Indorama Ventures PESTLE Analysis

Your Competitive Advantage Starts with This Report

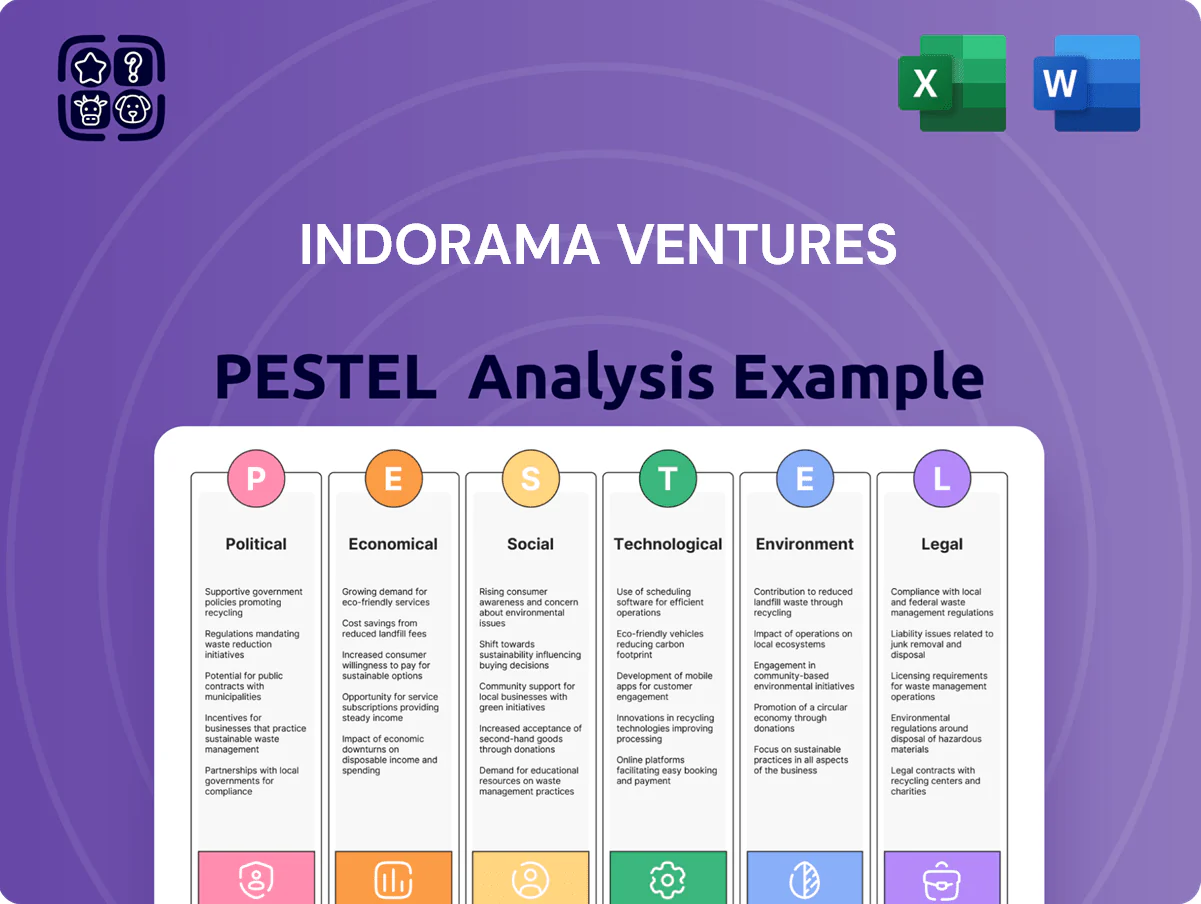

Gain a strategic advantage with our PESTLE Analysis of Indorama Ventures—unpack how politics, economics, social trends, technology, legal shifts, and environmental pressures will shape its growth and risks; buy the full report to get ready-to-use, expert insights and downloadable charts for investment or strategic planning.

Political factors

Trade protectionism and regional tariffs

The late-2025 trade landscape shows rising protectionism, with US and EU anti-dumping measures targeting Asian polyester/PET exporters—EU duties on certain PET imports reached up to 18.5% in 2024 while recent US investigations threaten similar levies. Indorama Ventures faces elevated compliance costs and margin pressure from tariffs and trade barriers that aim to shield domestic resin and fiber sectors. The company mitigates risk via a diversified manufacturing footprint—over 60 plants across 33 countries—shifting production into target markets to avoid import duties and preserve USD-denominated sales.

Geopolitical instability in energy-producing regions

Ongoing conflicts in Eastern Europe and the Middle East have driven Brent crude volatility, with 2024 average Brent at about $86/bbl and spot swings ±15% year-to-date, disrupting feedstock supply for Indorama Ventures’ PET and PTA chains; natural gas price spikes (EU TTF up ~40% vs 2023) raise production costs. Indorama uses strategic reserves and multiyear supply contracts—covering ~60–80% of feedstock needs in key plants—to stabilize operations and cash flow.

Government subsidies for green industrial transition

Regional political stability in Southeast Asia

As a Thailand-headquartered global chemicals leader, Indorama Ventures is exposed to ASEAN political shifts; Thailand's 2024 corporate tax rate remained at 20% for large firms while proposed incentives in 2025 target petrochemical clusters, potentially altering after-tax returns for local operations.

Government changes can reshape labor laws and export regulations affecting ~30% of IVL's 2024 Asia production capacity; active engagement with policymakers preserves incentives and supply-chain continuity.

- Headquarters exposure: Thailand policy affects corporate tax and incentives

- 2024 corporate tax baseline: 20% for major firms; 2025 incentive proposals for petrochemical hubs

- ~30% of IVL Asia production capacity sensitive to regional regulatory shifts

- Ongoing policymaker engagement essential to maintain stable operations

Global regulatory harmonization for plastics

International negotiations toward a global treaty on plastic pollution in 2025—backed by 175+ UN member states—are pushing for harmonized rules on production, waste management and circularity that will reshape petrochemical supply chains.

Indorama participates in industry forums and trade groups, aiming to influence standards so they remain technically feasible and economically viable amid projected regulatory compliance costs of up to $5–10 billion industry-wide by 2030.

- 175+ UN members engaged in treaty talks

- Global compliance cost estimate $5–10B by 2030

- Indorama active in industry forums to shape standards

- Focus areas: production limits, waste management, circularity

Protectionism, feedstock swings & plastics treaty reshape petrochem margins in 2024–25

Rising 2024–25 protectionism (EU PET duties up to 18.5%; US probes) and geopolitical-driven feedstock volatility (2024 Brent ~$86/bbl; EU TTF +40% vs 2023) elevate tariffs and input costs, while ~60 plants in 33 countries and multiyear contracts mitigate risk; green subsidies (~$150bn 2024–25) and Thailand’s 20% corporate tax plus 2025 petrochemical incentives improve CAPEX economics; 175+ states in 2025 plastics treaty raise compliance costs (industry $5–10B by 2030).

| Metric | Value |

|---|---|

| Brent 2024 avg | $86/bbl |

| EU PET duty (2024) | up to 18.5% |

| EU TTF change vs 2023 | +40% |

| Plants / Countries | ~60 / 33 |

| Green subsidies (2024–25) | ~$150bn |

| Thailand corp tax (2024) | 20% |

| UN treaty participants (2025) | 175+ |

| Industry compliance est. by 2030 | $5–10B |

What is included in the product

Explores how macro-environmental factors uniquely affect Indorama Ventures across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Indorama Ventures that relieves prep pain by providing an easily shareable, editable snapshot for meetings, presentations, and strategy sessions—ready to drop into decks or client reports and tailored with region- or business-line notes.

Economic factors

Volatility in feedstock and energy costs

Profitability at Indorama Ventures hinges on the spread between feedstocks such as paraxylene and MEG versus PET selling prices; in 2024 PET margins swung with paraxylene prices ranging $800–$1,200/ton and MEG $600–$900/ton versus average PET realizations near $1,200–$1,500/ton.

Global crude oil volatility—Brent averaged about $85/bbl in 2024—directly raised feedstock costs, forcing Indorama to use advanced hedging and feedstock integration to protect margins.

Shifts in chemical supply-demand, including 2024 Asian PX oversupply and regional MEG tightness, drove notable quarterly earnings volatility, with EBITDA margin fluctuations of several percentage points quarter-to-quarter.

Global interest rate environment and debt servicing

Following elevated global policy rates into 2025, corporate debt servicing costs remain high; Indorama Ventures carried net debt of about US$4.6bn at end-2024, making interest expense sensitivity material for its capital-intensive PET, PTA and fertilizer projects.

Large-scale acquisitions and capex are typically debt-funded, so central bank rate cuts could lower annual interest outflows—Indorama reported ~US$220m finance costs in 2024—supporting cash flow recovery.

Management prioritizes refinancing high-cost tranches and extending maturities to protect investment-grade metrics; target leverage and interest-cover ratios guide balance-sheet optimization amid volatile rates.

Consumer demand cycles in the FMCG sector

Demand for Indorama Ventures PET resins tracks FMCG health, with beverages and food packaging representing roughly 40-50% of resin end‑use; global PET demand grew ~3.5% in 2024 driven by beverage consumption in Asia. Economic downturns and squeezed purchasing power can cut volumes—Asia Pacific GDP slowdown in 2023–24 trimmed packaged goods growth to ~1–2% in some markets, pressuring revenue. Conversely, emerging market expansion (India GDP ~7% in 2024, SE Asia ~4–5%) supports higher packaged goods consumption, benefiting packaging and fibers segments.

Currency exchange rate fluctuations

Operating in over 30 countries, Indorama consolidates results into Thai Baht, exposing it to FX risk; in FY2024 roughly 18% of revenue was USD-denominated, making USD/THB swings material.

Volatility in USD and EUR versus local currencies causes non-cash translation gains/losses—FY2023 reported a net FX translation loss of about $72 million.

The company uses forwards, swaps and localized production (over 60% of sales produced locally) as hedges to limit profit volatility.

- 30+ countries exposure

- ~18% revenue USD-denominated (FY2024)

- FY2023 FX translation loss ≈ $72M

- 60%+ sales produced locally; use of forwards/swaps

Logistics costs and supply chain efficiency

Global freight rates and container shortages—container index up ~45% in 2021 and still volatile into 2024—directly affect Indorama Ventures’ export costs and timing across its 35+ countries of operation.

Higher fuel prices (bunker fuel up ~20% yr/yr in 2024) and logistics labor constraints raise COGS and risk shipment delays that compress margins.

Indorama’s investments in supply-chain digitalization and regional sourcing reduce lead times and buffer against rate spikes, supporting resilience and cost control.

- Freight/container volatility increases distribution costs

- Fuel and labor pressures raise COGS, risk delays

- Digitalization and localized sourcing mitigate disruptions

Volatile 2024: PET margins, $4.6bn net debt and rising costs amid 3.5% demand growth

Economic factors: feedstock-PET margin sensitivity (2024 PX $800–$1,200/t, MEG $600–$900/t; PET realizations $1,200–$1,500/t) plus Brent ~$85/bbl in 2024 drove volatility; net debt ~US$4.6bn end-2024 with finance costs ~US$220m; PET demand +3.5% in 2024, India GDP ~7% (2024); ~18% revenue USD-denominated, FY2023 FX loss ~$72m; freight, bunker and labor inflation raised logistics costs.

| Metric | 2024 |

|---|---|

| PX | $800–$1,200/t |

| MEG | $600–$900/t |

| PET realizations | $1,200–$1,500/t |

| Brent | $85/bbl |

| Net debt | $4.6bn |

| Finance costs | $220m |

| PET demand growth | +3.5% |

| USD revenue | ~18% |

| FY2023 FX loss | $72m |

Same Document Delivered

Indorama Ventures PESTLE Analysis

The preview shown here is the exact Indorama Ventures PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and structure visible now match the final file available for immediate download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Indorama Ventures—unpack how politics, economics, social trends, technology, legal shifts, and environmental pressures will shape its growth and risks; buy the full report to get ready-to-use, expert insights and downloadable charts for investment or strategic planning.

Political factors

Trade protectionism and regional tariffs

The late-2025 trade landscape shows rising protectionism, with US and EU anti-dumping measures targeting Asian polyester/PET exporters—EU duties on certain PET imports reached up to 18.5% in 2024 while recent US investigations threaten similar levies. Indorama Ventures faces elevated compliance costs and margin pressure from tariffs and trade barriers that aim to shield domestic resin and fiber sectors. The company mitigates risk via a diversified manufacturing footprint—over 60 plants across 33 countries—shifting production into target markets to avoid import duties and preserve USD-denominated sales.

Geopolitical instability in energy-producing regions

Ongoing conflicts in Eastern Europe and the Middle East have driven Brent crude volatility, with 2024 average Brent at about $86/bbl and spot swings ±15% year-to-date, disrupting feedstock supply for Indorama Ventures’ PET and PTA chains; natural gas price spikes (EU TTF up ~40% vs 2023) raise production costs. Indorama uses strategic reserves and multiyear supply contracts—covering ~60–80% of feedstock needs in key plants—to stabilize operations and cash flow.

Government subsidies for green industrial transition

Regional political stability in Southeast Asia

As a Thailand-headquartered global chemicals leader, Indorama Ventures is exposed to ASEAN political shifts; Thailand's 2024 corporate tax rate remained at 20% for large firms while proposed incentives in 2025 target petrochemical clusters, potentially altering after-tax returns for local operations.

Government changes can reshape labor laws and export regulations affecting ~30% of IVL's 2024 Asia production capacity; active engagement with policymakers preserves incentives and supply-chain continuity.

- Headquarters exposure: Thailand policy affects corporate tax and incentives

- 2024 corporate tax baseline: 20% for major firms; 2025 incentive proposals for petrochemical hubs

- ~30% of IVL Asia production capacity sensitive to regional regulatory shifts

- Ongoing policymaker engagement essential to maintain stable operations

Global regulatory harmonization for plastics

International negotiations toward a global treaty on plastic pollution in 2025—backed by 175+ UN member states—are pushing for harmonized rules on production, waste management and circularity that will reshape petrochemical supply chains.

Indorama participates in industry forums and trade groups, aiming to influence standards so they remain technically feasible and economically viable amid projected regulatory compliance costs of up to $5–10 billion industry-wide by 2030.

- 175+ UN members engaged in treaty talks

- Global compliance cost estimate $5–10B by 2030

- Indorama active in industry forums to shape standards

- Focus areas: production limits, waste management, circularity

Protectionism, feedstock swings & plastics treaty reshape petrochem margins in 2024–25

Rising 2024–25 protectionism (EU PET duties up to 18.5%; US probes) and geopolitical-driven feedstock volatility (2024 Brent ~$86/bbl; EU TTF +40% vs 2023) elevate tariffs and input costs, while ~60 plants in 33 countries and multiyear contracts mitigate risk; green subsidies (~$150bn 2024–25) and Thailand’s 20% corporate tax plus 2025 petrochemical incentives improve CAPEX economics; 175+ states in 2025 plastics treaty raise compliance costs (industry $5–10B by 2030).

| Metric | Value |

|---|---|

| Brent 2024 avg | $86/bbl |

| EU PET duty (2024) | up to 18.5% |

| EU TTF change vs 2023 | +40% |

| Plants / Countries | ~60 / 33 |

| Green subsidies (2024–25) | ~$150bn |

| Thailand corp tax (2024) | 20% |

| UN treaty participants (2025) | 175+ |

| Industry compliance est. by 2030 | $5–10B |

What is included in the product

Explores how macro-environmental factors uniquely affect Indorama Ventures across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Indorama Ventures that relieves prep pain by providing an easily shareable, editable snapshot for meetings, presentations, and strategy sessions—ready to drop into decks or client reports and tailored with region- or business-line notes.

Economic factors

Volatility in feedstock and energy costs

Profitability at Indorama Ventures hinges on the spread between feedstocks such as paraxylene and MEG versus PET selling prices; in 2024 PET margins swung with paraxylene prices ranging $800–$1,200/ton and MEG $600–$900/ton versus average PET realizations near $1,200–$1,500/ton.

Global crude oil volatility—Brent averaged about $85/bbl in 2024—directly raised feedstock costs, forcing Indorama to use advanced hedging and feedstock integration to protect margins.

Shifts in chemical supply-demand, including 2024 Asian PX oversupply and regional MEG tightness, drove notable quarterly earnings volatility, with EBITDA margin fluctuations of several percentage points quarter-to-quarter.

Global interest rate environment and debt servicing

Following elevated global policy rates into 2025, corporate debt servicing costs remain high; Indorama Ventures carried net debt of about US$4.6bn at end-2024, making interest expense sensitivity material for its capital-intensive PET, PTA and fertilizer projects.

Large-scale acquisitions and capex are typically debt-funded, so central bank rate cuts could lower annual interest outflows—Indorama reported ~US$220m finance costs in 2024—supporting cash flow recovery.

Management prioritizes refinancing high-cost tranches and extending maturities to protect investment-grade metrics; target leverage and interest-cover ratios guide balance-sheet optimization amid volatile rates.

Consumer demand cycles in the FMCG sector

Demand for Indorama Ventures PET resins tracks FMCG health, with beverages and food packaging representing roughly 40-50% of resin end‑use; global PET demand grew ~3.5% in 2024 driven by beverage consumption in Asia. Economic downturns and squeezed purchasing power can cut volumes—Asia Pacific GDP slowdown in 2023–24 trimmed packaged goods growth to ~1–2% in some markets, pressuring revenue. Conversely, emerging market expansion (India GDP ~7% in 2024, SE Asia ~4–5%) supports higher packaged goods consumption, benefiting packaging and fibers segments.

Currency exchange rate fluctuations

Operating in over 30 countries, Indorama consolidates results into Thai Baht, exposing it to FX risk; in FY2024 roughly 18% of revenue was USD-denominated, making USD/THB swings material.

Volatility in USD and EUR versus local currencies causes non-cash translation gains/losses—FY2023 reported a net FX translation loss of about $72 million.

The company uses forwards, swaps and localized production (over 60% of sales produced locally) as hedges to limit profit volatility.

- 30+ countries exposure

- ~18% revenue USD-denominated (FY2024)

- FY2023 FX translation loss ≈ $72M

- 60%+ sales produced locally; use of forwards/swaps

Logistics costs and supply chain efficiency

Global freight rates and container shortages—container index up ~45% in 2021 and still volatile into 2024—directly affect Indorama Ventures’ export costs and timing across its 35+ countries of operation.

Higher fuel prices (bunker fuel up ~20% yr/yr in 2024) and logistics labor constraints raise COGS and risk shipment delays that compress margins.

Indorama’s investments in supply-chain digitalization and regional sourcing reduce lead times and buffer against rate spikes, supporting resilience and cost control.

- Freight/container volatility increases distribution costs

- Fuel and labor pressures raise COGS, risk delays

- Digitalization and localized sourcing mitigate disruptions

Volatile 2024: PET margins, $4.6bn net debt and rising costs amid 3.5% demand growth

Economic factors: feedstock-PET margin sensitivity (2024 PX $800–$1,200/t, MEG $600–$900/t; PET realizations $1,200–$1,500/t) plus Brent ~$85/bbl in 2024 drove volatility; net debt ~US$4.6bn end-2024 with finance costs ~US$220m; PET demand +3.5% in 2024, India GDP ~7% (2024); ~18% revenue USD-denominated, FY2023 FX loss ~$72m; freight, bunker and labor inflation raised logistics costs.

| Metric | 2024 |

|---|---|

| PX | $800–$1,200/t |

| MEG | $600–$900/t |

| PET realizations | $1,200–$1,500/t |

| Brent | $85/bbl |

| Net debt | $4.6bn |

| Finance costs | $220m |

| PET demand growth | +3.5% |

| USD revenue | ~18% |

| FY2023 FX loss | $72m |

Same Document Delivered

Indorama Ventures PESTLE Analysis

The preview shown here is the exact Indorama Ventures PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and structure visible now match the final file available for immediate download.