ICL Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

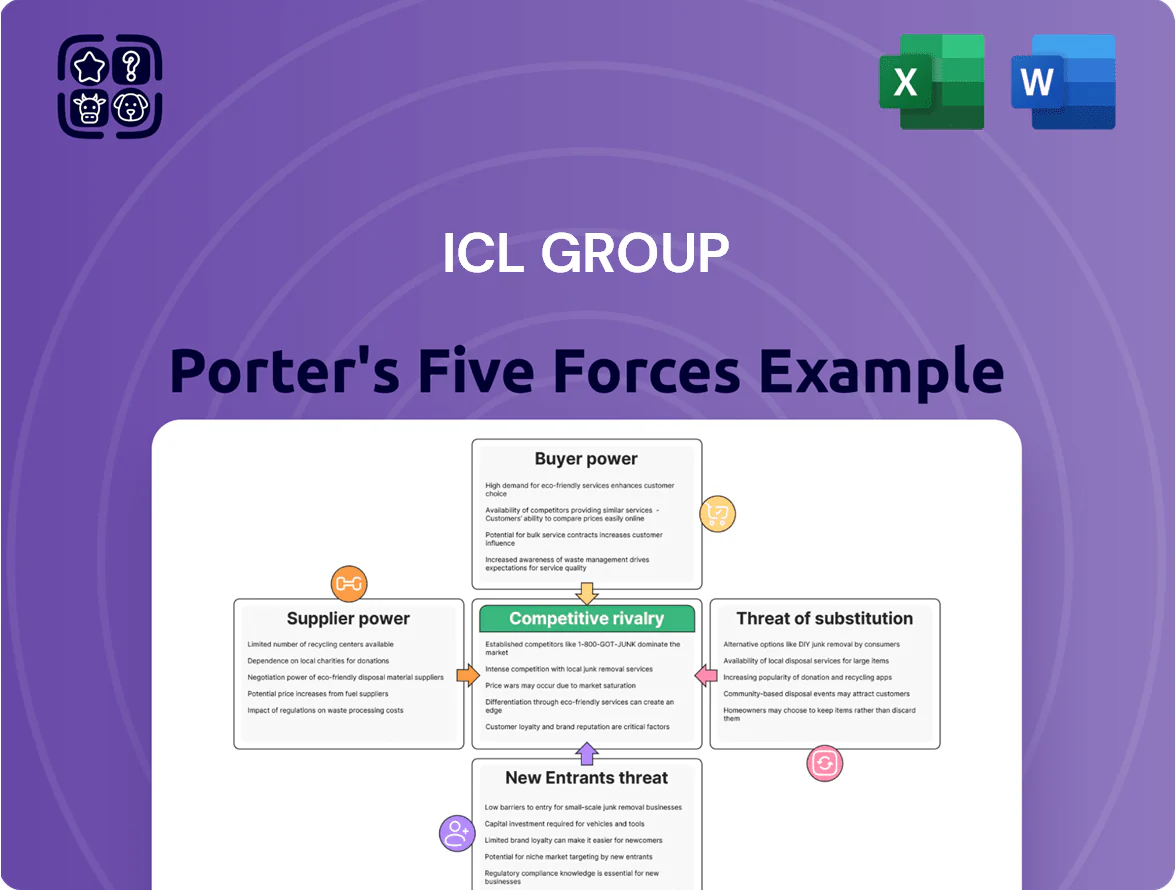

ICL Group faces moderate buyer power and supplier concentration, with raw material volatility and regulatory pressures shaping margins; competitive rivalry is high from global fertilizer and specialty chemicals players while threat of new entrants remains low due to capital intensity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ICL Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration of Key Raw Materials

ICL Group’s ownership of Dead Sea concessions and Negev phosphate mines gives it direct control of ~60% of its potash and bromine feedstock, cutting supplier bargaining power sharply.

Vertical integration shields ICL from commodity-price swings; in 2024 ICL reported a 12% lower raw-material cost per ton versus peers without mines, reducing margin pressure.

Energy and Utility Dependency

Despite mineral self-sufficiency, ICL Group relies on external natural gas and grid electricity for refining; energy accounts for about 18% of production costs and 12% of EBITDA as of Q3 2025.

By late 2025 ICL has locked multiple long-term gas and power contracts covering roughly 70% of needs, but regional price swings (±25% past 24 months) keep supplier risk moderate.

Energy suppliers are regionally concentrated—top three providers control ~65% of local capacity—so ICL has limited leverage when renegotiating renewal terms.

Specialized Mining Equipment and Technology

The global market for high-tech mining machinery and specialized chemical processing equipment is concentrated among a few vendors—Komatsu, Caterpillar, FLSmidth—giving suppliers moderate bargaining power due to complex tech and long-term service needs; switch costs are high, with aftermarket contracts often 10–20% of capex annually. ICL (Israel Chemicals Ltd) depends on these partnerships for brine extraction and potash processing; a 2024 industry report shows OEMs control ~60–70% of aftermarket parts for key equipment, raising lock-in risk and potential downtime costs.

Logistics and Maritime Shipping Constraints

As a global exporter, ICL depends on third-party shipping lines and port authorities to move bulk minerals; in 2025 average capesize freight rates stayed volatile, trading near 18,000 USD/day in Q1 2025, keeping supplier leverage high.

Long-term charters reduce spot exposure, but a 12–18% shortfall in specialized bulk carrier capacity versus 2019 levels and fuel (HFO) price swings of ±25% in 2024–25 give carriers pricing power.

Governmental and Regulatory Oversight

Government bodies function as unconventional suppliers by controlling extraction licenses, royalties and land access, giving them high bargaining power over ICL’s phosphate and potash assets.

In Israel, state-set royalties and the 2023–2025 environmental rules raised compliance costs; fiscal changes in 2024 increased effective royalty rates by about 2–3 percentage points, tightening margins.

Regulatory shifts—stricter emissions limits and water-use permits—directly affect capex and OPEX, reducing operational flexibility and raising project payback times.

- State controls licenses, royalties → high supplier power

- 2024 fiscal changes raised royalties ~2–3 ppt

- 2023–25 regs increased compliance capex and OPEX

- Regulatory risk compresses margins and delays projects

ICL controls feedstock (~60%) but energy, shipping costs and rising royalties keep supplier power high

ICL’s mine ownership cuts supplier bargaining power (feeds ~60% of potash/bromine). Energy and shipping remain key vulnerabilities: energy ~18% of production costs and 12% of EBITDA (Q3 2025); avg capesize ~18,000 USD/day (Q1 2025); bulk carrier capacity shortfall 12–18% vs 2019. Regulatory suppliers (licenses/royalties) raised effective royalties ~2–3 ppt in 2024, keeping supplier power moderate-to-high.

| Item | Key figure |

|---|---|

| Feedstock self-sufficiency | ~60% |

| Energy share of costs | 18% |

| Energy share of EBITDA | 12% |

| Capesize rate (Q1 2025) | 18,000 USD/day |

| Bulk carrier shortfall vs 2019 | 12–18% |

| Royalty rise (2024) | +2–3 ppt |

What is included in the product

Tailored Porter's Five Forces analysis for ICL Group uncovering competitive intensity, buyer/supplier power, entry barriers, substitute threats, and industry rivalry—with strategic insights on how these forces shape ICL’s pricing, margins, and growth prospects.

Concise Porter's Five Forces for ICL Group—one-sheet clarity to speed strategic decisions and spot where to relieve competitive pressures.

Customers Bargaining Power

Fragmentation of Agricultural End-Users

The vast majority of ICL Group's fertilizers reach millions of small farmers worldwide who hold negligible individual bargaining power, so ICL can avoid retail price pressure; in 2024 roughly 70–80% of global fertilizer volumes were sold via local dealers/cooperatives, which aggregate demand and dilute farmer influence.

Concentration of Large Scale Distributors

High Switching Costs for Specialty Chemicals

In ICL’s specialty minerals and food additives, customer switching costs are high because specific formulations and tight quality specs force costly requalification; industrial clients embedding ICL’s bromine flame retardants or phosphate additives into processes face re-testing and redesign bills often exceeding $500k, per industry case studies, lowering buyer bargaining power and anchoring long-term contracts and premium pricing for ICL.

Commodity Price Sensitivity in Potash

Potash and standard phosphate fertilizers trade as commodities, so buyers react strongly to price moves; bulk potash spot prices fell ~18% in 2024-25 when supply rose, showing this sensitivity.

By 2025 global buyers use real-time platforms and price indices, raising bargaining leverage and enabling tighter contract pricing; ICL often acts as a price taker in large deals, reducing margin control.

- Commoditized product → high buyer price sensitivity

- Spot price drop ~18% in 2024-25

- Real-time data raises buyer negotiating power

- ICL functions mainly as price taker in bulk contracts

Strategic Importance of Food Security

Distributor power vs. fragmented farmers: discounts, long credit & specialty premiums

Buyers split: millions of weak farmers vs. powerful distributors—~70–80% volumes via dealers (2024), top distributors >30% regional demand and orders 10k+ tonnes, forcing volume discounts and 60–120 day credit; ~40% upstream sales tied to distributor contracts. Specialty minerals see high switching costs—requalification >$500k, supporting premium pricing. Commodities remain price-sensitive: potash spot fell ~18% (2024–25); global fertilizer subsidies >$70B (2024).

| Metric | 2024–25 value |

|---|---|

| Dealer-sold share | 70–80% |

| Top distributor share | >30% regional |

| Upstream sales via distributors | ~40% |

| Potash spot change | −18% |

| Global subsidies | >$70B |

| Requalification cost (specialty) | >$500k |

Preview the Actual Deliverable

ICL Group Porter's Five Forces Analysis

This preview shows the exact ICL Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable; after payment you’ll get instant access to this same file for immediate application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

ICL Group faces moderate buyer power and supplier concentration, with raw material volatility and regulatory pressures shaping margins; competitive rivalry is high from global fertilizer and specialty chemicals players while threat of new entrants remains low due to capital intensity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ICL Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration of Key Raw Materials

ICL Group’s ownership of Dead Sea concessions and Negev phosphate mines gives it direct control of ~60% of its potash and bromine feedstock, cutting supplier bargaining power sharply.

Vertical integration shields ICL from commodity-price swings; in 2024 ICL reported a 12% lower raw-material cost per ton versus peers without mines, reducing margin pressure.

Energy and Utility Dependency

Despite mineral self-sufficiency, ICL Group relies on external natural gas and grid electricity for refining; energy accounts for about 18% of production costs and 12% of EBITDA as of Q3 2025.

By late 2025 ICL has locked multiple long-term gas and power contracts covering roughly 70% of needs, but regional price swings (±25% past 24 months) keep supplier risk moderate.

Energy suppliers are regionally concentrated—top three providers control ~65% of local capacity—so ICL has limited leverage when renegotiating renewal terms.

Specialized Mining Equipment and Technology

The global market for high-tech mining machinery and specialized chemical processing equipment is concentrated among a few vendors—Komatsu, Caterpillar, FLSmidth—giving suppliers moderate bargaining power due to complex tech and long-term service needs; switch costs are high, with aftermarket contracts often 10–20% of capex annually. ICL (Israel Chemicals Ltd) depends on these partnerships for brine extraction and potash processing; a 2024 industry report shows OEMs control ~60–70% of aftermarket parts for key equipment, raising lock-in risk and potential downtime costs.

Logistics and Maritime Shipping Constraints

As a global exporter, ICL depends on third-party shipping lines and port authorities to move bulk minerals; in 2025 average capesize freight rates stayed volatile, trading near 18,000 USD/day in Q1 2025, keeping supplier leverage high.

Long-term charters reduce spot exposure, but a 12–18% shortfall in specialized bulk carrier capacity versus 2019 levels and fuel (HFO) price swings of ±25% in 2024–25 give carriers pricing power.

Governmental and Regulatory Oversight

Government bodies function as unconventional suppliers by controlling extraction licenses, royalties and land access, giving them high bargaining power over ICL’s phosphate and potash assets.

In Israel, state-set royalties and the 2023–2025 environmental rules raised compliance costs; fiscal changes in 2024 increased effective royalty rates by about 2–3 percentage points, tightening margins.

Regulatory shifts—stricter emissions limits and water-use permits—directly affect capex and OPEX, reducing operational flexibility and raising project payback times.

- State controls licenses, royalties → high supplier power

- 2024 fiscal changes raised royalties ~2–3 ppt

- 2023–25 regs increased compliance capex and OPEX

- Regulatory risk compresses margins and delays projects

ICL controls feedstock (~60%) but energy, shipping costs and rising royalties keep supplier power high

ICL’s mine ownership cuts supplier bargaining power (feeds ~60% of potash/bromine). Energy and shipping remain key vulnerabilities: energy ~18% of production costs and 12% of EBITDA (Q3 2025); avg capesize ~18,000 USD/day (Q1 2025); bulk carrier capacity shortfall 12–18% vs 2019. Regulatory suppliers (licenses/royalties) raised effective royalties ~2–3 ppt in 2024, keeping supplier power moderate-to-high.

| Item | Key figure |

|---|---|

| Feedstock self-sufficiency | ~60% |

| Energy share of costs | 18% |

| Energy share of EBITDA | 12% |

| Capesize rate (Q1 2025) | 18,000 USD/day |

| Bulk carrier shortfall vs 2019 | 12–18% |

| Royalty rise (2024) | +2–3 ppt |

What is included in the product

Tailored Porter's Five Forces analysis for ICL Group uncovering competitive intensity, buyer/supplier power, entry barriers, substitute threats, and industry rivalry—with strategic insights on how these forces shape ICL’s pricing, margins, and growth prospects.

Concise Porter's Five Forces for ICL Group—one-sheet clarity to speed strategic decisions and spot where to relieve competitive pressures.

Customers Bargaining Power

Fragmentation of Agricultural End-Users

The vast majority of ICL Group's fertilizers reach millions of small farmers worldwide who hold negligible individual bargaining power, so ICL can avoid retail price pressure; in 2024 roughly 70–80% of global fertilizer volumes were sold via local dealers/cooperatives, which aggregate demand and dilute farmer influence.

Concentration of Large Scale Distributors

High Switching Costs for Specialty Chemicals

In ICL’s specialty minerals and food additives, customer switching costs are high because specific formulations and tight quality specs force costly requalification; industrial clients embedding ICL’s bromine flame retardants or phosphate additives into processes face re-testing and redesign bills often exceeding $500k, per industry case studies, lowering buyer bargaining power and anchoring long-term contracts and premium pricing for ICL.

Commodity Price Sensitivity in Potash

Potash and standard phosphate fertilizers trade as commodities, so buyers react strongly to price moves; bulk potash spot prices fell ~18% in 2024-25 when supply rose, showing this sensitivity.

By 2025 global buyers use real-time platforms and price indices, raising bargaining leverage and enabling tighter contract pricing; ICL often acts as a price taker in large deals, reducing margin control.

- Commoditized product → high buyer price sensitivity

- Spot price drop ~18% in 2024-25

- Real-time data raises buyer negotiating power

- ICL functions mainly as price taker in bulk contracts

Strategic Importance of Food Security

Distributor power vs. fragmented farmers: discounts, long credit & specialty premiums

Buyers split: millions of weak farmers vs. powerful distributors—~70–80% volumes via dealers (2024), top distributors >30% regional demand and orders 10k+ tonnes, forcing volume discounts and 60–120 day credit; ~40% upstream sales tied to distributor contracts. Specialty minerals see high switching costs—requalification >$500k, supporting premium pricing. Commodities remain price-sensitive: potash spot fell ~18% (2024–25); global fertilizer subsidies >$70B (2024).

| Metric | 2024–25 value |

|---|---|

| Dealer-sold share | 70–80% |

| Top distributor share | >30% regional |

| Upstream sales via distributors | ~40% |

| Potash spot change | −18% |

| Global subsidies | >$70B |

| Requalification cost (specialty) | >$500k |

Preview the Actual Deliverable

ICL Group Porter's Five Forces Analysis

This preview shows the exact ICL Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable; after payment you’ll get instant access to this same file for immediate application.