Infotel Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

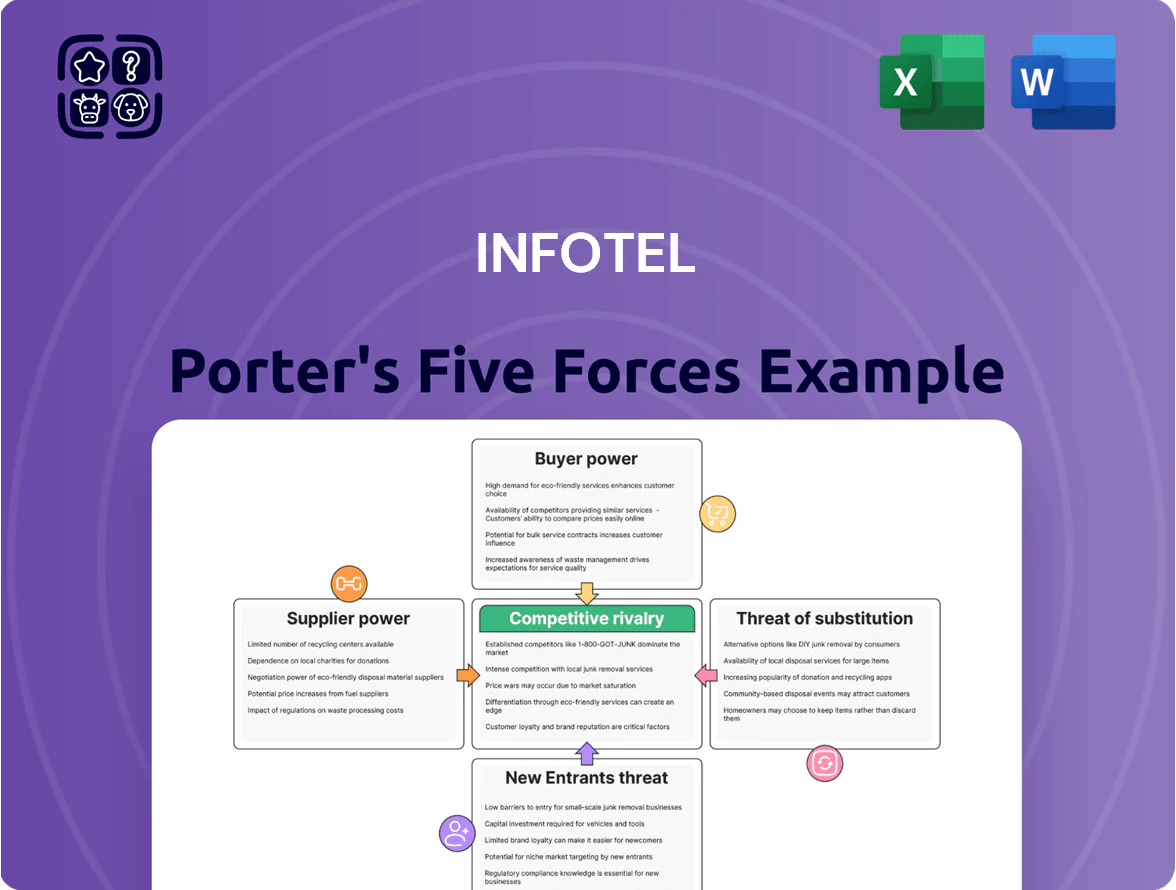

Infotel’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of substitutes, and barriers to entry—showing where strategic risks and opportunities lie for the company.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Infotel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

High demand for specialized IT talent

As of late 2025, a shortage of AI, cloud, and cybersecurity engineers—estimated at a 22% gap in EU tech roles per Eurostat 2024 data—gives suppliers high leverage; Infotel must outbid global giants like Google and AWS and local players such as SAP to secure talent.

High demand lifts wages: median senior cloud engineer pay in Europe rose to €95,000 in 2025 (LinkedIn Salary), pressuring Infotel’s margins unless it offers hybrid work, equity, or training pathways.

Dependence on major cloud infrastructure providers

Infotel depends on hyperscalers—AWS, Microsoft Azure, Google Cloud—for core hosting and delivery of digital transformation services, creating supplier concentration risk. These providers set standardized pricing and promote ecosystem lock-in, limiting Infotel’s leverage to negotiate discounts; global cloud IaaS/PaaS spend hit about $322 billion in 2024, concentrating bargaining power. Any cloud price increases feed directly into Infotel’s cost base and compress gross margins; a 5% average price rise could cut service margins by ~2–3 points.

Software vendor partnership requirements

Infotel’s ability to sell integrated solutions hinges on certified partnerships with enterprise vendors like SAP and Microsoft, who set certification criteria, training fees (often >€2,000 per engineer) and resale margins that shape Infotel’s pricing and margins.

Vendors can force certification cycles and co-selling rules, compressing Infotel’s gross margin by 3–7 percentage points; losing a major partner could cut addressable large-account revenue by an estimated 25–40% based on 2024 client mixes.

Concentration of specialized hardware suppliers

- Few dominant vendors: Cisco, Dell EMC, HPE

- 2025 lead times ~30% shorter vs 2021

- Certified banking-grade premium ~10–15%

Rising costs of proprietary third-party data

Infotel’s software ties in niche third-party financial and regulatory feeds—vendors that in 2025 captured ~60–80% share in specific data segments—letting them raise subscription rates by 5–12% annually without meaningful competition.

Because losing a feed would degrade bank clients’ compliance and pricing modules, Infotel has limited leverage to contest fee hikes, squeezing gross margins by an estimated 120–250 basis points in 2024–25.

- High vendor concentration: 60–80% market share in niches

- Typical annual fee inflation: 5–12%

- Estimated margin hit: 120–250 bps (2024–25)

Supplier power squeezes EU tech margins: talent gaps, hyperscaler dominance, rising fees

Suppliers hold strong leverage: 2024–25 EU tech talent gap ~22% (Eurostat 2024), median senior cloud pay €95,000 (2025 LinkedIn), hyperscalers (AWS/Azure/GCP) drove $322B IaaS/PaaS spend (2024) and limit discounts, SAP/Microsoft certification fees >€2,000 compress margins, niche data feeds control 60–80% share and raised fees 5–12% (2024–25), hardware premiums 10–15%.

| Metric | Value |

|---|---|

| EU tech gap | 22% |

| Senior cloud pay | €95,000 |

| IaaS/PaaS spend | $322B (2024) |

| Data-feed share | 60–80% |

What is included in the product

Tailored Porter's Five Forces analysis for Infotel that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and highlights disruptive trends affecting market share and profitability; fully editable for integration into reports and investor materials.

Instantly visualize competitive pressures with a concise Porter's Five Forces one-sheet—perfect for quick strategy sessions and slide-ready presentations.

Customers Bargaining Power

High concentration of revenue in large accounts

Formalized and rigorous procurement processes

Large accounts use formal procurement teams that commoditize IT services, squeezing Infotel’s margins; 68% of enterprise buyers used formal RFPs in 2024, per ProcureTech Research. Clients favor multi-vendor setups—often 3+ suppliers—to avoid dependence, keeping price pressure high. Public and private tenders increase transparency: 2024 EU IT tenders showed average bid discounts of 12% versus list prices.

Low switching costs for standardized IT services

While Infotel’s proprietary software creates some client stickiness, standard IT consulting and application maintenance have low switching costs; 62% of enterprise IT projects in 2024 switched vendors within 24 months, per Everest Group, so clients can move to rivals or offshore firms if unhappy with pricing or delivery. This mobility forces Infotel to show measurable ROI and value-add beyond technical execution—client retention tied to value propositions rather than contracts.

Increasing technical sophistication of internal IT departments

By late 2025 many of Infotel’s clients had built internal digital centers of excellence, letting them insource projects when consultancy fees exceed perceived value, reducing spend on generalist vendors by an estimated 15–25% per client annually.

As clients handle core digital work internally, they outsource only niche or high-risk tasks, raising customer selectivity and forcing Infotel to compete on specialized skills, IP, or outcome-based pricing.

- 15–25% reduced outsourcing on core projects

- Outsourcing shifts to niche/high-risk work

- Pressure on fees, push toward outcome pricing

Economic sensitivity of discretionary IT spending

During economic downturns banks and insurers often delay discretionary IT projects; 2023–2024 data showed financial services cut tech discretionary spend by ~8–12% year-over-year, letting clients pause contracts or seek renegotiation to protect capital.

That macro sensitivity forces Infotel to offer flexible payment terms, phased delivery, or reduced rates to retain relationships; a single large client pause can reduce annual revenue by mid-single digits.

Infotel faces margin squeeze as top clients, RFPs and insourcing drive fierce price pressure

Infotel’s largest five clients drive ~38% of 2024 revenue (EUR 210m), giving strong bargaining power and frequent demands for discounts and strict SLAs that squeeze margins.

Formal procurement and multi-vendor sourcing (68% RFP use in 2024) plus low switching costs (62% vendor churn within 24 months) keep price pressure high.

Insourcing trends cut client outsourcing by 15–25% and shift spend to niche/high-risk work, forcing outcome-based pricing and flexible terms.

| Metric | Value |

|---|---|

| 2024 Revenue | EUR 210m |

| Top 5 clients | ~38% |

| RFP use (2024) | 68% |

| Vendor churn (24m) | 62% |

| Insourcing impact | 15–25% cut |

Full Version Awaits

Infotel Porter's Five Forces Analysis

This preview shows the exact Infotel Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready to use.

You're viewing the final document: the same professionally written file available for instant download upon payment, suitable for presentations, reports, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Infotel’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of substitutes, and barriers to entry—showing where strategic risks and opportunities lie for the company.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Infotel’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

High demand for specialized IT talent

As of late 2025, a shortage of AI, cloud, and cybersecurity engineers—estimated at a 22% gap in EU tech roles per Eurostat 2024 data—gives suppliers high leverage; Infotel must outbid global giants like Google and AWS and local players such as SAP to secure talent.

High demand lifts wages: median senior cloud engineer pay in Europe rose to €95,000 in 2025 (LinkedIn Salary), pressuring Infotel’s margins unless it offers hybrid work, equity, or training pathways.

Dependence on major cloud infrastructure providers

Infotel depends on hyperscalers—AWS, Microsoft Azure, Google Cloud—for core hosting and delivery of digital transformation services, creating supplier concentration risk. These providers set standardized pricing and promote ecosystem lock-in, limiting Infotel’s leverage to negotiate discounts; global cloud IaaS/PaaS spend hit about $322 billion in 2024, concentrating bargaining power. Any cloud price increases feed directly into Infotel’s cost base and compress gross margins; a 5% average price rise could cut service margins by ~2–3 points.

Software vendor partnership requirements

Infotel’s ability to sell integrated solutions hinges on certified partnerships with enterprise vendors like SAP and Microsoft, who set certification criteria, training fees (often >€2,000 per engineer) and resale margins that shape Infotel’s pricing and margins.

Vendors can force certification cycles and co-selling rules, compressing Infotel’s gross margin by 3–7 percentage points; losing a major partner could cut addressable large-account revenue by an estimated 25–40% based on 2024 client mixes.

Concentration of specialized hardware suppliers

- Few dominant vendors: Cisco, Dell EMC, HPE

- 2025 lead times ~30% shorter vs 2021

- Certified banking-grade premium ~10–15%

Rising costs of proprietary third-party data

Infotel’s software ties in niche third-party financial and regulatory feeds—vendors that in 2025 captured ~60–80% share in specific data segments—letting them raise subscription rates by 5–12% annually without meaningful competition.

Because losing a feed would degrade bank clients’ compliance and pricing modules, Infotel has limited leverage to contest fee hikes, squeezing gross margins by an estimated 120–250 basis points in 2024–25.

- High vendor concentration: 60–80% market share in niches

- Typical annual fee inflation: 5–12%

- Estimated margin hit: 120–250 bps (2024–25)

Supplier power squeezes EU tech margins: talent gaps, hyperscaler dominance, rising fees

Suppliers hold strong leverage: 2024–25 EU tech talent gap ~22% (Eurostat 2024), median senior cloud pay €95,000 (2025 LinkedIn), hyperscalers (AWS/Azure/GCP) drove $322B IaaS/PaaS spend (2024) and limit discounts, SAP/Microsoft certification fees >€2,000 compress margins, niche data feeds control 60–80% share and raised fees 5–12% (2024–25), hardware premiums 10–15%.

| Metric | Value |

|---|---|

| EU tech gap | 22% |

| Senior cloud pay | €95,000 |

| IaaS/PaaS spend | $322B (2024) |

| Data-feed share | 60–80% |

What is included in the product

Tailored Porter's Five Forces analysis for Infotel that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and highlights disruptive trends affecting market share and profitability; fully editable for integration into reports and investor materials.

Instantly visualize competitive pressures with a concise Porter's Five Forces one-sheet—perfect for quick strategy sessions and slide-ready presentations.

Customers Bargaining Power

High concentration of revenue in large accounts

Formalized and rigorous procurement processes

Large accounts use formal procurement teams that commoditize IT services, squeezing Infotel’s margins; 68% of enterprise buyers used formal RFPs in 2024, per ProcureTech Research. Clients favor multi-vendor setups—often 3+ suppliers—to avoid dependence, keeping price pressure high. Public and private tenders increase transparency: 2024 EU IT tenders showed average bid discounts of 12% versus list prices.

Low switching costs for standardized IT services

While Infotel’s proprietary software creates some client stickiness, standard IT consulting and application maintenance have low switching costs; 62% of enterprise IT projects in 2024 switched vendors within 24 months, per Everest Group, so clients can move to rivals or offshore firms if unhappy with pricing or delivery. This mobility forces Infotel to show measurable ROI and value-add beyond technical execution—client retention tied to value propositions rather than contracts.

Increasing technical sophistication of internal IT departments

By late 2025 many of Infotel’s clients had built internal digital centers of excellence, letting them insource projects when consultancy fees exceed perceived value, reducing spend on generalist vendors by an estimated 15–25% per client annually.

As clients handle core digital work internally, they outsource only niche or high-risk tasks, raising customer selectivity and forcing Infotel to compete on specialized skills, IP, or outcome-based pricing.

- 15–25% reduced outsourcing on core projects

- Outsourcing shifts to niche/high-risk work

- Pressure on fees, push toward outcome pricing

Economic sensitivity of discretionary IT spending

During economic downturns banks and insurers often delay discretionary IT projects; 2023–2024 data showed financial services cut tech discretionary spend by ~8–12% year-over-year, letting clients pause contracts or seek renegotiation to protect capital.

That macro sensitivity forces Infotel to offer flexible payment terms, phased delivery, or reduced rates to retain relationships; a single large client pause can reduce annual revenue by mid-single digits.

Infotel faces margin squeeze as top clients, RFPs and insourcing drive fierce price pressure

Infotel’s largest five clients drive ~38% of 2024 revenue (EUR 210m), giving strong bargaining power and frequent demands for discounts and strict SLAs that squeeze margins.

Formal procurement and multi-vendor sourcing (68% RFP use in 2024) plus low switching costs (62% vendor churn within 24 months) keep price pressure high.

Insourcing trends cut client outsourcing by 15–25% and shift spend to niche/high-risk work, forcing outcome-based pricing and flexible terms.

| Metric | Value |

|---|---|

| 2024 Revenue | EUR 210m |

| Top 5 clients | ~38% |

| RFP use (2024) | 68% |

| Vendor churn (24m) | 62% |

| Insourcing impact | 15–25% cut |

Full Version Awaits

Infotel Porter's Five Forces Analysis

This preview shows the exact Infotel Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready to use.

You're viewing the final document: the same professionally written file available for instant download upon payment, suitable for presentations, reports, or strategic planning.