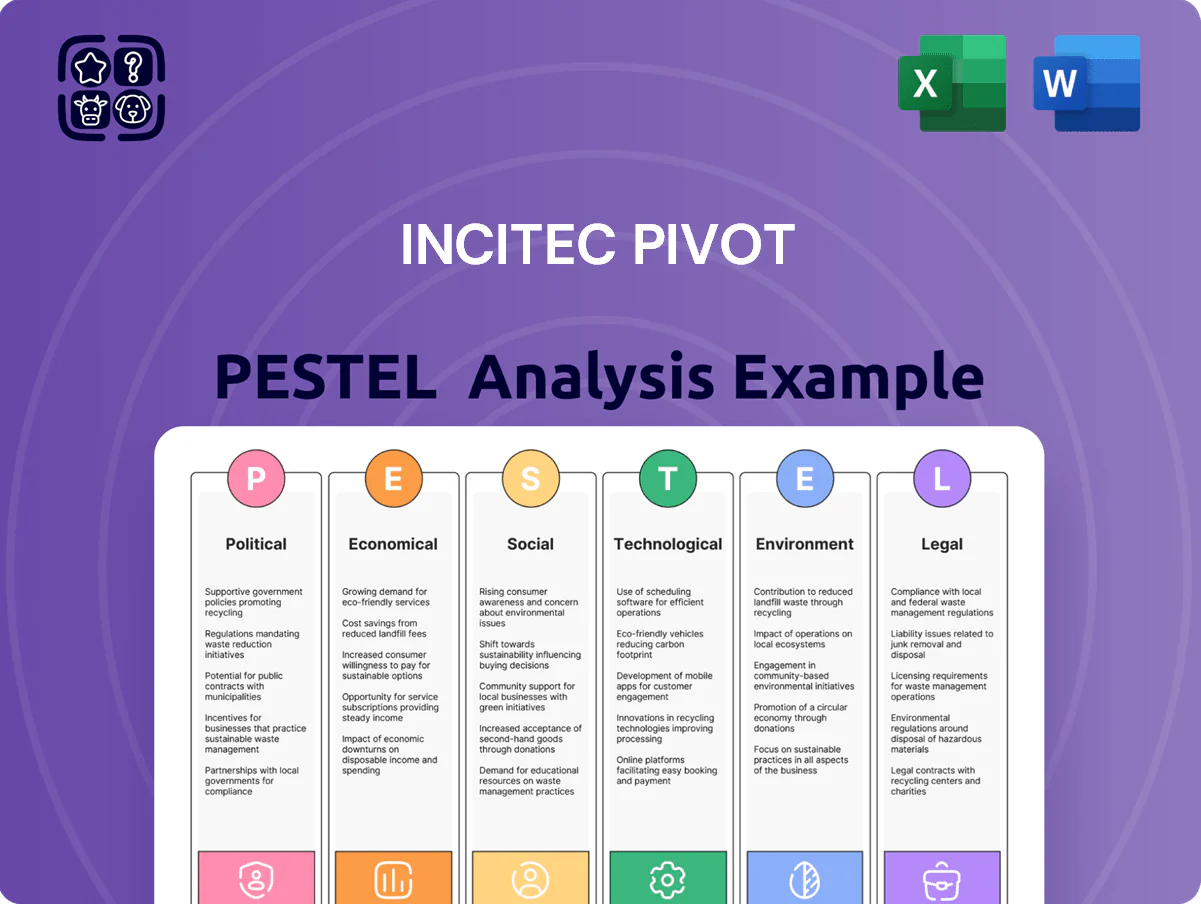

Incitec Pivot PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of Incitec Pivot—uncover how political, economic, social, technological, legal, and environmental forces are shaping its strategy and performance. Ideal for investors and strategists, this concise briefing highlights key external risks and opportunities. Purchase the full report to access in-depth, editable insights and actionable recommendations ready for immediate use.

Political factors

Geopolitical Trade Relations

Geopolitical trade relations shape Incitec Pivot’s Fertilisers and Dyno Nobel exports, with Australia, the US and key Asian markets (China, India, SEA) driving 60-75% of regional demand; 2024 tariffs and supply curbs raised Australian ammonia import costs by ~12% YoY, pressuring gross margins. Management must hedge inputs and diversify suppliers after 2023–25 trade tensions cut some export volumes by ~8%, safeguarding ~A$3.2bn in segment revenues.

Government Agricultural Subsidies

Political decisions on farmer subsidies in Australia and North America directly influence Incitec Pivot’s customer purchasing power; Australian farm support reached A$2.1bn in 2024 while US federal farm programs totaled about US$33.9bn in FY2024, affecting fertilizer affordability.

Shifts in policy have driven demand swings for NPK and specialty blends—Incitec Pivot reported a 7% volume variance in crop nutrient sales in 2023 tied to subsidy-related cropping changes.

Monitoring legislative shifts in farm support programs is essential for revenue forecasting, as modeled scenarios in 2025 show up to ±6% impact on domestic sales under different subsidy outcomes.

Mining Sector Regulations

As a supplier of industrial explosives, Incitec Pivot is highly exposed to political shifts on coal and mineral mining; Australia’s 2024 plan to phase down thermal coal and the EU’s 2024 Green Deal Industrial Plan risk reducing new mining permits, potentially denting Dyno Nobel revenues (mining accounted for ~45% of APAC explosives sales in FY2024). Conversely, US and Canadian incentives for critical minerals (eg. US IRA and 2024 Canada Critical Minerals Strategy) support higher explosives demand and represent a material growth tailwind.

Energy Security Policies

The manufacturing of nitrogen-based products is highly energy-intensive; natural gas accounts for roughly 60–70% of feedstock and energy costs for Incitec Pivot, with FY2024 gas spend estimated around A$500–700m.

Political interventions—domestic gas reservation, price caps or export curbs—can raise unit costs and disrupt supply, materially affecting margins and capex decisions.

Alignment with Australia’s 2025 National Gas Strategy and state energy security measures is essential to sustain domestic production and avoid relocation risk.

- Gas = ~60–70% of production costs

- Estimated FY2024 gas spend A$500–700m

- Policy risks: reservation, price caps, export limits

- Compliance with 2025 National Gas Strategy crucial

Foreign Investment Oversight

As a major industrial player, Incitec Pivot is regularly reviewed by the Foreign Investment Review Board; in 2024 Australia recorded A$85.9bn in foreign investment approvals, highlighting heightened scrutiny of resource and agricultural assets.

Political sensitivity over ownership of fertiliser plants and explosives facilities can delay or block M&A, directly affecting IPIC’s divestment and acquisition timelines and valuation assumptions.

Navigating FIRB and state-level approvals is integral to strategic planning—delays can shift capital allocation and impact FY2024–25 EBITDA forecasts (IPIC reported A$387m underlying EBITDA H1 FY2025).

- FIRB reviews intensive for agri/industrial assets

- 2024 AU foreign investment approvals A$85.9bn

- IPIC H1 FY2025 underlying EBITDA A$387m

- Regulatory delays affect M&A timing and valuations

Political risks squeeze margins—A$3.2bn fertiliser exposure, H1 EBITDA A$387m

Political risks—trade tensions, farm subsidies, gas policy, FIRB scrutiny—drive ±6% revenue variance and squeeze margins; 2024 data: ammonia import costs +12% YoY, A$500–700m gas spend, A$3.2bn fertiliser revenue at risk, FY2024 explosives mining = ~45% APAC sales, H1 FY2025 underlying EBITDA A$387m.

| Metric | 2024/25 |

|---|---|

| Ammonia import cost change | +12% YoY |

| Gas spend | A$500–700m |

| Fert. revenue at risk | A$3.2bn |

| Explosives mining share | ~45% APAC |

| H1 FY2025 EBITDA | A$387m |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Incitec Pivot, with data-driven insights and trend analysis tailored to its industry and regions to reveal risks, opportunities, and strategic implications for executives, investors, and advisors.

Condenses Incitec Pivot’s full PESTLE into a single, shareable summary that’s easy to drop into presentations or planning sessions, visually segmented by category for quick interpretation and editable for region- or business-specific notes.

Economic factors

Natural Gas Price Volatility

Natural gas is the primary feedstock for ammonia production, so Incitec Pivot’s margins are highly sensitive to energy market swings; European TTF averaged €40/MWh in 2024 vs €80/MWh in 2022, illustrating potential margin pressure. High gas prices can squeeze fertilizer profitability unless costs are passed to farmers—global fertilizer prices fell 18% in 2024 but remain volatile. The company uses hedging and long-term supply contracts covering ~60% of gas needs through 2026 to mitigate spikes.

Global Commodity Price Cycles

Demand for fertilizers tracks soft commodity prices; with global wheat at ~US$280/ton and corn ~US$240/ton in 2025, higher crop prices tend to raise farmer willingness to buy premium fertilizers, supporting Incitec Pivot’s revenues (FY2025 revenue AU$4.1bn).

Conversely, oversupply or price drops—e.g., 2024 global sugar surplus and 10% year decline in some crop prices—reduces application rates and sales volumes, pressuring margins and inventory levels.

Currency Exchange Rate Fluctuations

With significant operations in Australia and North America, Incitec Pivot faces exposure to AUD/USD swings; the AUD strengthened ~8% vs USD in 2023–2024, which can erode export competitiveness and lower translated US earnings (IPG reported ~USD-denominated sales comprising a material share of revenue in FY2024). Financial teams use hedging—forwards/options—and natural offsets to protect margins from adverse currency moves.

Interest Rate and Inflationary Pressures

Rising interest rates raise Incitec Pivot’s debt servicing costs for capital-intensive projects; Australian cash rate rose from 0.10% (2021) to 4.35% by Nov 2023 and sat at 4.10% in Jan 2026, increasing financing burdens for new plants and maintenance.

Inflation—Australia’s CPI was 3.6% in 2025—elevates labour, logistics and raw material costs, pressuring margins and requiring disciplined cost management and pricing power.

Higher financing costs and inflation constrain feasibility of large-scale capex and delay expansion unless returns exceed elevated hurdle rates.

- Higher cash rate (4.10% Jan 2026) increases WACC and project payback thresholds

- CPI ~3.6% (2025) raises input costs and wage pressures

- Requires tighter cost control, selective capex and stronger pricing

Industrial Production Demand

The explosives division Dyno Nobel depends on construction and quarrying activity; global infrastructure investment rose to about USD 4.5 trillion in 2024, supporting higher demand for blasting products.

Regions with major projects—India, China, and the US—drove volume growth; Australia mining capex recovered ~12% in 2024, benefiting explosives sales.

Conversely, 2023–2024 recessions saw construction starts fall up to 8% in some markets, causing temporary contractions in explosives consumption.

- 2024 global infrastructure spend ~USD 4.5T

- Australia mining capex +12% in 2024

- Construction starts down to 8% in some markets 2023–24

Fertilizer margins hinge on cheaper gas, hedges and crop prices amid AUD strength

Energy cost swings (TTF €40/MWh 2024 vs €80/MWh 2022) and gas hedges (~60% to 2026) drive fertilizer margins; FY2025 revenue AU$4.1bn. Crop prices (wheat ~US$280/t, corn ~US$240/t 2025) and 2024 fertilizer prices -18% affect demand. AUD strengthened ~8% vs USD (2023–24) and cash rate 4.10% Jan 2026 with CPI ~3.6% (2025) raise WACC and input costs.

| Metric | Value |

|---|---|

| TTF 2024 | €40/MWh |

| Wheat 2025 | US$280/t |

| FY2025 rev | AU$4.1bn |

| Cash rate Jan 2026 | 4.10% |

Full Version Awaits

Incitec Pivot PESTLE Analysis

The preview shown here is the exact Incitec Pivot PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

Everything displayed is part of the final, professionally structured file you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of Incitec Pivot—uncover how political, economic, social, technological, legal, and environmental forces are shaping its strategy and performance. Ideal for investors and strategists, this concise briefing highlights key external risks and opportunities. Purchase the full report to access in-depth, editable insights and actionable recommendations ready for immediate use.

Political factors

Geopolitical Trade Relations

Geopolitical trade relations shape Incitec Pivot’s Fertilisers and Dyno Nobel exports, with Australia, the US and key Asian markets (China, India, SEA) driving 60-75% of regional demand; 2024 tariffs and supply curbs raised Australian ammonia import costs by ~12% YoY, pressuring gross margins. Management must hedge inputs and diversify suppliers after 2023–25 trade tensions cut some export volumes by ~8%, safeguarding ~A$3.2bn in segment revenues.

Government Agricultural Subsidies

Political decisions on farmer subsidies in Australia and North America directly influence Incitec Pivot’s customer purchasing power; Australian farm support reached A$2.1bn in 2024 while US federal farm programs totaled about US$33.9bn in FY2024, affecting fertilizer affordability.

Shifts in policy have driven demand swings for NPK and specialty blends—Incitec Pivot reported a 7% volume variance in crop nutrient sales in 2023 tied to subsidy-related cropping changes.

Monitoring legislative shifts in farm support programs is essential for revenue forecasting, as modeled scenarios in 2025 show up to ±6% impact on domestic sales under different subsidy outcomes.

Mining Sector Regulations

As a supplier of industrial explosives, Incitec Pivot is highly exposed to political shifts on coal and mineral mining; Australia’s 2024 plan to phase down thermal coal and the EU’s 2024 Green Deal Industrial Plan risk reducing new mining permits, potentially denting Dyno Nobel revenues (mining accounted for ~45% of APAC explosives sales in FY2024). Conversely, US and Canadian incentives for critical minerals (eg. US IRA and 2024 Canada Critical Minerals Strategy) support higher explosives demand and represent a material growth tailwind.

Energy Security Policies

The manufacturing of nitrogen-based products is highly energy-intensive; natural gas accounts for roughly 60–70% of feedstock and energy costs for Incitec Pivot, with FY2024 gas spend estimated around A$500–700m.

Political interventions—domestic gas reservation, price caps or export curbs—can raise unit costs and disrupt supply, materially affecting margins and capex decisions.

Alignment with Australia’s 2025 National Gas Strategy and state energy security measures is essential to sustain domestic production and avoid relocation risk.

- Gas = ~60–70% of production costs

- Estimated FY2024 gas spend A$500–700m

- Policy risks: reservation, price caps, export limits

- Compliance with 2025 National Gas Strategy crucial

Foreign Investment Oversight

As a major industrial player, Incitec Pivot is regularly reviewed by the Foreign Investment Review Board; in 2024 Australia recorded A$85.9bn in foreign investment approvals, highlighting heightened scrutiny of resource and agricultural assets.

Political sensitivity over ownership of fertiliser plants and explosives facilities can delay or block M&A, directly affecting IPIC’s divestment and acquisition timelines and valuation assumptions.

Navigating FIRB and state-level approvals is integral to strategic planning—delays can shift capital allocation and impact FY2024–25 EBITDA forecasts (IPIC reported A$387m underlying EBITDA H1 FY2025).

- FIRB reviews intensive for agri/industrial assets

- 2024 AU foreign investment approvals A$85.9bn

- IPIC H1 FY2025 underlying EBITDA A$387m

- Regulatory delays affect M&A timing and valuations

Political risks squeeze margins—A$3.2bn fertiliser exposure, H1 EBITDA A$387m

Political risks—trade tensions, farm subsidies, gas policy, FIRB scrutiny—drive ±6% revenue variance and squeeze margins; 2024 data: ammonia import costs +12% YoY, A$500–700m gas spend, A$3.2bn fertiliser revenue at risk, FY2024 explosives mining = ~45% APAC sales, H1 FY2025 underlying EBITDA A$387m.

| Metric | 2024/25 |

|---|---|

| Ammonia import cost change | +12% YoY |

| Gas spend | A$500–700m |

| Fert. revenue at risk | A$3.2bn |

| Explosives mining share | ~45% APAC |

| H1 FY2025 EBITDA | A$387m |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Incitec Pivot, with data-driven insights and trend analysis tailored to its industry and regions to reveal risks, opportunities, and strategic implications for executives, investors, and advisors.

Condenses Incitec Pivot’s full PESTLE into a single, shareable summary that’s easy to drop into presentations or planning sessions, visually segmented by category for quick interpretation and editable for region- or business-specific notes.

Economic factors

Natural Gas Price Volatility

Natural gas is the primary feedstock for ammonia production, so Incitec Pivot’s margins are highly sensitive to energy market swings; European TTF averaged €40/MWh in 2024 vs €80/MWh in 2022, illustrating potential margin pressure. High gas prices can squeeze fertilizer profitability unless costs are passed to farmers—global fertilizer prices fell 18% in 2024 but remain volatile. The company uses hedging and long-term supply contracts covering ~60% of gas needs through 2026 to mitigate spikes.

Global Commodity Price Cycles

Demand for fertilizers tracks soft commodity prices; with global wheat at ~US$280/ton and corn ~US$240/ton in 2025, higher crop prices tend to raise farmer willingness to buy premium fertilizers, supporting Incitec Pivot’s revenues (FY2025 revenue AU$4.1bn).

Conversely, oversupply or price drops—e.g., 2024 global sugar surplus and 10% year decline in some crop prices—reduces application rates and sales volumes, pressuring margins and inventory levels.

Currency Exchange Rate Fluctuations

With significant operations in Australia and North America, Incitec Pivot faces exposure to AUD/USD swings; the AUD strengthened ~8% vs USD in 2023–2024, which can erode export competitiveness and lower translated US earnings (IPG reported ~USD-denominated sales comprising a material share of revenue in FY2024). Financial teams use hedging—forwards/options—and natural offsets to protect margins from adverse currency moves.

Interest Rate and Inflationary Pressures

Rising interest rates raise Incitec Pivot’s debt servicing costs for capital-intensive projects; Australian cash rate rose from 0.10% (2021) to 4.35% by Nov 2023 and sat at 4.10% in Jan 2026, increasing financing burdens for new plants and maintenance.

Inflation—Australia’s CPI was 3.6% in 2025—elevates labour, logistics and raw material costs, pressuring margins and requiring disciplined cost management and pricing power.

Higher financing costs and inflation constrain feasibility of large-scale capex and delay expansion unless returns exceed elevated hurdle rates.

- Higher cash rate (4.10% Jan 2026) increases WACC and project payback thresholds

- CPI ~3.6% (2025) raises input costs and wage pressures

- Requires tighter cost control, selective capex and stronger pricing

Industrial Production Demand

The explosives division Dyno Nobel depends on construction and quarrying activity; global infrastructure investment rose to about USD 4.5 trillion in 2024, supporting higher demand for blasting products.

Regions with major projects—India, China, and the US—drove volume growth; Australia mining capex recovered ~12% in 2024, benefiting explosives sales.

Conversely, 2023–2024 recessions saw construction starts fall up to 8% in some markets, causing temporary contractions in explosives consumption.

- 2024 global infrastructure spend ~USD 4.5T

- Australia mining capex +12% in 2024

- Construction starts down to 8% in some markets 2023–24

Fertilizer margins hinge on cheaper gas, hedges and crop prices amid AUD strength

Energy cost swings (TTF €40/MWh 2024 vs €80/MWh 2022) and gas hedges (~60% to 2026) drive fertilizer margins; FY2025 revenue AU$4.1bn. Crop prices (wheat ~US$280/t, corn ~US$240/t 2025) and 2024 fertilizer prices -18% affect demand. AUD strengthened ~8% vs USD (2023–24) and cash rate 4.10% Jan 2026 with CPI ~3.6% (2025) raise WACC and input costs.

| Metric | Value |

|---|---|

| TTF 2024 | €40/MWh |

| Wheat 2025 | US$280/t |

| FY2025 rev | AU$4.1bn |

| Cash rate Jan 2026 | 4.10% |

Full Version Awaits

Incitec Pivot PESTLE Analysis

The preview shown here is the exact Incitec Pivot PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

Everything displayed is part of the final, professionally structured file you’ll own upon checkout.