Hysan Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

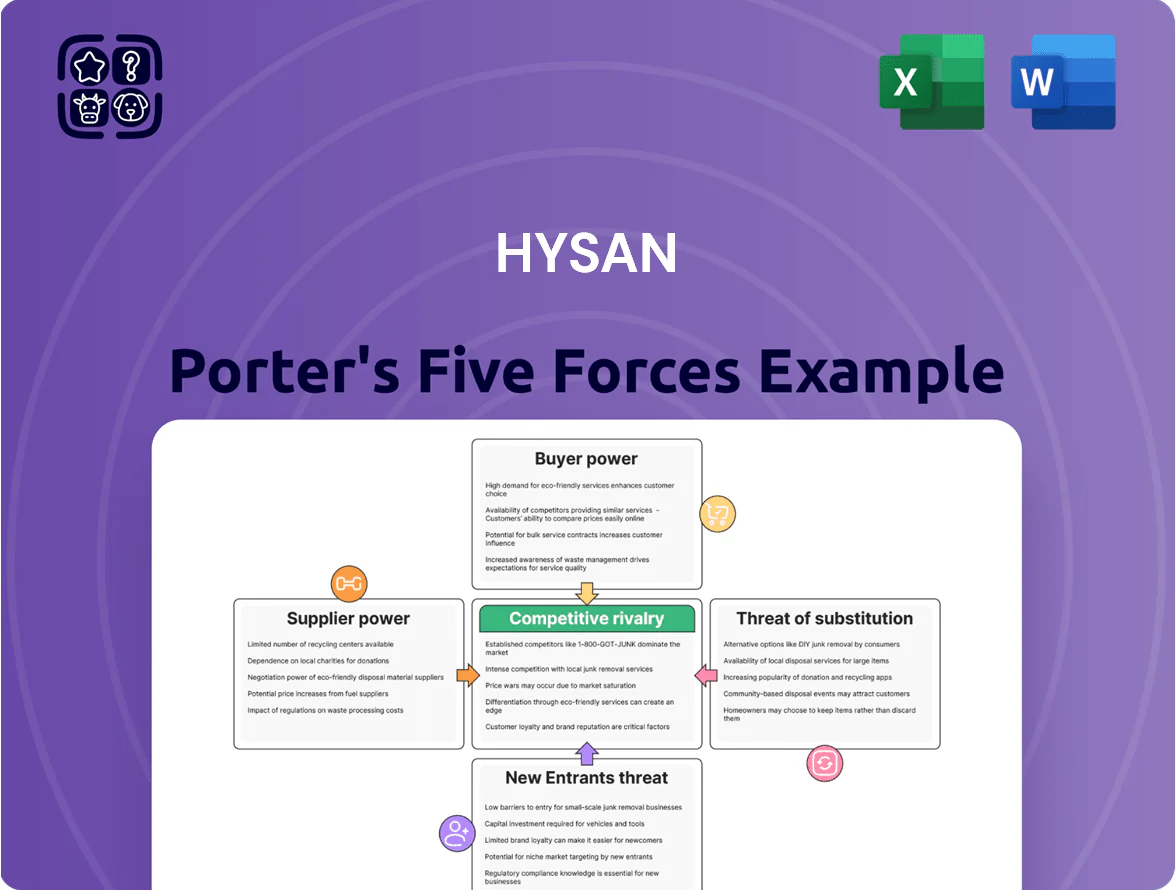

Hysan’s Porter's Five Forces snapshot highlights moderate buyer power, constrained supplier leverage, significant rivalry from peers, muted threat of substitutes, and entry barriers shaped by prime Hong Kong real estate—impacting margins and growth potential.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hysan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Government Control of Land Supply

The Hong Kong government controls new land supply via auctions and lease changes, giving it strong supplier power over developers like Hysan. By end-2025, available land in Causeway Bay is virtually exhausted, so the government can command high premiums—recent 2024 land bids averaged HKD 25,000–40,000 per sq ft in prime zones. Scarcity forces Hysan to pay steep prices or prioritize redevelopment of its existing 2.1m sq ft portfolio to expand.

Construction and Labor Costs

Construction firms and specialized labor providers hold moderate bargaining power for Hysan due to steady demand for high-end sustainable projects in Hong Kong; Tier-1 contractors command 2025 rate premiums about 8–12% above pre-2020 levels. Rising material costs—steel up ~22% YoY and concrete mixes ~14% in 2025—and a 15% shortage of technical construction workers have kept development budgets elevated, so Hysan must secure long-term contracts with top contractors to avoid schedule slips and >5% cost overruns.

Financial Institutions and Capital Markets

As a capital-intensive landlord, Hysan depends on banks and bond markets for funding large developments and refurbishments; in 2025 Hong Kong base rates rose to ~4.75%, pushing A- to BBB borrowing costs up 150–250bps and raising project hurdle rates.

Financial institutions exert bargaining power via covenants, tenor and pricing of credit facilities; Hysan’s strong 2024 net debt/EBITDA ~1.5x and S&P A- equivalent profile give it flexibility to shop lenders and issue HKD bonds at tighter spreads.

Utility and Energy Providers

Utility and energy providers in Hong Kong—largely monopolies or duopolies like CLP Power Hong Kong and HK Electric—wield strong supplier power over Hysan because electricity, water and district cooling are essential inputs.

Hysan’s target of carbon neutrality by 2025 raises dependence on green tariffs and onsite renewable investment; for example, green electricity premiums of 5–12% and HK’s 2024 levy increases can cut NOI on malls and offices by several percentage points.

Any energy-price swing or tighter emissions rules (HK’s 2030 carbon intensity targets, 2024 fuel levy changes) directly compress operating margins and raise capex for retrofits and PPA contracts.

- Major suppliers: CLP, HK Electric — limited alternatives

- Green tariff premium: ~5–12% (market range)

- Carbon neutrality target: Hysan 2025 — raises PPA/CapEx needs

- Energy cost volatility: can reduce NOI by multiple % points

Technological and Smart Building Vendors

The integration of AI and IoT across Lee Gardens has increased Hysan’s reliance on specialized tech vendors who deliver smart building platforms, analytics, and tenant apps that drive higher rents and occupancy.

These vendors supply critical infrastructure—edge sensors, cloud analytics, BMS integrations—with sector contracts often 5–7 years, creating high switching costs and steady revenue for suppliers.

In 2024 Hysan reported tech-enabled rent premiums ~3–5%, highlighting suppliers’ leverage over service levels and pricing.

- Dependency: AI/IoT core to differentiation

- Contracts: 5–7 year typical terms

- Switching cost: high due to integration

- Impact: 3–5% rent premium (2024)

Rising supplier power: land, materials, tariffs and rates squeeze Hong Kong real estate margins

Suppliers exert strong power: government land controls push 2024–25 prime land bids to HKD 25,000–40,000/sq ft; utilities (CLP, HK Electric) are near-monopolies with green tariffs +5–12%; construction rates +8–12% vs pre-2020, materials: steel +22% YoY, concrete +14% (2025); funding costs rose ~150–250bps with HK rates ~4.75%; AI/IoT vendors yield 3–5% rent premium, contracts 5–7 years.

| Item | 2024–25 |

|---|---|

| Land bids | HKD 25k–40k/sq ft |

| Green tariff | +5–12% |

| Construction premium | +8–12% |

| Steel/concrete | +22% / +14% |

| HK base rate | ~4.75% |

| Debt spread rise | 150–250 bps |

| IoT rent premium | 3–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Hysan that uncovers competitive intensity, buyer and supplier power, entry barriers, substitution threats, and strategic levers to protect market share and profitability.

Hysan Porter’s Five Forces condensed into a single, slide-ready snapshot—quickly identify competitive pressures and actionable strategic levers to relieve pain points across leasing, tenant mix, and development planning.

Customers Bargaining Power

Luxury Retail Brand Leverage

Corporate Office Tenant Demands

Hybrid work and flight-to-quality let tenants demand flexible, sustainable offices; a global 2024 CBRE survey found 62% of firms prioritize ESG and wellness when choosing offices.

Hysan’s 2025 portfolio already holds WELL/LEED-equivalent ratings across 80% of office GFA, so multinationals press for higher amenities and green leases.

Tenants negotiate flexible terms—shorter cores, turnover clauses—impacting Hysan’s rent reversion: Hong Kong Grade A vacancy rose to 6.8% in 2024, upping tenant bargaining power.

Consumer Spending Patterns

The ultimate customers of Hysan’s retail tenants—local shoppers and inbound tourists—drive turnover rents; in 2025 cross-border arrivals to Hong Kong recovered to ~70% of 2019 levels by Q1, lifting retail sales by 18% year-on-year and boosting footfall in Hysan’s Causeway Bay assets.

If consumer confidence falls, tenants can push for rent relief or shorter leases; during 2022–24 rent relief requests rose ~30%, so a renewed dip would shift bargaining power toward occupiers and pressure Hysan’s turnover-rent revenue mix.

Availability of Alternative Districts

The rise of decentralized districts like Kai Tak and new hubs expanded Grade-A office and retail stock in Hong Kong by about 6% in 2024, giving tenants more relocation options and stronger negotiation power at lease renewal.

Hysan stresses Lee Gardens’ integrated community, lifestyle amenities, and higher footfall—rent premiums there stayed ~10–15% above city average in 2024—to retain tenants.

- 2024 Grade-A supply +6%

- Lee Gardens rent premium ~10–15%

- Tenants gain leverage on renewals

Residential Tenant Mobility

Hysan’s residential tenants are highly mobile and rent-sensitive across Hong Kong Island, with global talent inflows boosting demand by ~4–6% year-over-year to end-2025 but facing many luxury alternatives in Mid-Levels and Southside.

To sustain >95% occupancy and justify 10–15% rent premiums, Hysan must deliver superior property management, amenities, and community programs that reduce churn and shorten vacancy days.

- Mobile, rent-sensitive tenant pool

- Global talent lift ~4–6% demand (2025)

- Competition: Mid-Levels, Southside luxury stock

- Target: >95% occupancy; 10–15% premium

Luxury giants boost footfall and rents; Hysan holds premium with >95% occupancy

| Metric | Value |

|---|---|

| Footfall share | ~40% |

| High-street rent share | ~30% |

| Grade-A supply change (2024) | +6% |

| Vacancy (2024) | 6.8% |

| Retail sales growth (Q1 2025) | +18% |

Full Version Awaits

Hysan Porter's Five Forces Analysis

This preview shows the exact Hysan Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Hysan’s Porter's Five Forces snapshot highlights moderate buyer power, constrained supplier leverage, significant rivalry from peers, muted threat of substitutes, and entry barriers shaped by prime Hong Kong real estate—impacting margins and growth potential.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hysan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Government Control of Land Supply

The Hong Kong government controls new land supply via auctions and lease changes, giving it strong supplier power over developers like Hysan. By end-2025, available land in Causeway Bay is virtually exhausted, so the government can command high premiums—recent 2024 land bids averaged HKD 25,000–40,000 per sq ft in prime zones. Scarcity forces Hysan to pay steep prices or prioritize redevelopment of its existing 2.1m sq ft portfolio to expand.

Construction and Labor Costs

Construction firms and specialized labor providers hold moderate bargaining power for Hysan due to steady demand for high-end sustainable projects in Hong Kong; Tier-1 contractors command 2025 rate premiums about 8–12% above pre-2020 levels. Rising material costs—steel up ~22% YoY and concrete mixes ~14% in 2025—and a 15% shortage of technical construction workers have kept development budgets elevated, so Hysan must secure long-term contracts with top contractors to avoid schedule slips and >5% cost overruns.

Financial Institutions and Capital Markets

As a capital-intensive landlord, Hysan depends on banks and bond markets for funding large developments and refurbishments; in 2025 Hong Kong base rates rose to ~4.75%, pushing A- to BBB borrowing costs up 150–250bps and raising project hurdle rates.

Financial institutions exert bargaining power via covenants, tenor and pricing of credit facilities; Hysan’s strong 2024 net debt/EBITDA ~1.5x and S&P A- equivalent profile give it flexibility to shop lenders and issue HKD bonds at tighter spreads.

Utility and Energy Providers

Utility and energy providers in Hong Kong—largely monopolies or duopolies like CLP Power Hong Kong and HK Electric—wield strong supplier power over Hysan because electricity, water and district cooling are essential inputs.

Hysan’s target of carbon neutrality by 2025 raises dependence on green tariffs and onsite renewable investment; for example, green electricity premiums of 5–12% and HK’s 2024 levy increases can cut NOI on malls and offices by several percentage points.

Any energy-price swing or tighter emissions rules (HK’s 2030 carbon intensity targets, 2024 fuel levy changes) directly compress operating margins and raise capex for retrofits and PPA contracts.

- Major suppliers: CLP, HK Electric — limited alternatives

- Green tariff premium: ~5–12% (market range)

- Carbon neutrality target: Hysan 2025 — raises PPA/CapEx needs

- Energy cost volatility: can reduce NOI by multiple % points

Technological and Smart Building Vendors

The integration of AI and IoT across Lee Gardens has increased Hysan’s reliance on specialized tech vendors who deliver smart building platforms, analytics, and tenant apps that drive higher rents and occupancy.

These vendors supply critical infrastructure—edge sensors, cloud analytics, BMS integrations—with sector contracts often 5–7 years, creating high switching costs and steady revenue for suppliers.

In 2024 Hysan reported tech-enabled rent premiums ~3–5%, highlighting suppliers’ leverage over service levels and pricing.

- Dependency: AI/IoT core to differentiation

- Contracts: 5–7 year typical terms

- Switching cost: high due to integration

- Impact: 3–5% rent premium (2024)

Rising supplier power: land, materials, tariffs and rates squeeze Hong Kong real estate margins

Suppliers exert strong power: government land controls push 2024–25 prime land bids to HKD 25,000–40,000/sq ft; utilities (CLP, HK Electric) are near-monopolies with green tariffs +5–12%; construction rates +8–12% vs pre-2020, materials: steel +22% YoY, concrete +14% (2025); funding costs rose ~150–250bps with HK rates ~4.75%; AI/IoT vendors yield 3–5% rent premium, contracts 5–7 years.

| Item | 2024–25 |

|---|---|

| Land bids | HKD 25k–40k/sq ft |

| Green tariff | +5–12% |

| Construction premium | +8–12% |

| Steel/concrete | +22% / +14% |

| HK base rate | ~4.75% |

| Debt spread rise | 150–250 bps |

| IoT rent premium | 3–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Hysan that uncovers competitive intensity, buyer and supplier power, entry barriers, substitution threats, and strategic levers to protect market share and profitability.

Hysan Porter’s Five Forces condensed into a single, slide-ready snapshot—quickly identify competitive pressures and actionable strategic levers to relieve pain points across leasing, tenant mix, and development planning.

Customers Bargaining Power

Luxury Retail Brand Leverage

Corporate Office Tenant Demands

Hybrid work and flight-to-quality let tenants demand flexible, sustainable offices; a global 2024 CBRE survey found 62% of firms prioritize ESG and wellness when choosing offices.

Hysan’s 2025 portfolio already holds WELL/LEED-equivalent ratings across 80% of office GFA, so multinationals press for higher amenities and green leases.

Tenants negotiate flexible terms—shorter cores, turnover clauses—impacting Hysan’s rent reversion: Hong Kong Grade A vacancy rose to 6.8% in 2024, upping tenant bargaining power.

Consumer Spending Patterns

The ultimate customers of Hysan’s retail tenants—local shoppers and inbound tourists—drive turnover rents; in 2025 cross-border arrivals to Hong Kong recovered to ~70% of 2019 levels by Q1, lifting retail sales by 18% year-on-year and boosting footfall in Hysan’s Causeway Bay assets.

If consumer confidence falls, tenants can push for rent relief or shorter leases; during 2022–24 rent relief requests rose ~30%, so a renewed dip would shift bargaining power toward occupiers and pressure Hysan’s turnover-rent revenue mix.

Availability of Alternative Districts

The rise of decentralized districts like Kai Tak and new hubs expanded Grade-A office and retail stock in Hong Kong by about 6% in 2024, giving tenants more relocation options and stronger negotiation power at lease renewal.

Hysan stresses Lee Gardens’ integrated community, lifestyle amenities, and higher footfall—rent premiums there stayed ~10–15% above city average in 2024—to retain tenants.

- 2024 Grade-A supply +6%

- Lee Gardens rent premium ~10–15%

- Tenants gain leverage on renewals

Residential Tenant Mobility

Hysan’s residential tenants are highly mobile and rent-sensitive across Hong Kong Island, with global talent inflows boosting demand by ~4–6% year-over-year to end-2025 but facing many luxury alternatives in Mid-Levels and Southside.

To sustain >95% occupancy and justify 10–15% rent premiums, Hysan must deliver superior property management, amenities, and community programs that reduce churn and shorten vacancy days.

- Mobile, rent-sensitive tenant pool

- Global talent lift ~4–6% demand (2025)

- Competition: Mid-Levels, Southside luxury stock

- Target: >95% occupancy; 10–15% premium

Luxury giants boost footfall and rents; Hysan holds premium with >95% occupancy

| Metric | Value |

|---|---|

| Footfall share | ~40% |

| High-street rent share | ~30% |

| Grade-A supply change (2024) | +6% |

| Vacancy (2024) | 6.8% |

| Retail sales growth (Q1 2025) | +18% |

Full Version Awaits

Hysan Porter's Five Forces Analysis

This preview shows the exact Hysan Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use.