Inapa Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

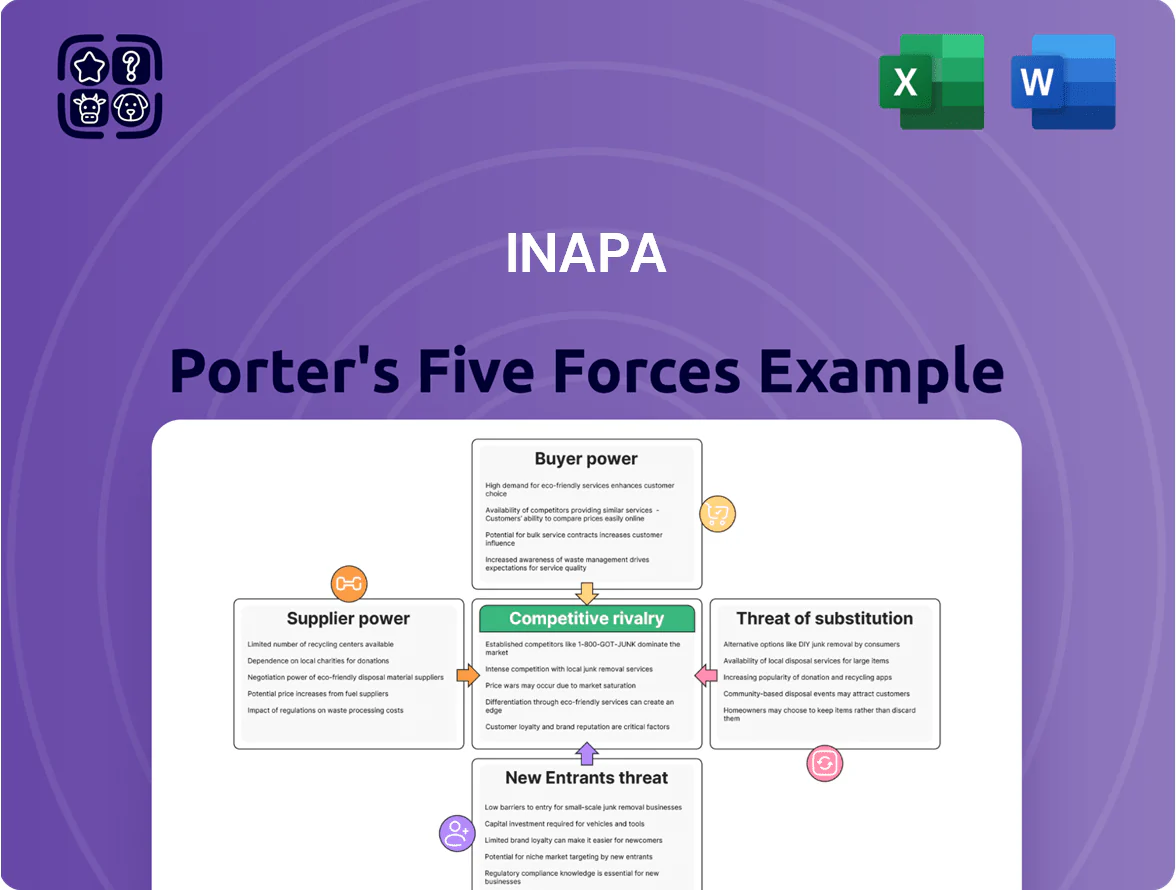

Inapa faces moderate supplier leverage, fragmented buyer power, and rising substitute threats from digital paperless trends, while scale and distribution costs temper new entrant risks and rival intensity remains competitive across European markets.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Inapa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Upstream Paper Producers

The European paper sector is highly consolidated: the top 10 mills control roughly 60% of coated paper capacity as of 2024, leaving merchants like Inapa with few large suppliers; this concentration lets mills set prices and ration supply—mill price hikes in 2023–24 pushed European pulp-based paper prices up ~25% year-on-year; distributors face limited negotiation power and often must absorb or pass these cost rises into a price-sensitive market.

Volatility in Energy and Raw Material Costs

Suppliers face large swings in wood pulp and energy costs; pulp prices rose ~18% in 2024 and European wholesale electricity peaked at €350/MWh in Aug 2022, with volatility persisting into 2025, so suppliers quickly pass spikes to merchants.

By end-2025 supply contracts show pass-through clauses; Inapa is exposed as suppliers prioritize margin, with pulp and energy representing ~40–55% of upstream cost for paper merchants, raising short-term price risk.

Strategic Pivot Toward Specialized Packaging

Integration of ESG and Sustainability Standards

Inapa relies on certified suppliers to serve corporate clients and comply with procurement rules, so compliant vendors can insist on longer contracts and stricter traceability terms, reducing Inapa’s bargaining room.

Logistical Dependencies and Lead Times

Logistical capabilities and proximity of major paper mills to Inapa’s €1.1bn distribution hubs in Iberia and France strongly affect supply reliability; mills within 200–500 km typically offer lead times of 3–7 days versus 10–21 days from distant suppliers.

Suppliers with better transport networks secure firmer pricing and credit terms by promising 95%+ on-time delivery; regional road strikes or port slowdowns in 2024 raised lead-time variance by 40%.

Mill-level labor shortages or outages can cut merchant inventory turnover from 8x to 4x annually, sharply raising stockout risk and emergency freight costs.

- Closer mills: 3–7 day lead times

- Distant mills: 10–21 day lead times

- On-time delivery target: 95%+

- 2024 disruptions ↑ lead-time variance 40%

- Turnover drop: 8x to 4x raises stockout risk

Supplier power surges: mills dominate, input costs 40–55%, lead-times spike

Suppliers hold strong leverage: top 10 mills ~60% coated-capacity (2024), pulp costs +18% (2024) and certified-fiber premiums 6–12% (2024) push Inapa’s input share to ~40–55% of product cost; lead times 3–7d (near) vs 10–21d (far), 95%+ OTIF target, 2024 disruptions raised lead-time variance 40%, forcing longer contracts and 5–10% volume premiums.

| Metric | Value (year) |

|---|---|

| Top-10 mill share | ~60% (2024) |

| Pulp price change | +18% (2024) |

| Certified premium | 6–12% (2024) |

| Input cost share | 40–55% |

| Lead times | 3–7d / 10–21d |

| Lead-time variance ↑ | 40% (2024) |

What is included in the product

Tailored exclusively for Inapa, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier influence, entry barriers, substitute threats, and disruptive trends affecting its market position and profitability.

A concise Porter's Five Forces snapshot for Inapa—streamlines competitor, supplier, buyer, new entrant, and substitute pressures into a single, board-ready view to speed strategic decisions.

Customers Bargaining Power

High Price Sensitivity in Commercial Printing

Commercial printers, Inapa’s main customers, run on single-digit net margins and treat standard paper grades as commodities, triggering extreme price sensitivity and easy switching for 1–3% per-sheet savings.

Inapa reported European gross margin pressure in 2024—distribution segment EBITDA margin fell to ~3.5%—as it repeatedly entered price-driven bids to defend volumes.

Fragmentation of the Small and Medium Enterprise Segment

While large printing houses each hold strong bargaining leverage, most of Inapa’s market is fragmented: over 150,000 European SMEs in paper and print (2024 Eurostat trade data) have low individual clout but high collective switching power because 40% now use digital procurement platforms with transparent pricing (2023 McKinsey survey). Inapa must offer bundled logistics, same‑day distribution, and trade credit (typical SME DSO 45–60 days) to retain loyalty.

Shift Toward Digital and Sustainable Solutions

Modern buyers push for eco-friendly paper and digital ordering; 72% of EU procurement officers rate sustainability as a buying criterion (2024 Eurobarometer).

Clients now request carbon-footprint data and recycled-content certificates; 38% of contracts in EU paper supply chains included sustainability clauses in 2023.

Merchants lacking transparent, digital sustainability tools risk losing share to niche suppliers—Inapa could face a 5–12% revenue hit in affected segments within 24 months.

Consolidation of Large Print Groups

Consolidation among print groups has created buyers controlling larger volumes and professional procurement; top 10 European print groups now account for roughly 35% of commercial print spend (2024), boosting their leverage.

These groups extract volume discounts up to 12% and push 60–90‑day payment terms, straining merchants’ working capital; Inapa faces margin pressure and higher DSO (days sales outstanding).

Inapa must offer advanced supply‑chain integration—EDI, vendor‑managed inventory, dynamic pricing—to stay a preferred partner for these industrial buyers.

- Top 10 buyers ~35% spend (2024)

- Volume discounts up to 12%

- Payment terms 60–90 days

- Requires EDI, VMI, dynamic pricing

Low Switching Costs for Standard Products

For commodity graphic papers and basic packaging, switching costs from Inapa to rivals are negligible, letting buyers pressure margins; industry data shows standard grades face price volatility of ±6-10% annually (2024 ECMA index). Inapa counters by selling technical expertise and value-added services—color management, just-in-time logistics, and sustainability certification—that raise entanglement and can lift account gross margins by ~2–4 percentage points.

- Low switching cost; price volatility 6–10% (2024 ECMA)

- Buyers use distributor competition to cut prices

- Inapa adds services: color management, JIT, sustainability

- Value services can increase account gross margin ~2–4 ppt

Inapa boosts margins 2–4ppt with JIT/EDI/VMI as buyers demand price, transparency, sustainability

Buyers are highly price-sensitive: top 10 printers = ~35% spend (2024); volume discounts up to 12%; payment terms 60–90 days; standard-paper price volatility ±6–10% (2024 ECMA). SMEs (150,000) use digital procurement (40%), pressing transparency and sustainability (72% of EU officers, 2024). Inapa offsets with JIT, EDI, VMI and sustainability services that lift account gross margins ~2–4 ppt.

| Metric | Value |

|---|---|

| Top-10 buyer spend | ~35% (2024) |

| Max volume discount | 12% |

| Payment terms | 60–90 days |

| Price volatility | ±6–10% (2024 ECMA) |

| Sustainability importance | 72% (2024) |

| SME digital procurement | 40% (2023) |

| Service margin lift | ~2–4 ppt |

Same Document Delivered

Inapa Porter's Five Forces Analysis

This preview shows the exact Inapa Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Inapa faces moderate supplier leverage, fragmented buyer power, and rising substitute threats from digital paperless trends, while scale and distribution costs temper new entrant risks and rival intensity remains competitive across European markets.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Inapa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Upstream Paper Producers

The European paper sector is highly consolidated: the top 10 mills control roughly 60% of coated paper capacity as of 2024, leaving merchants like Inapa with few large suppliers; this concentration lets mills set prices and ration supply—mill price hikes in 2023–24 pushed European pulp-based paper prices up ~25% year-on-year; distributors face limited negotiation power and often must absorb or pass these cost rises into a price-sensitive market.

Volatility in Energy and Raw Material Costs

Suppliers face large swings in wood pulp and energy costs; pulp prices rose ~18% in 2024 and European wholesale electricity peaked at €350/MWh in Aug 2022, with volatility persisting into 2025, so suppliers quickly pass spikes to merchants.

By end-2025 supply contracts show pass-through clauses; Inapa is exposed as suppliers prioritize margin, with pulp and energy representing ~40–55% of upstream cost for paper merchants, raising short-term price risk.

Strategic Pivot Toward Specialized Packaging

Integration of ESG and Sustainability Standards

Inapa relies on certified suppliers to serve corporate clients and comply with procurement rules, so compliant vendors can insist on longer contracts and stricter traceability terms, reducing Inapa’s bargaining room.

Logistical Dependencies and Lead Times

Logistical capabilities and proximity of major paper mills to Inapa’s €1.1bn distribution hubs in Iberia and France strongly affect supply reliability; mills within 200–500 km typically offer lead times of 3–7 days versus 10–21 days from distant suppliers.

Suppliers with better transport networks secure firmer pricing and credit terms by promising 95%+ on-time delivery; regional road strikes or port slowdowns in 2024 raised lead-time variance by 40%.

Mill-level labor shortages or outages can cut merchant inventory turnover from 8x to 4x annually, sharply raising stockout risk and emergency freight costs.

- Closer mills: 3–7 day lead times

- Distant mills: 10–21 day lead times

- On-time delivery target: 95%+

- 2024 disruptions ↑ lead-time variance 40%

- Turnover drop: 8x to 4x raises stockout risk

Supplier power surges: mills dominate, input costs 40–55%, lead-times spike

Suppliers hold strong leverage: top 10 mills ~60% coated-capacity (2024), pulp costs +18% (2024) and certified-fiber premiums 6–12% (2024) push Inapa’s input share to ~40–55% of product cost; lead times 3–7d (near) vs 10–21d (far), 95%+ OTIF target, 2024 disruptions raised lead-time variance 40%, forcing longer contracts and 5–10% volume premiums.

| Metric | Value (year) |

|---|---|

| Top-10 mill share | ~60% (2024) |

| Pulp price change | +18% (2024) |

| Certified premium | 6–12% (2024) |

| Input cost share | 40–55% |

| Lead times | 3–7d / 10–21d |

| Lead-time variance ↑ | 40% (2024) |

What is included in the product

Tailored exclusively for Inapa, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier influence, entry barriers, substitute threats, and disruptive trends affecting its market position and profitability.

A concise Porter's Five Forces snapshot for Inapa—streamlines competitor, supplier, buyer, new entrant, and substitute pressures into a single, board-ready view to speed strategic decisions.

Customers Bargaining Power

High Price Sensitivity in Commercial Printing

Commercial printers, Inapa’s main customers, run on single-digit net margins and treat standard paper grades as commodities, triggering extreme price sensitivity and easy switching for 1–3% per-sheet savings.

Inapa reported European gross margin pressure in 2024—distribution segment EBITDA margin fell to ~3.5%—as it repeatedly entered price-driven bids to defend volumes.

Fragmentation of the Small and Medium Enterprise Segment

While large printing houses each hold strong bargaining leverage, most of Inapa’s market is fragmented: over 150,000 European SMEs in paper and print (2024 Eurostat trade data) have low individual clout but high collective switching power because 40% now use digital procurement platforms with transparent pricing (2023 McKinsey survey). Inapa must offer bundled logistics, same‑day distribution, and trade credit (typical SME DSO 45–60 days) to retain loyalty.

Shift Toward Digital and Sustainable Solutions

Modern buyers push for eco-friendly paper and digital ordering; 72% of EU procurement officers rate sustainability as a buying criterion (2024 Eurobarometer).

Clients now request carbon-footprint data and recycled-content certificates; 38% of contracts in EU paper supply chains included sustainability clauses in 2023.

Merchants lacking transparent, digital sustainability tools risk losing share to niche suppliers—Inapa could face a 5–12% revenue hit in affected segments within 24 months.

Consolidation of Large Print Groups

Consolidation among print groups has created buyers controlling larger volumes and professional procurement; top 10 European print groups now account for roughly 35% of commercial print spend (2024), boosting their leverage.

These groups extract volume discounts up to 12% and push 60–90‑day payment terms, straining merchants’ working capital; Inapa faces margin pressure and higher DSO (days sales outstanding).

Inapa must offer advanced supply‑chain integration—EDI, vendor‑managed inventory, dynamic pricing—to stay a preferred partner for these industrial buyers.

- Top 10 buyers ~35% spend (2024)

- Volume discounts up to 12%

- Payment terms 60–90 days

- Requires EDI, VMI, dynamic pricing

Low Switching Costs for Standard Products

For commodity graphic papers and basic packaging, switching costs from Inapa to rivals are negligible, letting buyers pressure margins; industry data shows standard grades face price volatility of ±6-10% annually (2024 ECMA index). Inapa counters by selling technical expertise and value-added services—color management, just-in-time logistics, and sustainability certification—that raise entanglement and can lift account gross margins by ~2–4 percentage points.

- Low switching cost; price volatility 6–10% (2024 ECMA)

- Buyers use distributor competition to cut prices

- Inapa adds services: color management, JIT, sustainability

- Value services can increase account gross margin ~2–4 ppt

Inapa boosts margins 2–4ppt with JIT/EDI/VMI as buyers demand price, transparency, sustainability

Buyers are highly price-sensitive: top 10 printers = ~35% spend (2024); volume discounts up to 12%; payment terms 60–90 days; standard-paper price volatility ±6–10% (2024 ECMA). SMEs (150,000) use digital procurement (40%), pressing transparency and sustainability (72% of EU officers, 2024). Inapa offsets with JIT, EDI, VMI and sustainability services that lift account gross margins ~2–4 ppt.

| Metric | Value |

|---|---|

| Top-10 buyer spend | ~35% (2024) |

| Max volume discount | 12% |

| Payment terms | 60–90 days |

| Price volatility | ±6–10% (2024 ECMA) |

| Sustainability importance | 72% (2024) |

| SME digital procurement | 40% (2023) |

| Service margin lift | ~2–4 ppt |

Same Document Delivered

Inapa Porter's Five Forces Analysis

This preview shows the exact Inapa Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.