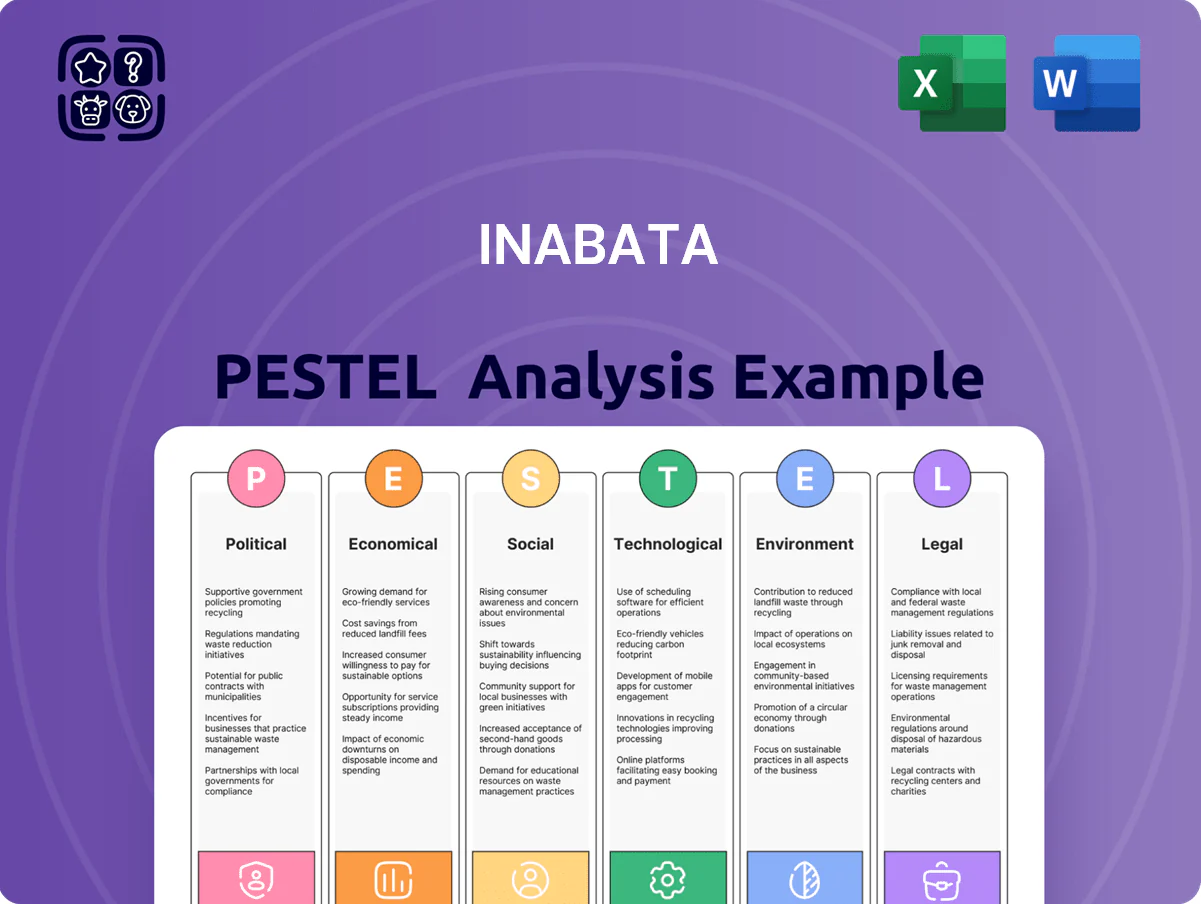

Inabata PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and tech disruption are shaping Inabata’s trajectory with our concise PESTLE snapshot—designed for investors and strategists who need immediate clarity. Purchase the full PESTLE analysis to access actionable insights, risk forecasts, and editable charts that speed decision-making and strengthen your competitive strategy.

Political factors

Geopolitical Trade Dynamics

Persistent US-China trade tensions force Inabata’s electronics and chemical segments to adjust strategy as tariffs and export controls rise; US restrictions on semiconductors and China’s countermeasures contributed to global chip export controls affecting ~$600bn in trade in 2024. Stricter controls on dual‑use materials and sanctions increase compliance costs and risk; Inabata faces tariff volatility and must monitor evolving lists of controlled items. The company must diversify suppliers—47% of key components sourced from East Asia in 2023—to build resilience against sudden policy shifts.

Southeast Asian Political Stability

Inabata’s large manufacturing and processing footprint in Southeast Asia—notably Vietnam (≈$270m APAC sales 2024) and Thailand—makes revenue and margins sensitive to political shifts; Vietnam’s 2024 FDI flows fell 1.7% YoY to $19.9bn and Thailand’s investor confidence index slipped 4.2 points in Q3 2024, both affecting operational certainty. Changes in leadership or foreign investment rules can alter tax and land-use regimes, impacting facility costs and capex plans. Continued ASEAN trade liberalization (ASEAN accounted for ~25% of Inabata’s regional procurement in 2024) preserves tariff preferences that support competitive pricing.

Japanese Economic Diplomacy

The Japanese government’s 2024 strategy to secure critical minerals and boost semiconductor resilience — including a ¥1.4 trillion package for supply-chain measures and a 2025 target to double domestic semiconductor production to ¥8 trillion by 2030 — underpins demand for Inabata’s specialty materials.

Participation in programs like the 2024 Reshoring Incentive Fund and subsidies covering up to 30% of capex for strategic sectors can lower Inabata’s expansion costs and accelerate domestic projects.

Aligning Inabata’s strategy with national economic security objectives enables access to public-private partnerships, predictable procurement pipelines, and potential long-term contracts supporting revenue stability and margin preservation.

Global Regulatory Harmonization

- Standardized rules raise compliance costs ~2-3% of revenue

- CPTPP/FTAs can change tariffs by 5-10%, altering margins 0.5-1.5pp

- Over 40% of overseas sales exposed to Asia-Pacific trade shifts

- Active trade association engagement required to mitigate risks

Sanctions and Compliance Risk

Expanding global sanctions regimes mean Inabata must run rigorous political risk assessments to avoid dealings with restricted entities; UN and US sanctions lists grew by 12% from 2022–2024, raising screening burdens for global traders.

Political instability in Eastern Europe and the Middle East can quickly alter prohibited partner lists, disrupting procurement of chemical feedstocks—energy- and base-chemical supply shocks in 2022–23 raised input costs up to 35% in some regions.

Maintaining a robust compliance department is essential: global fines for sanctions breaches exceeded $6.5bn in 2023, so proactive compliance protects Inabata’s legal standing and reputation.

- Sanctions lists +12% (2022–24)

- Input-cost spikes up to 35% (2022–23)

- Sanctions-related fines > $6.5bn (2023)

- Strong compliance mitigates legal/reputational risk

Inabata faces rising compliance, tariff and sanction risks amid East Asia sourcing and reshoring

US‑China tech tensions, export controls and rising sanctions raise compliance/tariff risks for Inabata (¥262.8bn FY2024); 47% components from East Asia (2023); ASEAN ~25% procurement (2024); Japan ¥1.4T supply‑chain package (2024) and reshoring subsidies up to 30% capex; sanctions lists +12% (2022–24); global fines >$6.5bn (2023).

| Metric | Value |

|---|---|

| FY2024 revenue | ¥262.8bn |

| East Asia sourcing | 47% |

| ASEAN procurement | 25% |

| Sanctions growth (22–24) | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Inabata across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends for reliable evaluation.

Condenses Inabata's full PESTLE into a clear, shareable summary that teams can drop into presentations or planning sessions to quickly align on external risks and strategic implications.

Economic factors

Currency Exchange Rate Volatility

As a major importer and exporter, Inabata’s profitability is highly sensitive to JPY/USD and regional FX moves; JPY depreciated ~6% vs USD in 2023 and remained volatile in 2024, affecting reported margins on overseas sales.

A weaker yen boosts the JPY value of foreign earnings but raises import costs for raw materials—Inabata reported FX-related cost pressure of ~¥3.8bn in FY2023.

The firm uses forward hedges, currency swaps and multi-currency accounting; as of FY2024 it hedged roughly 60% of anticipated FX exposures to stabilize EBITDA.

Global Industrial Demand Cycles

The demand for Inabata’s plastics and electronic materials tracks global auto and consumer electronics cycles; global auto production fell 2.9% in 2023 while global smartphone shipments declined 4% in 2024, pressuring orders and margins in key markets like Europe and China.

Raw Material Price Fluctuations

Raw material costs for chemicals and plastics Inabata distributes track crude oil and naphtha; Brent crude averaged about 86 USD/bbl in 2024 and naphtha volatility pushed Asian contract prices up ~18% year-on-year, squeezing margins when cost pass-through lags.

Rapid energy spikes—such as the 2022–24 shocks—can compress gross margins if customers delay accepting higher prices; Inabata mitigates this via strategic inventory and hedging.

Long-term supply contracts and inventory optimization reduced input-cost volatility impact by an estimated 30–40% for distributors in the region, stabilizing cash flows and protecting EBITDA.

Interest Rate Environments

Rising global interest rates—Japan's policy rate shifting from -0.1% (2023) toward 0.1–0.5% in 2024 and the US Fed funds target at 5.25–5.50% (2024)—increase Inabata's financing costs for trading and capex, raising weighted borrowing expense and pressuring ROIC.

Higher costs can constrain M&A and factory expansion in Southeast Asia; maintaining net cash or undrawn facilities and diversified currency funding is critical to withstand tightening across markets.

- Japan rate ~0.1–0.5% (2024) and US 5.25–5.50% (2024)

- Higher rates raise financing costs, limiting M&A and capex

- Requires strong balance sheet, diversified funding, undrawn credit lines

Emerging Market Growth Rates

Economic expansion in developing economies offers Inabata strong opportunities in housing and life-industry materials as ASEAN and South Asia GDP growth outpaced global averages—Indonesia 2024 GDP growth ~5.2% and India ~7.0% (IMF 2024), boosting middle-class demand for chemicals, food additives, and construction materials.

Inabata’s market capture hinges on local distribution and infrastructure investment; supply-chain strengths and exposure to FX and local economic stability (Indonesia inflation ~3.5%, India ~5.6% 2024) are key risks/opportunities.

- Indonesia GDP 2024 ~5.2%

- India GDP 2024 ~7.0%

- Indonesia inflation ~3.5%, India ~5.6% (2024)

- Growth tied to local infrastructure, FX and supply-chain resilience

Inabata margins squeezed by JPY weakness, higher naphtha and rising financing costs

Inabata's margins are FX-sensitive: JPY fell ~6% vs USD in 2023; FY2023 FX cost ≈¥3.8bn; ~60% FX hedged (FY2024). Brent avg $86/bbl (2024); Asian naphtha +18% YoY, squeezing margins. Japan rate ~0.1–0.5% and US 5.25–5.50% (2024) raise financing costs; ASEAN growth aids demand—Indonesia GDP ~5.2%, India ~7.0% (2024).

| Metric | 2024/2023 |

|---|---|

| JPY vs USD (2023) | -6% |

| FX cost FY2023 | ¥3.8bn |

| Hedge ratio FY2024 | 60% |

| Brent (2024) | $86/bbl |

| Naphtha change | +18% YoY |

| Japan rate | 0.1–0.5% |

| US rate | 5.25–5.50% |

| Indonesia GDP | 5.2% |

| India GDP | 7.0% |

Full Version Awaits

Inabata PESTLE Analysis

The preview shown here is the exact Inabata PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and tech disruption are shaping Inabata’s trajectory with our concise PESTLE snapshot—designed for investors and strategists who need immediate clarity. Purchase the full PESTLE analysis to access actionable insights, risk forecasts, and editable charts that speed decision-making and strengthen your competitive strategy.

Political factors

Geopolitical Trade Dynamics

Persistent US-China trade tensions force Inabata’s electronics and chemical segments to adjust strategy as tariffs and export controls rise; US restrictions on semiconductors and China’s countermeasures contributed to global chip export controls affecting ~$600bn in trade in 2024. Stricter controls on dual‑use materials and sanctions increase compliance costs and risk; Inabata faces tariff volatility and must monitor evolving lists of controlled items. The company must diversify suppliers—47% of key components sourced from East Asia in 2023—to build resilience against sudden policy shifts.

Southeast Asian Political Stability

Inabata’s large manufacturing and processing footprint in Southeast Asia—notably Vietnam (≈$270m APAC sales 2024) and Thailand—makes revenue and margins sensitive to political shifts; Vietnam’s 2024 FDI flows fell 1.7% YoY to $19.9bn and Thailand’s investor confidence index slipped 4.2 points in Q3 2024, both affecting operational certainty. Changes in leadership or foreign investment rules can alter tax and land-use regimes, impacting facility costs and capex plans. Continued ASEAN trade liberalization (ASEAN accounted for ~25% of Inabata’s regional procurement in 2024) preserves tariff preferences that support competitive pricing.

Japanese Economic Diplomacy

The Japanese government’s 2024 strategy to secure critical minerals and boost semiconductor resilience — including a ¥1.4 trillion package for supply-chain measures and a 2025 target to double domestic semiconductor production to ¥8 trillion by 2030 — underpins demand for Inabata’s specialty materials.

Participation in programs like the 2024 Reshoring Incentive Fund and subsidies covering up to 30% of capex for strategic sectors can lower Inabata’s expansion costs and accelerate domestic projects.

Aligning Inabata’s strategy with national economic security objectives enables access to public-private partnerships, predictable procurement pipelines, and potential long-term contracts supporting revenue stability and margin preservation.

Global Regulatory Harmonization

- Standardized rules raise compliance costs ~2-3% of revenue

- CPTPP/FTAs can change tariffs by 5-10%, altering margins 0.5-1.5pp

- Over 40% of overseas sales exposed to Asia-Pacific trade shifts

- Active trade association engagement required to mitigate risks

Sanctions and Compliance Risk

Expanding global sanctions regimes mean Inabata must run rigorous political risk assessments to avoid dealings with restricted entities; UN and US sanctions lists grew by 12% from 2022–2024, raising screening burdens for global traders.

Political instability in Eastern Europe and the Middle East can quickly alter prohibited partner lists, disrupting procurement of chemical feedstocks—energy- and base-chemical supply shocks in 2022–23 raised input costs up to 35% in some regions.

Maintaining a robust compliance department is essential: global fines for sanctions breaches exceeded $6.5bn in 2023, so proactive compliance protects Inabata’s legal standing and reputation.

- Sanctions lists +12% (2022–24)

- Input-cost spikes up to 35% (2022–23)

- Sanctions-related fines > $6.5bn (2023)

- Strong compliance mitigates legal/reputational risk

Inabata faces rising compliance, tariff and sanction risks amid East Asia sourcing and reshoring

US‑China tech tensions, export controls and rising sanctions raise compliance/tariff risks for Inabata (¥262.8bn FY2024); 47% components from East Asia (2023); ASEAN ~25% procurement (2024); Japan ¥1.4T supply‑chain package (2024) and reshoring subsidies up to 30% capex; sanctions lists +12% (2022–24); global fines >$6.5bn (2023).

| Metric | Value |

|---|---|

| FY2024 revenue | ¥262.8bn |

| East Asia sourcing | 47% |

| ASEAN procurement | 25% |

| Sanctions growth (22–24) | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Inabata across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends for reliable evaluation.

Condenses Inabata's full PESTLE into a clear, shareable summary that teams can drop into presentations or planning sessions to quickly align on external risks and strategic implications.

Economic factors

Currency Exchange Rate Volatility

As a major importer and exporter, Inabata’s profitability is highly sensitive to JPY/USD and regional FX moves; JPY depreciated ~6% vs USD in 2023 and remained volatile in 2024, affecting reported margins on overseas sales.

A weaker yen boosts the JPY value of foreign earnings but raises import costs for raw materials—Inabata reported FX-related cost pressure of ~¥3.8bn in FY2023.

The firm uses forward hedges, currency swaps and multi-currency accounting; as of FY2024 it hedged roughly 60% of anticipated FX exposures to stabilize EBITDA.

Global Industrial Demand Cycles

The demand for Inabata’s plastics and electronic materials tracks global auto and consumer electronics cycles; global auto production fell 2.9% in 2023 while global smartphone shipments declined 4% in 2024, pressuring orders and margins in key markets like Europe and China.

Raw Material Price Fluctuations

Raw material costs for chemicals and plastics Inabata distributes track crude oil and naphtha; Brent crude averaged about 86 USD/bbl in 2024 and naphtha volatility pushed Asian contract prices up ~18% year-on-year, squeezing margins when cost pass-through lags.

Rapid energy spikes—such as the 2022–24 shocks—can compress gross margins if customers delay accepting higher prices; Inabata mitigates this via strategic inventory and hedging.

Long-term supply contracts and inventory optimization reduced input-cost volatility impact by an estimated 30–40% for distributors in the region, stabilizing cash flows and protecting EBITDA.

Interest Rate Environments

Rising global interest rates—Japan's policy rate shifting from -0.1% (2023) toward 0.1–0.5% in 2024 and the US Fed funds target at 5.25–5.50% (2024)—increase Inabata's financing costs for trading and capex, raising weighted borrowing expense and pressuring ROIC.

Higher costs can constrain M&A and factory expansion in Southeast Asia; maintaining net cash or undrawn facilities and diversified currency funding is critical to withstand tightening across markets.

- Japan rate ~0.1–0.5% (2024) and US 5.25–5.50% (2024)

- Higher rates raise financing costs, limiting M&A and capex

- Requires strong balance sheet, diversified funding, undrawn credit lines

Emerging Market Growth Rates

Economic expansion in developing economies offers Inabata strong opportunities in housing and life-industry materials as ASEAN and South Asia GDP growth outpaced global averages—Indonesia 2024 GDP growth ~5.2% and India ~7.0% (IMF 2024), boosting middle-class demand for chemicals, food additives, and construction materials.

Inabata’s market capture hinges on local distribution and infrastructure investment; supply-chain strengths and exposure to FX and local economic stability (Indonesia inflation ~3.5%, India ~5.6% 2024) are key risks/opportunities.

- Indonesia GDP 2024 ~5.2%

- India GDP 2024 ~7.0%

- Indonesia inflation ~3.5%, India ~5.6% (2024)

- Growth tied to local infrastructure, FX and supply-chain resilience

Inabata margins squeezed by JPY weakness, higher naphtha and rising financing costs

Inabata's margins are FX-sensitive: JPY fell ~6% vs USD in 2023; FY2023 FX cost ≈¥3.8bn; ~60% FX hedged (FY2024). Brent avg $86/bbl (2024); Asian naphtha +18% YoY, squeezing margins. Japan rate ~0.1–0.5% and US 5.25–5.50% (2024) raise financing costs; ASEAN growth aids demand—Indonesia GDP ~5.2%, India ~7.0% (2024).

| Metric | 2024/2023 |

|---|---|

| JPY vs USD (2023) | -6% |

| FX cost FY2023 | ¥3.8bn |

| Hedge ratio FY2024 | 60% |

| Brent (2024) | $86/bbl |

| Naphtha change | +18% YoY |

| Japan rate | 0.1–0.5% |

| US rate | 5.25–5.50% |

| Indonesia GDP | 5.2% |

| India GDP | 7.0% |

Full Version Awaits

Inabata PESTLE Analysis

The preview shown here is the exact Inabata PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.