Icahn Enterprises Porter's Five Forces Analysis

Don't Miss the Bigger Picture

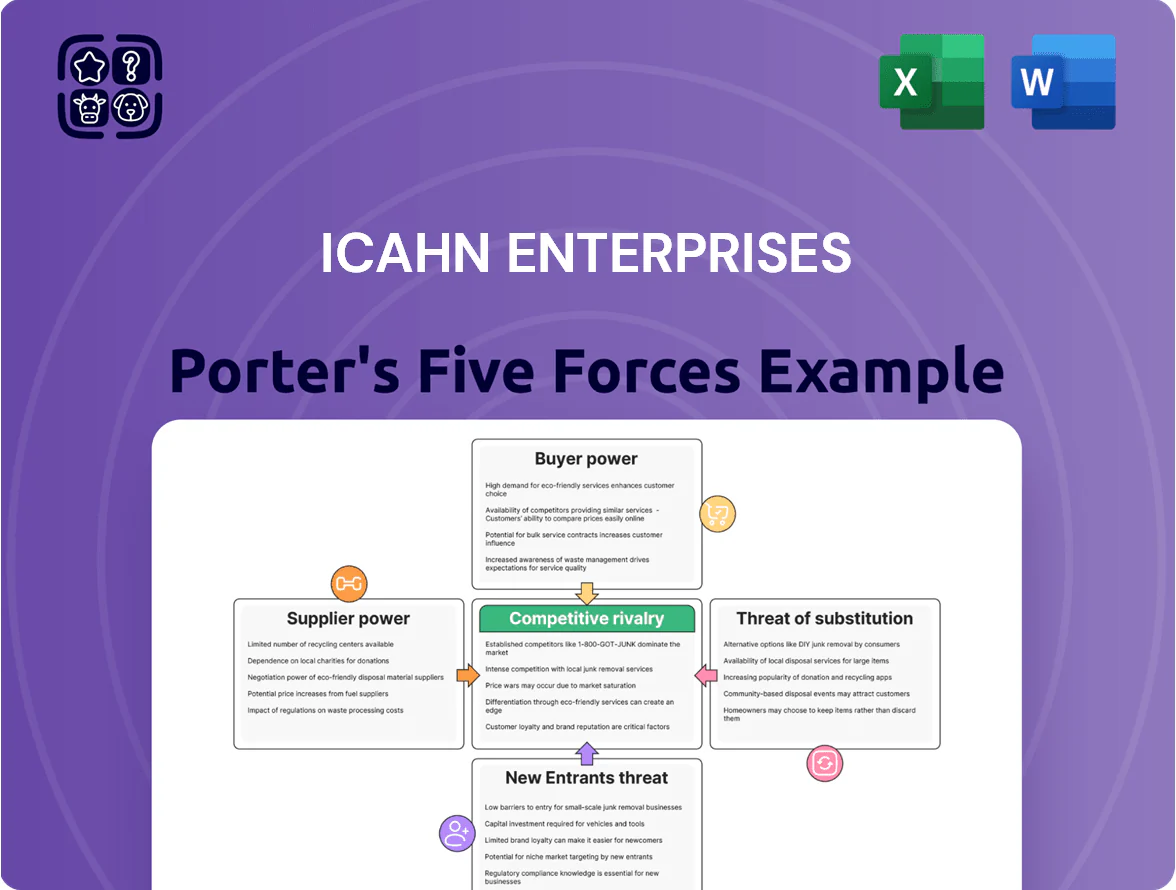

Icahn Enterprises faces mixed pressures: strong supplier influence in key holdings, moderate buyer power across diversified assets, and heightened rivalry from private-equity and activist competitors—while barriers to entry vary by segment.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Icahn Enterprises’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy Feedstock Volatility

As a major energy player via CVR Energy, Icahn Enterprises depends heavily on crude suppliers and global markets; Brent crude averaged about 85 USD/bbl in 2025, so feedstock swings materially affect input costs.

Geopolitical shifts and OPEC+ supply cuts—2024 cuts removed ~2.2 million bpd at peak—limit Icahn’s pricing power, forcing margins to absorb volatility.

Refining feedstocks are specialized, so disruptions in heavy sour or light sweet crude chains can compress refining margins quickly; U.S. refinery crack spreads fell to near 5 USD/bbl in late 2024, illustrating sensitivity.

Automotive Aftermarket Fragmentation

The automotive aftermarket for Icahn Enterprises depends on thousands of global parts makers, so no single supplier holds full leverage, but proprietary EV components are concentrating power in specialized tech vendors—EV parts suppliers grew 28% YoY in 2024 per industry tracker. Supply-chain resilience is key: Icahn must trade higher inventory carrying costs (average aftermarket inventory days ~45 in 2024) against service availability. Immediate part access affects service revenue and customer retention.

Specialized Labor and Technical Expertise

Across Icahn Enterprises’ industrial and automotive units, demand for skilled machinists, welders, and controls engineers raises supplier power; US Bureau of Labor Statistics data show employment in industrial machinery mechanics down 2% 2020–2024 while mean wages rose ~18%, tightening labor supply. Union contracts in refining/manufacturing and 2024 oilfield service wage growth of ~12% increase labor bargaining leverage, raising operating cost risk.

Raw Materials for Food Packaging and Fashion

Viskase and home fashion rely on cellulose, resins, and textile fibers bought from global chemical and agricultural suppliers, so supplier pricing drives input costs.

These inputs trade as commodities—cellulose pulp fell ~6% in 2024 while polyester fiber averaged $1.05/kg in Q4 2024—so Icahn Enterprises faces material price cycles.

With limited vertical integration in these raw materials, the company often absorbs hikes or passes costs and risks losing volume.

- High exposure to commodity cycles

- Cellulose down 6% in 2024

- Polyester ~1.05/kg in Q4 2024

- Limited vertical integration raises margin risk

Capital and Financing Access

As a debt-fueled holding company, Icahn Enterprises depends on capital providers whose pricing and covenants shape its activist moves; in 2024 the firm reported net debt of about $1.7 billion, so a 100 bp rise in rates raises annual interest expense materially.

Tighter credit markets or downgrades to its or subsidiaries’ ratings would raise funding costs and limit deal agility, potentially forcing asset sales or slower rollouts for capital-heavy units.

- Net debt ~ $1.7B (2024)

- 100 bp rate rise increases interest burden

- Credit tightening → reduced acquisition agility

- Unfavorable covenants may force disposals

Suppliers' Medium-High Power: Commodity & Labor Volatility Squeezes Margins

Suppliers exert medium-high power: commodity feedstocks (Brent ~$85/bbl 2025) and cellulose/polyester cycles (cellulose -6% 2024; polyester ~$1.05/kg Q4 2024) drive cost volatility, limited vertical integration forces Icahn to absorb or pass hikes, and specialized EV parts plus tightening skilled-labor supply (machinist wages +18% 2020–24) increase supplier leverage.

| Item | Key number |

|---|---|

| Brent crude (2025) | $85/bbl |

| Cellulose (2024) | -6% |

| Polyester (Q4 2024) | $1.05/kg |

| Aftermarket inventory days (2024) | ~45 days |

| Net debt (2024) | $1.7B |

What is included in the product

Tailored Porter's Five Forces analysis for Icahn Enterprises that uncovers competitive drivers, supplier and buyer leverage, threats from substitutes and new entrants, and strategic implications for profitability and market positioning.

Clear, one-sheet Porter's Five Forces for Icahn Enterprises—quickly assess bargaining power, rivalry, and threat levels to inform strategic moves and investor decisions.

Customers Bargaining Power

Concentration in Food Packaging

The food-packaging unit sells mainly to a small set of global processors and meat producers, who account for roughly 60–75% of segment volumes and wield strong purchasing power; they push for lower prices, bespoke specifications, and tight delivery windows. In 2024 a single lost contract representing ~8–12% of segment sales would cut adjusted EBIT by an estimated 15–20%, so customer concentration materially raises revenue and margin risk.

Retail Consumer Price Sensitivity

Retail consumers in Icahn Enterprises’ automotive aftermarket and home fashion segments are highly price-sensitive with low switching costs; surveys show 68% of U.S. shoppers compare prices online before buying (2024 Pew/Commerce data), so a 5–10% price gap often shifts demand.

Wide product choice and platforms like Amazon and AutoZone mean easy migration, pressuring Icahn’s subsidiaries to match prices and offer fast fulfillment; retention hinges on service quality and repeat discounts.

Energy Market Price Takers

The energy segment sells refined gasoline and diesel into wholesale markets and largely acts as a price taker; in 2024 U.S. wholesale gasoline averaged about $2.60/gal and diesel $3.10/gal, so Icahn Enterprises cannot command a premium. Large distributors and commercial buyers purchase on benchmark rates (NYMEX/OPIS), creating customer leverage. Buyers shift volumes to the lowest-cost regional supplier, making price the main competitive lever and compressing margins.

Investment Activism and Shareholder Influence

Shareholders and LP partners fund Icahn Enterprises’ activist plays and can withdraw capital or sell units if returns lag; the LP unit fell ~28% in 2022 and traded near $13 in Dec 2025, highlighting sensitivity to performance.

Icahn must continuously demonstrate alpha to a savvy investor base that can reallocate billions—Carl Icahn’s family office and institutional holders together controlled ~38% of voting power in 2024—so stewardship and short-term returns drive capital flows.

- LP unit price ~ $13 (Dec 2025)

- ~28% LP decline in 2022

- ~38% voting power held by insiders/institutions (2024)

- High redemption risk if activist returns underperform

B2B Contractual Rigidity

Many Icahn Enterprises industrial subsidiaries run multi-year contracts with corporate clients that include strict performance clauses; in 2024 roughly 60% of segment revenue came from contracts longer than three years, limiting pricing freedom.

Clients can renegotiate at renewal—especially after commodity swings or supply shocks—pushing margins down; a 2023–24 sample showed renewal concessions averaging 120–180 basis points.

That contractual rigidity forces sustained operational excellence to avoid penalties or terminations and caps upside in good markets.

- ~60% revenue under >3-year contracts

- Renewal concessions ~120–180 bps (2023–24)

- Performance clauses raise penalty/termination risk

Buyer Power Threatens Margins: Top Food Customers & Price-Sensitive Retailers Rule

Customer power is high: top food-packaging buyers drive 60–75% volumes and a lost contract (≈8–12% sales) would cut segment adj. EBIT ~15–20% (2024); retail buyers are price-sensitive (68% compare online, 2024) and switch on 5–10% price gaps; energy sales are price-taker (2024 wholesale gasoline ~$2.60/gal, diesel ~$3.10/gal) and large distributors buy on benchmarks.

| Metric | Value |

|---|---|

| Top-buyer share (food-pack) | 60–75% |

| Single-contract risk | 8–12% sales → −15–20% adj. EBIT |

| Online price checks (US) | 68% (2024) |

| Wholesale fuel prices (US) | Gas $2.60/gal, Diesel $3.10/gal (2024) |

Full Version Awaits

Icahn Enterprises Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Icahn Enterprises you'll receive after purchase—no placeholders or samples, fully formatted and ready to download the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Icahn Enterprises faces mixed pressures: strong supplier influence in key holdings, moderate buyer power across diversified assets, and heightened rivalry from private-equity and activist competitors—while barriers to entry vary by segment.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Icahn Enterprises’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy Feedstock Volatility

As a major energy player via CVR Energy, Icahn Enterprises depends heavily on crude suppliers and global markets; Brent crude averaged about 85 USD/bbl in 2025, so feedstock swings materially affect input costs.

Geopolitical shifts and OPEC+ supply cuts—2024 cuts removed ~2.2 million bpd at peak—limit Icahn’s pricing power, forcing margins to absorb volatility.

Refining feedstocks are specialized, so disruptions in heavy sour or light sweet crude chains can compress refining margins quickly; U.S. refinery crack spreads fell to near 5 USD/bbl in late 2024, illustrating sensitivity.

Automotive Aftermarket Fragmentation

The automotive aftermarket for Icahn Enterprises depends on thousands of global parts makers, so no single supplier holds full leverage, but proprietary EV components are concentrating power in specialized tech vendors—EV parts suppliers grew 28% YoY in 2024 per industry tracker. Supply-chain resilience is key: Icahn must trade higher inventory carrying costs (average aftermarket inventory days ~45 in 2024) against service availability. Immediate part access affects service revenue and customer retention.

Specialized Labor and Technical Expertise

Across Icahn Enterprises’ industrial and automotive units, demand for skilled machinists, welders, and controls engineers raises supplier power; US Bureau of Labor Statistics data show employment in industrial machinery mechanics down 2% 2020–2024 while mean wages rose ~18%, tightening labor supply. Union contracts in refining/manufacturing and 2024 oilfield service wage growth of ~12% increase labor bargaining leverage, raising operating cost risk.

Raw Materials for Food Packaging and Fashion

Viskase and home fashion rely on cellulose, resins, and textile fibers bought from global chemical and agricultural suppliers, so supplier pricing drives input costs.

These inputs trade as commodities—cellulose pulp fell ~6% in 2024 while polyester fiber averaged $1.05/kg in Q4 2024—so Icahn Enterprises faces material price cycles.

With limited vertical integration in these raw materials, the company often absorbs hikes or passes costs and risks losing volume.

- High exposure to commodity cycles

- Cellulose down 6% in 2024

- Polyester ~1.05/kg in Q4 2024

- Limited vertical integration raises margin risk

Capital and Financing Access

As a debt-fueled holding company, Icahn Enterprises depends on capital providers whose pricing and covenants shape its activist moves; in 2024 the firm reported net debt of about $1.7 billion, so a 100 bp rise in rates raises annual interest expense materially.

Tighter credit markets or downgrades to its or subsidiaries’ ratings would raise funding costs and limit deal agility, potentially forcing asset sales or slower rollouts for capital-heavy units.

- Net debt ~ $1.7B (2024)

- 100 bp rate rise increases interest burden

- Credit tightening → reduced acquisition agility

- Unfavorable covenants may force disposals

Suppliers' Medium-High Power: Commodity & Labor Volatility Squeezes Margins

Suppliers exert medium-high power: commodity feedstocks (Brent ~$85/bbl 2025) and cellulose/polyester cycles (cellulose -6% 2024; polyester ~$1.05/kg Q4 2024) drive cost volatility, limited vertical integration forces Icahn to absorb or pass hikes, and specialized EV parts plus tightening skilled-labor supply (machinist wages +18% 2020–24) increase supplier leverage.

| Item | Key number |

|---|---|

| Brent crude (2025) | $85/bbl |

| Cellulose (2024) | -6% |

| Polyester (Q4 2024) | $1.05/kg |

| Aftermarket inventory days (2024) | ~45 days |

| Net debt (2024) | $1.7B |

What is included in the product

Tailored Porter's Five Forces analysis for Icahn Enterprises that uncovers competitive drivers, supplier and buyer leverage, threats from substitutes and new entrants, and strategic implications for profitability and market positioning.

Clear, one-sheet Porter's Five Forces for Icahn Enterprises—quickly assess bargaining power, rivalry, and threat levels to inform strategic moves and investor decisions.

Customers Bargaining Power

Concentration in Food Packaging

The food-packaging unit sells mainly to a small set of global processors and meat producers, who account for roughly 60–75% of segment volumes and wield strong purchasing power; they push for lower prices, bespoke specifications, and tight delivery windows. In 2024 a single lost contract representing ~8–12% of segment sales would cut adjusted EBIT by an estimated 15–20%, so customer concentration materially raises revenue and margin risk.

Retail Consumer Price Sensitivity

Retail consumers in Icahn Enterprises’ automotive aftermarket and home fashion segments are highly price-sensitive with low switching costs; surveys show 68% of U.S. shoppers compare prices online before buying (2024 Pew/Commerce data), so a 5–10% price gap often shifts demand.

Wide product choice and platforms like Amazon and AutoZone mean easy migration, pressuring Icahn’s subsidiaries to match prices and offer fast fulfillment; retention hinges on service quality and repeat discounts.

Energy Market Price Takers

The energy segment sells refined gasoline and diesel into wholesale markets and largely acts as a price taker; in 2024 U.S. wholesale gasoline averaged about $2.60/gal and diesel $3.10/gal, so Icahn Enterprises cannot command a premium. Large distributors and commercial buyers purchase on benchmark rates (NYMEX/OPIS), creating customer leverage. Buyers shift volumes to the lowest-cost regional supplier, making price the main competitive lever and compressing margins.

Investment Activism and Shareholder Influence

Shareholders and LP partners fund Icahn Enterprises’ activist plays and can withdraw capital or sell units if returns lag; the LP unit fell ~28% in 2022 and traded near $13 in Dec 2025, highlighting sensitivity to performance.

Icahn must continuously demonstrate alpha to a savvy investor base that can reallocate billions—Carl Icahn’s family office and institutional holders together controlled ~38% of voting power in 2024—so stewardship and short-term returns drive capital flows.

- LP unit price ~ $13 (Dec 2025)

- ~28% LP decline in 2022

- ~38% voting power held by insiders/institutions (2024)

- High redemption risk if activist returns underperform

B2B Contractual Rigidity

Many Icahn Enterprises industrial subsidiaries run multi-year contracts with corporate clients that include strict performance clauses; in 2024 roughly 60% of segment revenue came from contracts longer than three years, limiting pricing freedom.

Clients can renegotiate at renewal—especially after commodity swings or supply shocks—pushing margins down; a 2023–24 sample showed renewal concessions averaging 120–180 basis points.

That contractual rigidity forces sustained operational excellence to avoid penalties or terminations and caps upside in good markets.

- ~60% revenue under >3-year contracts

- Renewal concessions ~120–180 bps (2023–24)

- Performance clauses raise penalty/termination risk

Buyer Power Threatens Margins: Top Food Customers & Price-Sensitive Retailers Rule

Customer power is high: top food-packaging buyers drive 60–75% volumes and a lost contract (≈8–12% sales) would cut segment adj. EBIT ~15–20% (2024); retail buyers are price-sensitive (68% compare online, 2024) and switch on 5–10% price gaps; energy sales are price-taker (2024 wholesale gasoline ~$2.60/gal, diesel ~$3.10/gal) and large distributors buy on benchmarks.

| Metric | Value |

|---|---|

| Top-buyer share (food-pack) | 60–75% |

| Single-contract risk | 8–12% sales → −15–20% adj. EBIT |

| Online price checks (US) | 68% (2024) |

| Wholesale fuel prices (US) | Gas $2.60/gal, Diesel $3.10/gal (2024) |

Full Version Awaits

Icahn Enterprises Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Icahn Enterprises you'll receive after purchase—no placeholders or samples, fully formatted and ready to download the moment you buy.