Indorama Ventures Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Indorama Ventures faces moderate buyer power and significant competitive rivalry driven by commodity pricing and capacity expansion, while supplier influence and substitute threats remain manageable due to integrated feedstock access and specialized product lines.

Regulatory and sustainability pressures raise barriers that both constrain new entrants and create differentiation opportunities for incumbents with scale and innovation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Indorama Ventures’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Feedstock Price Volatility

Feedstock price volatility heavily affects Indorama Ventures’ cost base because crude oil and natural gas set global prices for paraxylene and ethylene; in 2024 feedstock-linked costs swung ±22% year-over-year, squeezing margins. Suppliers gain leverage during supply tightness or geopolitical shocks—e.g., 2022–23 disruptions pushed benchmark paraxylene premiums up ~18%. Indorama mitigates via diversified sourcing and forward hedges covering ~30–40% of volumes, yet spot volatility still dominates margin risk.

Concentration of Key Raw Material Providers

Supplier concentration is high: fewer than 10 global producers can supply the high-purity paraxylene and ethylene glycol volumes Indorama needs, so upstream firms can push prices—spot PTA rose 24% in 2023 in Asia, showing leverage.

Regional bottlenecks matter: logistics and refinery outages in 2024 raised landed feedstock costs by ~12% in Southeast Asia, limiting switch options.

Indorama mitigates risk via long-term contracts: multi-year supply deals with BP (since 2021) and Saudi Aramco (2022) cover ~60% of feedstock needs, lowering short-term price exposure.

Strategic Vertical Integration

Indorama Ventures has reduced supplier power through strategic backward integration, adding PTA and MEG capacity—its 2024 integrated PTA/MEG output reached about 2.1 million tonnes, cutting third-party purchases by an estimated 35%.

This lowers exposure to feedstock price spikes; in 2023 feedstock volatility raised polyester margins swing by ~7 percentage points, which internal sourcing helped dampen in 2024.

Controlling more of the value chain lets Indorama internalize supplier margins and secure inputs, supporting more stable gross margins — 2024 adjusted gross margin improved to ~15.8% from 13.2% in 2022.

Regional Energy Cost Disparities

Energy suppliers, notably natural gas and electricity providers, wield differing bargaining power across Indorama Ventures’ manufacturing footprint; in 2024 European industrial gas prices averaged ~€35–45/MWh, squeezing PTA/PET margins, while US feedstock linked to shale gas kept ethylene-linked costs ~20–30% lower.

This variance forces Indorama to shift output and invest in energy efficiency and cogeneration to reduce local utility leverage and protect margins; 2023 capex on energy projects was about $120m.

- Europe: gas €35–45/MWh, high supplier leverage

- North America: shale gas lowers costs ~20–30%

- Action: $120m 2023 energy capex, footprint optimization

Transition Toward Bio-Based Feedstocks

As demand for low-carbon products rises, Indorama Ventures is shifting procurement toward bio-based feedstocks, weakening traditional fossil-fuel suppliers’ power; bio-based polymers accounted for about 8% of global PET feedstock initiatives by 2024, per industry reports.

Indorama is partnering with agricultural and biotech firms—pilots in 2023–2025 aimed to source >50 kt/year of renewable monoethylene glycol equivalents for its green lines, lowering oil dependence and creating new supplier segments.

Long term, bio-feedstock scaling (projected CAGR ~12% to 2030) will diversify inputs, reduce price correlation with crude, and introduce more fragmented supplier bargaining dynamics.

- Bio-feedstocks grew ~8% share in PET initiatives (2024)

- Indorama pilots target >50 kt/year renewable inputs (2023–25)

- Projected bio-feedstock CAGR ~12% to 2030

- Reduces oil-price exposure and supplier concentration

Suppliers tighten grip as Indorama’s 2.1Mt boost lifts margins to 15.8%

Suppliers hold moderate-to-high power: feedstock volatility (±22% y/y in 2024) and <10 global high‑purity PX/EG producers raise prices; long‑term deals (BP, Aramco) cover ~60% and forward hedges 30–40%, while Indorama’s 2024 PTA/MEG output ~2.1Mt cut third‑party buys ~35%, lifting adjusted gross margin to ~15.8% in 2024.

| Metric | 2024 |

|---|---|

| Feedstock vol | ±22% y/y |

| Integrated PTA/MEG | 2.1Mt |

| Long‑term cover | ~60% |

| Adj. gross margin | 15.8% |

What is included in the product

Tailored Porter's Five Forces analysis for Indorama Ventures that uncovers competitive pressures, supplier and buyer influence, threat of substitutes and new entrants, and identifies disruptive forces affecting pricing and profitability.

An at-a-glance Porter's Five Forces summary for Indorama Ventures—streamlines competitive insights into a single sheet for rapid strategic decisions.

Customers Bargaining Power

Consolidation of Global Consumer Brands

Mandates for Recycled Content

Major beverage and packaging buyers now demand higher recycled PET (rPET) shares—EU targets require 30% rPET in PET bottles by 2030 and Coca‑Cola aims for 50% recycled content by 2030—boosting buyer leverage.

Buyers push for suppliers who can deliver high‑quality rPET at scale to meet regs and ESG goals; this raises switching costs and price sensitivity for firms lacking circular supply chains.

Indorama Ventures has invested >$1.2bn in recycling since 2019 and operates 40+ recycling lines globally, directly responding to customer mandates and reducing buyer bargaining power by assuring supply.

Low Switching Costs for Standard Grades

For commodity PET and standard fibres, switching costs are low so buyers shift suppliers over price differences; global spot PET prices fell ~18% in 2024, sharpening this pressure.

Buyers prioritize price-per-ton and logistics; average delivered PET margin compression reached ~120–180 USD/ton in 2024 for integrated producers.

Indorama counters with specialty grades and services—R&D-driven formulations and on-site technical support—aiming to raise switching costs via deeper production integration.

Demand for Just-in-Time Global Supply

Large multinationals demand consistent, continent-spanning quality; Indorama Ventures’ 2025 footprint—over 100 manufacturing sites across 33 countries—helps meet that need but raises expectations for seamless logistics and local inventory.

Customers press for localized production near bottling plants, forcing Indorama to balance capex: its 2024 capex was about $450 million, and further localization would strain cash flow and facility management.

Higher customer bargaining power increases pressure on lead-time guarantees, service-level penalties, and near-shore investments, affecting margins and working capital.

- 100+ sites in 33 countries (2025)

- 2024 capex ≈ $450 million

- Local production raises capex and OPEX

- Stronger service SLAs reduce pricing power

Price Transparency and Market Benchmarking

Price transparency in petrochemicals is high: PET and PTA indices (ICIS, Platts) are monitored daily, with PET spot in 2025 averaging about $1,000/ton and PTA near $650/ton, letting buyers benchmark and push spreads.

That real-time data enables aggressive negotiation; customers use spread analysis (PET−PTA) to demand price cuts when spreads tighten, pressuring margins.

Indorama must run near-top quartile plant utilization and cost per ton to keep prices competitive while preserving margins; EBIT per ton targets need tight control.

- Daily PET/PTA indices used for bids

- 2025 avg PET ~$1,000/ton; PTA ~$650/ton

- Buyers negotiate on PET−PTA spread

- Indorama needs top-quartile costs to protect EBIT/ton

Indorama Battles Margin Squeeze as Buyers, rPET Rules and $1.2bn Recycling Pushes Prices

| Metric | Value |

|---|---|

| PET price (2025) | $1,000/ton |

| PTA (2025) | $650/ton |

| Sites | 100+ |

| Recycling spend | $1.2bn |

Same Document Delivered

Indorama Ventures Porter's Five Forces Analysis

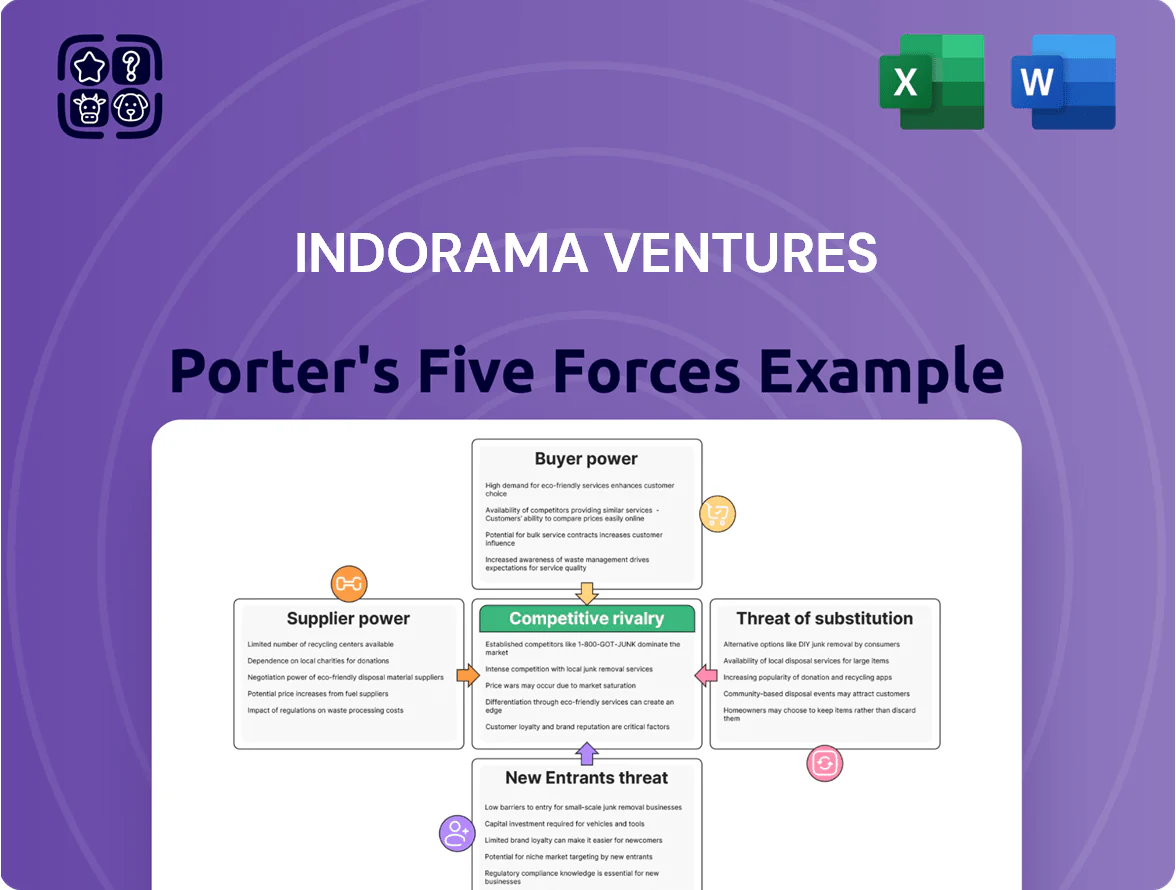

This preview shows the exact Indorama Ventures Porter's Five Forces analysis you'll receive instantly after purchase—no placeholders or mockups, fully formatted and ready for use. The document covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with concise insights and actionable implications. What you see is the final deliverable, downloadable immediately upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Indorama Ventures faces moderate buyer power and significant competitive rivalry driven by commodity pricing and capacity expansion, while supplier influence and substitute threats remain manageable due to integrated feedstock access and specialized product lines.

Regulatory and sustainability pressures raise barriers that both constrain new entrants and create differentiation opportunities for incumbents with scale and innovation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Indorama Ventures’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Feedstock Price Volatility

Feedstock price volatility heavily affects Indorama Ventures’ cost base because crude oil and natural gas set global prices for paraxylene and ethylene; in 2024 feedstock-linked costs swung ±22% year-over-year, squeezing margins. Suppliers gain leverage during supply tightness or geopolitical shocks—e.g., 2022–23 disruptions pushed benchmark paraxylene premiums up ~18%. Indorama mitigates via diversified sourcing and forward hedges covering ~30–40% of volumes, yet spot volatility still dominates margin risk.

Concentration of Key Raw Material Providers

Supplier concentration is high: fewer than 10 global producers can supply the high-purity paraxylene and ethylene glycol volumes Indorama needs, so upstream firms can push prices—spot PTA rose 24% in 2023 in Asia, showing leverage.

Regional bottlenecks matter: logistics and refinery outages in 2024 raised landed feedstock costs by ~12% in Southeast Asia, limiting switch options.

Indorama mitigates risk via long-term contracts: multi-year supply deals with BP (since 2021) and Saudi Aramco (2022) cover ~60% of feedstock needs, lowering short-term price exposure.

Strategic Vertical Integration

Indorama Ventures has reduced supplier power through strategic backward integration, adding PTA and MEG capacity—its 2024 integrated PTA/MEG output reached about 2.1 million tonnes, cutting third-party purchases by an estimated 35%.

This lowers exposure to feedstock price spikes; in 2023 feedstock volatility raised polyester margins swing by ~7 percentage points, which internal sourcing helped dampen in 2024.

Controlling more of the value chain lets Indorama internalize supplier margins and secure inputs, supporting more stable gross margins — 2024 adjusted gross margin improved to ~15.8% from 13.2% in 2022.

Regional Energy Cost Disparities

Energy suppliers, notably natural gas and electricity providers, wield differing bargaining power across Indorama Ventures’ manufacturing footprint; in 2024 European industrial gas prices averaged ~€35–45/MWh, squeezing PTA/PET margins, while US feedstock linked to shale gas kept ethylene-linked costs ~20–30% lower.

This variance forces Indorama to shift output and invest in energy efficiency and cogeneration to reduce local utility leverage and protect margins; 2023 capex on energy projects was about $120m.

- Europe: gas €35–45/MWh, high supplier leverage

- North America: shale gas lowers costs ~20–30%

- Action: $120m 2023 energy capex, footprint optimization

Transition Toward Bio-Based Feedstocks

As demand for low-carbon products rises, Indorama Ventures is shifting procurement toward bio-based feedstocks, weakening traditional fossil-fuel suppliers’ power; bio-based polymers accounted for about 8% of global PET feedstock initiatives by 2024, per industry reports.

Indorama is partnering with agricultural and biotech firms—pilots in 2023–2025 aimed to source >50 kt/year of renewable monoethylene glycol equivalents for its green lines, lowering oil dependence and creating new supplier segments.

Long term, bio-feedstock scaling (projected CAGR ~12% to 2030) will diversify inputs, reduce price correlation with crude, and introduce more fragmented supplier bargaining dynamics.

- Bio-feedstocks grew ~8% share in PET initiatives (2024)

- Indorama pilots target >50 kt/year renewable inputs (2023–25)

- Projected bio-feedstock CAGR ~12% to 2030

- Reduces oil-price exposure and supplier concentration

Suppliers tighten grip as Indorama’s 2.1Mt boost lifts margins to 15.8%

Suppliers hold moderate-to-high power: feedstock volatility (±22% y/y in 2024) and <10 global high‑purity PX/EG producers raise prices; long‑term deals (BP, Aramco) cover ~60% and forward hedges 30–40%, while Indorama’s 2024 PTA/MEG output ~2.1Mt cut third‑party buys ~35%, lifting adjusted gross margin to ~15.8% in 2024.

| Metric | 2024 |

|---|---|

| Feedstock vol | ±22% y/y |

| Integrated PTA/MEG | 2.1Mt |

| Long‑term cover | ~60% |

| Adj. gross margin | 15.8% |

What is included in the product

Tailored Porter's Five Forces analysis for Indorama Ventures that uncovers competitive pressures, supplier and buyer influence, threat of substitutes and new entrants, and identifies disruptive forces affecting pricing and profitability.

An at-a-glance Porter's Five Forces summary for Indorama Ventures—streamlines competitive insights into a single sheet for rapid strategic decisions.

Customers Bargaining Power

Consolidation of Global Consumer Brands

Mandates for Recycled Content

Major beverage and packaging buyers now demand higher recycled PET (rPET) shares—EU targets require 30% rPET in PET bottles by 2030 and Coca‑Cola aims for 50% recycled content by 2030—boosting buyer leverage.

Buyers push for suppliers who can deliver high‑quality rPET at scale to meet regs and ESG goals; this raises switching costs and price sensitivity for firms lacking circular supply chains.

Indorama Ventures has invested >$1.2bn in recycling since 2019 and operates 40+ recycling lines globally, directly responding to customer mandates and reducing buyer bargaining power by assuring supply.

Low Switching Costs for Standard Grades

For commodity PET and standard fibres, switching costs are low so buyers shift suppliers over price differences; global spot PET prices fell ~18% in 2024, sharpening this pressure.

Buyers prioritize price-per-ton and logistics; average delivered PET margin compression reached ~120–180 USD/ton in 2024 for integrated producers.

Indorama counters with specialty grades and services—R&D-driven formulations and on-site technical support—aiming to raise switching costs via deeper production integration.

Demand for Just-in-Time Global Supply

Large multinationals demand consistent, continent-spanning quality; Indorama Ventures’ 2025 footprint—over 100 manufacturing sites across 33 countries—helps meet that need but raises expectations for seamless logistics and local inventory.

Customers press for localized production near bottling plants, forcing Indorama to balance capex: its 2024 capex was about $450 million, and further localization would strain cash flow and facility management.

Higher customer bargaining power increases pressure on lead-time guarantees, service-level penalties, and near-shore investments, affecting margins and working capital.

- 100+ sites in 33 countries (2025)

- 2024 capex ≈ $450 million

- Local production raises capex and OPEX

- Stronger service SLAs reduce pricing power

Price Transparency and Market Benchmarking

Price transparency in petrochemicals is high: PET and PTA indices (ICIS, Platts) are monitored daily, with PET spot in 2025 averaging about $1,000/ton and PTA near $650/ton, letting buyers benchmark and push spreads.

That real-time data enables aggressive negotiation; customers use spread analysis (PET−PTA) to demand price cuts when spreads tighten, pressuring margins.

Indorama must run near-top quartile plant utilization and cost per ton to keep prices competitive while preserving margins; EBIT per ton targets need tight control.

- Daily PET/PTA indices used for bids

- 2025 avg PET ~$1,000/ton; PTA ~$650/ton

- Buyers negotiate on PET−PTA spread

- Indorama needs top-quartile costs to protect EBIT/ton

Indorama Battles Margin Squeeze as Buyers, rPET Rules and $1.2bn Recycling Pushes Prices

| Metric | Value |

|---|---|

| PET price (2025) | $1,000/ton |

| PTA (2025) | $650/ton |

| Sites | 100+ |

| Recycling spend | $1.2bn |

Same Document Delivered

Indorama Ventures Porter's Five Forces Analysis

This preview shows the exact Indorama Ventures Porter's Five Forces analysis you'll receive instantly after purchase—no placeholders or mockups, fully formatted and ready for use. The document covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with concise insights and actionable implications. What you see is the final deliverable, downloadable immediately upon payment.