IMAX PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and rapid tech adoption are reshaping IMAX’s market position in our concise PESTLE overview—perfect for investors and strategists seeking high-impact insights. Purchase the full PESTLE analysis to get a detailed, ready-to-use breakdown of regulatory risks, consumer trends, and environmental pressures affecting IMAX’s growth. Download now for actionable intelligence you can apply to investment theses, competitive planning, or board-level strategy.

Political factors

Geopolitical relations and trade policies

Ongoing US-China trade tensions materially affect IMAX, since China accounted for about 34% of global box office in 2024 and remains a top market for IMAX installations and revenue.

Escalation in tariffs or tech export controls could disrupt supply of proprietary projection systems and camera parts, risking installation delays and higher COGS; IMAX reported $513M revenue in 2024, with international exposure critical.

Management must engage diplomatically to protect film quota access and content flow into China and other territories, as restricted Hollywood releases would directly lower IMAX theater utilization and box office share.

Censorship and content regulation

IMAX's revenue is tied to global blockbuster rollouts, yet markets like the Middle East and Southeast Asia impose censorship that delayed or banned films, cutting into box office and royalty income—IMAX reported a 2023 international revenue of about 42% of total, amplifying exposure to such risks.

Strict local content laws can force edits or postpone releases, directly reducing IMAX's per-screen earnings; in 2024, studio partnerships accounted for over 60% of IMAX film supply, so disruptions materially impact throughput.

Mitigating this requires tight coordination with studios to pre-clear content and consider localized versions that preserve IMAX's immersive format while meeting regulations, minimizing lost screening days and revenue leakage.

Government subsidies for local film industries

Many governments offer subsidies and tax incentives to boost local film industries, increasing local-language content available for IMAX conversion; e.g., India’s Film Facilitation Office and 30–40% regional tax rebates helped India’s box office grow to $2.4bn in 2023, fueling IMAX releases like 2023’s big-budget titles.

Stability in emerging markets

The expansion of IMAX into emerging markets hinges on political stability; IMF data shows GDP volatility rises by 4-6 percentage points during political shocks, which can delay infrastructure and theater builds.

Political unrest or regime changes have led to multi-year suspension of projects in regions where foreign direct investment dropped up to 20% in 2023-24, increasing capital risk for IMAX.

Strategists should use country risk scores (e.g., Moody’s, Eurasia Group) to prioritize investments in nations with low sovereign risk and predictable regulatory environments.

- GDP volatility +4–6 pp during political shocks

- FDI down up to 20% in affected markets (2023–24)

- Use Moody’s/Eurasia Group risk scores to prioritize

Intellectual property protection policies

Political commitment to enforcing intellectual property rights is crucial for IMAX, which licenses Digital Media Remastering technology and brand; in 2024 IMAX reported licensing revenue of about $124 million, making IP protection economically material.

Weak IP enforcement in some markets raises risks of unauthorized branding and low-quality large-format competitors, potentially eroding market share and brand premiums.

Strengthening international treaties and local enforcement remains a primary political priority to preserve exclusivity and IMAX’s long-term licensing value.

- 2024 IMAX licensing revenue ≈ $124M

- High-risk jurisdictions: parts of Southeast Asia, Africa, LATAM

- Policy focus: stronger treaties, local enforcement, anti-counterfeit measures

Political risk imperils IMAX revenues—China exposure, FDI drops and GDP volatility

Political risks—US-China tensions, tariffs, censorship, and weak IP enforcement—can cut IMAX box office and licensing (2024 revenue $513M; licensing ~$124M) and raise COGS/installation delays; use sovereign risk scores to prioritize markets where FDI fell up to 20% in 2023–24 and GDP volatility rose ~4–6 pp during political shocks.

| Metric | Value |

|---|---|

| 2024 Revenue | $513M |

| Licensing | $124M |

| China box office share (2024) | 34% |

| FDI drop (2023–24) | up to 20% |

| GDP volatility rise | 4–6 pp |

What is included in the product

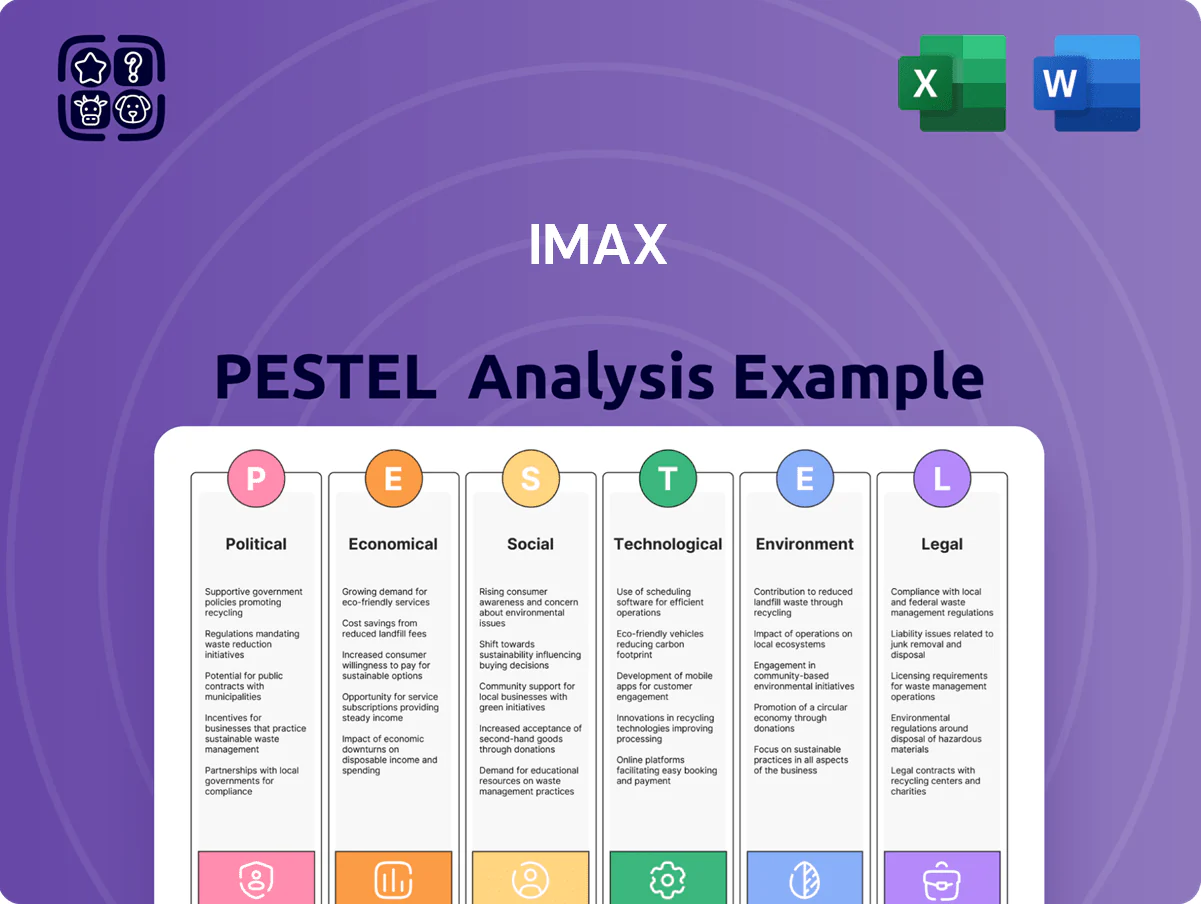

Explores how macro-environmental factors uniquely affect IMAX across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific insights to identify threats and opportunities for executives and investors.

Condenses IMAX's PESTLE into a crisp, shareable summary that teams can drop into presentations or use in planning sessions to quickly align on external risks and strategic positioning.

Economic factors

Global inflation and discretionary spending

Rising inflation—CPI at 3.4% in the US (2025 annualized) and 6.8% in the Eurozone (2024)—can curb discretionary spending and pressure box office receipts as households trim nonessentials, reducing theater attendance. IMAX's premium pricing, often 30–50% above standard tickets, makes revenues sensitive to such budget shifts. Yet premium large-format attendance fell less in 2023–24, with IMAX global box office growing 4% to $1.7bn in 2024, indicating resilient demand among higher-income patrons.

Foreign exchange rate volatility

As a global firm, IMAX faces forex exposure across dozens of markets; a 10% appreciation of the US dollar in 2023 trimmed reported international revenue by roughly $15–25m after conversion, per company filings.

Strong USD pressures translate to lower translated box office and licensing income and raise hedging costs—IMAX reported $8.4m in net FX losses in 2024—eroding margins.

Currency swings also affect affordability of IMAX systems for exhibitors; a 20% local currency depreciation versus USD can push acquisition costs well into six figures higher, constraining global capex demand.

Interest rates and theater expansion

The prevailing interest rate environment affects exhibitors’ ability to finance IMAX installs and retrofits; US prime rates rose from 3.25% in 2021 to ~8.5% by late 2023–2024, raising average borrowing costs and slowing capex for many chains, contributing to a 2024 global cinema circuit expansion slowdown of ~6–8%; IMAX offsets this by offering flexible financing and lease options to preserve rollout of laser upgrades and new auditoriums.

Growth of the premium large format market

There is a clear flight-to-quality: premium large-format box office grew to about 18% of global theatrical revenue in 2024, with IMAX reporting that premium screens captured roughly 25% of per-screen revenue versus standard screens.

This shift lets IMAX increase share of total box office even as overall admissions were flat in 2024, supporting higher margins and ROI on next-gen projection and sound investments.

- Premium LF = ~18% of global box office (2024)

- IMAX per-screen revenue ~25% higher than standard (2024)

- Higher margins justify capex in next-gen tech

Labor costs and supply chain dynamics

Rising labor costs—US manufacturing wages up about 4.2% in 2024 year-over-year and global tech salary inflation near 6%—increase OPEX for servicing IMAX systems worldwide, squeezing margins on maintenance contracts.

Semiconductor and optical component prices rose ~3–5% in 2024 as supply tightened, raising unit costs for IMAX cameras and projectors and pressuring gross margins on hardware sales.

Active input-cost management, supplier diversification and long-term procurement contracts are therefore critical to protect profitability in IMAX’s tech sales and maintenance segments.

- Labor wage inflation: +4.2% (US mfg 2024); tech wages ~+6%

- Component price increase: ~3–5% (semiconductors/optics 2024)

- Key actions: supplier diversification, long-term contracts, cost-pass-through in service agreements

IMAX: $1.7B Box Office Growth vs FX, Wage and Component Cost Pressures

Inflation and high interest rates pressure discretionary spend and exhibitor capex; IMAX saw global box office rise to $1.7bn (2024) even as FX losses hit $8.4m and USD strength trimmed ~$15–25m in translated revenue. Premium LF reached ~18% of global box office; IMAX per-screen revenue ~25% above standard. Labor and component cost inflation (+4.2% US wages; +3–5% semiconductors 2024) squeeze margins.

| Metric | 2024/25 |

|---|---|

| Global box office | $1.7bn (2024) |

| Premium LF share | ~18% |

| Per-screen premium delta | +25% |

| FX losses | $8.4m (2024) |

| Wage inflation | US mfg +4.2% (2024) |

Full Version Awaits

IMAX PESTLE Analysis

The preview shown here is the exact IMAX PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and rapid tech adoption are reshaping IMAX’s market position in our concise PESTLE overview—perfect for investors and strategists seeking high-impact insights. Purchase the full PESTLE analysis to get a detailed, ready-to-use breakdown of regulatory risks, consumer trends, and environmental pressures affecting IMAX’s growth. Download now for actionable intelligence you can apply to investment theses, competitive planning, or board-level strategy.

Political factors

Geopolitical relations and trade policies

Ongoing US-China trade tensions materially affect IMAX, since China accounted for about 34% of global box office in 2024 and remains a top market for IMAX installations and revenue.

Escalation in tariffs or tech export controls could disrupt supply of proprietary projection systems and camera parts, risking installation delays and higher COGS; IMAX reported $513M revenue in 2024, with international exposure critical.

Management must engage diplomatically to protect film quota access and content flow into China and other territories, as restricted Hollywood releases would directly lower IMAX theater utilization and box office share.

Censorship and content regulation

IMAX's revenue is tied to global blockbuster rollouts, yet markets like the Middle East and Southeast Asia impose censorship that delayed or banned films, cutting into box office and royalty income—IMAX reported a 2023 international revenue of about 42% of total, amplifying exposure to such risks.

Strict local content laws can force edits or postpone releases, directly reducing IMAX's per-screen earnings; in 2024, studio partnerships accounted for over 60% of IMAX film supply, so disruptions materially impact throughput.

Mitigating this requires tight coordination with studios to pre-clear content and consider localized versions that preserve IMAX's immersive format while meeting regulations, minimizing lost screening days and revenue leakage.

Government subsidies for local film industries

Many governments offer subsidies and tax incentives to boost local film industries, increasing local-language content available for IMAX conversion; e.g., India’s Film Facilitation Office and 30–40% regional tax rebates helped India’s box office grow to $2.4bn in 2023, fueling IMAX releases like 2023’s big-budget titles.

Stability in emerging markets

The expansion of IMAX into emerging markets hinges on political stability; IMF data shows GDP volatility rises by 4-6 percentage points during political shocks, which can delay infrastructure and theater builds.

Political unrest or regime changes have led to multi-year suspension of projects in regions where foreign direct investment dropped up to 20% in 2023-24, increasing capital risk for IMAX.

Strategists should use country risk scores (e.g., Moody’s, Eurasia Group) to prioritize investments in nations with low sovereign risk and predictable regulatory environments.

- GDP volatility +4–6 pp during political shocks

- FDI down up to 20% in affected markets (2023–24)

- Use Moody’s/Eurasia Group risk scores to prioritize

Intellectual property protection policies

Political commitment to enforcing intellectual property rights is crucial for IMAX, which licenses Digital Media Remastering technology and brand; in 2024 IMAX reported licensing revenue of about $124 million, making IP protection economically material.

Weak IP enforcement in some markets raises risks of unauthorized branding and low-quality large-format competitors, potentially eroding market share and brand premiums.

Strengthening international treaties and local enforcement remains a primary political priority to preserve exclusivity and IMAX’s long-term licensing value.

- 2024 IMAX licensing revenue ≈ $124M

- High-risk jurisdictions: parts of Southeast Asia, Africa, LATAM

- Policy focus: stronger treaties, local enforcement, anti-counterfeit measures

Political risk imperils IMAX revenues—China exposure, FDI drops and GDP volatility

Political risks—US-China tensions, tariffs, censorship, and weak IP enforcement—can cut IMAX box office and licensing (2024 revenue $513M; licensing ~$124M) and raise COGS/installation delays; use sovereign risk scores to prioritize markets where FDI fell up to 20% in 2023–24 and GDP volatility rose ~4–6 pp during political shocks.

| Metric | Value |

|---|---|

| 2024 Revenue | $513M |

| Licensing | $124M |

| China box office share (2024) | 34% |

| FDI drop (2023–24) | up to 20% |

| GDP volatility rise | 4–6 pp |

What is included in the product

Explores how macro-environmental factors uniquely affect IMAX across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific insights to identify threats and opportunities for executives and investors.

Condenses IMAX's PESTLE into a crisp, shareable summary that teams can drop into presentations or use in planning sessions to quickly align on external risks and strategic positioning.

Economic factors

Global inflation and discretionary spending

Rising inflation—CPI at 3.4% in the US (2025 annualized) and 6.8% in the Eurozone (2024)—can curb discretionary spending and pressure box office receipts as households trim nonessentials, reducing theater attendance. IMAX's premium pricing, often 30–50% above standard tickets, makes revenues sensitive to such budget shifts. Yet premium large-format attendance fell less in 2023–24, with IMAX global box office growing 4% to $1.7bn in 2024, indicating resilient demand among higher-income patrons.

Foreign exchange rate volatility

As a global firm, IMAX faces forex exposure across dozens of markets; a 10% appreciation of the US dollar in 2023 trimmed reported international revenue by roughly $15–25m after conversion, per company filings.

Strong USD pressures translate to lower translated box office and licensing income and raise hedging costs—IMAX reported $8.4m in net FX losses in 2024—eroding margins.

Currency swings also affect affordability of IMAX systems for exhibitors; a 20% local currency depreciation versus USD can push acquisition costs well into six figures higher, constraining global capex demand.

Interest rates and theater expansion

The prevailing interest rate environment affects exhibitors’ ability to finance IMAX installs and retrofits; US prime rates rose from 3.25% in 2021 to ~8.5% by late 2023–2024, raising average borrowing costs and slowing capex for many chains, contributing to a 2024 global cinema circuit expansion slowdown of ~6–8%; IMAX offsets this by offering flexible financing and lease options to preserve rollout of laser upgrades and new auditoriums.

Growth of the premium large format market

There is a clear flight-to-quality: premium large-format box office grew to about 18% of global theatrical revenue in 2024, with IMAX reporting that premium screens captured roughly 25% of per-screen revenue versus standard screens.

This shift lets IMAX increase share of total box office even as overall admissions were flat in 2024, supporting higher margins and ROI on next-gen projection and sound investments.

- Premium LF = ~18% of global box office (2024)

- IMAX per-screen revenue ~25% higher than standard (2024)

- Higher margins justify capex in next-gen tech

Labor costs and supply chain dynamics

Rising labor costs—US manufacturing wages up about 4.2% in 2024 year-over-year and global tech salary inflation near 6%—increase OPEX for servicing IMAX systems worldwide, squeezing margins on maintenance contracts.

Semiconductor and optical component prices rose ~3–5% in 2024 as supply tightened, raising unit costs for IMAX cameras and projectors and pressuring gross margins on hardware sales.

Active input-cost management, supplier diversification and long-term procurement contracts are therefore critical to protect profitability in IMAX’s tech sales and maintenance segments.

- Labor wage inflation: +4.2% (US mfg 2024); tech wages ~+6%

- Component price increase: ~3–5% (semiconductors/optics 2024)

- Key actions: supplier diversification, long-term contracts, cost-pass-through in service agreements

IMAX: $1.7B Box Office Growth vs FX, Wage and Component Cost Pressures

Inflation and high interest rates pressure discretionary spend and exhibitor capex; IMAX saw global box office rise to $1.7bn (2024) even as FX losses hit $8.4m and USD strength trimmed ~$15–25m in translated revenue. Premium LF reached ~18% of global box office; IMAX per-screen revenue ~25% above standard. Labor and component cost inflation (+4.2% US wages; +3–5% semiconductors 2024) squeeze margins.

| Metric | 2024/25 |

|---|---|

| Global box office | $1.7bn (2024) |

| Premium LF share | ~18% |

| Per-screen premium delta | +25% |

| FX losses | $8.4m (2024) |

| Wage inflation | US mfg +4.2% (2024) |

Full Version Awaits

IMAX PESTLE Analysis

The preview shown here is the exact IMAX PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.