Infotel SWOT Analysis

Your Strategic Toolkit Starts Here

Infotel’s SWOT snapshot highlights robust niche expertise and recurring revenue but also warns of scaling and regulatory risks; for a full, research-backed breakdown with strategic recommendations and editable Word/Excel deliverables, purchase the complete SWOT analysis to confidently plan, pitch, or invest.

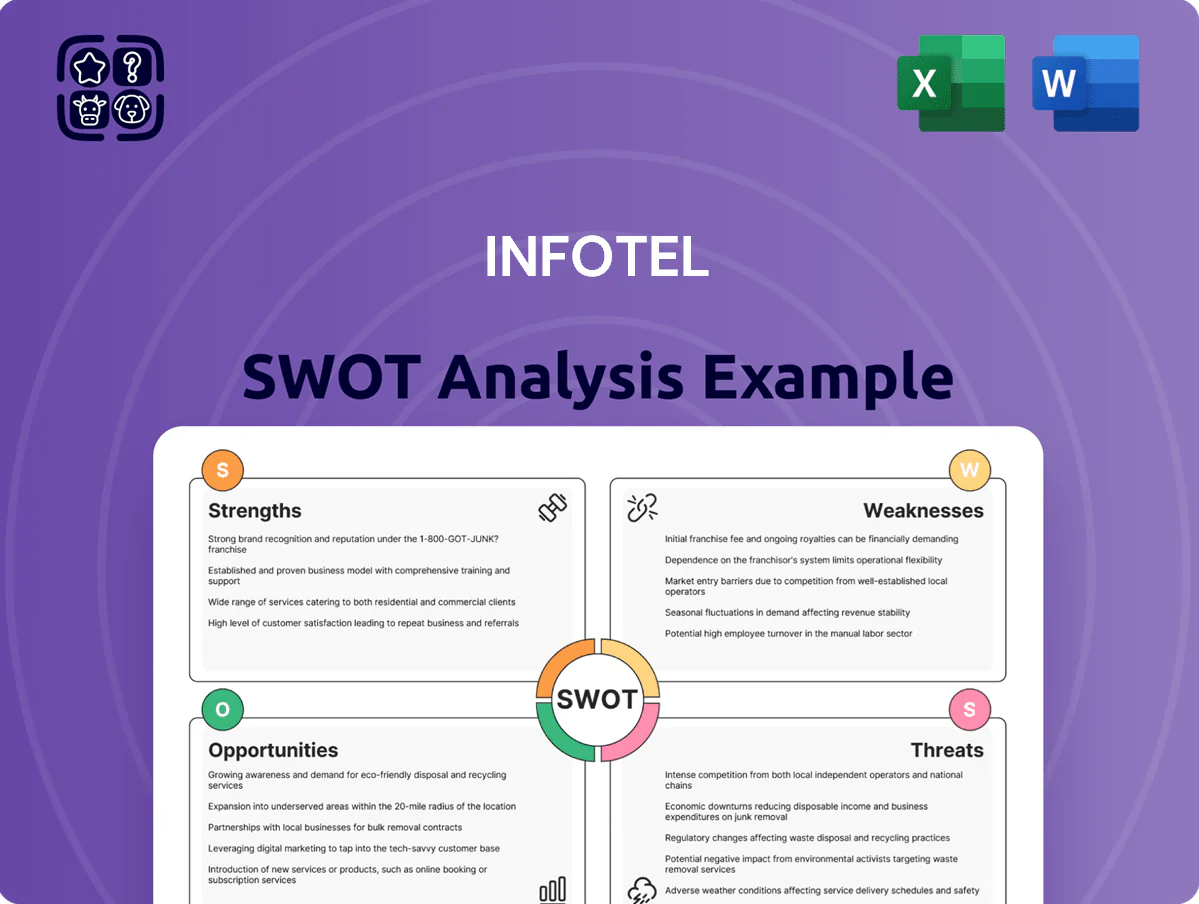

Strengths

Specialized Banking and Insurance Expertise

Infotel has built deep niche expertise in banking and insurance, serving top European clients like BNP Paribas and Allianz and capturing repeat contracts worth roughly €120m in 2024–2025.

By 4Q 2025 the company specializes in legacy core modernizations—mainframe-to-cloud migrations and regulatory reporting—projects generalist IT firms decline due to complexity and compliance risk.

This focus creates high entry barriers: competitors face multi-year ramp-up and certification costs, while Infotel’s backlog near €180m sustains steady high-value consulting revenue.

High-Margin Proprietary Software Division

Infotel’s proprietary software division, led by high-performance database management tools, yields recurring licensing revenue and gross margins around 68% versus ~28% for its services business, per company filings through 2025.

That margin gap lets software revenue—~38% of group revenue in FY2025—act as a buffer, cushioning EPS volatility when services bookings slow.

Robust Long-Term Client Loyalty

Infotel posts client retention above 95% for large accounts, with CAC 40 and global groups representing ~60% of 2025 revenue (€420m of €700m), and average relationship length >15 years, enabling trust-led cross-sell of cloud, AI and cybersecurity services that cut customer acquisition costs by ~30% and create a predictable multi-year revenue backlog.

Solid Financial Position and Cash Flow

As of FY2025 year-end, Infotel reported net cash of €185m, net debt/EBITDA of -0.2x and operating cash flow of €72m, enabling self-funding of organic growth and bolt-on M&A without costly external financing.

Investors prize this conservative stance: lower refinancing risk during 2024–25 rate spikes and a liquid buffer that supports capex and deal optionality.

- Net cash €185m

- OCF €72m in FY2025

- Net debt/EBITDA -0.2x

- Supports bolt-on M&A, reduces refinancing risk

Agility in Digital Transformation Services

Infotel has pivoted from legacy focus to offer cloud, big data, and mobile services, winning 18% revenue growth in digital services in 2024 and adding €24m in cloud contracts that year.

The firm bridges mainframes and modern architectures—mainframe modernization projects rose 35% in 2023—letting clients run hybrid IT stacks without rip-and-replace.

This dual capability keeps Infotel relevant as 62% of its customer base reported hybrid cloud adoption in 2025, reducing churn risk and expanding cross-sell opportunities.

- 2024 digital services rev +18%

- €24m in cloud contracts (2024)

- Mainframe modernization +35% (2023)

- 62% client hybrid cloud adoption (2025)

Infotel: €180m backlog, €185m net cash, 95% client retention — high-margin software growth

Infotel’s niche in banking/insurance drives repeat €120m contracts (2024–25) and a €180m backlog; FY2025 net cash €185m, OCF €72m, net debt/EBITDA -0.2x; software margins ~68% vs services ~28%, software = 38% revenue; digital services +18% (2024), €24m cloud deals; client retention >95%, avg relationship >15 years.

| Metric | Value |

|---|---|

| Backlog | €180m |

| Net cash | €185m |

| OCF FY2025 | €72m |

| Software margin | 68% |

What is included in the product

Provides a concise SWOT overview of Infotel, highlighting its core strengths and weaknesses while mapping external opportunities and threats that shape the company’s strategic trajectory.

Provides a clear, editable SWOT matrix tailored to Infotel for rapid alignment of strategy and stakeholder communication, enabling quick updates as priorities change.

Weaknesses

High Geographic Reliance on the French Market

About 75% of Infotel’s 2024 revenue (≈€210m of €280m) comes from France, leaving the firm highly exposed to French GDP swings and local regulation changes such as 2023–24 labor law updates that raised operating costs.

International sales grew 12% YoY in 2024 but still represent only ~25% of revenue, so Infotel lacks effective geographic hedging against a broader European slowdown.

Competitors with 40–60% non‑France revenue scale faster abroad; Infotel’s slower geographic diversification raises concentration risk and limits resilience.

Significant Client Concentration Risk

Infotel’s revenue is heavily weighted to a handful of large financial-services accounts—top 3 clients accounted for 58% of FY2025 revenue (year ending Dec 31, 2025), per company filings. If a major banking client insources IT or switches vendors, Infotel could lose a double-digit percentage of top-line growth in a single year. Replacing one lost contract would require many smaller engagements; average smaller-account revenue is $0.4m versus $45m for large accounts. This concentration raises acute renewal and pricing leverage risks.

Challenges in Scaling Global Operations

Infotel struggles to scale its specialized, proximity-driven service model into markets like North America and Asia, where competitors capture ~60–75% of large IT services deals; entering these regions raises upfront costs by an estimated $5–15M for local offices and talent per region. This localized expertise requirement slows bids, leaving Infotel at a size disadvantage on multi-regional contracts worth $200M+.

Labor Cost Sensitivity in Tech Recruitment

The ongoing shortage of specialized IT talent in Europe drove wage inflation of about 8–12% yearly in 2024, squeezing Infotel’s operating margins as hiring and retention costs rise.

As a mid-sized firm, Infotel competes with Big Tech and consultancies for the same engineers, causing 15–25% higher recruitment costs versus large peers, hitting the software division hardest where niche skills command premiums.

Slower Adoption of Emerging Technologies in Legacy Segments

Infotel’s strength in legacy systems risks tying revenue to tech being phased out; IDC reported in 2024 that 62% of enterprise workloads were on track to move to cloud-native by 2026, shrinking legacy demand.

If cloud adoption outpaces Infotel’s product modernization, its top-margin offerings could see a 20–30% revenue decline over three years based on similar transitions in European IT firms in 2023.

Balancing maintenance and new development forces sustained R&D spend—Infotel may need to raise R&D by ~3–5 percentage points of revenue to stay competitive, increasing cost pressure.

- Legacy expertise = near-term cash, long-term risk

- 62% cloud shift by 2026 (IDC, 2024)

- Potential 20–30% revenue hit in 3 years

- R&D likely +3–5 ppt of revenue required

Concentrated France exposure, client risk & legacy tech drag threaten margins and growth

High concentration: ~75% revenue from France (~€210m of €280m in 2024) and top 3 clients = 58% of FY2025 revenue, raising country and client risk; international sales ~25% (12% YoY growth) give weak geographic hedge. Talent squeeze: 2024 wage inflation 8–12% and 15–25% higher recruitment costs versus large peers, hitting software margins. Legacy exposure: 62% cloud shift by 2026 (IDC 2024) risks 20–30% revenue drop in 3 years; R&D likely needs +3–5 ppt of revenue.

| Metric | Value |

|---|---|

| France revenue share (2024) | ~75% (€210m/€280m) |

| Top 3 clients (FY2025) | 58% revenue |

| Intl revenue share (2024) | ~25% (12% YoY growth) |

| Wage inflation (2024) | 8–12% |

| Recruitment premium vs peers | 15–25% |

| Cloud shift (IDC) | 62% by 2026 |

| Potential legacy revenue hit | 20–30% in 3 years |

| Additional R&D needed | +3–5 ppt revenue |

Preview the Actual Deliverable

Infotel SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re viewing a live preview of the real analysis; once purchased, the complete, detailed report becomes available immediately.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Infotel’s SWOT snapshot highlights robust niche expertise and recurring revenue but also warns of scaling and regulatory risks; for a full, research-backed breakdown with strategic recommendations and editable Word/Excel deliverables, purchase the complete SWOT analysis to confidently plan, pitch, or invest.

Strengths

Specialized Banking and Insurance Expertise

Infotel has built deep niche expertise in banking and insurance, serving top European clients like BNP Paribas and Allianz and capturing repeat contracts worth roughly €120m in 2024–2025.

By 4Q 2025 the company specializes in legacy core modernizations—mainframe-to-cloud migrations and regulatory reporting—projects generalist IT firms decline due to complexity and compliance risk.

This focus creates high entry barriers: competitors face multi-year ramp-up and certification costs, while Infotel’s backlog near €180m sustains steady high-value consulting revenue.

High-Margin Proprietary Software Division

Infotel’s proprietary software division, led by high-performance database management tools, yields recurring licensing revenue and gross margins around 68% versus ~28% for its services business, per company filings through 2025.

That margin gap lets software revenue—~38% of group revenue in FY2025—act as a buffer, cushioning EPS volatility when services bookings slow.

Robust Long-Term Client Loyalty

Infotel posts client retention above 95% for large accounts, with CAC 40 and global groups representing ~60% of 2025 revenue (€420m of €700m), and average relationship length >15 years, enabling trust-led cross-sell of cloud, AI and cybersecurity services that cut customer acquisition costs by ~30% and create a predictable multi-year revenue backlog.

Solid Financial Position and Cash Flow

As of FY2025 year-end, Infotel reported net cash of €185m, net debt/EBITDA of -0.2x and operating cash flow of €72m, enabling self-funding of organic growth and bolt-on M&A without costly external financing.

Investors prize this conservative stance: lower refinancing risk during 2024–25 rate spikes and a liquid buffer that supports capex and deal optionality.

- Net cash €185m

- OCF €72m in FY2025

- Net debt/EBITDA -0.2x

- Supports bolt-on M&A, reduces refinancing risk

Agility in Digital Transformation Services

Infotel has pivoted from legacy focus to offer cloud, big data, and mobile services, winning 18% revenue growth in digital services in 2024 and adding €24m in cloud contracts that year.

The firm bridges mainframes and modern architectures—mainframe modernization projects rose 35% in 2023—letting clients run hybrid IT stacks without rip-and-replace.

This dual capability keeps Infotel relevant as 62% of its customer base reported hybrid cloud adoption in 2025, reducing churn risk and expanding cross-sell opportunities.

- 2024 digital services rev +18%

- €24m in cloud contracts (2024)

- Mainframe modernization +35% (2023)

- 62% client hybrid cloud adoption (2025)

Infotel: €180m backlog, €185m net cash, 95% client retention — high-margin software growth

Infotel’s niche in banking/insurance drives repeat €120m contracts (2024–25) and a €180m backlog; FY2025 net cash €185m, OCF €72m, net debt/EBITDA -0.2x; software margins ~68% vs services ~28%, software = 38% revenue; digital services +18% (2024), €24m cloud deals; client retention >95%, avg relationship >15 years.

| Metric | Value |

|---|---|

| Backlog | €180m |

| Net cash | €185m |

| OCF FY2025 | €72m |

| Software margin | 68% |

What is included in the product

Provides a concise SWOT overview of Infotel, highlighting its core strengths and weaknesses while mapping external opportunities and threats that shape the company’s strategic trajectory.

Provides a clear, editable SWOT matrix tailored to Infotel for rapid alignment of strategy and stakeholder communication, enabling quick updates as priorities change.

Weaknesses

High Geographic Reliance on the French Market

About 75% of Infotel’s 2024 revenue (≈€210m of €280m) comes from France, leaving the firm highly exposed to French GDP swings and local regulation changes such as 2023–24 labor law updates that raised operating costs.

International sales grew 12% YoY in 2024 but still represent only ~25% of revenue, so Infotel lacks effective geographic hedging against a broader European slowdown.

Competitors with 40–60% non‑France revenue scale faster abroad; Infotel’s slower geographic diversification raises concentration risk and limits resilience.

Significant Client Concentration Risk

Infotel’s revenue is heavily weighted to a handful of large financial-services accounts—top 3 clients accounted for 58% of FY2025 revenue (year ending Dec 31, 2025), per company filings. If a major banking client insources IT or switches vendors, Infotel could lose a double-digit percentage of top-line growth in a single year. Replacing one lost contract would require many smaller engagements; average smaller-account revenue is $0.4m versus $45m for large accounts. This concentration raises acute renewal and pricing leverage risks.

Challenges in Scaling Global Operations

Infotel struggles to scale its specialized, proximity-driven service model into markets like North America and Asia, where competitors capture ~60–75% of large IT services deals; entering these regions raises upfront costs by an estimated $5–15M for local offices and talent per region. This localized expertise requirement slows bids, leaving Infotel at a size disadvantage on multi-regional contracts worth $200M+.

Labor Cost Sensitivity in Tech Recruitment

The ongoing shortage of specialized IT talent in Europe drove wage inflation of about 8–12% yearly in 2024, squeezing Infotel’s operating margins as hiring and retention costs rise.

As a mid-sized firm, Infotel competes with Big Tech and consultancies for the same engineers, causing 15–25% higher recruitment costs versus large peers, hitting the software division hardest where niche skills command premiums.

Slower Adoption of Emerging Technologies in Legacy Segments

Infotel’s strength in legacy systems risks tying revenue to tech being phased out; IDC reported in 2024 that 62% of enterprise workloads were on track to move to cloud-native by 2026, shrinking legacy demand.

If cloud adoption outpaces Infotel’s product modernization, its top-margin offerings could see a 20–30% revenue decline over three years based on similar transitions in European IT firms in 2023.

Balancing maintenance and new development forces sustained R&D spend—Infotel may need to raise R&D by ~3–5 percentage points of revenue to stay competitive, increasing cost pressure.

- Legacy expertise = near-term cash, long-term risk

- 62% cloud shift by 2026 (IDC, 2024)

- Potential 20–30% revenue hit in 3 years

- R&D likely +3–5 ppt of revenue required

Concentrated France exposure, client risk & legacy tech drag threaten margins and growth

High concentration: ~75% revenue from France (~€210m of €280m in 2024) and top 3 clients = 58% of FY2025 revenue, raising country and client risk; international sales ~25% (12% YoY growth) give weak geographic hedge. Talent squeeze: 2024 wage inflation 8–12% and 15–25% higher recruitment costs versus large peers, hitting software margins. Legacy exposure: 62% cloud shift by 2026 (IDC 2024) risks 20–30% revenue drop in 3 years; R&D likely needs +3–5 ppt of revenue.

| Metric | Value |

|---|---|

| France revenue share (2024) | ~75% (€210m/€280m) |

| Top 3 clients (FY2025) | 58% revenue |

| Intl revenue share (2024) | ~25% (12% YoY growth) |

| Wage inflation (2024) | 8–12% |

| Recruitment premium vs peers | 15–25% |

| Cloud shift (IDC) | 62% by 2026 |

| Potential legacy revenue hit | 20–30% in 3 years |

| Additional R&D needed | +3–5 ppt revenue |

Preview the Actual Deliverable

Infotel SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re viewing a live preview of the real analysis; once purchased, the complete, detailed report becomes available immediately.