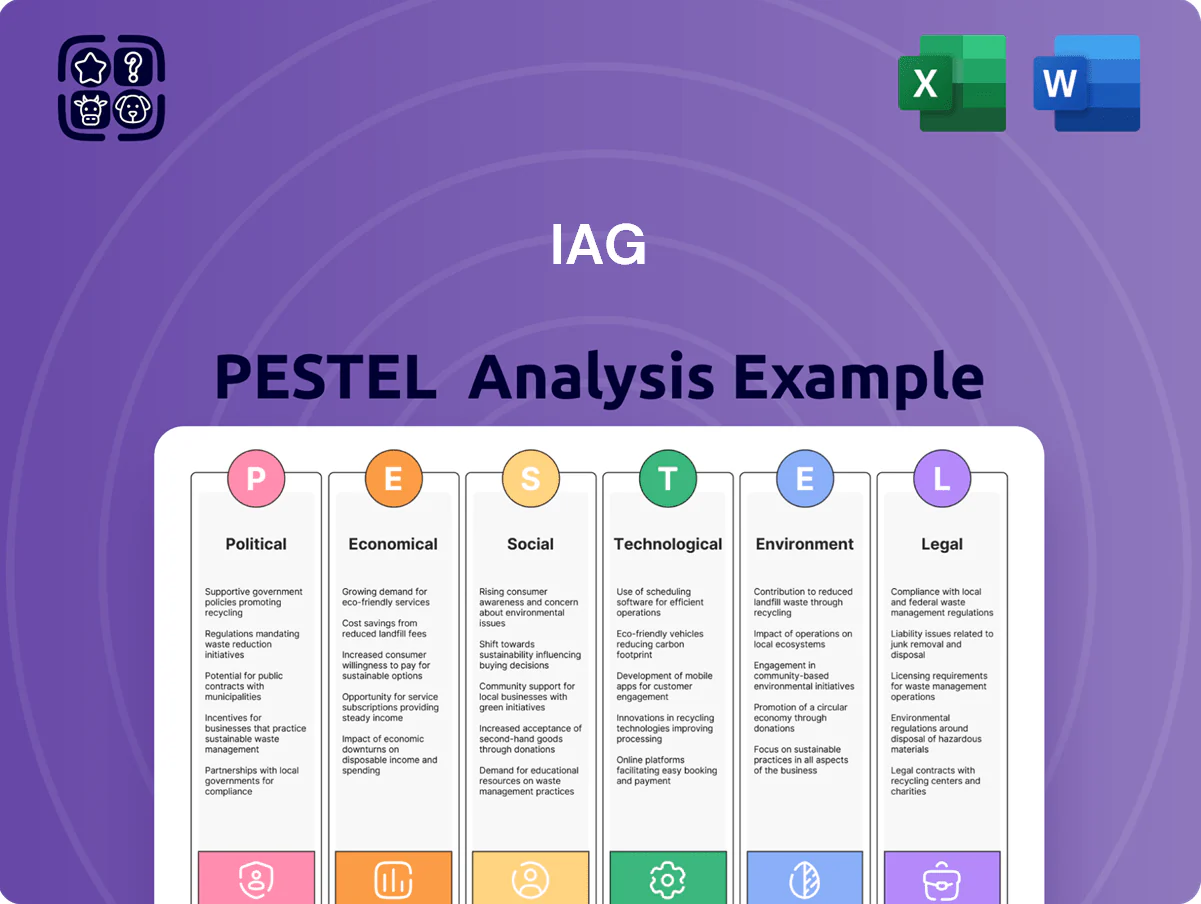

IAG PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a competitive advantage with our tailored PESTLE Analysis for IAG—uncover how political shifts, economic trends, social changes, technological advances, legal risks, and environmental pressures will shape its strategy and value. Ideal for investors, strategists, and advisors, this concise, actionable report is fully editable and ready for boardroom use. Purchase the full version now to access the complete, data-driven insights you need.

Political factors

Government Reinsurance Pool Initiatives

The Australian government’s cyclone and flood reinsurance pool, active through 2025, provides a government-backed layer covering ~A$10–15bn of catastrophe risk, helping lower premiums in northern Queensland and NT where IAG’s exposure is highest.

For IAG this reduces capital volatility and reinsurance costs—IAG reported catastrophe expense sensitivity of ~A$200–300m per major event—supporting underwriting capacity and social licence in vulnerable regions.

Bilateral Trade and Supply Chain Policy

Geopolitical tensions and trade policies between Australia and key partners (China 27% of goods imports 2024, US 12%) affect costs of imported repair materials, contributing to parts inflation that lifted motor/home claim costs ~6.5% yoy in 2023–24.

By end-2025, govt. supply‑chain diversification and A$1.2bn manufacturing incentives aim to reduce import dependency, potentially lowering claim severity if domestic supply scales.

IAG must monitor political shifts and potential tariffs—e.g., a 5–10% tariff could raise replacement parts costs materially and increase claims payouts—altering underwriting and reserves.

National Security and Cyber Governance

The Australian government has increased funding for cyber resilience, with the 2024 Cyber Security Strategy committing A$1.67 billion through 2030, raising expectations for insurers like IAG to harden critical infrastructure and incident response.

Heightened political focus on state-sponsored threats has driven mandates on data sovereignty and mandatory information sharing via the Joint Cyber Security Centre network, affecting IAG’s data handling and breach reporting timelines.

IAG’s alignment with these national security priorities is crucial to retain regulatory favor and avoid penalties; in 2023 Australian regulators issued over A$40m in fines across sectors for cyber compliance failures, underscoring operational and financial risks.

Disaster Response and Mitigation Funding

Political decisions on federal and state funding for disaster mitigation infrastructure, including recent bipartisan packages allocating over USD 40 billion for resilience through 2024–25, reshape IAG’s long-term risk models and capital planning.

By 2025 there is stronger political appetite for proactive community resilience spending versus post-event recovery, reducing projected claim frequency and severity in IAG’s actuarial scenarios.

IAG actively lobbies policymakers and partners on resilience funding, which management projects could lower insured losses by up to 15% in high-risk coastal regions over the next decade.

- USD 40bn+ resilience funding 2024–25

- Projected 15% reduction in coastal insured losses

- Shift from recovery to mitigation policy favored politically

Taxation Policy and Insurance Levies

The ongoing debate over reforming state-based insurance levies in 2025 poses material risk to IAG, with levies adding up to 20–30% to premiums in some Australian states and contributing to a national uninsured gap estimated at 1.2 million households.

IAG is actively lobbying for levy transparency and legislative reform to prevent levies from inflating consumer prices and reducing coverage, particularly in high-risk coastal and flood zones where premium increases have been most acute.

Failure to reform could compress IAG’s margin if levies are shifted onto insurers or sustain reduced uptake of comprehensive policies, impacting gross written premium growth already reporting mid-single-digit increases in 2024–25.

- Levies can add 20–30% to premiums

- ~1.2 million households potentially underinsured nationally

- IAG lobbying for transparency and reform

- High-risk zones face largest premium inflation

IAG: Reinsurance & resilience cut coastal losses ~15% but tariffs, levies raise costs

Government catastrophe reinsurance (A$10–15bn through 2025) and USD40bn+ resilience funding (2024–25) lower IAG’s capital volatility and expected coastal losses (~15% reduction projected), while trade tensions (China 27% imports) and potential 5–10% tariffs increase parts-driven claim severity; cyber funding A$1.67bn to 2030 raises compliance costs amid >A$40m fines in 2023, and state insurance levies (adding 20–30% to premiums) risk reducing coverage for ~1.2m households.

| Metric | Value |

|---|---|

| Catastrophe reinsurance | A$10–15bn (to 2025) |

| Resilience funding | USD40bn+ (2024–25) |

| Projected coastal loss reduction | ~15% |

| China share of imports | 27% (2024) |

| Cyber funding | A$1.67bn (to 2030) |

| Regulatory fines (2023) | >A$40m |

| Insurance levies impact | +20–30% premiums; ~1.2m underinsured |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect IAG, with each section backed by current data and trends to identify threats and opportunities.

A concise, PESTLE-organized brief of IAG that can be dropped into presentations or strategy sessions to streamline discussions on regulatory, economic, social, technological, and environmental risks.

Economic factors

Interest Rate Environment and Investment Income

By end-2025 the RBA’s stabilized cash rate near 4.10% has given IAG a more predictable fixed-income landscape, enabling investment yields on the premium float to lift returns—IAG reported ~A$1.15bn investment income in FY2024–25, helping offset combined operating ratio pressures. Sustained higher rates versus the prior decade boost net investment margin but may slow GDP growth in Australia/New Zealand (IMF 2025 forecasts: AUS 1.8%, NZ 1.6%), moderating demand for new policies.

Claims Inflation and Cost of Goods

Persistent inflationary pressures on labor and raw materials, notably automotive parts and building supplies, squeezed IAG’s margins into 2025, with average claim severity rising about 9–12% year-on-year and repair costs per motor claim up roughly AUD 450 since 2023.

While headline CPI eased to ~3.5% in 2024–25, construction and repair-sector inflation ran nearer 6–8%, pushing up the average cost per claim and loss ratios in home and motor portfolios.

IAG deploys dynamic pricing models and automated claims analytics to adjust premiums and restore combined operating ratios; management targets premium adequacy increases in recent rate filings of ~5–10% to offset reinstatement cost inflation.

Household Disposable Income Trends

Australian household disposable incomes remain under pressure into late 2025 after cumulative RBA rate hikes (cash rate peaked at 4.35% in 2024) and CPI running near 4% in 2024–25, reducing real incomes and depressing insurance penetration. Consumers increasingly trade down to higher excesses or lower cover, shifting IAG’s risk mix toward more severe but fewer claims. To retain price-sensitive customers IAG must scale flexible payment plans and tiered product structures, linked to digital underwriting and behavioural pricing. Such moves mitigate lapses amid a tightening household budget environment.

Reinsurance Market Hardening

The global reinsurance market remained disciplined through end-2025, with average reinsurer returns on equity near 12-14% and elevated cost of capital that pushed treaty rates up ~15-25% versus 2021-22, increasing IAG’s catastrophe protection premiums.

Higher reinsurance spend compresses IAG’s underwriting margin unless offset by capital optimisation, retention increases or premium pass-through; favourable treaty terms are therefore pivotal to IAG’s solvency metrics and capacity to write growth in volatile lines.

- Reinsurer RoE ~12-14% (end-2025)

- Treaty rate inflation ~15-25% vs 2021-22

- Impact: higher premiums → need for capital optimisation or consumer price increases

- Reinsurance terms drive IAG’s financial stability and new-business capacity

Labor Market Dynamics and Talent Retention

Tight labor markets in Australia and New Zealand in 2025 push median wages up; Australia’s annual wage growth was ~4.5% year-on-year in 2024, increasing costs for actuarial, data analytics and claims roles.

IAG competes with tech and finance for specialists, raising retention costs and sign-on premiums; churn in data roles is above industry average at ~18% in 2024.

Balancing higher human capital expenses with investments in training and automation is critical to sustain operational efficiency and technical capability.

- Wage growth ~4.5% (Australia 2024)

- Specialist churn ~18% (2024)

- Higher sign-on/retention spend vs prior years

Higher rates boost IAG investment but rising claims, reinsurance squeeze margins

Higher cash rates (~4.1% end‑2025) lifted IAG investment income (~A$1.15bn FY2024–25) but dampen GDP (AUS 1.8%, NZ 1.6% IMF 2025), reducing premium growth; claim severity rose ~9–12% with motor repair costs +AUD450 vs 2023; reinsurance treaty rates +15–25% vs 2021–22 (reinsurer RoE ~12–14%), pressuring underwriting margins and driving premium increases and capital optimisation.

| Metric | Value |

|---|---|

| Cash rate (RBA) | ~4.1% (end‑2025) |

| IAG investment income | ~A$1.15bn (FY2024–25) |

| GDP forecast | AUS 1.8%, NZ 1.6% (IMF 2025) |

| Claim severity rise | ~9–12% YoY |

| Motor repair cost change | +AUD450 vs 2023 |

| Treaty rate inflation | +15–25% vs 2021–22 |

| Reinsurer RoE | ~12–14% (end‑2025) |

Same Document Delivered

IAG PESTLE Analysis

The preview shown here is the exact IAG PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

What you see in the preview is the final file: complete content, headings, and visuals included with no placeholders or teasers.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a competitive advantage with our tailored PESTLE Analysis for IAG—uncover how political shifts, economic trends, social changes, technological advances, legal risks, and environmental pressures will shape its strategy and value. Ideal for investors, strategists, and advisors, this concise, actionable report is fully editable and ready for boardroom use. Purchase the full version now to access the complete, data-driven insights you need.

Political factors

Government Reinsurance Pool Initiatives

The Australian government’s cyclone and flood reinsurance pool, active through 2025, provides a government-backed layer covering ~A$10–15bn of catastrophe risk, helping lower premiums in northern Queensland and NT where IAG’s exposure is highest.

For IAG this reduces capital volatility and reinsurance costs—IAG reported catastrophe expense sensitivity of ~A$200–300m per major event—supporting underwriting capacity and social licence in vulnerable regions.

Bilateral Trade and Supply Chain Policy

Geopolitical tensions and trade policies between Australia and key partners (China 27% of goods imports 2024, US 12%) affect costs of imported repair materials, contributing to parts inflation that lifted motor/home claim costs ~6.5% yoy in 2023–24.

By end-2025, govt. supply‑chain diversification and A$1.2bn manufacturing incentives aim to reduce import dependency, potentially lowering claim severity if domestic supply scales.

IAG must monitor political shifts and potential tariffs—e.g., a 5–10% tariff could raise replacement parts costs materially and increase claims payouts—altering underwriting and reserves.

National Security and Cyber Governance

The Australian government has increased funding for cyber resilience, with the 2024 Cyber Security Strategy committing A$1.67 billion through 2030, raising expectations for insurers like IAG to harden critical infrastructure and incident response.

Heightened political focus on state-sponsored threats has driven mandates on data sovereignty and mandatory information sharing via the Joint Cyber Security Centre network, affecting IAG’s data handling and breach reporting timelines.

IAG’s alignment with these national security priorities is crucial to retain regulatory favor and avoid penalties; in 2023 Australian regulators issued over A$40m in fines across sectors for cyber compliance failures, underscoring operational and financial risks.

Disaster Response and Mitigation Funding

Political decisions on federal and state funding for disaster mitigation infrastructure, including recent bipartisan packages allocating over USD 40 billion for resilience through 2024–25, reshape IAG’s long-term risk models and capital planning.

By 2025 there is stronger political appetite for proactive community resilience spending versus post-event recovery, reducing projected claim frequency and severity in IAG’s actuarial scenarios.

IAG actively lobbies policymakers and partners on resilience funding, which management projects could lower insured losses by up to 15% in high-risk coastal regions over the next decade.

- USD 40bn+ resilience funding 2024–25

- Projected 15% reduction in coastal insured losses

- Shift from recovery to mitigation policy favored politically

Taxation Policy and Insurance Levies

The ongoing debate over reforming state-based insurance levies in 2025 poses material risk to IAG, with levies adding up to 20–30% to premiums in some Australian states and contributing to a national uninsured gap estimated at 1.2 million households.

IAG is actively lobbying for levy transparency and legislative reform to prevent levies from inflating consumer prices and reducing coverage, particularly in high-risk coastal and flood zones where premium increases have been most acute.

Failure to reform could compress IAG’s margin if levies are shifted onto insurers or sustain reduced uptake of comprehensive policies, impacting gross written premium growth already reporting mid-single-digit increases in 2024–25.

- Levies can add 20–30% to premiums

- ~1.2 million households potentially underinsured nationally

- IAG lobbying for transparency and reform

- High-risk zones face largest premium inflation

IAG: Reinsurance & resilience cut coastal losses ~15% but tariffs, levies raise costs

Government catastrophe reinsurance (A$10–15bn through 2025) and USD40bn+ resilience funding (2024–25) lower IAG’s capital volatility and expected coastal losses (~15% reduction projected), while trade tensions (China 27% imports) and potential 5–10% tariffs increase parts-driven claim severity; cyber funding A$1.67bn to 2030 raises compliance costs amid >A$40m fines in 2023, and state insurance levies (adding 20–30% to premiums) risk reducing coverage for ~1.2m households.

| Metric | Value |

|---|---|

| Catastrophe reinsurance | A$10–15bn (to 2025) |

| Resilience funding | USD40bn+ (2024–25) |

| Projected coastal loss reduction | ~15% |

| China share of imports | 27% (2024) |

| Cyber funding | A$1.67bn (to 2030) |

| Regulatory fines (2023) | >A$40m |

| Insurance levies impact | +20–30% premiums; ~1.2m underinsured |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect IAG, with each section backed by current data and trends to identify threats and opportunities.

A concise, PESTLE-organized brief of IAG that can be dropped into presentations or strategy sessions to streamline discussions on regulatory, economic, social, technological, and environmental risks.

Economic factors

Interest Rate Environment and Investment Income

By end-2025 the RBA’s stabilized cash rate near 4.10% has given IAG a more predictable fixed-income landscape, enabling investment yields on the premium float to lift returns—IAG reported ~A$1.15bn investment income in FY2024–25, helping offset combined operating ratio pressures. Sustained higher rates versus the prior decade boost net investment margin but may slow GDP growth in Australia/New Zealand (IMF 2025 forecasts: AUS 1.8%, NZ 1.6%), moderating demand for new policies.

Claims Inflation and Cost of Goods

Persistent inflationary pressures on labor and raw materials, notably automotive parts and building supplies, squeezed IAG’s margins into 2025, with average claim severity rising about 9–12% year-on-year and repair costs per motor claim up roughly AUD 450 since 2023.

While headline CPI eased to ~3.5% in 2024–25, construction and repair-sector inflation ran nearer 6–8%, pushing up the average cost per claim and loss ratios in home and motor portfolios.

IAG deploys dynamic pricing models and automated claims analytics to adjust premiums and restore combined operating ratios; management targets premium adequacy increases in recent rate filings of ~5–10% to offset reinstatement cost inflation.

Household Disposable Income Trends

Australian household disposable incomes remain under pressure into late 2025 after cumulative RBA rate hikes (cash rate peaked at 4.35% in 2024) and CPI running near 4% in 2024–25, reducing real incomes and depressing insurance penetration. Consumers increasingly trade down to higher excesses or lower cover, shifting IAG’s risk mix toward more severe but fewer claims. To retain price-sensitive customers IAG must scale flexible payment plans and tiered product structures, linked to digital underwriting and behavioural pricing. Such moves mitigate lapses amid a tightening household budget environment.

Reinsurance Market Hardening

The global reinsurance market remained disciplined through end-2025, with average reinsurer returns on equity near 12-14% and elevated cost of capital that pushed treaty rates up ~15-25% versus 2021-22, increasing IAG’s catastrophe protection premiums.

Higher reinsurance spend compresses IAG’s underwriting margin unless offset by capital optimisation, retention increases or premium pass-through; favourable treaty terms are therefore pivotal to IAG’s solvency metrics and capacity to write growth in volatile lines.

- Reinsurer RoE ~12-14% (end-2025)

- Treaty rate inflation ~15-25% vs 2021-22

- Impact: higher premiums → need for capital optimisation or consumer price increases

- Reinsurance terms drive IAG’s financial stability and new-business capacity

Labor Market Dynamics and Talent Retention

Tight labor markets in Australia and New Zealand in 2025 push median wages up; Australia’s annual wage growth was ~4.5% year-on-year in 2024, increasing costs for actuarial, data analytics and claims roles.

IAG competes with tech and finance for specialists, raising retention costs and sign-on premiums; churn in data roles is above industry average at ~18% in 2024.

Balancing higher human capital expenses with investments in training and automation is critical to sustain operational efficiency and technical capability.

- Wage growth ~4.5% (Australia 2024)

- Specialist churn ~18% (2024)

- Higher sign-on/retention spend vs prior years

Higher rates boost IAG investment but rising claims, reinsurance squeeze margins

Higher cash rates (~4.1% end‑2025) lifted IAG investment income (~A$1.15bn FY2024–25) but dampen GDP (AUS 1.8%, NZ 1.6% IMF 2025), reducing premium growth; claim severity rose ~9–12% with motor repair costs +AUD450 vs 2023; reinsurance treaty rates +15–25% vs 2021–22 (reinsurer RoE ~12–14%), pressuring underwriting margins and driving premium increases and capital optimisation.

| Metric | Value |

|---|---|

| Cash rate (RBA) | ~4.1% (end‑2025) |

| IAG investment income | ~A$1.15bn (FY2024–25) |

| GDP forecast | AUS 1.8%, NZ 1.6% (IMF 2025) |

| Claim severity rise | ~9–12% YoY |

| Motor repair cost change | +AUD450 vs 2023 |

| Treaty rate inflation | +15–25% vs 2021–22 |

| Reinsurer RoE | ~12–14% (end‑2025) |

Same Document Delivered

IAG PESTLE Analysis

The preview shown here is the exact IAG PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

What you see in the preview is the final file: complete content, headings, and visuals included with no placeholders or teasers.