Indra Sistemas SA Porter's Five Forces Analysis

From Overview to Strategy Blueprint

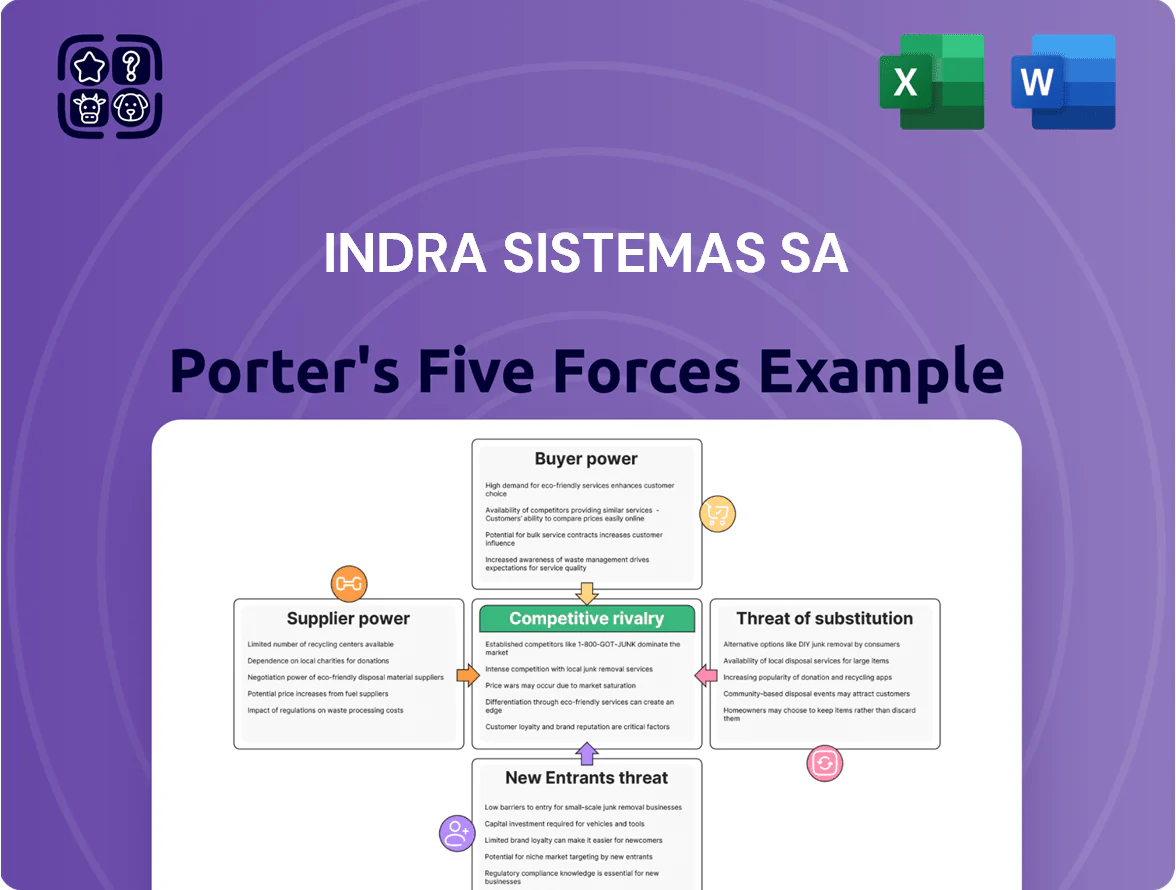

Indra Sistemas SA faces moderate rivalry driven by defense and transport contracts, while high buyer scrutiny and specialized supplier niches shape margins; digital transformation both raises barriers and invites niche entrants, and substitutes loom in software-as-a-service and global systems integrators. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Indra Sistemas SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Specialized Technical Talent

By end-2025 the global shortfall of senior software and cybersecurity experts—estimated at ~3.5 million high-tier roles—raises supplier power for labor, forcing Indra Sistemas SA to bid aggressively for talent.

Indra depends on specialized engineers to build defense and transport platforms, so talent scarcity pushes up labor costs and project timelines.

The firm now offers market-premium pay, equity and training; in 2024 R&D staffing costs rose ~12% year-over-year to retain staff against Big Tech poaching.

Dependence on Specialized Hardware Components

Indra depends on specialized semiconductors and advanced electronics for defense and ATM systems, sourcing from a few global suppliers that control ~60–70% of niche military-grade component capacity as of 2025; this concentration raises supplier bargaining power.

Software is in-house, but hardware dependency means supplier price hikes or supply shocks—like the 2021–23 chip disruptions that pushed aerospace component lead times to 24+ weeks—can cut Indra’s project margins and delay deliveries.

Strategic Partnerships with Technology Providers

Strategic partnerships with major cloud and software vendors give those suppliers strong leverage over Indra Sistemas SA; in 2024, global hyperscaler market share concentrated: AWS, Microsoft Azure, Google hold ~65% combined, affecting pricing and roadmaps.

As Indra shifts more workloads to hybrid cloud for defense and transport, dependency on provider SLAs and per-CPU/storage pricing rises; enterprise cloud spend for Indra-class firms often grows 12–18% annually.

Switching costs are very high: recertifying integrated defense systems can exceed tens of millions EUR and take 12–24 months, so suppliers retain bargaining power.

Geographic Concentration of Raw Materials

Advanced defense systems need rare earths and specialty alloys largely sourced from China, Russia, and Australia; by late 2025 rare earth prices rose ~22% YoY and spot premiums spiked amid export curbs, raising Indra Sistemas SA's input costs for radar and avionics modules.

Suppliers can use export bans or volume cuts to push prices; a 10–15% price shock to key materials could raise unit manufacturing costs for Indra's physical tech products by an estimated 3–6%.

- Rare earths concentrated: >70% processing in China (2025)

- Price change: +22% YoY (late 2025)

- Cost impact: +3–6% unit manufacturing costs

- Supplier leverage: export curbs, volume control

Intellectual Property and Licensing Costs

A portion of Indra Sistemas SA’s platforms rely on licensed patents from research institutes and niche tech firms; in 2024 Indra reported 18% of R&D-linked costs tied to external IP fees, constraining bargaining leverage.

These IP suppliers can push higher royalties or tighter usage limits at renewal; a 5–12% royalty hike would raise solution margins materially given Indra’s 2024 gross margin of ~21%.

Because these components are core to functionality, Indra has limited room to fight terms without risking product integrity, so it often accepts stricter clauses or pays premiums to secure continuity.

- 2024: ~18% of R&D costs from external IP

- Royalty sensitivity: 5–12% impact on margins

- Core tech = low negotiation leverage

Supply squeeze: talent, chips & rare earth concentration driving 3–6% unit cost shocks

Supplier power is high: talent shortfall (~3.5M senior roles by 2025) and concentrated suppliers for semiconductors, rare earths (>70% processing in China) and hyperscalers (AWS/Microsoft/Google ~65% share) push costs and timelines; 2024 R&D staffing +12% YoY, rare earths +22% YoY (late 2025), 10–15% material shocks could raise unit costs 3–6%.

| Metric | Value |

|---|---|

| Talent shortfall | ~3.5M (2025) |

| R&D staffing cost change | +12% YoY (2024) |

| Rare earth processing | >70% China (2025) |

| Rare earth price | +22% YoY (late 2025) |

| Hyperscaler share | ~65% (2024) |

| Unit cost shock | +3–6% (10–15% material shock) |

What is included in the product

Tailored Porter's Five Forces assessment of Indra Sistemas SA revealing competitive intensity, buyer and supplier bargaining power, threats from new entrants and substitutes, and strategic levers that protect or erode its market position.

Compact Porter's Five Forces for Indra Sistemas SA—one-sheet insight into competitive intensity, supplier/customer leverage, threat of substitutes/entrants and rivalry to speed strategic decisions.

Customers Bargaining Power

Dominance of Government Procurement

High Concentration of Major Clients

Indra Sistemas SA depends on multi-year contracts with few large clients in transport and energy; in 2024 roughly 45% of revenues came from top 10 clients, so a delayed project by a national airline or state rail operator can leave a multi-million-euro gap.

That client concentration gives those customers strong leverage to request bespoke features and extended support without extra fees; Indra reported a 2024 backlog of €3.2bn, yet renegotiations and scope changes raised margin pressure by ~150bps.

Stringent Performance and Security Standards

Availability of Detailed Market Information

Institutional buyers now use benchmarking platforms and consultants—Gartner, McKinsey, and bespoke TCO (total cost of ownership) models—to compare Indra Sistemas SA against peers, cutting information asymmetry and pressuring margins; public tender data show average bid-price declines of ~6–8% in European defense/transport IT contracts since 2020.

Clients negotiate from detailed delivery-cost lines and global project KPIs, forcing Indra to justify premium pricing with documented ROI and performance records; procurement cycles cite past-project on-time rates and unit costs as decisive factors.

- Benchmarking tools adoption up ~30% in public sector procurement since 2019

- Average bid-price compression ~6–8% in relevant tenders

- Clients demand KPI-backed SLAs and unit-cost transparency

Low Switching Costs for Consulting Services

While Indra Sistemas SA faces high switching costs for its integrated tech platforms, bargaining power is higher in its consulting and professional services where clients can shift to Accenture or Capgemini; consultancy revenue fell 2.1% YoY in 2024, raising pressure to retain margins.

Indra must show continuous value and innovation—clients cite price and delivery as top reasons for switching; win rates for repeat business dropped to 58% in 2024.

- Consulting seen as commoditized

- 2024 consultancy revenue −2.1% YoY

- Repeat win rate 58% in 2024

- Competitors: Accenture, Capgemini

Indra squeezed by public-sector monopsony: 62% buyers, €3.3bn revenue, margins cut

| Metric | Value |

|---|---|

| 2024 revenue | €3.3bn |

| Public-sector share | 62% |

| Top‑10 clients | 45% |

| Backlog | €3.2bn |

| Bid-price compression | 6–8% |

| Margin pressure | ~150bps |

| Penalty clauses | 10–20% contract value |

| Warranty/bond exposure rise | 15–25% (by 2025) |

| Consulting rev YoY | −2.1% (2024) |

| Repeat win rate | 58% (2024) |

Preview the Actual Deliverable

Indra Sistemas SA Porter's Five Forces Analysis

This preview shows the exact Indra Sistemas SA Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted version you’ll be able to download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use analysis file covering bargaining power of buyers and suppliers, competitive rivalry, threat of substitutes, and barriers to entry.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Indra Sistemas SA faces moderate rivalry driven by defense and transport contracts, while high buyer scrutiny and specialized supplier niches shape margins; digital transformation both raises barriers and invites niche entrants, and substitutes loom in software-as-a-service and global systems integrators. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Indra Sistemas SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Specialized Technical Talent

By end-2025 the global shortfall of senior software and cybersecurity experts—estimated at ~3.5 million high-tier roles—raises supplier power for labor, forcing Indra Sistemas SA to bid aggressively for talent.

Indra depends on specialized engineers to build defense and transport platforms, so talent scarcity pushes up labor costs and project timelines.

The firm now offers market-premium pay, equity and training; in 2024 R&D staffing costs rose ~12% year-over-year to retain staff against Big Tech poaching.

Dependence on Specialized Hardware Components

Indra depends on specialized semiconductors and advanced electronics for defense and ATM systems, sourcing from a few global suppliers that control ~60–70% of niche military-grade component capacity as of 2025; this concentration raises supplier bargaining power.

Software is in-house, but hardware dependency means supplier price hikes or supply shocks—like the 2021–23 chip disruptions that pushed aerospace component lead times to 24+ weeks—can cut Indra’s project margins and delay deliveries.

Strategic Partnerships with Technology Providers

Strategic partnerships with major cloud and software vendors give those suppliers strong leverage over Indra Sistemas SA; in 2024, global hyperscaler market share concentrated: AWS, Microsoft Azure, Google hold ~65% combined, affecting pricing and roadmaps.

As Indra shifts more workloads to hybrid cloud for defense and transport, dependency on provider SLAs and per-CPU/storage pricing rises; enterprise cloud spend for Indra-class firms often grows 12–18% annually.

Switching costs are very high: recertifying integrated defense systems can exceed tens of millions EUR and take 12–24 months, so suppliers retain bargaining power.

Geographic Concentration of Raw Materials

Advanced defense systems need rare earths and specialty alloys largely sourced from China, Russia, and Australia; by late 2025 rare earth prices rose ~22% YoY and spot premiums spiked amid export curbs, raising Indra Sistemas SA's input costs for radar and avionics modules.

Suppliers can use export bans or volume cuts to push prices; a 10–15% price shock to key materials could raise unit manufacturing costs for Indra's physical tech products by an estimated 3–6%.

- Rare earths concentrated: >70% processing in China (2025)

- Price change: +22% YoY (late 2025)

- Cost impact: +3–6% unit manufacturing costs

- Supplier leverage: export curbs, volume control

Intellectual Property and Licensing Costs

A portion of Indra Sistemas SA’s platforms rely on licensed patents from research institutes and niche tech firms; in 2024 Indra reported 18% of R&D-linked costs tied to external IP fees, constraining bargaining leverage.

These IP suppliers can push higher royalties or tighter usage limits at renewal; a 5–12% royalty hike would raise solution margins materially given Indra’s 2024 gross margin of ~21%.

Because these components are core to functionality, Indra has limited room to fight terms without risking product integrity, so it often accepts stricter clauses or pays premiums to secure continuity.

- 2024: ~18% of R&D costs from external IP

- Royalty sensitivity: 5–12% impact on margins

- Core tech = low negotiation leverage

Supply squeeze: talent, chips & rare earth concentration driving 3–6% unit cost shocks

Supplier power is high: talent shortfall (~3.5M senior roles by 2025) and concentrated suppliers for semiconductors, rare earths (>70% processing in China) and hyperscalers (AWS/Microsoft/Google ~65% share) push costs and timelines; 2024 R&D staffing +12% YoY, rare earths +22% YoY (late 2025), 10–15% material shocks could raise unit costs 3–6%.

| Metric | Value |

|---|---|

| Talent shortfall | ~3.5M (2025) |

| R&D staffing cost change | +12% YoY (2024) |

| Rare earth processing | >70% China (2025) |

| Rare earth price | +22% YoY (late 2025) |

| Hyperscaler share | ~65% (2024) |

| Unit cost shock | +3–6% (10–15% material shock) |

What is included in the product

Tailored Porter's Five Forces assessment of Indra Sistemas SA revealing competitive intensity, buyer and supplier bargaining power, threats from new entrants and substitutes, and strategic levers that protect or erode its market position.

Compact Porter's Five Forces for Indra Sistemas SA—one-sheet insight into competitive intensity, supplier/customer leverage, threat of substitutes/entrants and rivalry to speed strategic decisions.

Customers Bargaining Power

Dominance of Government Procurement

High Concentration of Major Clients

Indra Sistemas SA depends on multi-year contracts with few large clients in transport and energy; in 2024 roughly 45% of revenues came from top 10 clients, so a delayed project by a national airline or state rail operator can leave a multi-million-euro gap.

That client concentration gives those customers strong leverage to request bespoke features and extended support without extra fees; Indra reported a 2024 backlog of €3.2bn, yet renegotiations and scope changes raised margin pressure by ~150bps.

Stringent Performance and Security Standards

Availability of Detailed Market Information

Institutional buyers now use benchmarking platforms and consultants—Gartner, McKinsey, and bespoke TCO (total cost of ownership) models—to compare Indra Sistemas SA against peers, cutting information asymmetry and pressuring margins; public tender data show average bid-price declines of ~6–8% in European defense/transport IT contracts since 2020.

Clients negotiate from detailed delivery-cost lines and global project KPIs, forcing Indra to justify premium pricing with documented ROI and performance records; procurement cycles cite past-project on-time rates and unit costs as decisive factors.

- Benchmarking tools adoption up ~30% in public sector procurement since 2019

- Average bid-price compression ~6–8% in relevant tenders

- Clients demand KPI-backed SLAs and unit-cost transparency

Low Switching Costs for Consulting Services

While Indra Sistemas SA faces high switching costs for its integrated tech platforms, bargaining power is higher in its consulting and professional services where clients can shift to Accenture or Capgemini; consultancy revenue fell 2.1% YoY in 2024, raising pressure to retain margins.

Indra must show continuous value and innovation—clients cite price and delivery as top reasons for switching; win rates for repeat business dropped to 58% in 2024.

- Consulting seen as commoditized

- 2024 consultancy revenue −2.1% YoY

- Repeat win rate 58% in 2024

- Competitors: Accenture, Capgemini

Indra squeezed by public-sector monopsony: 62% buyers, €3.3bn revenue, margins cut

| Metric | Value |

|---|---|

| 2024 revenue | €3.3bn |

| Public-sector share | 62% |

| Top‑10 clients | 45% |

| Backlog | €3.2bn |

| Bid-price compression | 6–8% |

| Margin pressure | ~150bps |

| Penalty clauses | 10–20% contract value |

| Warranty/bond exposure rise | 15–25% (by 2025) |

| Consulting rev YoY | −2.1% (2024) |

| Repeat win rate | 58% (2024) |

Preview the Actual Deliverable

Indra Sistemas SA Porter's Five Forces Analysis

This preview shows the exact Indra Sistemas SA Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted version you’ll be able to download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use analysis file covering bargaining power of buyers and suppliers, competitive rivalry, threat of substitutes, and barriers to entry.