ICICI Lombard General Insurance PESTLE Analysis

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE snapshot on ICICI Lombard General Insurance—spot regulatory risks, economic headwinds, technological opportunities, and social trends shaping future growth. This concise briefing previews the full analysis to help investors and strategists act faster. Purchase the complete PESTLE now for a detailed, actionable report ready for immediate use.

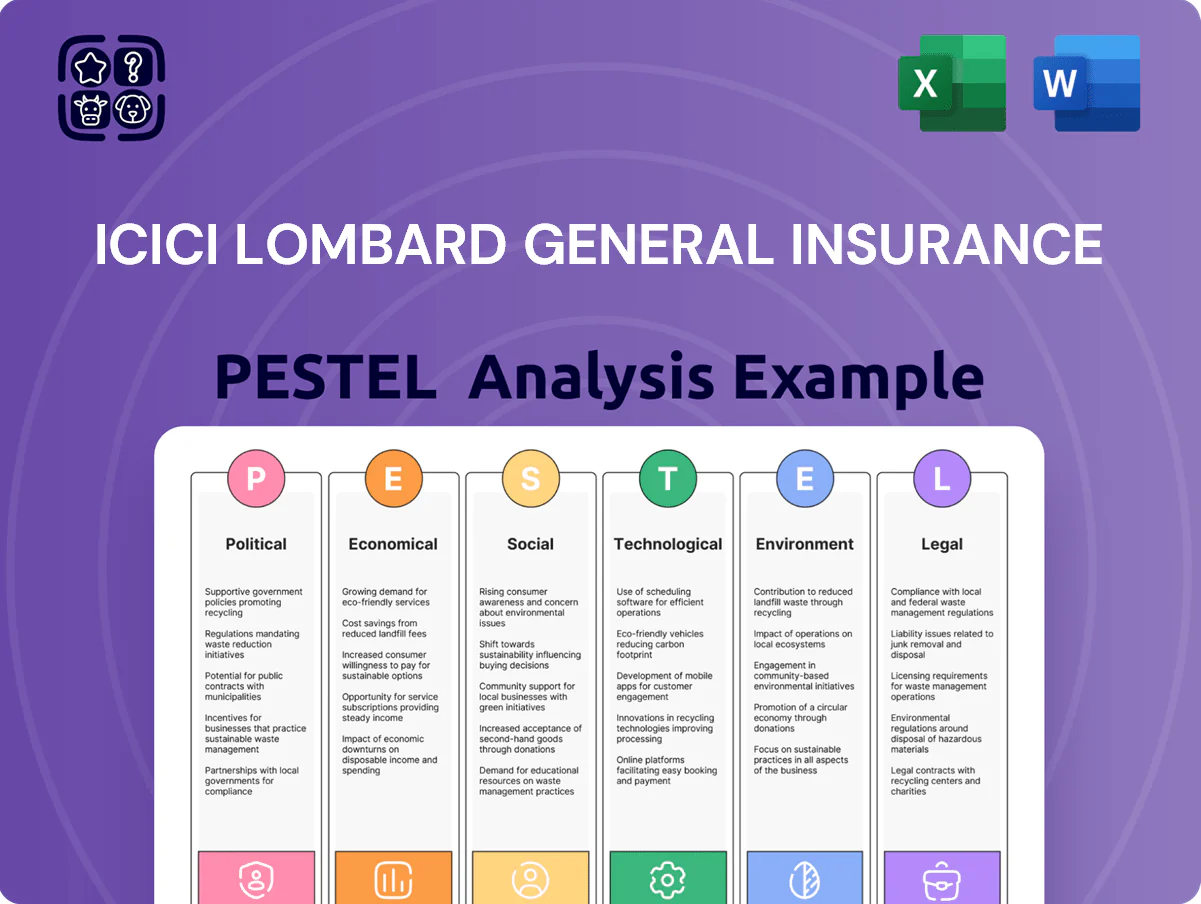

Political factors

Government focus on Insurance for All by 2047

The Indian government and IRDAI aim for universal insurance by 2047, boosting demand for players like ICICI Lombard; IRDAI reported retail penetration rising to 4.2% in 2024, underpinning growth opportunities.

Regulatory easing—simplified distribution norms and sandbox approvals—encourages product innovation and rural outreach, aligning with ICICI Lombard’s FY2024 rural premium growth of ~11%.

State-backed schemes and subsidy linkages reduce acquisition costs and expand scale; political emphasis on financial inclusion supports sustained market expansion and lower per-policy risk.

Foreign Direct Investment policy stability

The continuation of the 74 percent FDI cap in insurance preserves access to global capital—foreign investment inflows to India totaled USD 83.5 billion in FY2024, supporting insurers’ capital needs—benefiting ICICI Lombard by enabling long-term planning and potential JV/ reinsurer tie-ups; bipartisan support for financial-sector liberalization reduces policy-reversal risk, aiding premium growth (ICICI Lombard gross written premium INR 27,472 crore FY2024) and cross-border collaboration.

Taxation policies and GST structures

Government GST decisions shape premium affordability; at 18 percent GST on health insurance in 2024-25, retail demand and lapse ratios remain sensitive, and a cut to 12 or 5 percent could boost sector GWP—ICICI Lombard reported consolidated GWP of INR 39,141 crore in FY2024, so GST relief would materially raise volumes. Changes in corporate tax or capital gains rules also affect underwriting surplus and investment income, where FY2024 investment income was ~INR 3,200 crore.

Geopolitical stability and trade relations

India’s stronger geopolitical standing has tightened reinsurance capacity, lifting international risk cover costs; global reinsurer rates rose ~8-12% in 2024, impacting ICICI Lombard’s pricing for cross-border commercial risks.

Stable trade ties support smoother marine and transit operations, with India’s merchandise exports at $441bn in FY2023–24 aiding premium flows for cargo lines.

Global conflicts drive volatility in investment markets where ICICI Lombard manages a float exceeding ₹25,000 crore, increasing asset-risk and capital-market sensitivity.

- Reinsurance rate rise: ~8–12% (2024)

- India exports FY2023–24: $441bn

- Investment float: >₹25,000 crore

Public sector push for digitalization

ICICI Lombard’s tech-first strategy benefits from the government’s Digital India mission, enabling integration with public APIs and Aadhaar-enabled KYC to speed policy issuance; by FY2024 the insurer reported over 70% of retail policies sourced digitally, cutting turnaround times. Political support for the National Health Stack and Ayushman Bharat Digital Mission allows automated claims adjudication and risk assessment, reducing claim processing costs. This public-private synergy helped lower administrative expense ratios, contributing to improved combined operating ratios and underwriting efficiency.

- Digital policy sourcing >70% (FY2024)

- Faster KYC via Aadhaar/API integration

- Automated claims through NHSP/ABDM reduces processing costs

- Improved underwriting efficiency and lower admin expense ratio

ICICI Lombard poised by retail growth, digital sourcing; margins pressured by rising reinsurance

Political push for universal insurance by 2047, rising retail penetration to 4.2% (2024), and IRDAI-friendly sandboxes drive ICICI Lombard’s growth (GWP INR 39,141cr FY2024; consolidated GWP INR 39,141cr; FY2024 gross written premium INR 27,472cr), while 74% FDI cap, 18% GST on health, rising reinsurance rates (+8–12% 2024) and geopolitical risks affect costs and pricing.

| Metric | Value |

|---|---|

| Retail penetration (2024) | 4.2% |

| Consolidated GWP (FY2024) | INR 39,141 crore |

| Gross written premium (FY2024) | INR 27,472 crore |

| Reinsurance rate change (2024) | +8–12% |

| Digital policy sourcing (FY2024) | >70% |

What is included in the product

Explores how external macro-environmental factors uniquely affect ICICI Lombard General Insurance across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by relevant data and current trends for reliable evaluation.

A concise PESTLE snapshot of ICICI Lombard that’s visually segmented for quick interpretation, easily droppable into presentations or planning sessions to align teams on regulatory, economic, and technological risks and opportunities.

Economic factors

GDP growth and rising disposable income

India’s GDP grew ~7.2% in FY2024–25, lifting per capita income and accelerating demand for motor and travel insurance; ICICI Lombard reported 12% gross written premium growth in FY2024 driven by retail lines. Expansion of a middle class nearing 300 million households increases discretionary insurance uptake, directly supporting the insurer’s top-line. Economic resilience amid global headwinds underpinned a 15% rise in retail policy counts year-on-year, enabling portfolio expansion.

Interest rate environment and investment yields

The RBI rate pauses and hikes through 2023–2025 shaped ICICI Lombard’s yield profile as its debt-heavy investment book earned higher coupon income; reported investment income rose to Rs 2,360 crore in FY2024 (up ~12% YoY), helping offset underwriting strain from rising claims. As 10-year G-sec yield oscillated between ~6.5%–7.5% in 2024–25, active duration management and credit mix rebalancing were necessary to protect solvency margin and FY2025 profitability targets.

Inflationary pressures on claim costs

Rising medical inflation of about 10–12% in India (2024) and a 15–20% surge in automobile spare-part costs since 2022 have pushed up average claim severities in ICICI Lombard’s health and motor books, raising combined ratio pressures. The insurer must calibrate premium increases—recently averaging 7–9% in select segments—while protecting retention to keep combined ratio near its FY2024 level of ~102%. Frequent repricing, underwriting adjustments and cost containment are therefore essential to maintain solvency and long-term margin.

Growth in the automotive and infrastructure sectors

The health of India’s automotive industry—vehicle sales reaching about 4.1 million units in FY2024—directly drives ICICI Lombard’s motor segment, which accounted for roughly 45% of gross written premiums in 2023-24; slowing auto cycles reduce retail motor premium volumes and loss ratios pressure underwriting. Increased government capital expenditure, with infrastructure outlays at INR 12.2 trillion in FY2024, expands demand for fire, engineering and liability covers, lifting commercial premium pools. Cyclical upswings in auto and infrastructure translate into higher corporate and commercial premium inflows and diversification of risk exposure for the insurer.

- Auto sales ~4.1M units FY2024; motor ~45% of GWP (2023-24)

- Infrastructure capex ~INR 12.2T FY2024 boosting engineering/fire/liability demand

- Sectors’ economic cycles directly affect corporate/commercial premium volumes

Currency fluctuations and global trade

Volatility in the INR-USD rate raises reinsurance costs and alters valuation of cross-border claims; INR weakened ~8% vs USD in 2022-2023 then stabilized, increasing reinsurers' premium pressure on Indian cedants like ICICI Lombard.

ICICI Lombard prefers currency stability to manage USD-denominated reinsurance exposure—foreign currency reserves and hedging affect combined ratio and solvency metrics.

Trade shifts: India merchandise exports rose to $450bn in FY2023, boosting demand for marine insurance, while import cycles drive cargo risk and premium volumes.

- INR volatility → higher reinsurance costs

- Hedging/FX reserves mitigate exposure

- Exports $450bn (FY2023) increase marine premiums

Strong GDP and retail growth vs rising claim costs: motor drives GWP, combined ratio ~102%

GDP ~7.2% FY2024–25, retail GWP growth 12% FY2024; middle class ~300M households supports demand; motor ~45% of GWP (FY2023-24) with auto sales ~4.1M units FY2024. Investment income Rs 2,360 crore FY2024 (↑12% YoY) as 10y G-sec ~6.5–7.5% (2024–25). Medical inflation ~10–12% (2024) and auto-part cost ↑15–20% since 2022 raise claim severities; combined ratio ~102% FY2024.

| Metric | Value |

|---|---|

| GDP growth | ~7.2% FY2024–25 |

| Retail GWP growth | 12% FY2024 |

| Motor share | ~45% GWP (FY2023-24) |

| Auto sales | ~4.1M units FY2024 |

| Investment income | Rs 2,360 Cr FY2024 |

| Medical inflation | 10–12% (2024) |

| Combined ratio | ~102% FY2024 |

Preview Before You Purchase

ICICI Lombard General Insurance PESTLE Analysis

The preview shown here is the exact ICICI Lombard General Insurance PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE snapshot on ICICI Lombard General Insurance—spot regulatory risks, economic headwinds, technological opportunities, and social trends shaping future growth. This concise briefing previews the full analysis to help investors and strategists act faster. Purchase the complete PESTLE now for a detailed, actionable report ready for immediate use.

Political factors

Government focus on Insurance for All by 2047

The Indian government and IRDAI aim for universal insurance by 2047, boosting demand for players like ICICI Lombard; IRDAI reported retail penetration rising to 4.2% in 2024, underpinning growth opportunities.

Regulatory easing—simplified distribution norms and sandbox approvals—encourages product innovation and rural outreach, aligning with ICICI Lombard’s FY2024 rural premium growth of ~11%.

State-backed schemes and subsidy linkages reduce acquisition costs and expand scale; political emphasis on financial inclusion supports sustained market expansion and lower per-policy risk.

Foreign Direct Investment policy stability

The continuation of the 74 percent FDI cap in insurance preserves access to global capital—foreign investment inflows to India totaled USD 83.5 billion in FY2024, supporting insurers’ capital needs—benefiting ICICI Lombard by enabling long-term planning and potential JV/ reinsurer tie-ups; bipartisan support for financial-sector liberalization reduces policy-reversal risk, aiding premium growth (ICICI Lombard gross written premium INR 27,472 crore FY2024) and cross-border collaboration.

Taxation policies and GST structures

Government GST decisions shape premium affordability; at 18 percent GST on health insurance in 2024-25, retail demand and lapse ratios remain sensitive, and a cut to 12 or 5 percent could boost sector GWP—ICICI Lombard reported consolidated GWP of INR 39,141 crore in FY2024, so GST relief would materially raise volumes. Changes in corporate tax or capital gains rules also affect underwriting surplus and investment income, where FY2024 investment income was ~INR 3,200 crore.

Geopolitical stability and trade relations

India’s stronger geopolitical standing has tightened reinsurance capacity, lifting international risk cover costs; global reinsurer rates rose ~8-12% in 2024, impacting ICICI Lombard’s pricing for cross-border commercial risks.

Stable trade ties support smoother marine and transit operations, with India’s merchandise exports at $441bn in FY2023–24 aiding premium flows for cargo lines.

Global conflicts drive volatility in investment markets where ICICI Lombard manages a float exceeding ₹25,000 crore, increasing asset-risk and capital-market sensitivity.

- Reinsurance rate rise: ~8–12% (2024)

- India exports FY2023–24: $441bn

- Investment float: >₹25,000 crore

Public sector push for digitalization

ICICI Lombard’s tech-first strategy benefits from the government’s Digital India mission, enabling integration with public APIs and Aadhaar-enabled KYC to speed policy issuance; by FY2024 the insurer reported over 70% of retail policies sourced digitally, cutting turnaround times. Political support for the National Health Stack and Ayushman Bharat Digital Mission allows automated claims adjudication and risk assessment, reducing claim processing costs. This public-private synergy helped lower administrative expense ratios, contributing to improved combined operating ratios and underwriting efficiency.

- Digital policy sourcing >70% (FY2024)

- Faster KYC via Aadhaar/API integration

- Automated claims through NHSP/ABDM reduces processing costs

- Improved underwriting efficiency and lower admin expense ratio

ICICI Lombard poised by retail growth, digital sourcing; margins pressured by rising reinsurance

Political push for universal insurance by 2047, rising retail penetration to 4.2% (2024), and IRDAI-friendly sandboxes drive ICICI Lombard’s growth (GWP INR 39,141cr FY2024; consolidated GWP INR 39,141cr; FY2024 gross written premium INR 27,472cr), while 74% FDI cap, 18% GST on health, rising reinsurance rates (+8–12% 2024) and geopolitical risks affect costs and pricing.

| Metric | Value |

|---|---|

| Retail penetration (2024) | 4.2% |

| Consolidated GWP (FY2024) | INR 39,141 crore |

| Gross written premium (FY2024) | INR 27,472 crore |

| Reinsurance rate change (2024) | +8–12% |

| Digital policy sourcing (FY2024) | >70% |

What is included in the product

Explores how external macro-environmental factors uniquely affect ICICI Lombard General Insurance across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by relevant data and current trends for reliable evaluation.

A concise PESTLE snapshot of ICICI Lombard that’s visually segmented for quick interpretation, easily droppable into presentations or planning sessions to align teams on regulatory, economic, and technological risks and opportunities.

Economic factors

GDP growth and rising disposable income

India’s GDP grew ~7.2% in FY2024–25, lifting per capita income and accelerating demand for motor and travel insurance; ICICI Lombard reported 12% gross written premium growth in FY2024 driven by retail lines. Expansion of a middle class nearing 300 million households increases discretionary insurance uptake, directly supporting the insurer’s top-line. Economic resilience amid global headwinds underpinned a 15% rise in retail policy counts year-on-year, enabling portfolio expansion.

Interest rate environment and investment yields

The RBI rate pauses and hikes through 2023–2025 shaped ICICI Lombard’s yield profile as its debt-heavy investment book earned higher coupon income; reported investment income rose to Rs 2,360 crore in FY2024 (up ~12% YoY), helping offset underwriting strain from rising claims. As 10-year G-sec yield oscillated between ~6.5%–7.5% in 2024–25, active duration management and credit mix rebalancing were necessary to protect solvency margin and FY2025 profitability targets.

Inflationary pressures on claim costs

Rising medical inflation of about 10–12% in India (2024) and a 15–20% surge in automobile spare-part costs since 2022 have pushed up average claim severities in ICICI Lombard’s health and motor books, raising combined ratio pressures. The insurer must calibrate premium increases—recently averaging 7–9% in select segments—while protecting retention to keep combined ratio near its FY2024 level of ~102%. Frequent repricing, underwriting adjustments and cost containment are therefore essential to maintain solvency and long-term margin.

Growth in the automotive and infrastructure sectors

The health of India’s automotive industry—vehicle sales reaching about 4.1 million units in FY2024—directly drives ICICI Lombard’s motor segment, which accounted for roughly 45% of gross written premiums in 2023-24; slowing auto cycles reduce retail motor premium volumes and loss ratios pressure underwriting. Increased government capital expenditure, with infrastructure outlays at INR 12.2 trillion in FY2024, expands demand for fire, engineering and liability covers, lifting commercial premium pools. Cyclical upswings in auto and infrastructure translate into higher corporate and commercial premium inflows and diversification of risk exposure for the insurer.

- Auto sales ~4.1M units FY2024; motor ~45% of GWP (2023-24)

- Infrastructure capex ~INR 12.2T FY2024 boosting engineering/fire/liability demand

- Sectors’ economic cycles directly affect corporate/commercial premium volumes

Currency fluctuations and global trade

Volatility in the INR-USD rate raises reinsurance costs and alters valuation of cross-border claims; INR weakened ~8% vs USD in 2022-2023 then stabilized, increasing reinsurers' premium pressure on Indian cedants like ICICI Lombard.

ICICI Lombard prefers currency stability to manage USD-denominated reinsurance exposure—foreign currency reserves and hedging affect combined ratio and solvency metrics.

Trade shifts: India merchandise exports rose to $450bn in FY2023, boosting demand for marine insurance, while import cycles drive cargo risk and premium volumes.

- INR volatility → higher reinsurance costs

- Hedging/FX reserves mitigate exposure

- Exports $450bn (FY2023) increase marine premiums

Strong GDP and retail growth vs rising claim costs: motor drives GWP, combined ratio ~102%

GDP ~7.2% FY2024–25, retail GWP growth 12% FY2024; middle class ~300M households supports demand; motor ~45% of GWP (FY2023-24) with auto sales ~4.1M units FY2024. Investment income Rs 2,360 crore FY2024 (↑12% YoY) as 10y G-sec ~6.5–7.5% (2024–25). Medical inflation ~10–12% (2024) and auto-part cost ↑15–20% since 2022 raise claim severities; combined ratio ~102% FY2024.

| Metric | Value |

|---|---|

| GDP growth | ~7.2% FY2024–25 |

| Retail GWP growth | 12% FY2024 |

| Motor share | ~45% GWP (FY2023-24) |

| Auto sales | ~4.1M units FY2024 |

| Investment income | Rs 2,360 Cr FY2024 |

| Medical inflation | 10–12% (2024) |

| Combined ratio | ~102% FY2024 |

Preview Before You Purchase

ICICI Lombard General Insurance PESTLE Analysis

The preview shown here is the exact ICICI Lombard General Insurance PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.