iKang Group SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

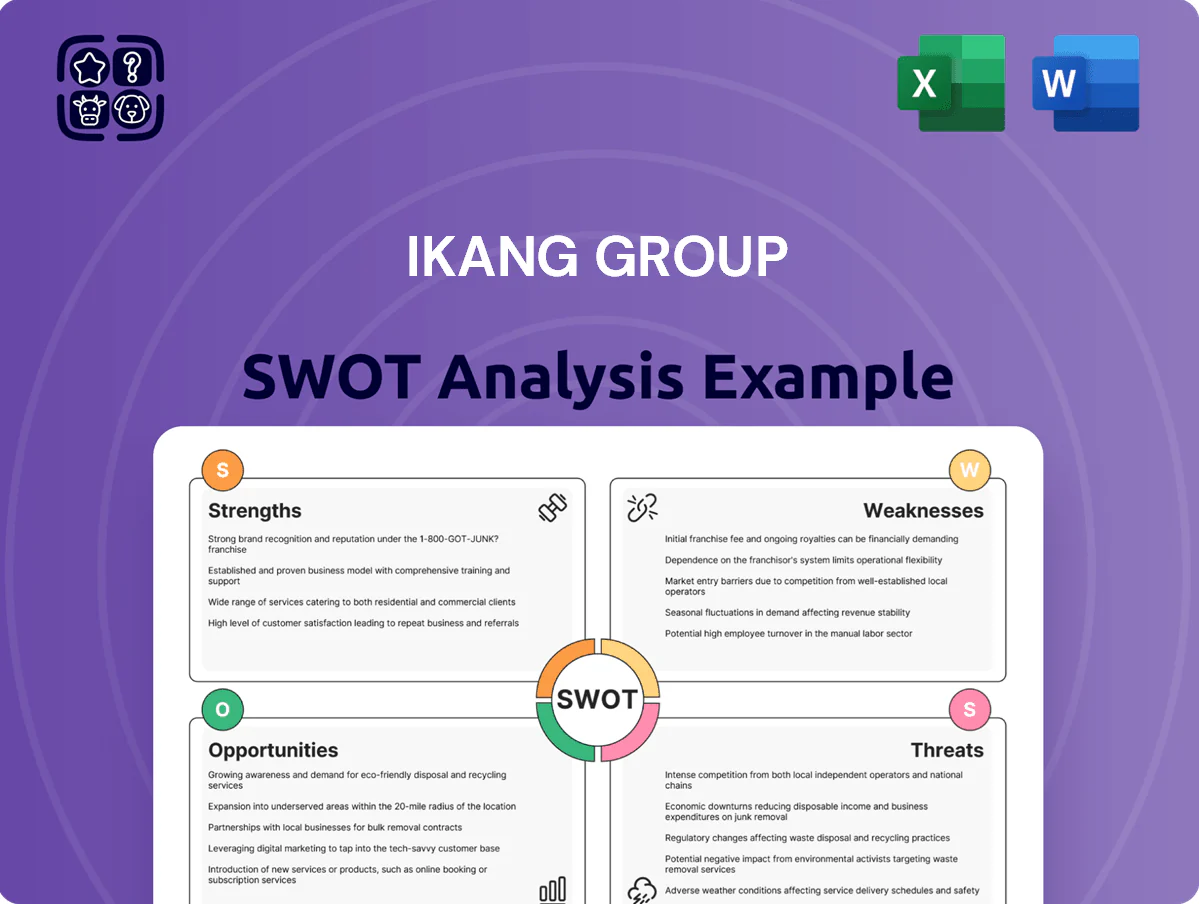

Strengths

Dominant Market Position and Brand Recognition

iKang Group holds the largest share among China’s private preventive healthcare chains, serving over 20 million customers by FY2024 and operating 1,100+ service locations, which makes the brand widely recognized for quality.

That reputation lets iKang charge premiums roughly 15–25% above local clinics for executive physicals and advanced screenings, supporting higher gross margins (FY2024 gross margin ~38%).

Strong brand equity, national scale, and established referral partnerships create a high barrier to entry in the high-end segment, limiting disruption from smaller rivals.

Advanced AI and Digital Integration

iKang’s iKang AI plus uses AI trained on over 25 million annual checkup records (2024 internal report) to lift diagnostic accuracy; pilot studies reported a 12–18% reduction in false positives for imaging-based screens. Leveraging big data across 240+ centers, the platform generates finer risk stratification and personalized follow-ups, strengthening appeal to tech-savvy urban consumers and supporting higher per-visit revenue and retention.

Robust Corporate Client Base

iKang Health Group (iKang) serves an extensive B2B roster, including dozens of Fortune 500 firms in China, which accounted for roughly 62% of its 2024 service revenue, giving predictable, recurring cash flows.

Long-term corporate contracts deliver retention rates above 85% and multi-year agreements; customized employee health packages drive higher per-client ARPU and reduce churn.

Comprehensive Nationwide Network

- 400+ centers, 60+ cities (Dec 2025)

- 18M outpatient visits (2024)

- RMB 1.2B procurement savings (FY2024)

High-End Service Differentiation

iKang targets the premium preventive-care niche with personalized packages, not mass-market checkups, driving higher ASPs (average selling price) and better margins; in 2024 the company reported a 28% gross margin in premium service lines versus ~15% in basic screening segments industry-wide.

The group offers advanced cardiovascular and oncology screening—CT coronary angiography, low-dose CT for lung cancer, PET-CT—for higher diagnostic yield and cross-sell; premium customers generate ~60% more revenue per visit.

This high-end focus shields iKang from lower-tier price wars and helped sustain revenue growth of 12% YoY in 2024 despite broader industry pricing pressure.

- Premium focus → higher ASPs, 28% gross margin

- Advanced imaging: CT, PET-CT, low-dose CT

- Premium patients = ~60% more revenue/visit

- Resilient: 12% revenue growth YoY 2024

iKang: China’s preventive-care leader — 400+ centers, 20M customers, 38% gross margin

iKang leads China’s private preventive care with 400+ centers in 60+ cities (Dec 2025), 18M outpatient visits (2024), 20M customers by FY2024, FY2024 gross margin ~38%, RMB1.2B procurement savings, 62% revenue from B2B, 85%+ corporate retention, and premium services driving ~28% gross margin and 12% YoY revenue growth (2024).

| Metric | Value |

|---|---|

| Centers/cities | 400+/60+ |

| Outpatient visits | 18M (2024) |

| Customers | 20M (FY2024) |

| Gross margin | ~38% (FY2024) |

| Procurement savings | RMB1.2B (FY2024) |

| B2B revenue | 62% (2024) |

| Corporate retention | 85%+ |

| Revenue growth | 12% YoY (2024) |

What is included in the product

Provides a concise SWOT overview of iKang Group, highlighting its core strengths and weaknesses, key market opportunities, and external threats to inform strategic decision-making and competitive positioning.

Provides a concise SWOT matrix for iKang Group to quickly align strategic decisions and communicate strengths, weaknesses, opportunities, and threats to stakeholders.

Weaknesses

High Capital Expenditure and Operational Costs

Variable Service Quality Across Locations

Heavy Reliance on the Domestic Market

iKang Group generates over 95% of revenue from mainland China (2024 audited results: RMB 3.2bn of RMB 3.35bn total), so it’s highly exposed to local cycles.

A Chinese GDP growth slowdown to 5.2% in 2024 and corporate cost-cutting can cut employer-paid health benefits, hurting demand for iKang’s corporate screening services.

With minimal international ops, iKang lacks geographic hedges against domestic systemic shocks, raising cash-flow and valuation volatility.

Challenges in Retaining Specialized Talent

iKang faces intense competition for qualified doctors, radiologists, and nurses in China, where public hospitals employ over 70% of specialists; in 2024 private clinics reported vacancy rates up to 18% for radiology roles.

The company must match public-hospital pay and offer sign-on bonuses—iKang’s 2023 staff costs rose 12% year-over-year to RMB 1.1 billion, reflecting this pressure.

High turnover or shortages can delay scans, raise per-patient costs, and degrade diagnostic accuracy, directly affecting revenue and reputation.

- Vacancy rates: radiology ~18% (2024)

- Staff costs: +12% to RMB 1.1bn (2023)

- Public hospitals hold >70% of specialists

Complex Corporate Debt Structure

- Net debt ~RMB 2.1bn (FY2023)

- Limits on M&A and capex

- High financing costs raise WACC

High capex, staff shortages and China concentration squeeze margins and raise cyclic risk

| Metric | Value |

|---|---|

| Capex (FY2024) | RMB 600–800m |

| R&D/IT (FY2024) | RMB 150m |

| Revenue concentration (2024) | 95% China (RMB 3.2bn/3.35bn) |

| Staff costs (2023) | RMB 1.1bn (+12%) |

| Radiology vacancy (2024) | ~18% |

| Net debt (FY2023) | RMB 2.1bn |

Preview the Actual Deliverable

iKang Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live excerpt of the complete, editable file that becomes available after checkout. The content shown is the real report you'll download post-purchase, structured and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Strengths

Dominant Market Position and Brand Recognition

iKang Group holds the largest share among China’s private preventive healthcare chains, serving over 20 million customers by FY2024 and operating 1,100+ service locations, which makes the brand widely recognized for quality.

That reputation lets iKang charge premiums roughly 15–25% above local clinics for executive physicals and advanced screenings, supporting higher gross margins (FY2024 gross margin ~38%).

Strong brand equity, national scale, and established referral partnerships create a high barrier to entry in the high-end segment, limiting disruption from smaller rivals.

Advanced AI and Digital Integration

iKang’s iKang AI plus uses AI trained on over 25 million annual checkup records (2024 internal report) to lift diagnostic accuracy; pilot studies reported a 12–18% reduction in false positives for imaging-based screens. Leveraging big data across 240+ centers, the platform generates finer risk stratification and personalized follow-ups, strengthening appeal to tech-savvy urban consumers and supporting higher per-visit revenue and retention.

Robust Corporate Client Base

iKang Health Group (iKang) serves an extensive B2B roster, including dozens of Fortune 500 firms in China, which accounted for roughly 62% of its 2024 service revenue, giving predictable, recurring cash flows.

Long-term corporate contracts deliver retention rates above 85% and multi-year agreements; customized employee health packages drive higher per-client ARPU and reduce churn.

Comprehensive Nationwide Network

- 400+ centers, 60+ cities (Dec 2025)

- 18M outpatient visits (2024)

- RMB 1.2B procurement savings (FY2024)

High-End Service Differentiation

iKang targets the premium preventive-care niche with personalized packages, not mass-market checkups, driving higher ASPs (average selling price) and better margins; in 2024 the company reported a 28% gross margin in premium service lines versus ~15% in basic screening segments industry-wide.

The group offers advanced cardiovascular and oncology screening—CT coronary angiography, low-dose CT for lung cancer, PET-CT—for higher diagnostic yield and cross-sell; premium customers generate ~60% more revenue per visit.

This high-end focus shields iKang from lower-tier price wars and helped sustain revenue growth of 12% YoY in 2024 despite broader industry pricing pressure.

- Premium focus → higher ASPs, 28% gross margin

- Advanced imaging: CT, PET-CT, low-dose CT

- Premium patients = ~60% more revenue/visit

- Resilient: 12% revenue growth YoY 2024

iKang: China’s preventive-care leader — 400+ centers, 20M customers, 38% gross margin

iKang leads China’s private preventive care with 400+ centers in 60+ cities (Dec 2025), 18M outpatient visits (2024), 20M customers by FY2024, FY2024 gross margin ~38%, RMB1.2B procurement savings, 62% revenue from B2B, 85%+ corporate retention, and premium services driving ~28% gross margin and 12% YoY revenue growth (2024).

| Metric | Value |

|---|---|

| Centers/cities | 400+/60+ |

| Outpatient visits | 18M (2024) |

| Customers | 20M (FY2024) |

| Gross margin | ~38% (FY2024) |

| Procurement savings | RMB1.2B (FY2024) |

| B2B revenue | 62% (2024) |

| Corporate retention | 85%+ |

| Revenue growth | 12% YoY (2024) |

What is included in the product

Provides a concise SWOT overview of iKang Group, highlighting its core strengths and weaknesses, key market opportunities, and external threats to inform strategic decision-making and competitive positioning.

Provides a concise SWOT matrix for iKang Group to quickly align strategic decisions and communicate strengths, weaknesses, opportunities, and threats to stakeholders.

Weaknesses

High Capital Expenditure and Operational Costs

Variable Service Quality Across Locations

Heavy Reliance on the Domestic Market

iKang Group generates over 95% of revenue from mainland China (2024 audited results: RMB 3.2bn of RMB 3.35bn total), so it’s highly exposed to local cycles.

A Chinese GDP growth slowdown to 5.2% in 2024 and corporate cost-cutting can cut employer-paid health benefits, hurting demand for iKang’s corporate screening services.

With minimal international ops, iKang lacks geographic hedges against domestic systemic shocks, raising cash-flow and valuation volatility.

Challenges in Retaining Specialized Talent

iKang faces intense competition for qualified doctors, radiologists, and nurses in China, where public hospitals employ over 70% of specialists; in 2024 private clinics reported vacancy rates up to 18% for radiology roles.

The company must match public-hospital pay and offer sign-on bonuses—iKang’s 2023 staff costs rose 12% year-over-year to RMB 1.1 billion, reflecting this pressure.

High turnover or shortages can delay scans, raise per-patient costs, and degrade diagnostic accuracy, directly affecting revenue and reputation.

- Vacancy rates: radiology ~18% (2024)

- Staff costs: +12% to RMB 1.1bn (2023)

- Public hospitals hold >70% of specialists

Complex Corporate Debt Structure

- Net debt ~RMB 2.1bn (FY2023)

- Limits on M&A and capex

- High financing costs raise WACC

High capex, staff shortages and China concentration squeeze margins and raise cyclic risk

| Metric | Value |

|---|---|

| Capex (FY2024) | RMB 600–800m |

| R&D/IT (FY2024) | RMB 150m |

| Revenue concentration (2024) | 95% China (RMB 3.2bn/3.35bn) |

| Staff costs (2023) | RMB 1.1bn (+12%) |

| Radiology vacancy (2024) | ~18% |

| Net debt (FY2023) | RMB 2.1bn |

Preview the Actual Deliverable

iKang Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live excerpt of the complete, editable file that becomes available after checkout. The content shown is the real report you'll download post-purchase, structured and ready to use.