Infotel PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic trends, and rapid tech change are shaping Infotel’s prospects with our concise PESTLE snapshot—designed to inform investors and strategists quickly. Dive deeper with the full PESTLE Analysis for actionable risks, opportunities, and ready-to-use slides and tables. Purchase the complete report now to get the detailed intelligence you need.

Political factors

EU Digital Sovereignty Initiatives

The EU’s digital sovereignty push—backed by a 2023 EU budget increase to 32 billion euros for digital transformation and the 2024 EU Cybersecurity Strategy—reduces reliance on non-European vendors; Infotel, as a French IT supplier with 2024 revenue ~€220m, is well positioned to capture contracts in banking and defense requiring localized, secure services. Recent French government mandates favoring European software create a steady pipeline for Infotel’s software publishing division, supporting recurring revenue and margin stability.

Geopolitical Stability and Global Delivery

Ongoing tensions in Eastern Europe and parts of Asia have shifted 28% of European IT deliveries toward nearshore hubs since 2022, forcing Infotel to re-evaluate offshore exposures to protect €340m+ in managed-account revenues.

Infotel must locate service centers in politically stable jurisdictions to ensure SLA compliance and business continuity for major clients, reducing geopolitical disruption risk by an estimated 12–18% in operating volatility.

Political stability in France and key EU markets underpins capital allocation: Infotel’s 2024–25 infrastructure investments prioritize EU sites, aligning with projected 10% CAGR in continental demand.

Public Sector Digital Transformation Budgets

National governments are directing large budget shares to public sector digitalization—OECD reports 2024 public IT spending rose ~6% to over $450bn globally—boosting modernization of administration and healthcare; Infotel’s large-scale system integration expertise positions it to win insulated public tenders that reduce exposure to private-market cycles; sustained political commitment to e-government and health IT creates predictable demand for consulting and application maintenance services.

Tax Policies and Research Incentives

The French Research Tax Credit (CIR) and related innovation incentives, representing roughly 0.4% of GDP and offering refundable credits up to 30% of eligible R&D spending, underpin Infotel’s software publishing R&D investments; in 2024 CIR claims totaled about €6.5bn nationally, directly lowering Infotel’s net innovation costs.

A political shift toward austerity cutting these subsidies would raise Infotel’s effective R&D expense, compressing margins—France’s tech sector relies on CIR for an estimated 25–30% of R&D financing—and could hamstring scaling versus global competitors.

Maintaining a favorable tax environment for high-tech firms is vital for Infotel to stay competitive against multinationals that leverage R&D credits and lower tax jurisdictions; preserving CIR levels supports talent retention and long-term product investment.

- 2024 CIR total: ~€6.5bn

- Typical credit rate: up to 30% of R&D

- Sector reliance: ~25–30% of R&D funding

Data Governance and Cross-Border Regulations

Political mandates on data localization and EU-US/UK adequacy decisions shape Infotel’s cloud architecture and edge deployments; over 60% of EU financial data processing now requires local residency, raising hosting costs ~8–12%.

Serving banks and insurers, Infotel must mirror national privacy stances like GDPR and Brazil’s LGPD to keep client SLAs intact and avoid fines that can reach 4% of global turnover.

Diplomatic tensions can abruptly impose export controls or certification barriers, complicating cross-border licensing and potentially delaying deployments by months.

- Data residency mandates >60% in EU financial workloads

- Compliance fines up to 4% of global revenue (GDPR)

- Hosting cost uplift ~8–12% for localized infrastructure

- Cross-border licensing delays: potential multi-month impact

Infotel benefits from €32bn EU digital push but faces 8–12% local hosting cost rise

EU digital sovereignty funding (€32bn 2023), France CIR €6.5bn (2024) and +6% global public IT spend (~$450bn) boost Infotel’s EU-focused revenue (~€220m 2024) and R&D; data residency (>60% EU financial workloads) and GDPR fines (up to 4% turnover) raise localized hosting costs ~8–12% and operational compliance risks.

| Metric | Value |

|---|---|

| Infotel revenue 2024 | ~€220m |

| EU digital fund | €32bn (2023) |

| France CIR 2024 | €6.5bn |

| Public IT spend 2024 | ~$450bn (+6%) |

| Data residency | >60% EU financial |

| Hosting cost uplift | 8–12% |

What is included in the product

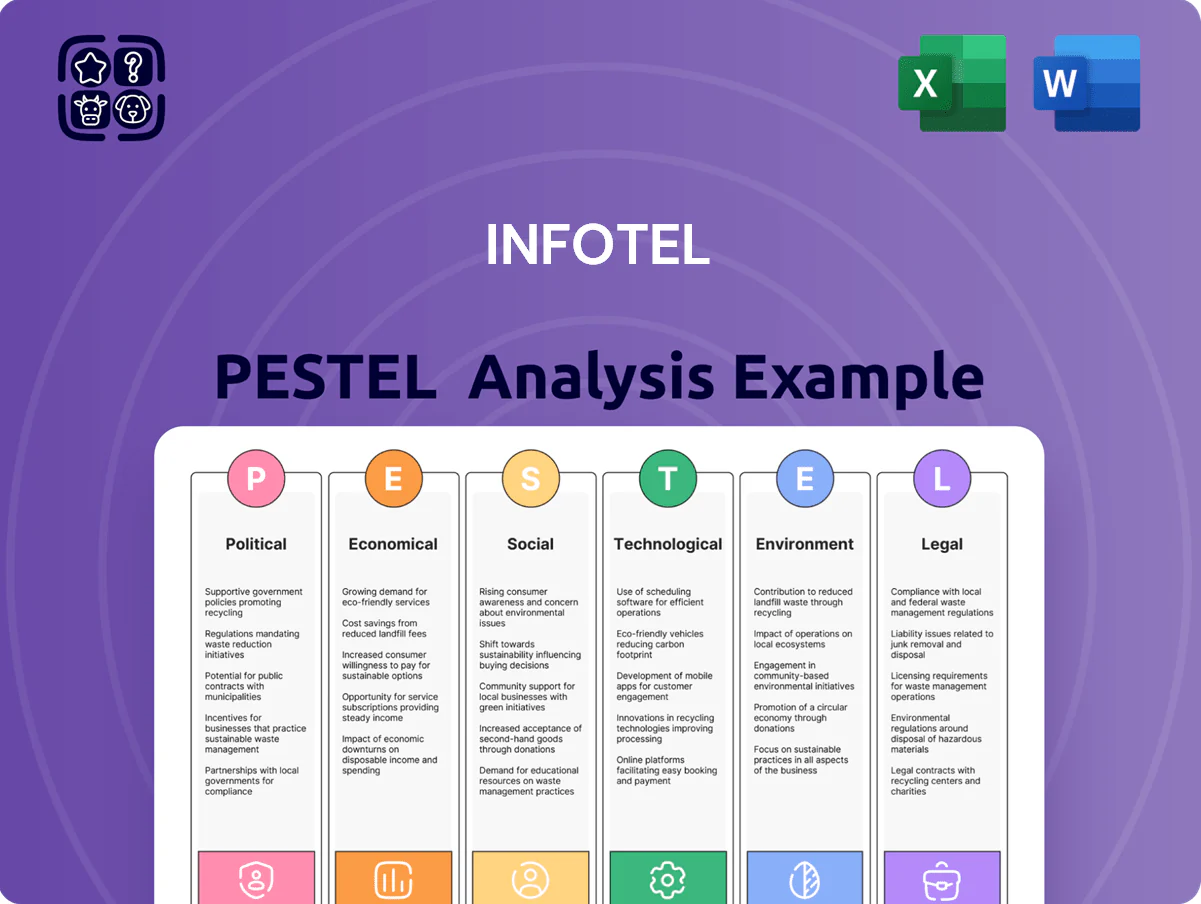

Explores how external macro-environmental factors uniquely affect Infotel across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities.

Provides a clean, visually segmented PESTLE summary that’s easy to drop into presentations or share across teams, with editable notes for regional or business-line context to streamline planning and risk discussions.

Economic factors

IT Spending Trends in Financial Services

Banking and insurance account for roughly 55% of Infotel’s revenue, making the firm highly sensitive to sector IT budget cycles; Gartner reported banks cut discretionary IT spend by 4% in 2024. By end-2025, 62% of financial institutions plan cost-optimization via automation, sustaining demand for Infotel’s workflow and RPA offerings. However, a sectoral downturn could delay large-scale digital transformations, with 38% of projects deferred in 2023–24 during stress periods.

Wage Inflation in the Technology Sector

Wage inflation in tech remains acute: specialized developer salaries rose about 8–12% in 2023–24 globally, with US median software engineer pay up ~10% year-over-year to about $140k in 2024; Indian IT specialist wages climbed ~9% in 2024, pressuring margins for Infotel’s offshore/onshore mix.

Infotel must raise pay to retain talent while managing service-contract margins—if wage inflation exceeds client rate adjustments (client daily-rate growth ~3–5% in 2024), profitability risks downward pressure.

Interest Rate Impacts on Corporate Investment

At end-2025, global policy rates averaged about 4.8%, with US Fed funds around 5.25% and ECB depo ~3.5%, directly shaping Infotel clients’ CAPEX; lower-rate sectors increased tech spend by ~12% YoY, while high-rate industries cut discretionary IT spend by ~6%.

Lower rates incentivize aggressive investment in cloud, AI and SaaS stacks, boosting demand for Infotel’s digital services; higher rates push clients toward cost-focused maintenance of legacy mainframes.

Infotel’s dual capabilities in mainframe modernization and modern digital tooling position it to capture spend shifting between upgrades and new implementations across interest-rate cycles.

Currency Volatility in Global Operations

While Infotel focuses on Europe, 2024 saw EUR/USD volatility with a range ~1.05–1.12, exposing international software sales and offshore delivery centers to exchange risk that can compress margins or raise local labor costs.

Movements in the euro versus delivery-hub currencies (e.g., INR, PHP) can alter price competitiveness; in 2024 INR appreciated ~3% vs EUR, increasing offshore cost pressure.

Effective hedging (forwards, options) and local-currency billing are essential; companies using such measures reported up to 1–2% EBITDA volatility reduction in 2023–2024.

- EUR/USD 2024 range ~1.05–1.12

- INR ≈+3% vs EUR in 2024

- Hedging can cut EBITDA volatility ~1–2%

- Local-currency billing preserves pricing competitiveness

Economic Resilience of the Banking Sector

The health of Europe’s banking sector—assets worth roughly €41 trillion in 2024—directly affects Infotel’s contract pipeline, with banks cutting costs but prioritizing core IT spend.

Facing margin pressure (EU bank RoE ~6.5% in 2024), lenders outsource back-office functions, increasing demand for Infotel’s services.

Deep integration with clients’ core systems creates a defensive revenue stream during economic stagnation, supporting recurring maintenance income.

- €41 trillion European banking assets (2024)

- EU bank RoE ~6.5% (2024)

- Higher outsourcing of back-office to preserve margins

Infotel faces margin squeeze as bank cuts, wage inflation and FX headwinds bite

Infotel’s revenue tied to banking/insurance (~55%) makes it sensitive to discretionary IT cuts; banks cut IT spend ~4% in 2024 while 62% plan automation-led cost optimization by end-2025. Wage inflation (dev pay +8–12% in 2023–24; India +9% in 2024) pressures margins versus client rate growth ~3–5%. EUR/USD 2024 ~1.05–1.12; INR +3% vs EUR raises offshore costs; hedging cuts EBITDA volatility ~1–2%.

| Metric | 2024–25 |

|---|---|

| Banking share of revenue | ~55% |

| Bank IT spend change (2024) | -4% |

| Automation adoption target | 62% by end‑2025 |

| Dev wage inflation | +8–12% |

| INR vs EUR (2024) | +3% |

| EUR/USD range (2024) | 1.05–1.12 |

| Hedging EBITDA benefit | ~1–2% vol reduction |

Same Document Delivered

Infotel PESTLE Analysis

The preview shown here is the exact Infotel PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without any placeholders or edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic trends, and rapid tech change are shaping Infotel’s prospects with our concise PESTLE snapshot—designed to inform investors and strategists quickly. Dive deeper with the full PESTLE Analysis for actionable risks, opportunities, and ready-to-use slides and tables. Purchase the complete report now to get the detailed intelligence you need.

Political factors

EU Digital Sovereignty Initiatives

The EU’s digital sovereignty push—backed by a 2023 EU budget increase to 32 billion euros for digital transformation and the 2024 EU Cybersecurity Strategy—reduces reliance on non-European vendors; Infotel, as a French IT supplier with 2024 revenue ~€220m, is well positioned to capture contracts in banking and defense requiring localized, secure services. Recent French government mandates favoring European software create a steady pipeline for Infotel’s software publishing division, supporting recurring revenue and margin stability.

Geopolitical Stability and Global Delivery

Ongoing tensions in Eastern Europe and parts of Asia have shifted 28% of European IT deliveries toward nearshore hubs since 2022, forcing Infotel to re-evaluate offshore exposures to protect €340m+ in managed-account revenues.

Infotel must locate service centers in politically stable jurisdictions to ensure SLA compliance and business continuity for major clients, reducing geopolitical disruption risk by an estimated 12–18% in operating volatility.

Political stability in France and key EU markets underpins capital allocation: Infotel’s 2024–25 infrastructure investments prioritize EU sites, aligning with projected 10% CAGR in continental demand.

Public Sector Digital Transformation Budgets

National governments are directing large budget shares to public sector digitalization—OECD reports 2024 public IT spending rose ~6% to over $450bn globally—boosting modernization of administration and healthcare; Infotel’s large-scale system integration expertise positions it to win insulated public tenders that reduce exposure to private-market cycles; sustained political commitment to e-government and health IT creates predictable demand for consulting and application maintenance services.

Tax Policies and Research Incentives

The French Research Tax Credit (CIR) and related innovation incentives, representing roughly 0.4% of GDP and offering refundable credits up to 30% of eligible R&D spending, underpin Infotel’s software publishing R&D investments; in 2024 CIR claims totaled about €6.5bn nationally, directly lowering Infotel’s net innovation costs.

A political shift toward austerity cutting these subsidies would raise Infotel’s effective R&D expense, compressing margins—France’s tech sector relies on CIR for an estimated 25–30% of R&D financing—and could hamstring scaling versus global competitors.

Maintaining a favorable tax environment for high-tech firms is vital for Infotel to stay competitive against multinationals that leverage R&D credits and lower tax jurisdictions; preserving CIR levels supports talent retention and long-term product investment.

- 2024 CIR total: ~€6.5bn

- Typical credit rate: up to 30% of R&D

- Sector reliance: ~25–30% of R&D funding

Data Governance and Cross-Border Regulations

Political mandates on data localization and EU-US/UK adequacy decisions shape Infotel’s cloud architecture and edge deployments; over 60% of EU financial data processing now requires local residency, raising hosting costs ~8–12%.

Serving banks and insurers, Infotel must mirror national privacy stances like GDPR and Brazil’s LGPD to keep client SLAs intact and avoid fines that can reach 4% of global turnover.

Diplomatic tensions can abruptly impose export controls or certification barriers, complicating cross-border licensing and potentially delaying deployments by months.

- Data residency mandates >60% in EU financial workloads

- Compliance fines up to 4% of global revenue (GDPR)

- Hosting cost uplift ~8–12% for localized infrastructure

- Cross-border licensing delays: potential multi-month impact

Infotel benefits from €32bn EU digital push but faces 8–12% local hosting cost rise

EU digital sovereignty funding (€32bn 2023), France CIR €6.5bn (2024) and +6% global public IT spend (~$450bn) boost Infotel’s EU-focused revenue (~€220m 2024) and R&D; data residency (>60% EU financial workloads) and GDPR fines (up to 4% turnover) raise localized hosting costs ~8–12% and operational compliance risks.

| Metric | Value |

|---|---|

| Infotel revenue 2024 | ~€220m |

| EU digital fund | €32bn (2023) |

| France CIR 2024 | €6.5bn |

| Public IT spend 2024 | ~$450bn (+6%) |

| Data residency | >60% EU financial |

| Hosting cost uplift | 8–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Infotel across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities.

Provides a clean, visually segmented PESTLE summary that’s easy to drop into presentations or share across teams, with editable notes for regional or business-line context to streamline planning and risk discussions.

Economic factors

IT Spending Trends in Financial Services

Banking and insurance account for roughly 55% of Infotel’s revenue, making the firm highly sensitive to sector IT budget cycles; Gartner reported banks cut discretionary IT spend by 4% in 2024. By end-2025, 62% of financial institutions plan cost-optimization via automation, sustaining demand for Infotel’s workflow and RPA offerings. However, a sectoral downturn could delay large-scale digital transformations, with 38% of projects deferred in 2023–24 during stress periods.

Wage Inflation in the Technology Sector

Wage inflation in tech remains acute: specialized developer salaries rose about 8–12% in 2023–24 globally, with US median software engineer pay up ~10% year-over-year to about $140k in 2024; Indian IT specialist wages climbed ~9% in 2024, pressuring margins for Infotel’s offshore/onshore mix.

Infotel must raise pay to retain talent while managing service-contract margins—if wage inflation exceeds client rate adjustments (client daily-rate growth ~3–5% in 2024), profitability risks downward pressure.

Interest Rate Impacts on Corporate Investment

At end-2025, global policy rates averaged about 4.8%, with US Fed funds around 5.25% and ECB depo ~3.5%, directly shaping Infotel clients’ CAPEX; lower-rate sectors increased tech spend by ~12% YoY, while high-rate industries cut discretionary IT spend by ~6%.

Lower rates incentivize aggressive investment in cloud, AI and SaaS stacks, boosting demand for Infotel’s digital services; higher rates push clients toward cost-focused maintenance of legacy mainframes.

Infotel’s dual capabilities in mainframe modernization and modern digital tooling position it to capture spend shifting between upgrades and new implementations across interest-rate cycles.

Currency Volatility in Global Operations

While Infotel focuses on Europe, 2024 saw EUR/USD volatility with a range ~1.05–1.12, exposing international software sales and offshore delivery centers to exchange risk that can compress margins or raise local labor costs.

Movements in the euro versus delivery-hub currencies (e.g., INR, PHP) can alter price competitiveness; in 2024 INR appreciated ~3% vs EUR, increasing offshore cost pressure.

Effective hedging (forwards, options) and local-currency billing are essential; companies using such measures reported up to 1–2% EBITDA volatility reduction in 2023–2024.

- EUR/USD 2024 range ~1.05–1.12

- INR ≈+3% vs EUR in 2024

- Hedging can cut EBITDA volatility ~1–2%

- Local-currency billing preserves pricing competitiveness

Economic Resilience of the Banking Sector

The health of Europe’s banking sector—assets worth roughly €41 trillion in 2024—directly affects Infotel’s contract pipeline, with banks cutting costs but prioritizing core IT spend.

Facing margin pressure (EU bank RoE ~6.5% in 2024), lenders outsource back-office functions, increasing demand for Infotel’s services.

Deep integration with clients’ core systems creates a defensive revenue stream during economic stagnation, supporting recurring maintenance income.

- €41 trillion European banking assets (2024)

- EU bank RoE ~6.5% (2024)

- Higher outsourcing of back-office to preserve margins

Infotel faces margin squeeze as bank cuts, wage inflation and FX headwinds bite

Infotel’s revenue tied to banking/insurance (~55%) makes it sensitive to discretionary IT cuts; banks cut IT spend ~4% in 2024 while 62% plan automation-led cost optimization by end-2025. Wage inflation (dev pay +8–12% in 2023–24; India +9% in 2024) pressures margins versus client rate growth ~3–5%. EUR/USD 2024 ~1.05–1.12; INR +3% vs EUR raises offshore costs; hedging cuts EBITDA volatility ~1–2%.

| Metric | 2024–25 |

|---|---|

| Banking share of revenue | ~55% |

| Bank IT spend change (2024) | -4% |

| Automation adoption target | 62% by end‑2025 |

| Dev wage inflation | +8–12% |

| INR vs EUR (2024) | +3% |

| EUR/USD range (2024) | 1.05–1.12 |

| Hedging EBITDA benefit | ~1–2% vol reduction |

Same Document Delivered

Infotel PESTLE Analysis

The preview shown here is the exact Infotel PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without any placeholders or edits.