IBM Boston Consulting Group Matrix

Actionable Strategy Starts Here

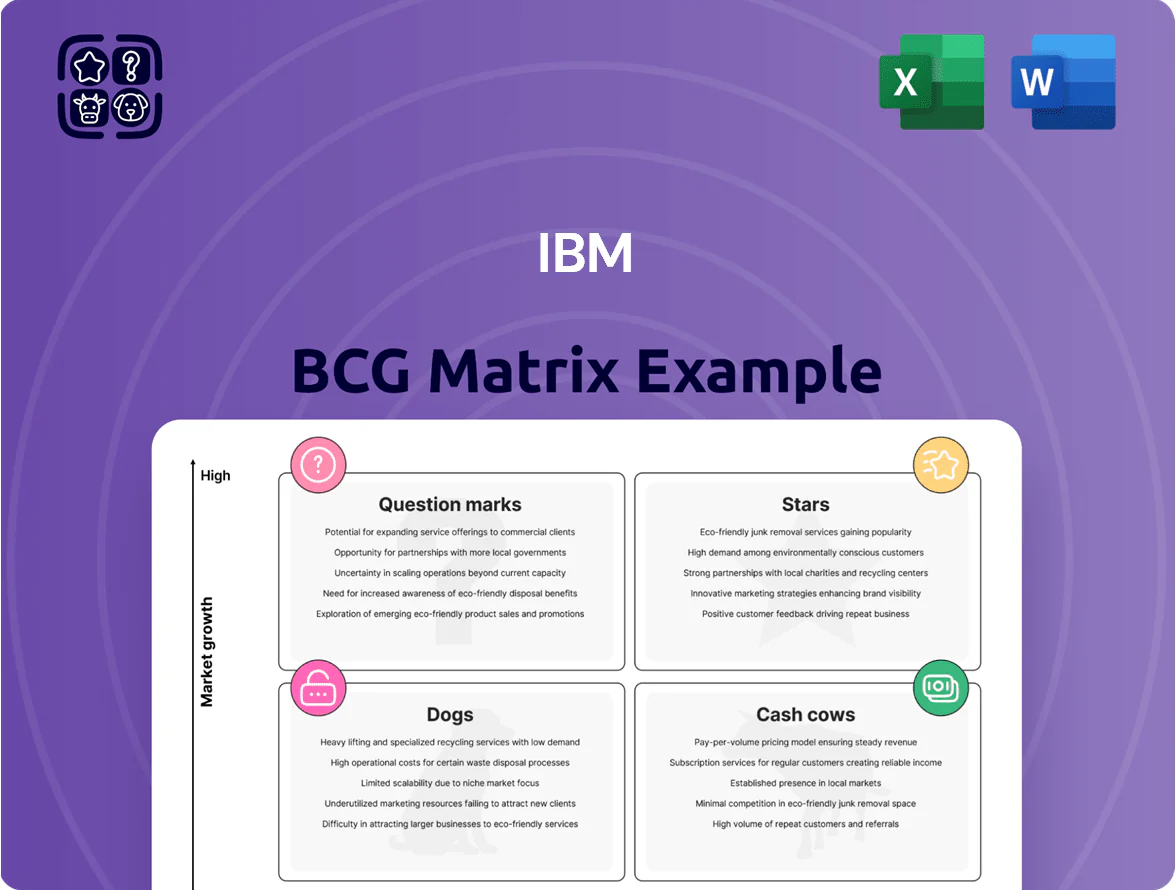

IBM’s BCG Matrix snapshot highlights its mix of mature Cash Cows in legacy IT services, potential Stars in hybrid cloud and AI platforms, Question Marks in emerging edge-computing areas, and a few weaker Dogs from divested hardware lines—offering a strategic snapshot of where cash generation and growth potential intersect. This preview scratches the surface; buy the full BCG Matrix to get quadrant-level data, actionable recommendations, and ready-to-use Word and Excel files that guide capital allocation and product strategy.

Stars

Red Hat and Hybrid Cloud Software

IBM’s hybrid cloud business, anchored by Red Hat, is a Star: double-digit growth with Red Hat revenue climbing 12–14% in 2025 as OpenShift adoption rose to manage multicloud workloads across public and private clouds.

The unit holds a dominant share in open-source enterprise solutions and drove IBM software revenue, with Red Hat contributing roughly $6.3B ARR by year-end 2025.

It needs heavy capital to compete with hyperscalers on R&D and partnerships, yet remains IBM’s primary engine for a software-led transformation and long-term viability.

Enterprise Automation Software

Automation moved into the Star quadrant after IBM integrated HashiCorp and scaled AI workflow tools, hitting growth up to 22% in Q4 2025 and contributing roughly $1.1B incremental revenue in 2025 YTD.

Data and AI Software

Driven by rapid adoption of watsonx, IBM’s Data and AI software unit grew revenue 14–19% in 2025 as enterprises adopted foundation models and data lakehouse architectures, lifting segment sales to about $8.4–9.1 billion for the year.

IBM leads in enterprise AI with a strong position in regulated sectors; governance and trustworthy AI won key contracts in healthcare, finance, and government, accounting for roughly 35% of new deals.

Market competition from hyperscalers and AI startups is intense, so IBM must keep investing—R&D and cloud capex rose ~22% in 2025—to defend share and scale watsonx deployments.

Generative AI Consulting Services

As of late 2025, IBM's generative AI consulting is a Star in the BCG matrix, with a book of business above $10.5 billion for generative-AI projects and annual growth north of 40% as pilots moved to production.

This unit led enterprise transformation share, pulled through IBM software and infrastructure sales, and became a top hiring and marketing priority amid broader consulting headwinds.

- Book: >$10.5B (gen-AI projects)

- Growth: ~40%+ YoY to late 2025

- Role: drives software & infrastructure revenue

- Priority: talent, marketing, production deployments

Cybersecurity and Compliance Tools

IBM’s cybersecurity and compliance tools are a Star: identity management and threat detection growth is driven by complex global threats and rules like the EU AI Act (effective 2024), with IBM holding ~45% market share among Fortune 500 firms and revenue from security software up 12% in 2025 to $5.6B.

AI-driven automation boosts detection-to-response speed, keeping products relevant despite fierce pure-play competition; deep integration across IBM Cloud and hybrid stacks gives a durable edge.

- Star due to rising threats + EU AI Act (2024)

- ~45% share among Fortune 500; security revenue $5.6B in 2025 (+12%)

- AI automation shortens response times; hybrid integration = moat

- Competitive pressure from CrowdStrike, Palo Alto, but IBM ecosystem offsets risk

IBM’s AI & Hybrid Cloud Surge: Strong Growth, $30B+ Opportunity, Heavy R&D Push

IBM’s Stars: hybrid cloud (Red Hat) growing 12–14% in 2025 with ~$6.3B ARR; Data & AI (watsonx) up 14–19% to ~$8.4–9.1B; generative-AI consulting >$10.5B book, ~40%+ growth; security tools $5.6B in 2025 (+12%), ~45% Fortune 500 share; heavy R&D/capex (+22% in 2025) required to defend vs hyperscalers.

| Unit | 2025 Growth | Revenue/Book | Notes |

|---|---|---|---|

| Hybrid cloud (Red Hat) | 12–14% | ~$6.3B ARR | OpenShift multicloud |

| Data & AI (watsonx) | 14–19% | $8.4–9.1B | foundation models, lakehouse |

| Gen‑AI consulting | 40%+ | >$10.5B book | production deployments |

| Security & compliance | 12% | $5.6B | ~45% Fortune 500 share |

What is included in the product

Comprehensive BCG Matrix review of IBM’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page IBM BCG Matrix placing each business unit in a quadrant for quick strategic decisions and presentations

Cash Cows

IBM zSystems Mainframes

The IBM Z mainframe remains the ultimate Cash Cow, generating massive free cash flow from a near-monopoly in mission-critical transaction processing and delivering ~40–50% gross margins on hardware plus recurring maintenance that yields steady operating cash.

In 2025 the z17 cycle lifted infrastructure revenue over 60% in select quarters and helped IBM Systems report a 22% year-over-year revenue bump in H1 2025, underscoring continued demand from banks and governments.

The mainframe market is mature and low-growth, yet high margins and subscription-style maintenance funded $6–8 billion in IBM R&D investments in 2025, including AI and Quantum efforts.

This sticky, high-retention model lets IBM harvest outsized cash with low promotion spend versus cloud-native software, supporting M&A and capital returns without stressing core cash flow.

Transaction Processing Software

Closely tied to IBM mainframes, transaction-processing software delivers steady, high-margin revenue with low growth; IBM reported Z Systems software and middleware revenue roughly flat in 2025, supporting predictable cash flows.

Despite cloud migration, an estimated 60–70% of global interbank transactions still run on IBM middleware, preserving market share and low churn.

In 2025 this annuity income funded dividends and debt service—IBM paid $1.66B quarterly in dividends for FY2025—while needing minimal capex, so management can milk it to fund Stars.

Legacy Middleware and WebSphere

WebSphere and related middleware hold top share in the mature enterprise app-server market, with IBM reporting roughly 40% market share in legacy middleware revenue streams and multi-year enterprise contracts worth an estimated $3–4B in annual support revenue (2024 figures).

These platforms are deeply embedded in large firms, so replacement costs run into hundreds of millions per major client, keeping churn low and profit margins high—operating margins for middleware/support exceed 25%.

Growth is low as workloads shift to container-native stacks like Kubernetes, but IBM channels cash from this cash cow to fund cloud-native investments such as Red Hat OpenShift, which received over $1B in R&D and go-to-market spend in 2024 to accelerate client migration.

Enterprise Data Software and Db2

IBM’s legacy database software, led by Db2, remains a reliable Cash Cow with ~25,000 enterprise customers and heavy presence in finance and insurance, where regulated datasets resist migration, yielding retention rates above 90% and predictable license and maintenance cash flows.

Global growth for traditional relational databases is single-digit; Gartner estimated 6% CAGR for RDBMS to 2025, vs 20%+ for data lakes, but IBM holds a dominant niche share in large enterprises, driving high margins.

That steady profit stream funds IBM’s reinvestment into watsonx.data and modern analytics—IBM reported software cloud and cognitive revenues of $22.2B in FY2024, enabling R&D and go-to-market spend for next-gen data products.

- 25,000 enterprise Db2 customers; >90% retention

- RDBMS CAGR ~6% to 2025; data lakes 20%+

- FY2024 software cloud & cognitive revenues $22.2B

Infrastructure Support and Maintenance

IBM’s Infrastructure Support and Maintenance is a Cash Cow: multi-year contracts across 175+ countries and $19.6B services backlog (2024) yield high margins and low growth, giving steady cash despite product cycles.

Existing infrastructure cuts delivery cost, driving strong free cash flow — IBM reported $13.3B free cash flow in 2024 — and stabilizes credit metrics while funding M&A.

- High margin, low growth

- Multi-year contracts = predictable cash

- $19.6B services backlog (2024)

- $13.3B free cash flow (2024)

- Supports investment-grade rating + M&A

IBM’s cash engines: Z, Middleware, Db2 & Support fuel $13.3B FCF and $1.66B quarterly dividends

IBM cash cows: Z mainframes, WebSphere/middleware, Db2, and Infrastructure Support generate steady, high-margin cash (40–50% gross on Z; middleware/support >25% operating margins), funded $13.3B free cash flow (2024) and supported $1.66B quarterly dividends (FY2025), $19.6B services backlog (2024), ~25,000 Db2 customers (>90% retention).

| Asset | Key metric | 2024–25 fact |

|---|---|---|

| IBM Z | Gross margin | 40–50% |

| Middleware | Op margin | >25% |

| Db2 | Customers/retention | ~25,000 / >90% |

| Services | Backlog / FCF | $19.6B / $13.3B |

| Dividends | Quarterly | $1.66B (FY2025) |

Preview = Final Product

IBM BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just the fully formatted, analysis-ready document designed for strategic clarity and immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

IBM’s BCG Matrix snapshot highlights its mix of mature Cash Cows in legacy IT services, potential Stars in hybrid cloud and AI platforms, Question Marks in emerging edge-computing areas, and a few weaker Dogs from divested hardware lines—offering a strategic snapshot of where cash generation and growth potential intersect. This preview scratches the surface; buy the full BCG Matrix to get quadrant-level data, actionable recommendations, and ready-to-use Word and Excel files that guide capital allocation and product strategy.

Stars

Red Hat and Hybrid Cloud Software

IBM’s hybrid cloud business, anchored by Red Hat, is a Star: double-digit growth with Red Hat revenue climbing 12–14% in 2025 as OpenShift adoption rose to manage multicloud workloads across public and private clouds.

The unit holds a dominant share in open-source enterprise solutions and drove IBM software revenue, with Red Hat contributing roughly $6.3B ARR by year-end 2025.

It needs heavy capital to compete with hyperscalers on R&D and partnerships, yet remains IBM’s primary engine for a software-led transformation and long-term viability.

Enterprise Automation Software

Automation moved into the Star quadrant after IBM integrated HashiCorp and scaled AI workflow tools, hitting growth up to 22% in Q4 2025 and contributing roughly $1.1B incremental revenue in 2025 YTD.

Data and AI Software

Driven by rapid adoption of watsonx, IBM’s Data and AI software unit grew revenue 14–19% in 2025 as enterprises adopted foundation models and data lakehouse architectures, lifting segment sales to about $8.4–9.1 billion for the year.

IBM leads in enterprise AI with a strong position in regulated sectors; governance and trustworthy AI won key contracts in healthcare, finance, and government, accounting for roughly 35% of new deals.

Market competition from hyperscalers and AI startups is intense, so IBM must keep investing—R&D and cloud capex rose ~22% in 2025—to defend share and scale watsonx deployments.

Generative AI Consulting Services

As of late 2025, IBM's generative AI consulting is a Star in the BCG matrix, with a book of business above $10.5 billion for generative-AI projects and annual growth north of 40% as pilots moved to production.

This unit led enterprise transformation share, pulled through IBM software and infrastructure sales, and became a top hiring and marketing priority amid broader consulting headwinds.

- Book: >$10.5B (gen-AI projects)

- Growth: ~40%+ YoY to late 2025

- Role: drives software & infrastructure revenue

- Priority: talent, marketing, production deployments

Cybersecurity and Compliance Tools

IBM’s cybersecurity and compliance tools are a Star: identity management and threat detection growth is driven by complex global threats and rules like the EU AI Act (effective 2024), with IBM holding ~45% market share among Fortune 500 firms and revenue from security software up 12% in 2025 to $5.6B.

AI-driven automation boosts detection-to-response speed, keeping products relevant despite fierce pure-play competition; deep integration across IBM Cloud and hybrid stacks gives a durable edge.

- Star due to rising threats + EU AI Act (2024)

- ~45% share among Fortune 500; security revenue $5.6B in 2025 (+12%)

- AI automation shortens response times; hybrid integration = moat

- Competitive pressure from CrowdStrike, Palo Alto, but IBM ecosystem offsets risk

IBM’s AI & Hybrid Cloud Surge: Strong Growth, $30B+ Opportunity, Heavy R&D Push

IBM’s Stars: hybrid cloud (Red Hat) growing 12–14% in 2025 with ~$6.3B ARR; Data & AI (watsonx) up 14–19% to ~$8.4–9.1B; generative-AI consulting >$10.5B book, ~40%+ growth; security tools $5.6B in 2025 (+12%), ~45% Fortune 500 share; heavy R&D/capex (+22% in 2025) required to defend vs hyperscalers.

| Unit | 2025 Growth | Revenue/Book | Notes |

|---|---|---|---|

| Hybrid cloud (Red Hat) | 12–14% | ~$6.3B ARR | OpenShift multicloud |

| Data & AI (watsonx) | 14–19% | $8.4–9.1B | foundation models, lakehouse |

| Gen‑AI consulting | 40%+ | >$10.5B book | production deployments |

| Security & compliance | 12% | $5.6B | ~45% Fortune 500 share |

What is included in the product

Comprehensive BCG Matrix review of IBM’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page IBM BCG Matrix placing each business unit in a quadrant for quick strategic decisions and presentations

Cash Cows

IBM zSystems Mainframes

The IBM Z mainframe remains the ultimate Cash Cow, generating massive free cash flow from a near-monopoly in mission-critical transaction processing and delivering ~40–50% gross margins on hardware plus recurring maintenance that yields steady operating cash.

In 2025 the z17 cycle lifted infrastructure revenue over 60% in select quarters and helped IBM Systems report a 22% year-over-year revenue bump in H1 2025, underscoring continued demand from banks and governments.

The mainframe market is mature and low-growth, yet high margins and subscription-style maintenance funded $6–8 billion in IBM R&D investments in 2025, including AI and Quantum efforts.

This sticky, high-retention model lets IBM harvest outsized cash with low promotion spend versus cloud-native software, supporting M&A and capital returns without stressing core cash flow.

Transaction Processing Software

Closely tied to IBM mainframes, transaction-processing software delivers steady, high-margin revenue with low growth; IBM reported Z Systems software and middleware revenue roughly flat in 2025, supporting predictable cash flows.

Despite cloud migration, an estimated 60–70% of global interbank transactions still run on IBM middleware, preserving market share and low churn.

In 2025 this annuity income funded dividends and debt service—IBM paid $1.66B quarterly in dividends for FY2025—while needing minimal capex, so management can milk it to fund Stars.

Legacy Middleware and WebSphere

WebSphere and related middleware hold top share in the mature enterprise app-server market, with IBM reporting roughly 40% market share in legacy middleware revenue streams and multi-year enterprise contracts worth an estimated $3–4B in annual support revenue (2024 figures).

These platforms are deeply embedded in large firms, so replacement costs run into hundreds of millions per major client, keeping churn low and profit margins high—operating margins for middleware/support exceed 25%.

Growth is low as workloads shift to container-native stacks like Kubernetes, but IBM channels cash from this cash cow to fund cloud-native investments such as Red Hat OpenShift, which received over $1B in R&D and go-to-market spend in 2024 to accelerate client migration.

Enterprise Data Software and Db2

IBM’s legacy database software, led by Db2, remains a reliable Cash Cow with ~25,000 enterprise customers and heavy presence in finance and insurance, where regulated datasets resist migration, yielding retention rates above 90% and predictable license and maintenance cash flows.

Global growth for traditional relational databases is single-digit; Gartner estimated 6% CAGR for RDBMS to 2025, vs 20%+ for data lakes, but IBM holds a dominant niche share in large enterprises, driving high margins.

That steady profit stream funds IBM’s reinvestment into watsonx.data and modern analytics—IBM reported software cloud and cognitive revenues of $22.2B in FY2024, enabling R&D and go-to-market spend for next-gen data products.

- 25,000 enterprise Db2 customers; >90% retention

- RDBMS CAGR ~6% to 2025; data lakes 20%+

- FY2024 software cloud & cognitive revenues $22.2B

Infrastructure Support and Maintenance

IBM’s Infrastructure Support and Maintenance is a Cash Cow: multi-year contracts across 175+ countries and $19.6B services backlog (2024) yield high margins and low growth, giving steady cash despite product cycles.

Existing infrastructure cuts delivery cost, driving strong free cash flow — IBM reported $13.3B free cash flow in 2024 — and stabilizes credit metrics while funding M&A.

- High margin, low growth

- Multi-year contracts = predictable cash

- $19.6B services backlog (2024)

- $13.3B free cash flow (2024)

- Supports investment-grade rating + M&A

IBM’s cash engines: Z, Middleware, Db2 & Support fuel $13.3B FCF and $1.66B quarterly dividends

IBM cash cows: Z mainframes, WebSphere/middleware, Db2, and Infrastructure Support generate steady, high-margin cash (40–50% gross on Z; middleware/support >25% operating margins), funded $13.3B free cash flow (2024) and supported $1.66B quarterly dividends (FY2025), $19.6B services backlog (2024), ~25,000 Db2 customers (>90% retention).

| Asset | Key metric | 2024–25 fact |

|---|---|---|

| IBM Z | Gross margin | 40–50% |

| Middleware | Op margin | >25% |

| Db2 | Customers/retention | ~25,000 / >90% |

| Services | Backlog / FCF | $19.6B / $13.3B |

| Dividends | Quarterly | $1.66B (FY2025) |

Preview = Final Product

IBM BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just the fully formatted, analysis-ready document designed for strategic clarity and immediate use.