indie semiconductor Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Indie Semiconductor faces intense buyer scrutiny, evolving supplier dynamics, and tech-driven substitute risks that shape its margin potential and growth trajectory; this snapshot highlights core pressures but omits force-level ratings and quantified impacts.

This brief only scratches the surface — unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to indie semiconductor.

Suppliers Bargaining Power

Foundry manufacturing dependency

As a fabless firm, indie Semiconductor depends entirely on foundries such as TSMC and GlobalFoundries for automotive-grade chips, giving suppliers strong leverage.

Specialized manufacturing for ISO 26262-grade silicon limits high-end capacity; by 2025 TSMC and GF still control most advanced automotive node supply, keeping pricing power.

Even with ~2024–25 capacity expansions (TSMC capex ~$40B in 2024; GF investments $6B+), AI and ADAS demand sustains long lead times and margin pressure for indie.

Proprietary IP and EDA tool costs

The development of complex automotive SoCs forces indie semiconductor to rely on EDA vendors like Synopsys and Cadence and IP providers like Arm; Synopsys reported 2024 revenue of $5.6B and Arm’s 2024 licensing fees average tens of millions per design, so licensing and tool costs (EDA suites $0.5M–$5M+ per seat annually) keep upward pressure on indie’s OPEX and limit supplier substitution.

Specialized automotive raw materials

Suppliers of high-purity silicon carbide and specialized radar/lidar substrates are few—global SiC wafer capacity was ~1.1 million 6-inch equivalent wafers in 2024—giving them pricing and delivery leverage over indie semiconductor as automotive electrification raises demand.

Because top suppliers (e.g., Wolfspeed, II‑VI) control >60% of SiC capacity, supply shocks or longer lead times can raise unit costs by 10–30% and delay deliveries, materially affecting indie’s sensor and power management margins and time-to-market.

Limited high-end packaging providers

Post-fabrication automotive chips need advanced packaging to survive heat, vibration, and moisture; outsourced assembly/test (OSAT) firms meeting AEC‑Q and IATF standards are few, giving suppliers pricing power as indie Semiconductor scales multi-modal sensor packages.

Concentration: top 5 OSATs control ~60% of automotive advanced packaging revenue; specialized OSAT pricing grew ~8% YoY in 2024, pressuring indie’s margins on complex modules.

- Few certified OSATs: high entry barriers

- Top 5 = ~60% market share (2024)

- Specialized OSAT pricing +8% YoY (2024)

- Indie faces margin squeeze as complexity rises

Capacity allocation for advanced nodes

Securing capacity at sub-7nm nodes for advanced computer vision is a major bottleneck late 2025, with TSMC and Samsung reporting utilization >95% for 5nm/3nm lines and wafer prices up 18% YoY.

Foundries favor high-volume consumer and automotive IDMs, pushing indie semiconductor into multi-year offtake deals and $50–150M prepayments that raise manufacturers' leverage and increase indie's fixed costs.

This supply squeeze raises supply-side bargaining power, forcing indie to trade margin pressure for guaranteed node access and ramp predictability.

- TSMC/Samsung utilization >95%

- 5–3nm wafer price +18% YoY (2025)

- Typical prepayments $50–150M

- Multi-year offtakes (3–5 years) common

Chipmakers and suppliers choke auto semis: >90% sub‑7nm control, wafer costs +18%

Suppliers hold high bargaining power: TSMC/GlobalFoundries/Samsung dominate advanced automotive nodes (>90% of sub-7nm capacity), 5–3nm utilization >95% (late‑2025) and wafer prices +18% YoY, forcing indie into $50–150M prepayments and 3–5 year offtakes; EDA/IP (Synopsys $5.6B 2024) and SiC/OSAT concentration (top vendors >60% share; SiC capacity ~1.1M 6in wafers 2024) squeeze margins and raise lead‑time risk.

| Metric | Value |

|---|---|

| Sub-7nm share | >90% |

| 5–3nm utilization (late‑2025) | >95% |

| Wafer price change (2025) | +18% YoY |

| Prepayment range | $50–150M |

| EDA vendor revenue (Synopsys 2024) | $5.6B |

| SiC capacity (2024) | ~1.1M 6in wafers |

| Top OSAT market share | ~60% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to indie semiconductor, uncovering competitive pressures, supplier and buyer bargaining power, threat of entrants and substitutes, and strategic levers to defend and grow market share.

A concise Porter's Five Forces one-sheet for indie semiconductor firms—instantly highlights supplier/buyer leverage, entrant threats, substitutes, and rivalry to speed strategic choices.

Customers Bargaining Power

Tier 1 supplier market concentration

Indie Semiconductor primarily sells to a small set of powerful Tier 1 suppliers—Bosch, Continental, and Magna—who act as gatekeepers to OEMs and collectively accounted for ~25–30% of global automotive parts procurement in 2024; their scale lets them demand steep price concessions and extended payment terms.

Long-term automotive design cycles

The automotive industry’s 4–7 year design cycles lock buyers into chip choices, giving indie semiconductor steady revenue once a design win occurs but forcing fierce price competition at selection; OEMs secured average 30–40% supplier cost reductions in 2023 procurement rounds, squeezing margins.

High switching costs for OEMs

Buyers exert strong pressure during bidding, but switching to a new chip architecture mid-cycle is costly—software and hardware validation often exceed $5–10M and 6–12 months per platform, so indie Semiconductor can hold pricing after a design win if it hits performance milestones.

That creates a balanced dynamic: indie keeps gross margin leverage (gross margin 2024: ~32%) post-win, yet customers leverage the credible threat of switching on future models to extract better terms on current contracts.

Price pressure in volume segments

As ADAS and connectivity shift into mass-market cars, OEMs and Tier 1s are pushing hard on price; indie semiconductor must cut cost per unit to win large RFPs where margins compress.

By 2025, basic sensor functions are commoditized—industry reports show 20–30% YoY ASP (average selling price) decline for entry sensors—tilting bargaining power to volume buyers.

Indie’s competitive response: simplify silicon, consolidate IP, and target <$5 BOM reductions to protect 2024–25 revenue mix.

- OEM/Tier1 price focus rising

- 20–30% ASP decline for basic sensors by 2025

- Indie must cut BOM ≈$5/unit

- Bidding driven by cost, not features

Demand for highly customized solutions

Modern automakers demand highly customized integrated circuits to differentiate safety and UX, giving buyers leverage to insist on specific features and engineering support; in 2024 automotive semiconductor content rose ~15% to $80B, increasing OEM bargaining power.

Indie Semiconductor must weigh these customer demands against higher R&D and NRE costs—custom projects can raise per-unit costs by 20–40% and stretch development timelines 6–12 months.

- OEMs demand bespoke features, boosting bargaining power

- Automotive chip market $80B in 2024, +15% YoY

- Customization raises per-unit cost 20–40%

- Dev timelines extend 6–12 months, increasing cash burn

Buyers squeeze suppliers: $80B auto-chip market, indie margins 32% but costly to scale

Buyers (Tier1s/OEMs) hold strong leverage: they drove ~30% supplier share in 2024, forced 30–40% procurement cuts in 2023, and benefit from 15% YoY growth in auto chip spend to $80B (2024); ASPs for basic sensors fell 20–30% by 2025. Indie keeps ~32% gross margin post-win but faces $5–10M validation costs and needs ≈$5 BOM cuts to win volume RFPs.

| Metric | Value |

|---|---|

| Auto chip market 2024 | $80B (+15% YoY) |

| Indie gross margin 2024 | ~32% |

| Sensor ASP decline by 2025 | 20–30% |

| Validation cost | $5–10M |

| Needed BOM cut | ≈$5/unit |

Preview Before You Purchase

indie semiconductor Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Indie Semiconductor you'll receive immediately after purchase—no placeholders or mockups.

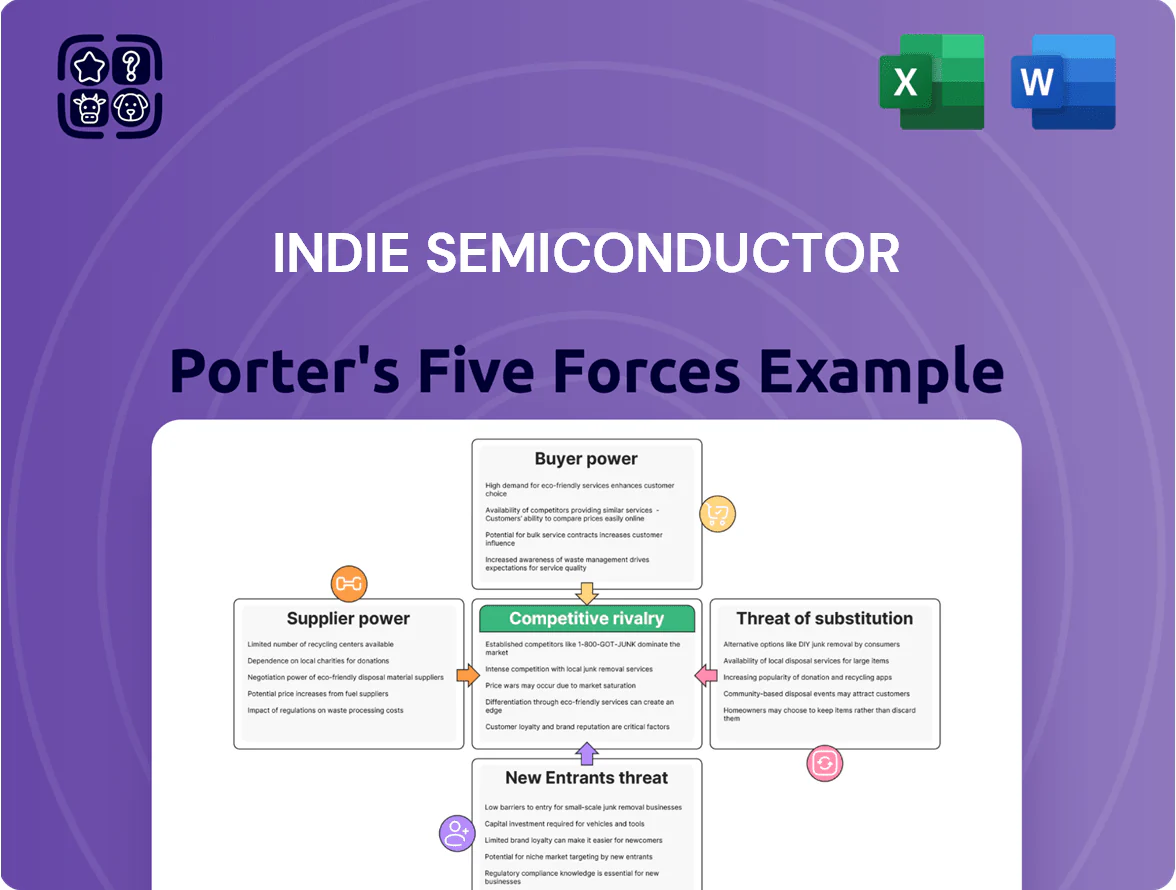

The document is the complete, professionally formatted deliverable, ready for download and use the moment you buy, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Indie Semiconductor faces intense buyer scrutiny, evolving supplier dynamics, and tech-driven substitute risks that shape its margin potential and growth trajectory; this snapshot highlights core pressures but omits force-level ratings and quantified impacts.

This brief only scratches the surface — unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to indie semiconductor.

Suppliers Bargaining Power

Foundry manufacturing dependency

As a fabless firm, indie Semiconductor depends entirely on foundries such as TSMC and GlobalFoundries for automotive-grade chips, giving suppliers strong leverage.

Specialized manufacturing for ISO 26262-grade silicon limits high-end capacity; by 2025 TSMC and GF still control most advanced automotive node supply, keeping pricing power.

Even with ~2024–25 capacity expansions (TSMC capex ~$40B in 2024; GF investments $6B+), AI and ADAS demand sustains long lead times and margin pressure for indie.

Proprietary IP and EDA tool costs

The development of complex automotive SoCs forces indie semiconductor to rely on EDA vendors like Synopsys and Cadence and IP providers like Arm; Synopsys reported 2024 revenue of $5.6B and Arm’s 2024 licensing fees average tens of millions per design, so licensing and tool costs (EDA suites $0.5M–$5M+ per seat annually) keep upward pressure on indie’s OPEX and limit supplier substitution.

Specialized automotive raw materials

Suppliers of high-purity silicon carbide and specialized radar/lidar substrates are few—global SiC wafer capacity was ~1.1 million 6-inch equivalent wafers in 2024—giving them pricing and delivery leverage over indie semiconductor as automotive electrification raises demand.

Because top suppliers (e.g., Wolfspeed, II‑VI) control >60% of SiC capacity, supply shocks or longer lead times can raise unit costs by 10–30% and delay deliveries, materially affecting indie’s sensor and power management margins and time-to-market.

Limited high-end packaging providers

Post-fabrication automotive chips need advanced packaging to survive heat, vibration, and moisture; outsourced assembly/test (OSAT) firms meeting AEC‑Q and IATF standards are few, giving suppliers pricing power as indie Semiconductor scales multi-modal sensor packages.

Concentration: top 5 OSATs control ~60% of automotive advanced packaging revenue; specialized OSAT pricing grew ~8% YoY in 2024, pressuring indie’s margins on complex modules.

- Few certified OSATs: high entry barriers

- Top 5 = ~60% market share (2024)

- Specialized OSAT pricing +8% YoY (2024)

- Indie faces margin squeeze as complexity rises

Capacity allocation for advanced nodes

Securing capacity at sub-7nm nodes for advanced computer vision is a major bottleneck late 2025, with TSMC and Samsung reporting utilization >95% for 5nm/3nm lines and wafer prices up 18% YoY.

Foundries favor high-volume consumer and automotive IDMs, pushing indie semiconductor into multi-year offtake deals and $50–150M prepayments that raise manufacturers' leverage and increase indie's fixed costs.

This supply squeeze raises supply-side bargaining power, forcing indie to trade margin pressure for guaranteed node access and ramp predictability.

- TSMC/Samsung utilization >95%

- 5–3nm wafer price +18% YoY (2025)

- Typical prepayments $50–150M

- Multi-year offtakes (3–5 years) common

Chipmakers and suppliers choke auto semis: >90% sub‑7nm control, wafer costs +18%

Suppliers hold high bargaining power: TSMC/GlobalFoundries/Samsung dominate advanced automotive nodes (>90% of sub-7nm capacity), 5–3nm utilization >95% (late‑2025) and wafer prices +18% YoY, forcing indie into $50–150M prepayments and 3–5 year offtakes; EDA/IP (Synopsys $5.6B 2024) and SiC/OSAT concentration (top vendors >60% share; SiC capacity ~1.1M 6in wafers 2024) squeeze margins and raise lead‑time risk.

| Metric | Value |

|---|---|

| Sub-7nm share | >90% |

| 5–3nm utilization (late‑2025) | >95% |

| Wafer price change (2025) | +18% YoY |

| Prepayment range | $50–150M |

| EDA vendor revenue (Synopsys 2024) | $5.6B |

| SiC capacity (2024) | ~1.1M 6in wafers |

| Top OSAT market share | ~60% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to indie semiconductor, uncovering competitive pressures, supplier and buyer bargaining power, threat of entrants and substitutes, and strategic levers to defend and grow market share.

A concise Porter's Five Forces one-sheet for indie semiconductor firms—instantly highlights supplier/buyer leverage, entrant threats, substitutes, and rivalry to speed strategic choices.

Customers Bargaining Power

Tier 1 supplier market concentration

Indie Semiconductor primarily sells to a small set of powerful Tier 1 suppliers—Bosch, Continental, and Magna—who act as gatekeepers to OEMs and collectively accounted for ~25–30% of global automotive parts procurement in 2024; their scale lets them demand steep price concessions and extended payment terms.

Long-term automotive design cycles

The automotive industry’s 4–7 year design cycles lock buyers into chip choices, giving indie semiconductor steady revenue once a design win occurs but forcing fierce price competition at selection; OEMs secured average 30–40% supplier cost reductions in 2023 procurement rounds, squeezing margins.

High switching costs for OEMs

Buyers exert strong pressure during bidding, but switching to a new chip architecture mid-cycle is costly—software and hardware validation often exceed $5–10M and 6–12 months per platform, so indie Semiconductor can hold pricing after a design win if it hits performance milestones.

That creates a balanced dynamic: indie keeps gross margin leverage (gross margin 2024: ~32%) post-win, yet customers leverage the credible threat of switching on future models to extract better terms on current contracts.

Price pressure in volume segments

As ADAS and connectivity shift into mass-market cars, OEMs and Tier 1s are pushing hard on price; indie semiconductor must cut cost per unit to win large RFPs where margins compress.

By 2025, basic sensor functions are commoditized—industry reports show 20–30% YoY ASP (average selling price) decline for entry sensors—tilting bargaining power to volume buyers.

Indie’s competitive response: simplify silicon, consolidate IP, and target <$5 BOM reductions to protect 2024–25 revenue mix.

- OEM/Tier1 price focus rising

- 20–30% ASP decline for basic sensors by 2025

- Indie must cut BOM ≈$5/unit

- Bidding driven by cost, not features

Demand for highly customized solutions

Modern automakers demand highly customized integrated circuits to differentiate safety and UX, giving buyers leverage to insist on specific features and engineering support; in 2024 automotive semiconductor content rose ~15% to $80B, increasing OEM bargaining power.

Indie Semiconductor must weigh these customer demands against higher R&D and NRE costs—custom projects can raise per-unit costs by 20–40% and stretch development timelines 6–12 months.

- OEMs demand bespoke features, boosting bargaining power

- Automotive chip market $80B in 2024, +15% YoY

- Customization raises per-unit cost 20–40%

- Dev timelines extend 6–12 months, increasing cash burn

Buyers squeeze suppliers: $80B auto-chip market, indie margins 32% but costly to scale

Buyers (Tier1s/OEMs) hold strong leverage: they drove ~30% supplier share in 2024, forced 30–40% procurement cuts in 2023, and benefit from 15% YoY growth in auto chip spend to $80B (2024); ASPs for basic sensors fell 20–30% by 2025. Indie keeps ~32% gross margin post-win but faces $5–10M validation costs and needs ≈$5 BOM cuts to win volume RFPs.

| Metric | Value |

|---|---|

| Auto chip market 2024 | $80B (+15% YoY) |

| Indie gross margin 2024 | ~32% |

| Sensor ASP decline by 2025 | 20–30% |

| Validation cost | $5–10M |

| Needed BOM cut | ≈$5/unit |

Preview Before You Purchase

indie semiconductor Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Indie Semiconductor you'll receive immediately after purchase—no placeholders or mockups.

The document is the complete, professionally formatted deliverable, ready for download and use the moment you buy, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry.