Iluka PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our tailored PESTLE Analysis for Iluka—uncover how political shifts, commodity cycles, environmental regulation, and tech trends will shape its strategy and valuation; ideal for investors, advisors, and strategists. Buy the full report for a complete, editable breakdown and actionable insights you can apply immediately.

Political factors

Strategic critical minerals support

The Australian government has extended the Critical Minerals Strategy through 2025, creating a policy tailwind for Iluka as a domestic processor of rare earths; Canberra has committed over A$2.3 billion in targeted loan facilities and grants to 2025 to support downstream projects. The Eneabba rare earths refinery received accelerated approvals and access to concessional financing, reducing time-to-FID and capital risk. Alignment with national security priorities secures long-term offtake confidence and potential sovereign-backed financing for Iluka's downstream expansion.

Geopolitical supply chain diversification

Geopolitical tensions and China-plus-one strategies have raised Iluka’s political value as a non-Chinese supplier of rare earths and zircon, with global governments aiming to cut China’s >80% control of rare-earth refining. Western efforts to secure permanent-magnet supply chains for EVs and defense—backed by US CHIPS/IRA funding and EU critical-raw-materials initiatives—boost Iluka’s leverage for long-term off-take contracts.

Sovereign risk in international jurisdictions

Iluka’s core asset base is Australia-centric, yet legacy interests and exploration targets in jurisdictions like Sierra Leone and Madagascar carry sovereign risk; between 2020–2024, resource disputes in Africa led to an average 18–25% write-down on foreign mining JV valuations. Political shifts or mining-code revisions can materially affect exit values and contingent liabilities, so real-time monitoring of emerging-market political indices (e.g., World Bank political stability scores) is essential to safeguard shareholder value and operations.

Trade policy and tariff fluctuations

Trade relations between Australia and key buyers, especially China (accounting for about 35% of Iluka's exports in 2024), heavily affect demand for mineral sands; China’s 2023–24 downturn in pigment demand cut seaborne ilmenite/titanomagnetite prices by ~12% YoY.

Tariffs or barriers on ceramics or TiO2 pigments would disrupt flows and pricing—global TiO2 capacity additions lifted supply, pressuring margins in 2024.

Iluka mitigates risk by diversifying customers across North America, Europe and Asia; in 2024 ~40% of revenue came from non-China markets.

- China ~35% of exports (2024)

- Non-China revenue ~40% (2024)

- Seaborne ilmenite/Ti prices down ~12% YoY (2023–24)

Governmental focus on energy transition

Policy shifts to renewables have driven demand for minerals used in wind turbines and electric motors; global wind capacity additions hit 114 GW in 2024 and EV sales surpassed 15 million units, increasing rare earths demand.

Iluka, with its 2024 rare earths pilot and target to scale production, stands to benefit from government mandates and incentives supporting decarbonisation.

Ongoing political pressure to meet 2050 net-zero targets—over 130 countries with net-zero commitments—provides a sustained policy tailwind for Iluka’s rare earths segment.

- 114 GW global wind additions (2024)

- 15M+ EVs sold (2024)

- 130+ countries with net-zero pledges

- Iluka scaling rare earths production in 2024

Iluka gets A$2.3bn boost as rare-earths push gains strategic premium amid China risk

Strong Australian policy support and A$2.3bn+ funding to 2025 bolsters Iluka’s downstream rare-earths plans; Eneabba approvals shortened time-to-FID and financing risk. Geopolitical push to diversify from China (China ~35% exports, non-China ~40% revenue in 2024) raises strategic premium for Iluka’s supply. Emerging-market asset sovereignty remains a material risk; seaborne ilmenite/Ti prices fell ~12% YoY (2023–24).

| Metric | 2024/2025 |

|---|---|

| A$ funding to 2025 | A$2.3bn+ |

| China share of exports | ~35% |

| Non-China revenue | ~40% |

| Seaborne ilmenite/Ti price change | -12% YoY (2023–24) |

| Global wind additions | 114 GW (2024) |

| EV sales | 15M+ (2024) |

What is included in the product

Explores how macro-environmental forces uniquely impact Iluka across Political, Economic, Social, Technological, Environmental and Legal dimensions, each backed by current data and trends to identify threats and opportunities for executives, investors and strategists.

Condenses Iluka's PESTLE into a concise, editable summary that stakeholders can drop into presentations, share across teams, and use in planning sessions to quickly align on external risks and strategic implications.

Economic factors

Rare earths market price volatility

Iluka’s economic performance is increasingly linked to neodymium-praseodymium (NdPr) prices, which swung between US$45–90/kg NdPr oxide in 2023–2024, driving revenue sensitivity as Eneabba refinery nears late-2025 commissioning.

With Eneabba set to add significant NdPr output, price cycles are forecasted to explain a majority of short-term EBITDA volatility; a 10% NdPr price move could alter Iluka’s FY26 EBITDA by an estimated A$50–120m based on public guidance.

Management will need sophisticated hedging, staged inventory build-ups and offtake contracts to smooth cash flow and protect the balance sheet against the demonstrated high intra-year NdPr volatility.

Global construction and industrial demand

Demand for zircon and synthetic rutile tracks global GDP and construction: world GDP grew 3.5% in 2024 and global construction output rose ~2.8%, supporting mineral sands pricing, while a 2023–24 slowdown in China trimmed ceramics demand and pressured Iluka earnings. Economic contractions in key markets can cut high-end pigment and ceramics volumes, reducing Iluka's core revenue, which saw zircon sales revenue decline 12% YoY in FY2024. Ongoing urbanization—UN projects 2.4 billion more urban residents by 2050, largely in Asia and Africa—provides a structural floor for long-term zircon and titania feedstock consumption.

Operational cost inflation

Persistent inflation through 2025 pushed Australian mining input costs up ~8–12% year-on-year; Iluka reported unit cash costs rising ~10% in FY2024 driven by labor and energy.

Diesel prices averaged ~A$1.80/L in 2024 (up ~20% vs 2022) and specialized flotation chemicals costs rose ~15–25%, pressuring mineral separation margins.

Iluka’s response includes cost-containment and efficiency programs targeting ~US$50–70/tonne savings and productivity gains to protect EBITDA amid these macro headwinds.

Currency exchange rate sensitivity

As an Australian-based miner selling a large share of zircon and rutile in US dollars, Iluka’s FY2024 revenue exposure meant a 10% AUD appreciation versus USD would have cut AUD-reported earnings by roughly 8–12%, compressing margins as domestic costs are AUD-denominated.

Iluka reported using hedging and natural offset strategies—FY2024 hedges covered a portion of forecast USD receipts—and maintains treasury programs, but persistent macro shifts (e.g., 2023–24 AUD/USD range 0.62–0.74) keep translation risk material.

- FY2024 AUD/USD range 0.62–0.74

- 10% AUD rise ≈ 8–12% hit to AUD-reported earnings

- Hedging programs partially cover forecast USD receipts

Interest rate impacts on capital projects

The recent high-rate environment raised Iluka's weighted average cost of capital, pushing estimated project financing costs for Eneabba-style refineries up roughly 200–300 basis points versus 2020 levels; higher debt servicing can delay start dates or scale reductions for multi-year capital projects.

Investors track Iluka's net debt/EBITDA (1.1x FY2024) and debt/equity (~0.25 at end-2024) to assess reliance on internal cash flow—FY2024 operating cash flow was A$402m—versus external borrowing for growth.

- Higher rates add ~A$X–A$Y annual financing cost per A$100m borrowed

- Net debt/EBITDA 1.1x (FY2024)

- Debt/equity ~0.25 (end-2024)

- Operating cash flow A$402m (FY2024)

Iluka earnings hinge on volatile NdPr prices—10% move could swing FY26 EBITDA A$50–120m

Iluka's earnings are highly NdPr-price sensitive (US$45–90/kg in 2023–24); Eneabba (late-2025) amplifies revenue volatility—10% NdPr move ≈ A$50–120m FY26 EBITDA impact. FY2024: net debt/EBITDA 1.1x, debt/equity ~0.25, operating cash flow A$402m; unit costs +~10% YoY; AUD/USD 0.62–0.74 raised translation risk; higher rates added ~200–300bp to project finance costs.

| Metric | Value |

|---|---|

| NdPr (2023–24) | US$45–90/kg |

| Net debt/EBITDA | 1.1x |

| Op cash flow (FY2024) | A$402m |

Preview the Actual Deliverable

Iluka PESTLE Analysis

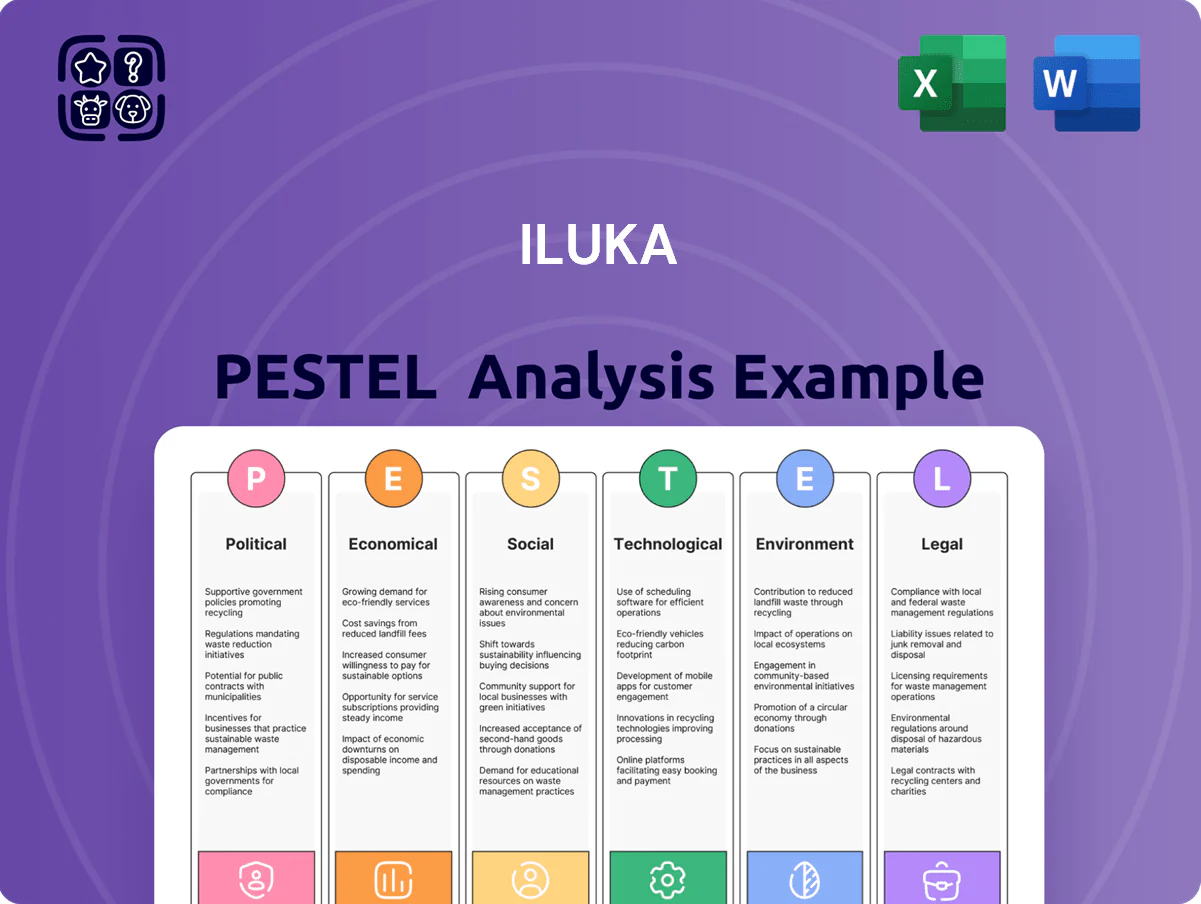

The preview shown here is the exact Iluka PESTLE document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying, delivered exactly as shown with no placeholders or teasers. The layout, content, and structure visible here are identical to the downloadable file you’ll get immediately after payment. Everything displayed is part of the final, professionally structured report.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our tailored PESTLE Analysis for Iluka—uncover how political shifts, commodity cycles, environmental regulation, and tech trends will shape its strategy and valuation; ideal for investors, advisors, and strategists. Buy the full report for a complete, editable breakdown and actionable insights you can apply immediately.

Political factors

Strategic critical minerals support

The Australian government has extended the Critical Minerals Strategy through 2025, creating a policy tailwind for Iluka as a domestic processor of rare earths; Canberra has committed over A$2.3 billion in targeted loan facilities and grants to 2025 to support downstream projects. The Eneabba rare earths refinery received accelerated approvals and access to concessional financing, reducing time-to-FID and capital risk. Alignment with national security priorities secures long-term offtake confidence and potential sovereign-backed financing for Iluka's downstream expansion.

Geopolitical supply chain diversification

Geopolitical tensions and China-plus-one strategies have raised Iluka’s political value as a non-Chinese supplier of rare earths and zircon, with global governments aiming to cut China’s >80% control of rare-earth refining. Western efforts to secure permanent-magnet supply chains for EVs and defense—backed by US CHIPS/IRA funding and EU critical-raw-materials initiatives—boost Iluka’s leverage for long-term off-take contracts.

Sovereign risk in international jurisdictions

Iluka’s core asset base is Australia-centric, yet legacy interests and exploration targets in jurisdictions like Sierra Leone and Madagascar carry sovereign risk; between 2020–2024, resource disputes in Africa led to an average 18–25% write-down on foreign mining JV valuations. Political shifts or mining-code revisions can materially affect exit values and contingent liabilities, so real-time monitoring of emerging-market political indices (e.g., World Bank political stability scores) is essential to safeguard shareholder value and operations.

Trade policy and tariff fluctuations

Trade relations between Australia and key buyers, especially China (accounting for about 35% of Iluka's exports in 2024), heavily affect demand for mineral sands; China’s 2023–24 downturn in pigment demand cut seaborne ilmenite/titanomagnetite prices by ~12% YoY.

Tariffs or barriers on ceramics or TiO2 pigments would disrupt flows and pricing—global TiO2 capacity additions lifted supply, pressuring margins in 2024.

Iluka mitigates risk by diversifying customers across North America, Europe and Asia; in 2024 ~40% of revenue came from non-China markets.

- China ~35% of exports (2024)

- Non-China revenue ~40% (2024)

- Seaborne ilmenite/Ti prices down ~12% YoY (2023–24)

Governmental focus on energy transition

Policy shifts to renewables have driven demand for minerals used in wind turbines and electric motors; global wind capacity additions hit 114 GW in 2024 and EV sales surpassed 15 million units, increasing rare earths demand.

Iluka, with its 2024 rare earths pilot and target to scale production, stands to benefit from government mandates and incentives supporting decarbonisation.

Ongoing political pressure to meet 2050 net-zero targets—over 130 countries with net-zero commitments—provides a sustained policy tailwind for Iluka’s rare earths segment.

- 114 GW global wind additions (2024)

- 15M+ EVs sold (2024)

- 130+ countries with net-zero pledges

- Iluka scaling rare earths production in 2024

Iluka gets A$2.3bn boost as rare-earths push gains strategic premium amid China risk

Strong Australian policy support and A$2.3bn+ funding to 2025 bolsters Iluka’s downstream rare-earths plans; Eneabba approvals shortened time-to-FID and financing risk. Geopolitical push to diversify from China (China ~35% exports, non-China ~40% revenue in 2024) raises strategic premium for Iluka’s supply. Emerging-market asset sovereignty remains a material risk; seaborne ilmenite/Ti prices fell ~12% YoY (2023–24).

| Metric | 2024/2025 |

|---|---|

| A$ funding to 2025 | A$2.3bn+ |

| China share of exports | ~35% |

| Non-China revenue | ~40% |

| Seaborne ilmenite/Ti price change | -12% YoY (2023–24) |

| Global wind additions | 114 GW (2024) |

| EV sales | 15M+ (2024) |

What is included in the product

Explores how macro-environmental forces uniquely impact Iluka across Political, Economic, Social, Technological, Environmental and Legal dimensions, each backed by current data and trends to identify threats and opportunities for executives, investors and strategists.

Condenses Iluka's PESTLE into a concise, editable summary that stakeholders can drop into presentations, share across teams, and use in planning sessions to quickly align on external risks and strategic implications.

Economic factors

Rare earths market price volatility

Iluka’s economic performance is increasingly linked to neodymium-praseodymium (NdPr) prices, which swung between US$45–90/kg NdPr oxide in 2023–2024, driving revenue sensitivity as Eneabba refinery nears late-2025 commissioning.

With Eneabba set to add significant NdPr output, price cycles are forecasted to explain a majority of short-term EBITDA volatility; a 10% NdPr price move could alter Iluka’s FY26 EBITDA by an estimated A$50–120m based on public guidance.

Management will need sophisticated hedging, staged inventory build-ups and offtake contracts to smooth cash flow and protect the balance sheet against the demonstrated high intra-year NdPr volatility.

Global construction and industrial demand

Demand for zircon and synthetic rutile tracks global GDP and construction: world GDP grew 3.5% in 2024 and global construction output rose ~2.8%, supporting mineral sands pricing, while a 2023–24 slowdown in China trimmed ceramics demand and pressured Iluka earnings. Economic contractions in key markets can cut high-end pigment and ceramics volumes, reducing Iluka's core revenue, which saw zircon sales revenue decline 12% YoY in FY2024. Ongoing urbanization—UN projects 2.4 billion more urban residents by 2050, largely in Asia and Africa—provides a structural floor for long-term zircon and titania feedstock consumption.

Operational cost inflation

Persistent inflation through 2025 pushed Australian mining input costs up ~8–12% year-on-year; Iluka reported unit cash costs rising ~10% in FY2024 driven by labor and energy.

Diesel prices averaged ~A$1.80/L in 2024 (up ~20% vs 2022) and specialized flotation chemicals costs rose ~15–25%, pressuring mineral separation margins.

Iluka’s response includes cost-containment and efficiency programs targeting ~US$50–70/tonne savings and productivity gains to protect EBITDA amid these macro headwinds.

Currency exchange rate sensitivity

As an Australian-based miner selling a large share of zircon and rutile in US dollars, Iluka’s FY2024 revenue exposure meant a 10% AUD appreciation versus USD would have cut AUD-reported earnings by roughly 8–12%, compressing margins as domestic costs are AUD-denominated.

Iluka reported using hedging and natural offset strategies—FY2024 hedges covered a portion of forecast USD receipts—and maintains treasury programs, but persistent macro shifts (e.g., 2023–24 AUD/USD range 0.62–0.74) keep translation risk material.

- FY2024 AUD/USD range 0.62–0.74

- 10% AUD rise ≈ 8–12% hit to AUD-reported earnings

- Hedging programs partially cover forecast USD receipts

Interest rate impacts on capital projects

The recent high-rate environment raised Iluka's weighted average cost of capital, pushing estimated project financing costs for Eneabba-style refineries up roughly 200–300 basis points versus 2020 levels; higher debt servicing can delay start dates or scale reductions for multi-year capital projects.

Investors track Iluka's net debt/EBITDA (1.1x FY2024) and debt/equity (~0.25 at end-2024) to assess reliance on internal cash flow—FY2024 operating cash flow was A$402m—versus external borrowing for growth.

- Higher rates add ~A$X–A$Y annual financing cost per A$100m borrowed

- Net debt/EBITDA 1.1x (FY2024)

- Debt/equity ~0.25 (end-2024)

- Operating cash flow A$402m (FY2024)

Iluka earnings hinge on volatile NdPr prices—10% move could swing FY26 EBITDA A$50–120m

Iluka's earnings are highly NdPr-price sensitive (US$45–90/kg in 2023–24); Eneabba (late-2025) amplifies revenue volatility—10% NdPr move ≈ A$50–120m FY26 EBITDA impact. FY2024: net debt/EBITDA 1.1x, debt/equity ~0.25, operating cash flow A$402m; unit costs +~10% YoY; AUD/USD 0.62–0.74 raised translation risk; higher rates added ~200–300bp to project finance costs.

| Metric | Value |

|---|---|

| NdPr (2023–24) | US$45–90/kg |

| Net debt/EBITDA | 1.1x |

| Op cash flow (FY2024) | A$402m |

Preview the Actual Deliverable

Iluka PESTLE Analysis

The preview shown here is the exact Iluka PESTLE document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying, delivered exactly as shown with no placeholders or teasers. The layout, content, and structure visible here are identical to the downloadable file you’ll get immediately after payment. Everything displayed is part of the final, professionally structured report.