IMA Klessmann GmbH Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

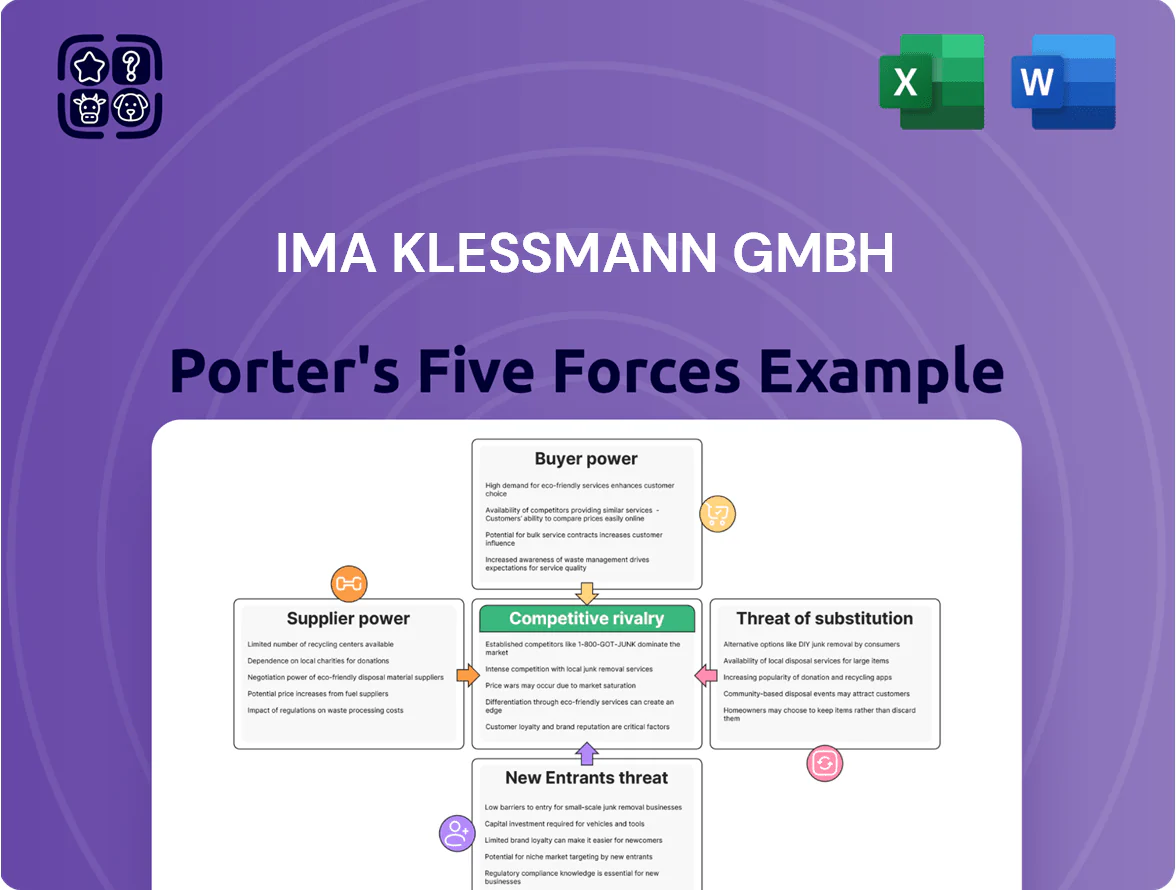

IMA Klessmann GmbH faces moderate supplier power and differentiated buyer demands, while incumbents and substitutes shape a competitive landscape that rewards innovation in packaging machinery and automation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore IMA Klessmann GmbH’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component and CNC Control Providers

Reliance on high-tech electronic components and specialized CNC control systems gives a few global suppliers strong leverage over IMA Klessmann, especially for low-volume, proprietary parts; global industrial control supplier concentration (top 5 firms) exceeds 60% in 2024.

As IMA Klessmann adds Industry 4.0 features—edge computing and OPC UA integration—dependency on specialist vendors rises, increasing switch costs and lead times, often 12–20 weeks for custom controllers.

Being part of HOMAG Group (reported 2024 revenue ~1.4 billion EUR) provides volume-based bargaining power, enabling price discounts of 5–15% and prioritized support that mitigates, but does not eliminate, supplier power.

Raw Material Price Volatility

Suppliers of high-grade steel and specialized alloys hold moderate bargaining power; global steel plate benchmark HRC rose 22% in 2024 and spot nickel surged 35% by Q3 2025, driving input cost swings for heavy machinery. Geopolitical tensions (Russia-Ukraine, China trade controls) tightened supply, lifting alloy premiums ~12% year-on-year to late 2025. IMA Klessmann must hedge and pass-through costs to protect margins on multi-million-euro equipment contracts.

Specialized Software and IoT Developers

Energy and Utility Providers

- Germany industrial price ~EUR 0.18/kWh (2024)

- EU industrial avg ~EUR 0.12/kWh (2024)

- Grid fees and renewables surcharges sustain inflexibility

- On-site generation reduces but requires capex

Highly Skilled Engineering Labor

The scarcity of specialized mechanical and software engineers in Germany’s industrial sector raises supplier power; Germany reported a 2024 shortfall of roughly 200,000 STEM workers, tightening hiring for IMA Klessmann GmbH.

Competitive labor markets give engineers leverage on wages and conditions—median salary for senior mechanical engineers in Germany rose to about €75,000 in 2024, driving payroll pressure.

Retaining top talent is critical to keep the firm’s precision reputation and R&D edge; turnover costs can exceed 1.5x annual salary and threaten delivery timelines.

- ~200,000 STEM worker shortfall in Germany (2024)

- Median senior mechanical engineer pay ≈ €75,000 (2024)

- Turnover cost >1.5x annual salary, risking precision and timelines

Suppliers wield strong leverage: long lead times, high input costs, and STEM squeeze

Suppliers hold moderate-to-high power: concentrated electronics and IoT vendors, long lead times (12–20 weeks), and high-cost steel/alloys push input volatility; HOMAG scale trims costs (5–15% discounts) but can’t remove supplier leverage; German industrial electricity (~EUR 0.18/kWh in 2024) and STEM shortages (~200,000 gap; €75k median senior engineer pay) add recurring pressure.

| Item | 2024–25 Metric |

|---|---|

| Electronics supplier concentration | Top 5 >60% (2024) |

| Custom controller lead time | 12–20 weeks |

| HOMAG pricing leverage | 5–15% discounts |

| German industrial electricity | EUR 0.18/kWh (2024) |

| STEM shortfall Germany | ~200,000 (2024) |

What is included in the product

Tailored exclusively for IMA Klessmann GmbH, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A concise, one-sheet Porter's Five Forces view for IMA Klessmann—instantly shows competitive pressures and strategic levers to ease decision-making.

Customers Bargaining Power

Large Scale Industrial Furniture Manufacturers

Major global furniture producers hold high bargaining power: the top 10 OEMs account for ~38% of global contract volume (2024 UN Comtrade-based estimate), letting them negotiate price cuts of 5–12% and bespoke tooling fees waived for multi-year deals.

Increasing Demand for Integrated Smart Factories

Customers now prefer full-service automation partners over standalone machine vendors, and 62% of German manufacturers surveyed in 2024 said they prioritize integrated smart-factory solutions, boosting buyer leverage.

This shift lets buyers demand deeper systems integration and bundled after-sales support within the initial contract, often reallocating 15–25% of project budgets to service and software modules.

System complexity gives purchasers the right to ask for strict performance guarantees and 5–10 year maintenance agreements; contract terms increasingly include uptime SLAs of 99.5% or higher.

Availability of Alternative Global Brands

The availability of global competitors like Biesse (2024 revenue €1.2bn) and SCM Group (2023 revenue ~€800m) gives IMA Klessmann customers clear alternatives, raising buyer bargaining power.

Buyers leverage switching threats to extract better prices, service SLAs, or extra features, pressuring margins—industry churn rates hit ~8% in 2024 for panel-processing OEMs.

That pushes IMA Klessmann to prioritize customer satisfaction scores and tech differentiation; R&D spend across peers averages 4–6% of revenue, a benchmark it must meet.

Transparency in Performance and Pricing

In 2025 buyers access extensive data on machine uptime, energy use and total cost of ownership (TCO), with marketplaces like MachineryCloud reporting 42% of industrial buyers using third-party benchmarks.

Information symmetry lets customers demand empirical proof—field performance logs, ISO 50001 energy metrics, and lifecycle cost models—to negotiate prices and SLAs.

IMA Klessmann must publish transparent test data and superior specs; firms showing 10–15% lower energy intensity win faster procurement cycles.

Sensitivity to Economic Cycles

The demand for IMA Klessmann GmbH’s woodworking machinery tracks construction and furniture spending; global furniture production fell 3.4% in 2023, raising buyer leverage as firms delay capex or push for bigger discounts.

In recessions customers can extract better terms, so IMA Klessmann must offer flexible financing, staged payments, and short-term discounts to protect backlog and smooth revenue.

- 2023 furniture output -3.4% (UN Comtrade)

- Buyers delay capex → higher discount pressure

- Flexible financing preserves orders

Buyers wield power: OEM concentration, churn & integration demand force IMA Klessmann action

Buyers have high leverage: top 10 OEMs ~38% contract volume (2024), panel-OEM churn ~8% (2024), 62% of German manufacturers prioritize integrated solutions (2024), 42% use third‑party benchmarks (2025). Recession sensitivity: global furniture output -3.4% (2023). IMA Klessmann must meet 4–6% R&D spend, publish uptime/TCO data, and offer flexible financing.

| Metric | Value |

|---|---|

| Top 10 OEM share | ~38% (2024) |

| German buyers favor integration | 62% (2024) |

| Buyers using benchmarks | 42% (2025) |

| Panel-OEM churn | ~8% (2024) |

| Furniture output | -3.4% (2023) |

| Peer R&D target | 4–6% revenue |

What You See Is What You Get

IMA Klessmann GmbH Porter's Five Forces Analysis

This preview shows the exact IMA Klessmann GmbH Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready to use. The document displayed is the final, professionally written file included in your download; once payment is completed, you gain instant access to this same deliverable. Use it as-is for strategic planning, presentations, or internal review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

IMA Klessmann GmbH faces moderate supplier power and differentiated buyer demands, while incumbents and substitutes shape a competitive landscape that rewards innovation in packaging machinery and automation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore IMA Klessmann GmbH’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component and CNC Control Providers

Reliance on high-tech electronic components and specialized CNC control systems gives a few global suppliers strong leverage over IMA Klessmann, especially for low-volume, proprietary parts; global industrial control supplier concentration (top 5 firms) exceeds 60% in 2024.

As IMA Klessmann adds Industry 4.0 features—edge computing and OPC UA integration—dependency on specialist vendors rises, increasing switch costs and lead times, often 12–20 weeks for custom controllers.

Being part of HOMAG Group (reported 2024 revenue ~1.4 billion EUR) provides volume-based bargaining power, enabling price discounts of 5–15% and prioritized support that mitigates, but does not eliminate, supplier power.

Raw Material Price Volatility

Suppliers of high-grade steel and specialized alloys hold moderate bargaining power; global steel plate benchmark HRC rose 22% in 2024 and spot nickel surged 35% by Q3 2025, driving input cost swings for heavy machinery. Geopolitical tensions (Russia-Ukraine, China trade controls) tightened supply, lifting alloy premiums ~12% year-on-year to late 2025. IMA Klessmann must hedge and pass-through costs to protect margins on multi-million-euro equipment contracts.

Specialized Software and IoT Developers

Energy and Utility Providers

- Germany industrial price ~EUR 0.18/kWh (2024)

- EU industrial avg ~EUR 0.12/kWh (2024)

- Grid fees and renewables surcharges sustain inflexibility

- On-site generation reduces but requires capex

Highly Skilled Engineering Labor

The scarcity of specialized mechanical and software engineers in Germany’s industrial sector raises supplier power; Germany reported a 2024 shortfall of roughly 200,000 STEM workers, tightening hiring for IMA Klessmann GmbH.

Competitive labor markets give engineers leverage on wages and conditions—median salary for senior mechanical engineers in Germany rose to about €75,000 in 2024, driving payroll pressure.

Retaining top talent is critical to keep the firm’s precision reputation and R&D edge; turnover costs can exceed 1.5x annual salary and threaten delivery timelines.

- ~200,000 STEM worker shortfall in Germany (2024)

- Median senior mechanical engineer pay ≈ €75,000 (2024)

- Turnover cost >1.5x annual salary, risking precision and timelines

Suppliers wield strong leverage: long lead times, high input costs, and STEM squeeze

Suppliers hold moderate-to-high power: concentrated electronics and IoT vendors, long lead times (12–20 weeks), and high-cost steel/alloys push input volatility; HOMAG scale trims costs (5–15% discounts) but can’t remove supplier leverage; German industrial electricity (~EUR 0.18/kWh in 2024) and STEM shortages (~200,000 gap; €75k median senior engineer pay) add recurring pressure.

| Item | 2024–25 Metric |

|---|---|

| Electronics supplier concentration | Top 5 >60% (2024) |

| Custom controller lead time | 12–20 weeks |

| HOMAG pricing leverage | 5–15% discounts |

| German industrial electricity | EUR 0.18/kWh (2024) |

| STEM shortfall Germany | ~200,000 (2024) |

What is included in the product

Tailored exclusively for IMA Klessmann GmbH, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A concise, one-sheet Porter's Five Forces view for IMA Klessmann—instantly shows competitive pressures and strategic levers to ease decision-making.

Customers Bargaining Power

Large Scale Industrial Furniture Manufacturers

Major global furniture producers hold high bargaining power: the top 10 OEMs account for ~38% of global contract volume (2024 UN Comtrade-based estimate), letting them negotiate price cuts of 5–12% and bespoke tooling fees waived for multi-year deals.

Increasing Demand for Integrated Smart Factories

Customers now prefer full-service automation partners over standalone machine vendors, and 62% of German manufacturers surveyed in 2024 said they prioritize integrated smart-factory solutions, boosting buyer leverage.

This shift lets buyers demand deeper systems integration and bundled after-sales support within the initial contract, often reallocating 15–25% of project budgets to service and software modules.

System complexity gives purchasers the right to ask for strict performance guarantees and 5–10 year maintenance agreements; contract terms increasingly include uptime SLAs of 99.5% or higher.

Availability of Alternative Global Brands

The availability of global competitors like Biesse (2024 revenue €1.2bn) and SCM Group (2023 revenue ~€800m) gives IMA Klessmann customers clear alternatives, raising buyer bargaining power.

Buyers leverage switching threats to extract better prices, service SLAs, or extra features, pressuring margins—industry churn rates hit ~8% in 2024 for panel-processing OEMs.

That pushes IMA Klessmann to prioritize customer satisfaction scores and tech differentiation; R&D spend across peers averages 4–6% of revenue, a benchmark it must meet.

Transparency in Performance and Pricing

In 2025 buyers access extensive data on machine uptime, energy use and total cost of ownership (TCO), with marketplaces like MachineryCloud reporting 42% of industrial buyers using third-party benchmarks.

Information symmetry lets customers demand empirical proof—field performance logs, ISO 50001 energy metrics, and lifecycle cost models—to negotiate prices and SLAs.

IMA Klessmann must publish transparent test data and superior specs; firms showing 10–15% lower energy intensity win faster procurement cycles.

Sensitivity to Economic Cycles

The demand for IMA Klessmann GmbH’s woodworking machinery tracks construction and furniture spending; global furniture production fell 3.4% in 2023, raising buyer leverage as firms delay capex or push for bigger discounts.

In recessions customers can extract better terms, so IMA Klessmann must offer flexible financing, staged payments, and short-term discounts to protect backlog and smooth revenue.

- 2023 furniture output -3.4% (UN Comtrade)

- Buyers delay capex → higher discount pressure

- Flexible financing preserves orders

Buyers wield power: OEM concentration, churn & integration demand force IMA Klessmann action

Buyers have high leverage: top 10 OEMs ~38% contract volume (2024), panel-OEM churn ~8% (2024), 62% of German manufacturers prioritize integrated solutions (2024), 42% use third‑party benchmarks (2025). Recession sensitivity: global furniture output -3.4% (2023). IMA Klessmann must meet 4–6% R&D spend, publish uptime/TCO data, and offer flexible financing.

| Metric | Value |

|---|---|

| Top 10 OEM share | ~38% (2024) |

| German buyers favor integration | 62% (2024) |

| Buyers using benchmarks | 42% (2025) |

| Panel-OEM churn | ~8% (2024) |

| Furniture output | -3.4% (2023) |

| Peer R&D target | 4–6% revenue |

What You See Is What You Get

IMA Klessmann GmbH Porter's Five Forces Analysis

This preview shows the exact IMA Klessmann GmbH Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready to use. The document displayed is the final, professionally written file included in your download; once payment is completed, you gain instant access to this same deliverable. Use it as-is for strategic planning, presentations, or internal review.