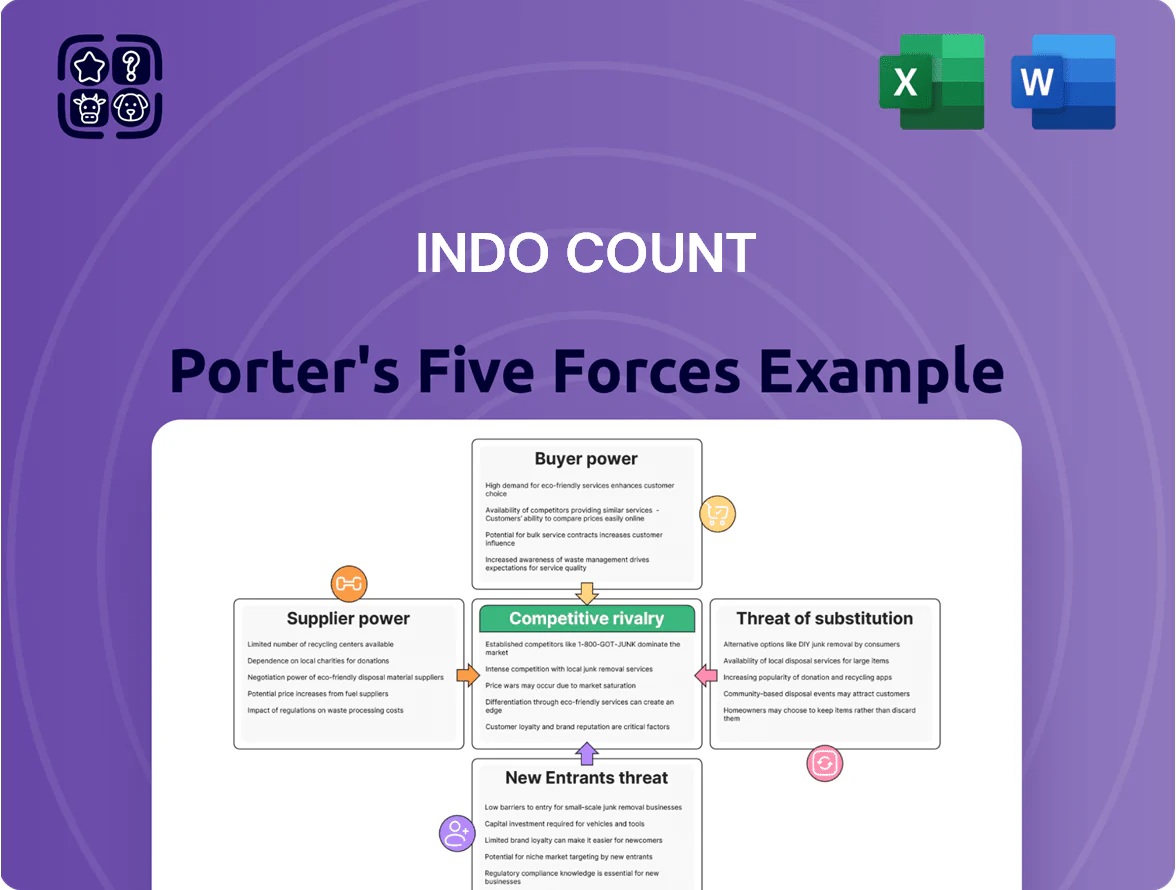

Indo Count Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Indo Count’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Cotton Price Volatility

Indo Count depends on cotton, a global commodity whose price swung ~28% in 2024–25 after adverse yields and export curbs; this volatility raises raw-material cost risk for margins.

The firm sources from thousands of farmers and ginners, so no single small supplier can set prices, limiting supplier concentration power.

Still, long-staple cotton for luxury linens is scarce—premium fiber suppliers command price premia up to 40%, giving them meaningful leverage.

Energy and Utility Costs

Manufacturing home textiles is energy‑intensive, needing steady power for spinning and weaving; electricity and fuel suppliers—often state utilities or regional monopolies—limit Indo Count’s bargaining on rates, squeezing margins. By December 2025 Indo Count deployed captive solar capacity totalling about 50 MW, cutting grid consumption by ~22% and trimming energy costs roughly 8–10% year on year. What this estimate hides: seasonal load and battery limits still force some grid reliance.

Specialized Chemical and Dye Providers

Indo Count relies on specialized dyes and chemicals to meet OEKO-TEX and similar standards; in 2024 roughly 35% of its suppliers had eco-certifications, limiting sourcing options.

Only about 8–12 global manufacturers supply consistent, certified chemicals at scale, concentrating supply and raising switching costs for Indo Count.

This concentration gives suppliers moderate bargaining power—price pass-throughs affected margins by an estimated 0.5–1.2 percentage points in 2023.

Logistics and Freight Dependencies

As an export-oriented firm, Indo Count relies on shipping lines and freight forwarders to access North American and European markets, and 2025 saw container rates spike 28% year-on-year amid geopolitical strains, giving large logistics firms strong bargaining power.

Indo Count mitigates this with multiyear contracts covering ~60% of volumes and spot-market hedges, but remains exposed to systemic shifts like port congestion and carrier consolidation that can quickly raise costs.

- 2025 container rate rise: +28%

- Long-term contracts: ~60% volumes

- Exposure: port congestion, carrier consolidation

- Leverage: large logistics firms set terms

Labor Market Dynamics

Indo Count must boost retention and training; companies that cut attrition to <15% vs. sector ~25% save ~3–5% in recruitment/training costs annually, protecting capacity and cost structure.

- Skilled pool large: 60–70% national workforce in hubs

- Wage pressure: +8–12% in 2024 in key states

- Attrition benchmark: sector ~25%, target <15%

- Savings: lower attrition ≈3–5% of annual HR costs

Moderate supplier power: cotton shocks, scarce long‑staple, shipping & inputs squeeze margins

Supplier power is moderate: commodity cotton price swings (≈+28% in 2024–25) and scarce long-staple fiber (premium +≈40%) raise input risk, while thousands of farm suppliers dilute concentration. Energy, certified chemicals (≈8–12 global suppliers) and shipping (container rates +28% in 2025; ~60% volumes under long contracts) give specific suppliers leverage, affecting margins ~0.5–1.2 ppt.

| Item | Key number |

|---|---|

| Cotton swing 2024–25 | +28% |

| Premium long-staple | +40% |

| Certified chemical suppliers | 8–12 |

| Container rate change 2025 | +28% |

| Long-term shipping cover | ~60% |

What is included in the product

Tailored Porter's Five Forces analysis for Indo Count that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats, with industry data and strategic implications to inform investor decks and strategic planning.

Compact Porter’s Five Forces snapshot for Indo Count—quickly spot competitive pressures and prioritize strategic moves to reduce supplier and buyer risks.

Customers Bargaining Power

Concentration of Global Retailers

Indo Count supplies global big-box retailers and department stores such as Walmart, Target, and Macy’s, which buy massive volumes and push for lower prices and tighter lead times.

By end-2025 retail consolidation left the top 10 US retailers controlling ~55% of apparel/home-textiles sales, shifting bargaining power to buyers and pressuring Indo Count’s margins.

Indo Count must keep operating margins above its 2024 reported 8.3% and improve on-time delivery to meet buyer SLAs and avoid contract losses.

Low Switching Costs for Brands

Low switching costs weaken Indo Count’s customer power: global brands can shift volume to Indian, Pakistani, or Vietnamese mills if Indo Count’s prices lag—India and Vietnam together exported $22.4B in home textiles in 2024, showing ample alternatives.

Home textile specs are standardized, so buyers can transfer orders with little technical friction; lead-time and cost drive switching more than capability.

Indo Count builds stickiness via design services and inventory management; in 2024 value-added sales grew ~12%, helping protect margins.

Demand for Sustainable Certifications

Price Sensitivity in Economic Downturns

Growth of Private Labels

Retailers' private-label home brands grew global share to ~18% of apparel & home textiles by 2024, letting buyers capture higher margins and control sourcing—this supplies Indo Count with volume but shifts value to retailer brands, constraining Indo Count’s own brand equity.

Retailers can benchmark Indo Count against low-cost makers worldwide; in 2024 top US and EU retailers sourced price-competitive private-label linens from Asia, pressuring Indo Count on yield and margin.

- Private-label share ~18% (2024)

- Provides stable volume, reduces brand equity

- Enables easy global benchmarking vs low-cost suppliers

- Pressures pricing, margins, and differentiation

Retailer Power Squeezes Indo Count: Rising audit costs, sustainability rules cut margins

Buyers (Walmart, Target, Macy’s) hold high bargaining power—top 10 US retailers ~55% of sales (end-2025), private-label ~18% (2024), and 72% of EU/US buyers required sustainability certs in 2025, forcing Indo Count to absorb rising audit/cert costs (~+12% in 2024) or face double-digit order cuts; low switching costs and standardized specs push price/lead-time pressure, squeezing margins (gross ~11.5% FY2023-24; operating 8.3% 2024).

| Metric | Value |

|---|---|

| Top-10 retailer share | ~55% (end-2025) |

| Private-label | ~18% (2024) |

| Sustainability req | 72% buyers (2025) |

| Audit cost rise | ~+12% (2024) |

| Gross margin | ~11.5% (FY2023-24) |

| Op margin | 8.3% (2024) |

Preview the Actual Deliverable

Indo Count Porter's Five Forces Analysis

This preview shows the exact Indo Count Porter’s Five Forces analysis you'll receive after purchase—fully formatted, professionally written, and ready for immediate use without placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Indo Count’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Cotton Price Volatility

Indo Count depends on cotton, a global commodity whose price swung ~28% in 2024–25 after adverse yields and export curbs; this volatility raises raw-material cost risk for margins.

The firm sources from thousands of farmers and ginners, so no single small supplier can set prices, limiting supplier concentration power.

Still, long-staple cotton for luxury linens is scarce—premium fiber suppliers command price premia up to 40%, giving them meaningful leverage.

Energy and Utility Costs

Manufacturing home textiles is energy‑intensive, needing steady power for spinning and weaving; electricity and fuel suppliers—often state utilities or regional monopolies—limit Indo Count’s bargaining on rates, squeezing margins. By December 2025 Indo Count deployed captive solar capacity totalling about 50 MW, cutting grid consumption by ~22% and trimming energy costs roughly 8–10% year on year. What this estimate hides: seasonal load and battery limits still force some grid reliance.

Specialized Chemical and Dye Providers

Indo Count relies on specialized dyes and chemicals to meet OEKO-TEX and similar standards; in 2024 roughly 35% of its suppliers had eco-certifications, limiting sourcing options.

Only about 8–12 global manufacturers supply consistent, certified chemicals at scale, concentrating supply and raising switching costs for Indo Count.

This concentration gives suppliers moderate bargaining power—price pass-throughs affected margins by an estimated 0.5–1.2 percentage points in 2023.

Logistics and Freight Dependencies

As an export-oriented firm, Indo Count relies on shipping lines and freight forwarders to access North American and European markets, and 2025 saw container rates spike 28% year-on-year amid geopolitical strains, giving large logistics firms strong bargaining power.

Indo Count mitigates this with multiyear contracts covering ~60% of volumes and spot-market hedges, but remains exposed to systemic shifts like port congestion and carrier consolidation that can quickly raise costs.

- 2025 container rate rise: +28%

- Long-term contracts: ~60% volumes

- Exposure: port congestion, carrier consolidation

- Leverage: large logistics firms set terms

Labor Market Dynamics

Indo Count must boost retention and training; companies that cut attrition to <15% vs. sector ~25% save ~3–5% in recruitment/training costs annually, protecting capacity and cost structure.

- Skilled pool large: 60–70% national workforce in hubs

- Wage pressure: +8–12% in 2024 in key states

- Attrition benchmark: sector ~25%, target <15%

- Savings: lower attrition ≈3–5% of annual HR costs

Moderate supplier power: cotton shocks, scarce long‑staple, shipping & inputs squeeze margins

Supplier power is moderate: commodity cotton price swings (≈+28% in 2024–25) and scarce long-staple fiber (premium +≈40%) raise input risk, while thousands of farm suppliers dilute concentration. Energy, certified chemicals (≈8–12 global suppliers) and shipping (container rates +28% in 2025; ~60% volumes under long contracts) give specific suppliers leverage, affecting margins ~0.5–1.2 ppt.

| Item | Key number |

|---|---|

| Cotton swing 2024–25 | +28% |

| Premium long-staple | +40% |

| Certified chemical suppliers | 8–12 |

| Container rate change 2025 | +28% |

| Long-term shipping cover | ~60% |

What is included in the product

Tailored Porter's Five Forces analysis for Indo Count that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats, with industry data and strategic implications to inform investor decks and strategic planning.

Compact Porter’s Five Forces snapshot for Indo Count—quickly spot competitive pressures and prioritize strategic moves to reduce supplier and buyer risks.

Customers Bargaining Power

Concentration of Global Retailers

Indo Count supplies global big-box retailers and department stores such as Walmart, Target, and Macy’s, which buy massive volumes and push for lower prices and tighter lead times.

By end-2025 retail consolidation left the top 10 US retailers controlling ~55% of apparel/home-textiles sales, shifting bargaining power to buyers and pressuring Indo Count’s margins.

Indo Count must keep operating margins above its 2024 reported 8.3% and improve on-time delivery to meet buyer SLAs and avoid contract losses.

Low Switching Costs for Brands

Low switching costs weaken Indo Count’s customer power: global brands can shift volume to Indian, Pakistani, or Vietnamese mills if Indo Count’s prices lag—India and Vietnam together exported $22.4B in home textiles in 2024, showing ample alternatives.

Home textile specs are standardized, so buyers can transfer orders with little technical friction; lead-time and cost drive switching more than capability.

Indo Count builds stickiness via design services and inventory management; in 2024 value-added sales grew ~12%, helping protect margins.

Demand for Sustainable Certifications

Price Sensitivity in Economic Downturns

Growth of Private Labels

Retailers' private-label home brands grew global share to ~18% of apparel & home textiles by 2024, letting buyers capture higher margins and control sourcing—this supplies Indo Count with volume but shifts value to retailer brands, constraining Indo Count’s own brand equity.

Retailers can benchmark Indo Count against low-cost makers worldwide; in 2024 top US and EU retailers sourced price-competitive private-label linens from Asia, pressuring Indo Count on yield and margin.

- Private-label share ~18% (2024)

- Provides stable volume, reduces brand equity

- Enables easy global benchmarking vs low-cost suppliers

- Pressures pricing, margins, and differentiation

Retailer Power Squeezes Indo Count: Rising audit costs, sustainability rules cut margins

Buyers (Walmart, Target, Macy’s) hold high bargaining power—top 10 US retailers ~55% of sales (end-2025), private-label ~18% (2024), and 72% of EU/US buyers required sustainability certs in 2025, forcing Indo Count to absorb rising audit/cert costs (~+12% in 2024) or face double-digit order cuts; low switching costs and standardized specs push price/lead-time pressure, squeezing margins (gross ~11.5% FY2023-24; operating 8.3% 2024).

| Metric | Value |

|---|---|

| Top-10 retailer share | ~55% (end-2025) |

| Private-label | ~18% (2024) |

| Sustainability req | 72% buyers (2025) |

| Audit cost rise | ~+12% (2024) |

| Gross margin | ~11.5% (FY2023-24) |

| Op margin | 8.3% (2024) |

Preview the Actual Deliverable

Indo Count Porter's Five Forces Analysis

This preview shows the exact Indo Count Porter’s Five Forces analysis you'll receive after purchase—fully formatted, professionally written, and ready for immediate use without placeholders or samples.