Hytera Communications Corporation Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

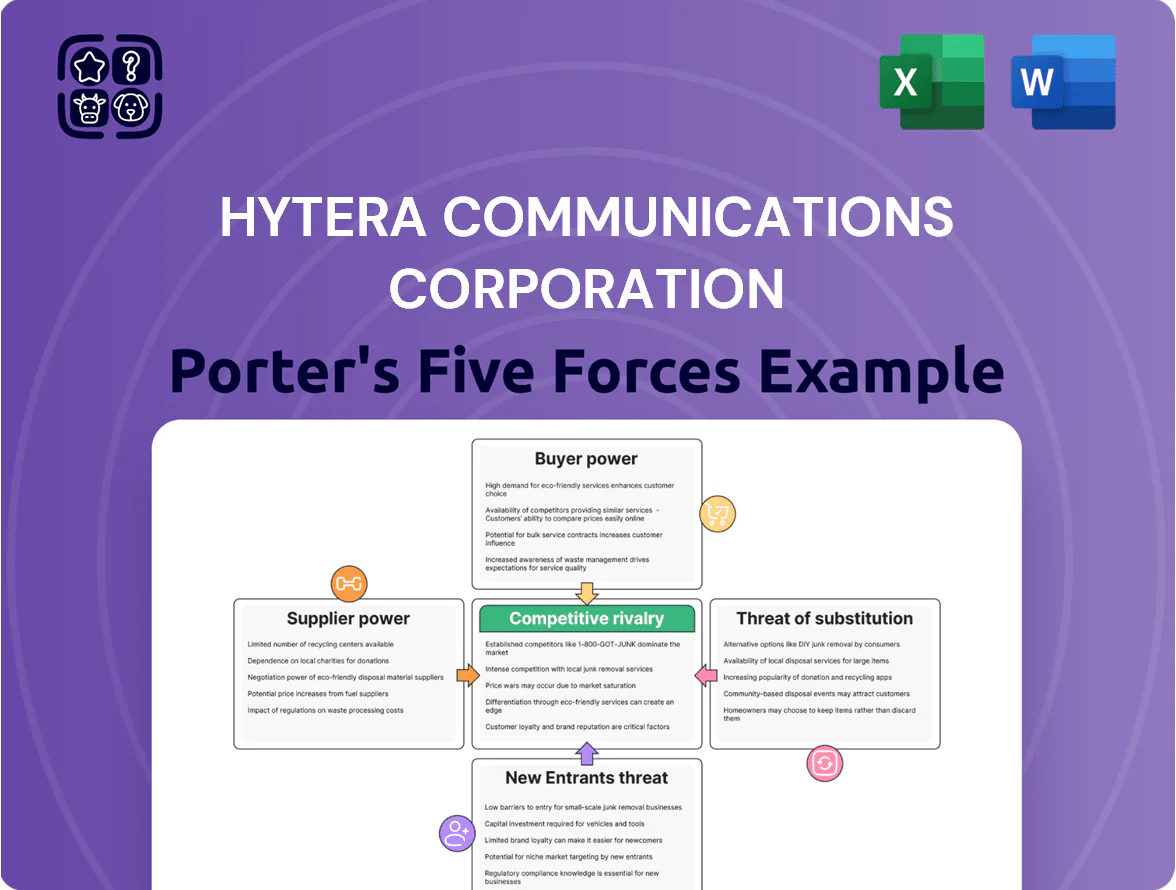

Hytera faces intense rivalry from global radio vendors, moderate supplier leverage for specialized components, and growing buyer power as customers demand integrated digital solutions and lower costs.

New entrants face high barriers due to spectrum regulation and tech IP, while substitutes like cellular broadband pose an escalating long-term threat to traditional PMR markets.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hytera Communications Corporation’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor and Chipset Dependency

The production of advanced digital radios and broadband trunking systems depends on high-performance semiconductors and chipsets; Hytera reported in 2024 that components account for roughly 28% of COGS, up from 24% in 2021. Despite increased domestic sourcing in China, about 70–80% of cutting-edge RF and baseband IC capacity remains concentrated among a handful of global suppliers, giving them pricing and delivery leverage during supply shocks or geopolitical strain.

Geopolitical Supply Chain Constraints

As a major Chinese firm, Hytera faces US and EU export controls since 2019 that restrict access to certain Western semiconductors and encryption tech, raising supplier power; in 2024 Hytera reported supply-cost increases of ~6–9% tied to sourcing constraints.

Alternative suppliers who can meet compliance demands charge premiums—often 10–25% higher—or require special licensing, forcing Hytera to mix domestic sourcing and premium imports to keep product quality for export markets.

Raw Material Price Volatility

Hytera’s rugged radios need high-grade plastics, specialty antenna metals, and rare earths for batteries; global rare-earth prices rose ~45% in 2023–2024, pushing component costs up and squeezing margins.

Commodity swings—copper +20% and ABS plastics +12% in 2024—raise procurement risk; Hytera’s need to meet public-safety durability standards limits switching to lower-cost suppliers without losing certification.

Proprietary Software and Protocol Licensing

Hytera relies on third-party software stacks and must comply with DMR, TETRA, and PDT standards, so IP holders for these protocols wield strong supplier power due to essential interoperability needs.

Hytera owns substantial IP but still pays royalties/licensing and engages standards bodies; in 2024 Hytera reported R&D spend of RMB 1.8bn (≈USD 250m), underscoring investment to reduce dependency.

Stable licensor relationships matter: disruption or fee hikes could raise COGS and slow certifications, impacting margins and time-to-market.

- Third-party protocol IP creates dependency risk

- DMR/TETRA/PDT compliance essential for market access

- 2024 R&D RMB 1.8bn to internalize stacks

- Licensing disputes could raise COGS and delay launches

Supplier Fragmentation for Non-Core Components

For generic electronic components and accessories, supplier fragmentation is high: over 70% of Hytera’s low-value parts come from thousands of small-to-medium suppliers, cutting their bargaining power and letting Hytera secure volume discounts and flexible terms.

Hytera’s global scale—reported 2024 revenue ~RMB 12.4 billion—lets it aggregate buys, driving 3–6% cost savings in these categories to offset higher-margin specialized tech suppliers.

- Fragmented market: thousands of SMEs supply generic parts

- Supplier power: low for non-core components

- Negotiation leverage: volume discounts, diverse vendor base

- Impact: 3–6% cost saving on generic components vs. specialized suppliers

Supply concentration, rising commodity costs and export controls squeeze IC margins

Suppliers of advanced RF/baseband ICs, rare earths, and protocol IP hold high leverage—70–80% of cutting-edge IC capacity concentrated among few vendors; 2024 component share ≈28% of COGS and R&D was RMB 1.8bn. Geopolitical export controls since 2019 raised sourcing costs ~6–9% in 2024; commodity swings (rare earths +45%, copper +20% in 2023–24) further squeeze margins, while fragmented generic suppliers cut costs 3–6%.

| Metric | Value (2024) |

|---|---|

| Component share of COGS | ~28% |

| R&D spend | RMB 1.8bn (~USD 250m) |

| IC capacity concentration | 70–80% |

| Sourcing cost increase | ~6–9% |

| Rare-earth price change | +45% (2023–24) |

| Copper price change | +20% (2024) |

| Generic parts savings | 3–6% |

What is included in the product

Tailored exclusively for Hytera Communications Corporation, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitution risks, and barriers to entry, highlighting disruptive threats and strategic levers that influence its pricing, profitability, and market position.

A compact Porter's Five Forces snapshot for Hytera Communications that highlights competitive pressures and regulatory risks—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

High Concentration of Government and Public Safety Buyers

A substantial share of Hytera’s 2024 revenue—about 45% of RMB 7.8 billion (≈USD 1.1 billion)—comes from government and public safety tenders for police, fire, and EMS, concentrating buying power. These buyers set strict specs and run formal competitive bids, forcing price cuts and long-term service commitments; Hytera reported 12% margin compression on large tender contracts in 2023. This buyer mix raises renewal and pricing pressure, so customer-driven terms shape product design and margins.

High Switching Costs and Infrastructure Lock-in

Once a client installs Hytera’s trunking systems or radio infrastructure, switching costs—hardware replacement, retraining, and spectrum reconfiguration—often exceed millions; for example, municipal fleet upgrades averaged $2.1M in 2024, creating strong vendor lock-in that reduces buyer bargaining power mid-life cycle.

Still, during initial procurement or full-system replacements every 8–12 years, buyers regain leverage: tenders and RFPs see price concessions up to 12% as agencies threaten migration to competitors like Motorola Solutions or Tait.

Demand for Interoperability and Open Standards

Modern customers demand interoperability and open standards to avoid vendor lock-in, raising their bargaining power; 62% of enterprise buyers in 2024 preferred multi-vendor radio ecosystems, per ETSI/IHS estimates. This lets buyers mix Hytera terminals with third-party networks, reducing switching costs and forcing Hytera to compete on unit price and feature set rather than system exclusivity. In 2025 Hytera saw device-margin pressure, with gross margin on terminals down ~180 basis points year-over-year as open-standard sales rose.

Price Sensitivity in Commercial and Industrial Sectors

Customers in hospitality, logistics, and property management prioritize cost: surveys show 62% cite price as the top purchase driver versus 18% citing mission-critical reliability; Hytera faces easy switching to sub-$200 consumer apps or <$500 unbranded radios that meet basic needs.

To hold share Hytera must match price points or prove a clear ROI—e.g., lower total cost of ownership by 15–25% over three years through longer lifecycles and service contracts.

- High price sensitivity: 62% prioritize cost

- Low reliability needs vs public safety: 18% prioritize reliability

- Switching risk: consumer apps <$200, unbranded radios <$500

- Retention levers: competitive pricing, 15–25% TCO savings

Technological Savvy of Professional Users

Decision-makers—often financial professionals and radio-engineering teams—run rigorous performance tests and demand detailed benchmarks, so Hytera can’t rely on marketing-led price premiums; 2024 product R&D spend was about CNY 1.8bn (≈USD 250m) to stay competitive.

The buyers’ ability to perform deep technical audits and side-by-side real-world comparisons forces Hytera to sustain high R&D and quality testing to justify contracts and margins.

- Highly technical buyers

- Benchmark-driven negotiations

- R&D spend CNY 1.8bn (2024)

- Low tolerance for price premiums

Tender-driven pricing vs. upgrade lock-in: open standards slash margins, R&D fights back

Buyers hold mixed power: 45% of 2024 revenue from concentrated public-safety tenders forces price and long-service concessions, while installed-system switching costs (avg municipal upgrade $2.1M in 2024) create mid-life lock-in; however 62% buyer preference for multi-vendor/open standards (2024 ETSI/IHS) and price-sensitive commercial sectors push down terminal margins ~180 bps in 2025, forcing R&D-driven parity (CNY 1.8bn in 2024).

| Metric | Value |

|---|---|

| 2024 revenue from tenders | 45% |

| Municipal upgrade avg | RMB 2.1M |

| Open-standard buyers | 62% |

| Terminal margin change 2025 | -180 bps |

| R&D 2024 | CNY 1.8bn |

Preview Before You Purchase

Hytera Communications Corporation Porter's Five Forces Analysis

This preview shows the exact Hytera Communications Corporation Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full ready-to-use file—fully formatted and downloadable the moment you buy.

You’re previewing the final version: the same professionally written analysis that becomes instantly available to you after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Hytera faces intense rivalry from global radio vendors, moderate supplier leverage for specialized components, and growing buyer power as customers demand integrated digital solutions and lower costs.

New entrants face high barriers due to spectrum regulation and tech IP, while substitutes like cellular broadband pose an escalating long-term threat to traditional PMR markets.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hytera Communications Corporation’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor and Chipset Dependency

The production of advanced digital radios and broadband trunking systems depends on high-performance semiconductors and chipsets; Hytera reported in 2024 that components account for roughly 28% of COGS, up from 24% in 2021. Despite increased domestic sourcing in China, about 70–80% of cutting-edge RF and baseband IC capacity remains concentrated among a handful of global suppliers, giving them pricing and delivery leverage during supply shocks or geopolitical strain.

Geopolitical Supply Chain Constraints

As a major Chinese firm, Hytera faces US and EU export controls since 2019 that restrict access to certain Western semiconductors and encryption tech, raising supplier power; in 2024 Hytera reported supply-cost increases of ~6–9% tied to sourcing constraints.

Alternative suppliers who can meet compliance demands charge premiums—often 10–25% higher—or require special licensing, forcing Hytera to mix domestic sourcing and premium imports to keep product quality for export markets.

Raw Material Price Volatility

Hytera’s rugged radios need high-grade plastics, specialty antenna metals, and rare earths for batteries; global rare-earth prices rose ~45% in 2023–2024, pushing component costs up and squeezing margins.

Commodity swings—copper +20% and ABS plastics +12% in 2024—raise procurement risk; Hytera’s need to meet public-safety durability standards limits switching to lower-cost suppliers without losing certification.

Proprietary Software and Protocol Licensing

Hytera relies on third-party software stacks and must comply with DMR, TETRA, and PDT standards, so IP holders for these protocols wield strong supplier power due to essential interoperability needs.

Hytera owns substantial IP but still pays royalties/licensing and engages standards bodies; in 2024 Hytera reported R&D spend of RMB 1.8bn (≈USD 250m), underscoring investment to reduce dependency.

Stable licensor relationships matter: disruption or fee hikes could raise COGS and slow certifications, impacting margins and time-to-market.

- Third-party protocol IP creates dependency risk

- DMR/TETRA/PDT compliance essential for market access

- 2024 R&D RMB 1.8bn to internalize stacks

- Licensing disputes could raise COGS and delay launches

Supplier Fragmentation for Non-Core Components

For generic electronic components and accessories, supplier fragmentation is high: over 70% of Hytera’s low-value parts come from thousands of small-to-medium suppliers, cutting their bargaining power and letting Hytera secure volume discounts and flexible terms.

Hytera’s global scale—reported 2024 revenue ~RMB 12.4 billion—lets it aggregate buys, driving 3–6% cost savings in these categories to offset higher-margin specialized tech suppliers.

- Fragmented market: thousands of SMEs supply generic parts

- Supplier power: low for non-core components

- Negotiation leverage: volume discounts, diverse vendor base

- Impact: 3–6% cost saving on generic components vs. specialized suppliers

Supply concentration, rising commodity costs and export controls squeeze IC margins

Suppliers of advanced RF/baseband ICs, rare earths, and protocol IP hold high leverage—70–80% of cutting-edge IC capacity concentrated among few vendors; 2024 component share ≈28% of COGS and R&D was RMB 1.8bn. Geopolitical export controls since 2019 raised sourcing costs ~6–9% in 2024; commodity swings (rare earths +45%, copper +20% in 2023–24) further squeeze margins, while fragmented generic suppliers cut costs 3–6%.

| Metric | Value (2024) |

|---|---|

| Component share of COGS | ~28% |

| R&D spend | RMB 1.8bn (~USD 250m) |

| IC capacity concentration | 70–80% |

| Sourcing cost increase | ~6–9% |

| Rare-earth price change | +45% (2023–24) |

| Copper price change | +20% (2024) |

| Generic parts savings | 3–6% |

What is included in the product

Tailored exclusively for Hytera Communications Corporation, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitution risks, and barriers to entry, highlighting disruptive threats and strategic levers that influence its pricing, profitability, and market position.

A compact Porter's Five Forces snapshot for Hytera Communications that highlights competitive pressures and regulatory risks—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

High Concentration of Government and Public Safety Buyers

A substantial share of Hytera’s 2024 revenue—about 45% of RMB 7.8 billion (≈USD 1.1 billion)—comes from government and public safety tenders for police, fire, and EMS, concentrating buying power. These buyers set strict specs and run formal competitive bids, forcing price cuts and long-term service commitments; Hytera reported 12% margin compression on large tender contracts in 2023. This buyer mix raises renewal and pricing pressure, so customer-driven terms shape product design and margins.

High Switching Costs and Infrastructure Lock-in

Once a client installs Hytera’s trunking systems or radio infrastructure, switching costs—hardware replacement, retraining, and spectrum reconfiguration—often exceed millions; for example, municipal fleet upgrades averaged $2.1M in 2024, creating strong vendor lock-in that reduces buyer bargaining power mid-life cycle.

Still, during initial procurement or full-system replacements every 8–12 years, buyers regain leverage: tenders and RFPs see price concessions up to 12% as agencies threaten migration to competitors like Motorola Solutions or Tait.

Demand for Interoperability and Open Standards

Modern customers demand interoperability and open standards to avoid vendor lock-in, raising their bargaining power; 62% of enterprise buyers in 2024 preferred multi-vendor radio ecosystems, per ETSI/IHS estimates. This lets buyers mix Hytera terminals with third-party networks, reducing switching costs and forcing Hytera to compete on unit price and feature set rather than system exclusivity. In 2025 Hytera saw device-margin pressure, with gross margin on terminals down ~180 basis points year-over-year as open-standard sales rose.

Price Sensitivity in Commercial and Industrial Sectors

Customers in hospitality, logistics, and property management prioritize cost: surveys show 62% cite price as the top purchase driver versus 18% citing mission-critical reliability; Hytera faces easy switching to sub-$200 consumer apps or <$500 unbranded radios that meet basic needs.

To hold share Hytera must match price points or prove a clear ROI—e.g., lower total cost of ownership by 15–25% over three years through longer lifecycles and service contracts.

- High price sensitivity: 62% prioritize cost

- Low reliability needs vs public safety: 18% prioritize reliability

- Switching risk: consumer apps <$200, unbranded radios <$500

- Retention levers: competitive pricing, 15–25% TCO savings

Technological Savvy of Professional Users

Decision-makers—often financial professionals and radio-engineering teams—run rigorous performance tests and demand detailed benchmarks, so Hytera can’t rely on marketing-led price premiums; 2024 product R&D spend was about CNY 1.8bn (≈USD 250m) to stay competitive.

The buyers’ ability to perform deep technical audits and side-by-side real-world comparisons forces Hytera to sustain high R&D and quality testing to justify contracts and margins.

- Highly technical buyers

- Benchmark-driven negotiations

- R&D spend CNY 1.8bn (2024)

- Low tolerance for price premiums

Tender-driven pricing vs. upgrade lock-in: open standards slash margins, R&D fights back

Buyers hold mixed power: 45% of 2024 revenue from concentrated public-safety tenders forces price and long-service concessions, while installed-system switching costs (avg municipal upgrade $2.1M in 2024) create mid-life lock-in; however 62% buyer preference for multi-vendor/open standards (2024 ETSI/IHS) and price-sensitive commercial sectors push down terminal margins ~180 bps in 2025, forcing R&D-driven parity (CNY 1.8bn in 2024).

| Metric | Value |

|---|---|

| 2024 revenue from tenders | 45% |

| Municipal upgrade avg | RMB 2.1M |

| Open-standard buyers | 62% |

| Terminal margin change 2025 | -180 bps |

| R&D 2024 | CNY 1.8bn |

Preview Before You Purchase

Hytera Communications Corporation Porter's Five Forces Analysis

This preview shows the exact Hytera Communications Corporation Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full ready-to-use file—fully formatted and downloadable the moment you buy.

You’re previewing the final version: the same professionally written analysis that becomes instantly available to you after payment.