automotive and construction cycles drives premiums; in 2024 auto aluminum demand rose ~3% while construction steel-to-aluminum substitution pushed regional premiums up to $200–$450/ton.

Hydro employs hedging and fixed-price contracts covering a significant portion of production—management reported ~40–60% hedged volumes in 2024—to stabilize margins during volatile LME moves.

Energy Market Integration and Price Trends

Energy accounts for roughly 20-30% of primary aluminum production costs, making Hydro’s captive hydropower—≈13 TWh annual generation capacity in 2024—a major cost advantage; European wholesale power prices averaged about €120/MWh in 2022-23 but eased to ~€70-90/MWh in 2024, while gas-driven volatility and renewable intermittency keep spot swings large, impacting non-integrated smelter margins; Hydro’s ability to sell surplus power (sold ~3 TWh in 2024) creates an important revenue hedge against metal price downturns.

Global Inflation and Operational Costs

Persistent global inflation raised Hydro's input costs in 2024: energy and raw material prices (caustic soda up ~18% YoY) and freight surged, pressuring margins and lifting cash production cost per tonne by an estimated $15–25 versus 2023.

Hydro accelerated internal improvement programs and announced cost-cutting targets aiming to save NOK 3–4 billion by 2025 to defend its position on the global cost curve.

Higher interest rates in 2024 pushed weighted average cost of capital estimates above pre-2022 levels, increasing financing costs for decarbonization and planned recycling expansions and delaying some CAPEX timing.

Currency Exchange Rate Fluctuations

As a global exporter, Hydro faces FX exposure between NOK, USD and EUR; about 85% of aluminum is priced in USD while 2024 reported ~40% of operating costs in NOK and ~10% in BRL, creating translation and transaction risk.

Active hedging reduced 2025 realized FX volatility; a 10% NOK depreciation vs USD would lift reported EBITDA by ~5–7% but raise local production costs in Norway.

- ~85% sales in USD

- ~40% costs in NOK, ~10% in BRL

- 10% NOK move → ~5–7% EBITDA impact

- Requires active currency hedging and pricing strategies

Circular Economy and Recycling Market Growth

Economic shifts to a circular economy have raised aluminum scrap value; Hydro reported recycled metal sales contributing ~15% of volumes in 2024, with global scrap premiums up ~18% year-on-year.

Investing in advanced sorting tech boosts margins on post-consumer scrap; Hydro’s recycling EBITDA margins improved by ~250 basis points in 2024 after automation upgrades.

Price premiums for certified low-carbon brands like CIRCAL and REDUXA reached $200–400/t in 2024, signaling stronger market valuation of sustainability.

- Scrap-driven revenue growth: ~15% of volumes (2024)

- Scrap premiums: +18% YoY (2024)

- Recycling margin uplift: +250 bps post-tech (2024)

- Low-carbon premium: $200–400/t (CIRCAL/REDUXA, 2024)

Aluminium margins hinge on LME, energy costs, FX and rising low‑carbon/scrap premiums

Aluminum revenue closely follows LME (2024 range $1,900–$2,600/t); energy (≈13 TWh captive, sold ~3 TWh) and input inflation raised cash costs ~$15–25/t in 2024; ~85% sales USD vs ~40% costs NOK/~10% BRL causing FX sensitivity (10% NOK move → ~5–7% EBITDA); recycling ≈15% volumes with +18% scrap premiums and low-carbon premiums $200–400/t.

| Metric | 2024 |

|---|---|

| LME range | $1,900–$2,600/t |

| Captive hydrogen | ≈13 TWh (sold ~3 TWh) |

| Hedged volumes | 40–60% |

| Recycling share | ≈15% |

| Scrap premium YoY | +18% |

| Cost rise vs 2023 | $15–25/t |

| FX mix | ~85% sales USD; ~40% costs NOK; ~10% BRL |

| Low-carbon premium | $200–400/t |

What You See Is What You Get

Norsk Hydro PESTLE Analysis

The preview shown here is the exact Norsk Hydro PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Explore how geopolitical shifts, regulatory pressures, and decarbonization trends are reshaping Norsk Hydro’s outlook—our concise PESTLE highlights the most consequential external forces and their strategic implications. Purchase the full PESTLE for a complete, actionable analysis that investors, strategists, and consultants can use immediately to inform decisions and mitigate risks.

Political factors

Geopolitical Trade Barriers and Tariffs

Geopolitical trade protectionism—notably US Section 232 tariffs and recent EU anti-dumping measures—reshapes global aluminum flows and can raise input costs; US tariffs on aluminum (2018) remain active while the EU imposed duties of up to 48.5% on some imports in 2023-24. Norsk Hydro must adapt to shifting trade alliances and regional blocs that affect bauxite and primary metal movement, risking margin pressure. Political stability in Brazil is critical, where Hydro’s Alunorte refinery and Paragominas mine supply a significant share of its alumina; disruptions there could impact roughly 20–25% of its upstream volumes.

European Green Deal and Carbon Border Adjustment Mechanism

As an EU-based producer, Hydro benefits from the Carbon Border Adjustment Mechanism (CBAM) in force from late 2025, which taxed high-carbon imports and increased demand for low-carbon aluminum; Hydro reported 2025 low-carbon premium volumes up ~18% YoY, supporting a 2025 EBITDA margin uplift of ~1.2 percentage points. Political shifts in Brussels on industrial subsidies and green aid—including €20–30 billion/state aid frameworks in 2024–25—directly affect Hydro's investment capacity for decarbonization projects. Continued EU support for energy transition reduces financing costs for Hydro's €1.1bn planned green smelter upgrades through 2026, while potential subsidy retrenchment could raise capital costs and delay projects.

Norwegian State Ownership and Energy Policy

The Norwegian state holds a 34.3% direct stake in Norsk Hydro ASA (2025), anchoring strategic alignment and governance stability; state control aids access to favorable long-term financing and policy influence. Government rulings on hydropower concessions and regulated domestic industrial power prices directly affect smelting margins—Hydro reported NOK 12.6 billion power-related costs in 2024. Political pressure to preserve roughly 7,000 Norwegian jobs often tempers shutdowns despite global cost pressures.

Resource Nationalism in Emerging Markets

Resource nationalism elevates risk for Hydro’s upstream operations: 2024 saw 15% of global mining policy reforms target royalties and local processing, affecting Hydro’s sourcing in South America and Africa where metals contributed ~22% of its raw-material spend in 2023.

Political shifts can trigger higher taxes or local-processing mandates—Argentina, Peru and Zambia introduced tougher mineral codes between 2022–2024—putting pressure on margins and CAPEX planning.

Maintaining diplomatic ties, stakeholder engagement and local investments reduces expropriation/operational-halt risk; Hydro’s 2024 community and license-related provisions equaled ~0.4% of revenue.

- Upstream exposure: metals ~22% of raw-material spend (2023)

- 2022–2024: >15% of mining-policy reforms increased royalties/processing rules

- 2024 community/license provisions ≈0.4% of Hydro revenue

Global Defense and Infrastructure Spending

Rising NATO and EU defense budgets—NATO allies plan collective defense spending above 2% of GDP, with EU green infrastructure investment targets of €312 billion (2024–2027)—increase demand for lightweight aluminum, favoring Hydro’s products in aerospace and transport.

Political mandates for onshore supply chains in Europe and North America align with Hydro’s localized production, supporting revenue resilience as governments prioritize domestic sourcing.

Friend-shoring trends and government procurement programs create opportunities for Hydro to win multi-year, government-backed contracts, strengthening long-term order books and cash flow visibility.

- EU green investment target €312bn (2024–27) boosts aluminum demand

- NATO 2% GDP defense spending raise supports aerospace aluminum

- Local sourcing mandates favor Hydro’s Europe/North America footprint

- Friend-shoring opens path to long-term government contracts

Tariffs, resource nationalism and power costs squeeze margins despite state backing

Trade barriers (US tariffs active since 2018; EU duties up to 48.5% in 2023–24) and resource-nationalism (2022–24: >15% mining-policy reforms) risk margin pressure; Brazil supplies ~20–25% upstream volumes. Norwegian state 34.3% stake (2025) supports financing; Hydro reported NOK 12.6bn power costs (2024) and 2024 community provisions ≈0.4% revenue.

| Metric | Value |

|---|---|

| Norwegian state stake (2025) | 34.3% |

| Brazil upstream share | 20–25% |

| Power costs (2024) | NOK 12.6bn |

| Community provisions (2024) | ≈0.4% revenue |

| EU duties peak | up to 48.5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Norsk Hydro across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current market and regulatory dynamics relevant to its industry and regions.

A concise, shareable PESTLE summary tailored to Norsk Hydro that highlights regulatory, market, and geopolitical risks and opportunities for quick inclusion in presentations or team planning sessions.

Economic factors

Volatility in LME Aluminum Prices

Norsk Hydro's revenue closely tracks LME aluminum prices, which swung between $1,900–$2,600/ton in 2024 amid supply tightness and Chinese demand shifts, directly affecting top-line performance.

Demand from automotive and construction cycles drives premiums; in 2024 auto aluminum demand rose ~3% while construction steel-to-aluminum substitution pushed regional premiums up to $200–$450/ton.

Hydro employs hedging and fixed-price contracts covering a significant portion of production—management reported ~40–60% hedged volumes in 2024—to stabilize margins during volatile LME moves.

Energy Market Integration and Price Trends

Energy accounts for roughly 20-30% of primary aluminum production costs, making Hydro’s captive hydropower—≈13 TWh annual generation capacity in 2024—a major cost advantage; European wholesale power prices averaged about €120/MWh in 2022-23 but eased to ~€70-90/MWh in 2024, while gas-driven volatility and renewable intermittency keep spot swings large, impacting non-integrated smelter margins; Hydro’s ability to sell surplus power (sold ~3 TWh in 2024) creates an important revenue hedge against metal price downturns.

Global Inflation and Operational Costs

Persistent global inflation raised Hydro's input costs in 2024: energy and raw material prices (caustic soda up ~18% YoY) and freight surged, pressuring margins and lifting cash production cost per tonne by an estimated $15–25 versus 2023.

Hydro accelerated internal improvement programs and announced cost-cutting targets aiming to save NOK 3–4 billion by 2025 to defend its position on the global cost curve.

Higher interest rates in 2024 pushed weighted average cost of capital estimates above pre-2022 levels, increasing financing costs for decarbonization and planned recycling expansions and delaying some CAPEX timing.

Currency Exchange Rate Fluctuations

As a global exporter, Hydro faces FX exposure between NOK, USD and EUR; about 85% of aluminum is priced in USD while 2024 reported ~40% of operating costs in NOK and ~10% in BRL, creating translation and transaction risk.

Active hedging reduced 2025 realized FX volatility; a 10% NOK depreciation vs USD would lift reported EBITDA by ~5–7% but raise local production costs in Norway.

- ~85% sales in USD

- ~40% costs in NOK, ~10% in BRL

- 10% NOK move → ~5–7% EBITDA impact

- Requires active currency hedging and pricing strategies

Circular Economy and Recycling Market Growth

Economic shifts to a circular economy have raised aluminum scrap value; Hydro reported recycled metal sales contributing ~15% of volumes in 2024, with global scrap premiums up ~18% year-on-year.

Investing in advanced sorting tech boosts margins on post-consumer scrap; Hydro’s recycling EBITDA margins improved by ~250 basis points in 2024 after automation upgrades.

Price premiums for certified low-carbon brands like CIRCAL and REDUXA reached $200–400/t in 2024, signaling stronger market valuation of sustainability.

- Scrap-driven revenue growth: ~15% of volumes (2024)

- Scrap premiums: +18% YoY (2024)

- Recycling margin uplift: +250 bps post-tech (2024)

- Low-carbon premium: $200–400/t (CIRCAL/REDUXA, 2024)

Aluminium margins hinge on LME, energy costs, FX and rising low‑carbon/scrap premiums

Aluminum revenue closely follows LME (2024 range $1,900–$2,600/t); energy (≈13 TWh captive, sold ~3 TWh) and input inflation raised cash costs ~$15–25/t in 2024; ~85% sales USD vs ~40% costs NOK/~10% BRL causing FX sensitivity (10% NOK move → ~5–7% EBITDA); recycling ≈15% volumes with +18% scrap premiums and low-carbon premiums $200–400/t.

| Metric | 2024 |

|---|---|

| LME range | $1,900–$2,600/t |

| Captive hydrogen | ≈13 TWh (sold ~3 TWh) |

| Hedged volumes | 40–60% |

| Recycling share | ≈15% |

| Scrap premium YoY | +18% |

| Cost rise vs 2023 | $15–25/t |

| FX mix | ~85% sales USD; ~40% costs NOK; ~10% BRL |

| Low-carbon premium | $200–400/t |

What You See Is What You Get

Norsk Hydro PESTLE Analysis

The preview shown here is the exact Norsk Hydro PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.