Ibstock Porter's Five Forces Analysis

From Overview to Strategy Blueprint

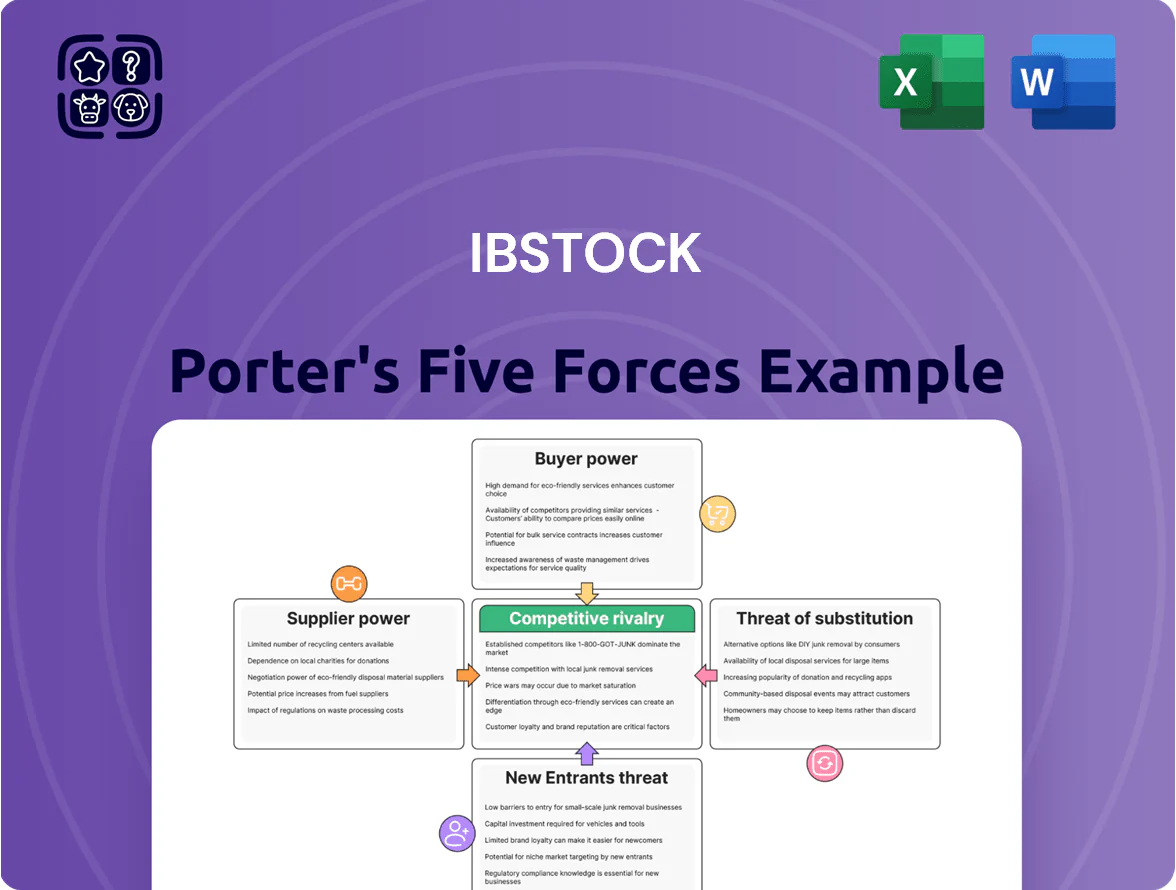

Ibstock faces moderate supplier power and steady buyer demand, while competitive rivalry is intense due to capacity and pricing pressure; substitutes and new entrants remain restrained by capital intensity and regulation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ibstock’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy market volatility and hedging

Natural gas fuels ~70% of Ibstock’s kilns, so exposure to global wholesale price swings is high; UK gas TTF averaged €45/MWh in 2024, up 30% vs 2020, driving raw energy costs.

Ibstock hedges via forwards and swaps covering ~60% of projected consumption, cutting short-term volatility, but the UK’s few major utilities (Centrica, EDF, Drax) keep negotiating power on long-term tariffs.

By end-2025, electrification and hydrogen trials introduced specialist suppliers (electrolyser makers, power electronics), adding sourcing complexity but potential to reduce gas share toward a 20% target in low-carbon scenarios.

Cement and raw material inputs

While Ibstock owns extensive clay reserves, its concrete division relies heavily on external cement and specialized aggregates suppliers; the UK cement market is concentrated with Hanson (Heidelberg Materials), Cemex, and Breedon controlling ~70% of capacity in 2024, limiting Ibstock’s bargaining power.

Dependency worsens as low-carbon cements cost 15–30% more on average in 2024; meeting 2025 UK environmental standards raises binder costs and squeezes Ibstock’s margins.

Skilled labor and engineering

The Atlas factory and similar automated plants need industrial engineers and skilled technicians; UK vacancy rates for engineering roles hit 6.5% in 2024, boosting worker leverage and agency fees.

Persistent shortages mean these staff can demand higher pay—average UK engineering salaries rose 4.2% in 2024—raising Ibstock’s operating costs.

Ibstock must spend on training and retention; a 2023 EEF survey found manufacturers spend £3,200 per hire annually to upskill, or risk downtime from labor mobility.

Carbon permit and regulatory costs

The UK Emissions Trading Scheme (ETS) functions as a de facto supplier of carbon permits, driving a direct, non-negotiable cost into heavy clay production for Ibstock; ETS allowance prices rose to about 80 €/tCO2 in late 2025 benchmarks, pushing compliance costs materially higher.

With free allowance ceilings shrinking through 2025 and beyond, regulatory authorities fix the available supply, creating vertical pricing power: firms must buy permits or pay fines, so the regulator effectively sets a hard cost floor on operations.

- UK ETS price ≈ 80 €/tCO2 (late 2025 benchmark)

- Free allowances reduced annually through 2025

- Compliance is non-discretionary cost

- Regulator holds de facto pricing power

Logistics and distribution partners

Ibstock depends on third-party haulage to move heavy bricks and concrete across the UK; in 2024 diesel rose ~15% vs 2023, pushing logistics rates up and adding ~£2–4/tonne to delivered cost.

Driver shortages (UK HGV driver shortfall ~100,000 in 2023) and need for specialist handling give carriers leverage, narrowing Ibstock’s supplier options and raising switching costs.

- Diesel +15% (2024 vs 2023)

- UK HGV shortfall ~100,000 (2023)

- Specialized handling limits partners

- Added £2–4/tonne delivery cost

Supply squeeze: gas, ETS and transport drive cement costs up 15–30%+

Suppliers hold moderate-to-high power: gas fuels ~70% of kilns (UK TTF €45/MWh in 2024), cement firms (Hanson, Cemex, Breedon) ~70% capacity, low-carbon binders cost +15–30% (2024), UK ETS ≈80 €/tCO2 (late-2025), diesel +15% (2024) adding £2–4/tonne, and HGV shortfall ~100,000 (2023) raising logistics/leverage.

| Metric | Value |

|---|---|

| Gas share | ~70% |

| UK TTF (2024) | €45/MWh |

| Cement market share (top3) | ~70% |

| Low‑carbon binder premium | +15–30% |

| UK ETS (late‑2025) | ≈80 €/tCO2 |

| Diesel change (2024) | +15% |

| Added delivery cost | £2–4/tonne |

| HGV shortfall (2023) | ~100,000 |

What is included in the product

Tailored Porter's Five Forces for Ibstock, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and market protections that shape its brick and masonry industry positioning.

A concise Porter's Five Forces snapshot for Ibstock—clarifies competitive pressures and opportunity drivers for quick strategic decisions.

Customers Bargaining Power

Concentration of major housebuilders

A significant share of Ibstock plc’s revenue—about 35% in FY2024—comes from a handful of large volume housebuilders, giving these buyers strong leverage.

These corporate clients routinely secure volume discounts (often 5–10%) and extended payment terms, pressuring Ibstock’s margins and working capital.

By late 2025, UK housing market consolidation left the top five developers controlling ~50% of private completions, further strengthening buyer bargaining power.

Influence of builders merchants

Price sensitivity in the housing market

Demand for Ibstock plc brick and tile products is highly cyclical and tied to UK mortgage rates and consumer confidence; UK housing starts fell about 6% in 2024 vs 2023, raising buyer price sensitivity.

When housing starts slow, customers delay orders or switch to cheaper aggregates or concrete blocks, squeezing volumes and average selling prices.

This sensitivity limits Ibstock’s ability to pass through inflation—higher input costs in 2024 (energy +18% y/y) risk volume loss if prices rise.

Low switching costs for standard products

For standard clay bricks and concrete blocks, switching costs for developers are low—price drives choice; in UK 2024 brick market surveys showed 12% of volume switched suppliers year-on-year for price reasons.

Extensions needing aesthetic matches are an exception, but new-builds (≈60% of UK demand in 2023) can specify alternatives during design, reducing supplier lock-in.

This weak technical lock-in lets buyers pit manufacturers against each other, pressuring margins; Ibstock faced a 2023 gross margin of ~29% amid competitive pricing.

- Low switching costs: price-led switches (12% volume, 2024)

- New-build flexibility: ~60% of demand (2023)

- Aesthetic lock-in: affects extensions only

- Margin pressure: Ibstock gross margin ~29% (2023)

Growing demand for sustainable specifications

Modern customers increasingly demand products with verified Environmental Product Declarations (EPDs) and lower embodied carbon; 68% of UK major developers surveyed in 2024 required EPDs in tenders, raising supplier pressure on Ibstock.

Large developers now use bargaining power to make strict sustainability criteria a tender gate; projects worth over £5bn in 2024 cited low-carbon targets as mandatory.

Supplying green products is a baseline for major contracts, not a premium add-on, shifting cost and capex priorities for Ibstock’s clay and concrete portfolio.

- 68% of UK developers required EPDs (2024)

- £5bn+ projects mandated low-carbon supply (2024)

- Green supply now baseline, affects pricing and CAPEX

Buyer concentration and discounts squeeze Ibstock margins amid weak UK housing demand

Large housebuilders and merchants concentrated ~65–75% of Ibstock’s FY2024 volumes, winning 5–10% volume discounts and longer payment terms, which squeezed Ibstock’s 2023 gross margin (~29%). Low switching costs (12% volume switched for price in 2024) and cyclical demand (UK starts −6% in 2024) amplify buyer leverage; sustainability rules (68% developers required EPDs in 2024) add cost pressure.

| Metric | 2023–2024 |

|---|---|

| Buyer concentration | 65–75% volumes |

| Volume discounts | 5–10% |

| Switching rate | 12% |

| UK starts | −6% (2024) |

| EPD requirement | 68% |

| Gross margin | ~29% (2023) |

Full Version Awaits

Ibstock Porter's Five Forces Analysis

This preview shows the exact Ibstock Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Ibstock faces moderate supplier power and steady buyer demand, while competitive rivalry is intense due to capacity and pricing pressure; substitutes and new entrants remain restrained by capital intensity and regulation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ibstock’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy market volatility and hedging

Natural gas fuels ~70% of Ibstock’s kilns, so exposure to global wholesale price swings is high; UK gas TTF averaged €45/MWh in 2024, up 30% vs 2020, driving raw energy costs.

Ibstock hedges via forwards and swaps covering ~60% of projected consumption, cutting short-term volatility, but the UK’s few major utilities (Centrica, EDF, Drax) keep negotiating power on long-term tariffs.

By end-2025, electrification and hydrogen trials introduced specialist suppliers (electrolyser makers, power electronics), adding sourcing complexity but potential to reduce gas share toward a 20% target in low-carbon scenarios.

Cement and raw material inputs

While Ibstock owns extensive clay reserves, its concrete division relies heavily on external cement and specialized aggregates suppliers; the UK cement market is concentrated with Hanson (Heidelberg Materials), Cemex, and Breedon controlling ~70% of capacity in 2024, limiting Ibstock’s bargaining power.

Dependency worsens as low-carbon cements cost 15–30% more on average in 2024; meeting 2025 UK environmental standards raises binder costs and squeezes Ibstock’s margins.

Skilled labor and engineering

The Atlas factory and similar automated plants need industrial engineers and skilled technicians; UK vacancy rates for engineering roles hit 6.5% in 2024, boosting worker leverage and agency fees.

Persistent shortages mean these staff can demand higher pay—average UK engineering salaries rose 4.2% in 2024—raising Ibstock’s operating costs.

Ibstock must spend on training and retention; a 2023 EEF survey found manufacturers spend £3,200 per hire annually to upskill, or risk downtime from labor mobility.

Carbon permit and regulatory costs

The UK Emissions Trading Scheme (ETS) functions as a de facto supplier of carbon permits, driving a direct, non-negotiable cost into heavy clay production for Ibstock; ETS allowance prices rose to about 80 €/tCO2 in late 2025 benchmarks, pushing compliance costs materially higher.

With free allowance ceilings shrinking through 2025 and beyond, regulatory authorities fix the available supply, creating vertical pricing power: firms must buy permits or pay fines, so the regulator effectively sets a hard cost floor on operations.

- UK ETS price ≈ 80 €/tCO2 (late 2025 benchmark)

- Free allowances reduced annually through 2025

- Compliance is non-discretionary cost

- Regulator holds de facto pricing power

Logistics and distribution partners

Ibstock depends on third-party haulage to move heavy bricks and concrete across the UK; in 2024 diesel rose ~15% vs 2023, pushing logistics rates up and adding ~£2–4/tonne to delivered cost.

Driver shortages (UK HGV driver shortfall ~100,000 in 2023) and need for specialist handling give carriers leverage, narrowing Ibstock’s supplier options and raising switching costs.

- Diesel +15% (2024 vs 2023)

- UK HGV shortfall ~100,000 (2023)

- Specialized handling limits partners

- Added £2–4/tonne delivery cost

Supply squeeze: gas, ETS and transport drive cement costs up 15–30%+

Suppliers hold moderate-to-high power: gas fuels ~70% of kilns (UK TTF €45/MWh in 2024), cement firms (Hanson, Cemex, Breedon) ~70% capacity, low-carbon binders cost +15–30% (2024), UK ETS ≈80 €/tCO2 (late-2025), diesel +15% (2024) adding £2–4/tonne, and HGV shortfall ~100,000 (2023) raising logistics/leverage.

| Metric | Value |

|---|---|

| Gas share | ~70% |

| UK TTF (2024) | €45/MWh |

| Cement market share (top3) | ~70% |

| Low‑carbon binder premium | +15–30% |

| UK ETS (late‑2025) | ≈80 €/tCO2 |

| Diesel change (2024) | +15% |

| Added delivery cost | £2–4/tonne |

| HGV shortfall (2023) | ~100,000 |

What is included in the product

Tailored Porter's Five Forces for Ibstock, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and market protections that shape its brick and masonry industry positioning.

A concise Porter's Five Forces snapshot for Ibstock—clarifies competitive pressures and opportunity drivers for quick strategic decisions.

Customers Bargaining Power

Concentration of major housebuilders

A significant share of Ibstock plc’s revenue—about 35% in FY2024—comes from a handful of large volume housebuilders, giving these buyers strong leverage.

These corporate clients routinely secure volume discounts (often 5–10%) and extended payment terms, pressuring Ibstock’s margins and working capital.

By late 2025, UK housing market consolidation left the top five developers controlling ~50% of private completions, further strengthening buyer bargaining power.

Influence of builders merchants

Price sensitivity in the housing market

Demand for Ibstock plc brick and tile products is highly cyclical and tied to UK mortgage rates and consumer confidence; UK housing starts fell about 6% in 2024 vs 2023, raising buyer price sensitivity.

When housing starts slow, customers delay orders or switch to cheaper aggregates or concrete blocks, squeezing volumes and average selling prices.

This sensitivity limits Ibstock’s ability to pass through inflation—higher input costs in 2024 (energy +18% y/y) risk volume loss if prices rise.

Low switching costs for standard products

For standard clay bricks and concrete blocks, switching costs for developers are low—price drives choice; in UK 2024 brick market surveys showed 12% of volume switched suppliers year-on-year for price reasons.

Extensions needing aesthetic matches are an exception, but new-builds (≈60% of UK demand in 2023) can specify alternatives during design, reducing supplier lock-in.

This weak technical lock-in lets buyers pit manufacturers against each other, pressuring margins; Ibstock faced a 2023 gross margin of ~29% amid competitive pricing.

- Low switching costs: price-led switches (12% volume, 2024)

- New-build flexibility: ~60% of demand (2023)

- Aesthetic lock-in: affects extensions only

- Margin pressure: Ibstock gross margin ~29% (2023)

Growing demand for sustainable specifications

Modern customers increasingly demand products with verified Environmental Product Declarations (EPDs) and lower embodied carbon; 68% of UK major developers surveyed in 2024 required EPDs in tenders, raising supplier pressure on Ibstock.

Large developers now use bargaining power to make strict sustainability criteria a tender gate; projects worth over £5bn in 2024 cited low-carbon targets as mandatory.

Supplying green products is a baseline for major contracts, not a premium add-on, shifting cost and capex priorities for Ibstock’s clay and concrete portfolio.

- 68% of UK developers required EPDs (2024)

- £5bn+ projects mandated low-carbon supply (2024)

- Green supply now baseline, affects pricing and CAPEX

Buyer concentration and discounts squeeze Ibstock margins amid weak UK housing demand

Large housebuilders and merchants concentrated ~65–75% of Ibstock’s FY2024 volumes, winning 5–10% volume discounts and longer payment terms, which squeezed Ibstock’s 2023 gross margin (~29%). Low switching costs (12% volume switched for price in 2024) and cyclical demand (UK starts −6% in 2024) amplify buyer leverage; sustainability rules (68% developers required EPDs in 2024) add cost pressure.

| Metric | 2023–2024 |

|---|---|

| Buyer concentration | 65–75% volumes |

| Volume discounts | 5–10% |

| Switching rate | 12% |

| UK starts | −6% (2024) |

| EPD requirement | 68% |

| Gross margin | ~29% (2023) |

Full Version Awaits

Ibstock Porter's Five Forces Analysis

This preview shows the exact Ibstock Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.