Infratil Boston Consulting Group Matrix

Actionable Strategy Starts Here

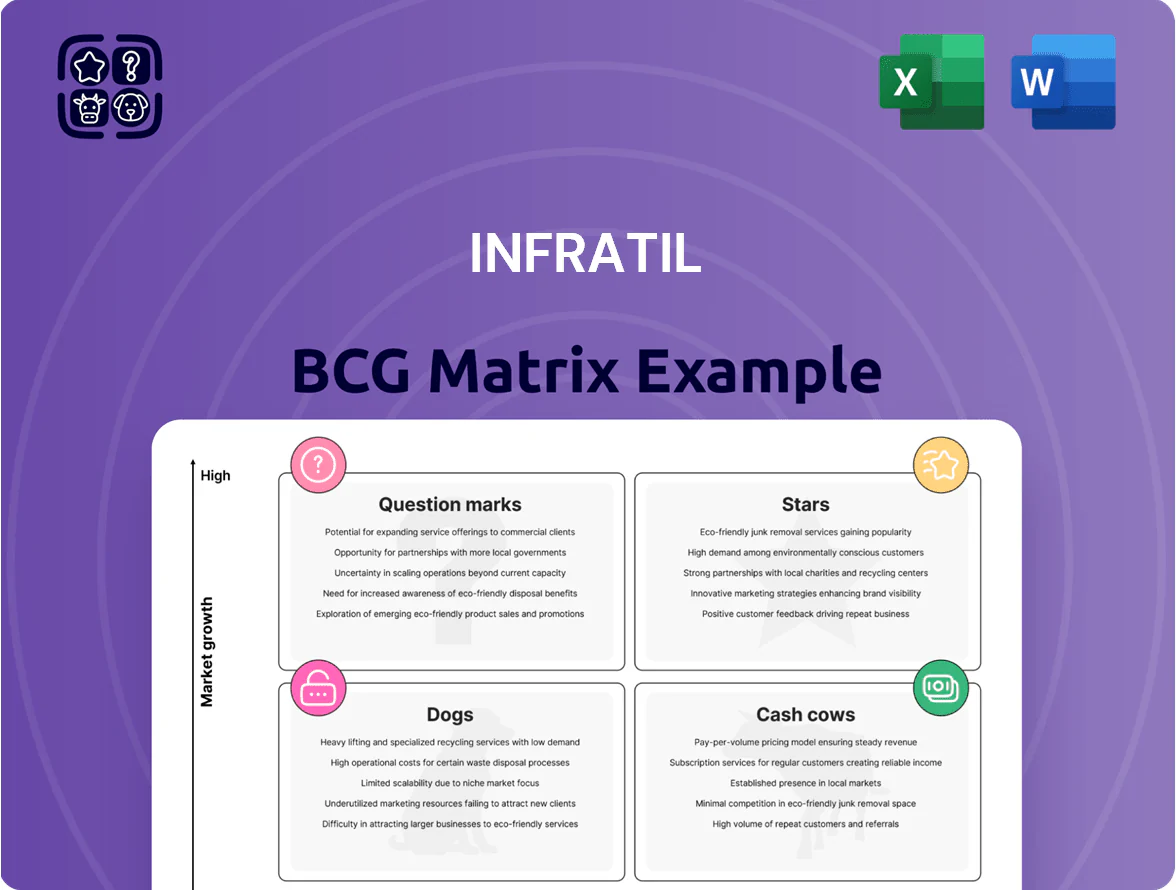

Infratil’s BCG Matrix preview highlights how its core infrastructure assets likely span Cash Cows (steady utilities and airports) and potential Stars (growing renewable energy platforms), while showing where selective divestment could trim underperforming holdings. This snapshot hints at capital allocation levers and risk concentrations across the portfolio—critical for investors and strategists alike. Purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and a downloadable Word + Excel package to act on these insights immediately.

Stars

CDC Data Centres

CDC Data Centres remains Infratil’s primary growth engine, holding ~38% market share in sovereign data centre capacity across Australia and New Zealand by Q3 2025 and driving LTM revenue of NZD 420m.

Surging generative AI and cloud demand pushed CDC to add ~120 MW of capacity in 2024–25, requiring capex of NZD 560m and lifting EBITDA margins to ~48%.

High growth class placement in the BCG Matrix is clear: strong market share in a high-growth sector, but ongoing heavy capital intensity keeps cash conversion and dividend contributions constrained.

One New Zealand

One NZ, New Zealand’s leading mobile and digital services provider, is a Star in Infratil’s BCG matrix after 5G rollout and integrated solutions lifted service ARPU to NZD 45.2 in FY2024 and mobile market share to ~38% as of Dec 2024.

Heavy capex—NZD 620m on 5G, satellite-to-mobile trials, and NZD 180m on enterprise fiber in 2024—supports high growth and premium pricing in a digital-first economy, making One NZ a portfolio cornerstone.

Console Connect

Console Connect, Infratil’s software-defined interconnection platform, held an estimated 18% share of the global automated networking market by end-2025 and reported revenue growth of 27% YoY in 2025 (~NZD 62m), classifying it as a Star in the BCG matrix.

Operating in the cloud-to-cloud connectivity segment—which grew ~22% CAGR 2020–2025 to USD 7.4bn—Console Connect needs sustained capex and R&D to fend off global rivals and preserve margin expansion.

The platform’s value rises with multi-cloud complexity: by 2025 enterprises ran an average 3.2 clouds, increasing demand for dynamic interconnection and strengthening Console Connect’s strategic role in global digital infrastructure.

Kao Data

Kao Data is a Star in Infratil’s BCG matrix, serving the UK high-performance computing (HPC) market with industrial-scale AI capacity; by Dec 2025 it operated 120+ MW of commissioned capacity across London, Thames Valley, and Manchester, capturing ~18% of the UK AI colocation market.

Its regional expansion into UK hubs by late 2025 secured strong positioning in the fast-growing European data corridor, with revenue growth ~42% YoY in 2024–25 and >90% average rack utilization from tier-one cloud and AI clients.

It remains cash-hungry for facility builds—capex ~£260m 2023–25—but high utilization and multi-year contracts validate leadership and pathway to margin improvement as scale amortizes costs.

- 120+ MW capacity by Dec 2025

- ~18% UK AI colocation share

- ~42% revenue growth 2024–25

- 90% rack utilization

- £260m capex 2023–25

Gurīn Energy

Gurīn Energy sits in Infratil’s BCG Matrix Star quadrant as its Asian solar and wind pipeline nears operational scale, with 2025 consolidated capacity reaching ~1.1 GW and expected 35% EBITDA CAGR through 2027.

Rapid electrification in Indonesia and Thailand boosts demand—regional renewables growth projected at ~9% CAGR 2024–30—giving Gurīn a strong market tailwind.

Infratil’s funding—NZD 450m since 2023—helped capture ~12% of new utility-scale renewables capacity awards versus legacy utilities.

- 2025 capacity ~1.1 GW

- EBITDA CAGR 35% (2025–27)

- Regional renewables growth ~9% CAGR (2024–30)

- Infratil funding NZD 450m since 2023

- Market share ~12% of new capacity awards

Infratil’s Growth Engines: Data Centres, 5G, Networking, AI Power & Renewables

Infratil Stars: CDC Data Centres (38% ANZ sovereign share, LTM revenue NZD 420m, NZD 560m capex 2024–25); One NZ (38% mobile share, ARPU NZD 45.2, NZD 620m 5G capex 2024); Console Connect (18% automated networking, 27% revenue growth 2025, NZD 62m revenue); Kao Data (120+ MW, ~18% UK AI colocation, £260m capex 2023–25); Gurīn (1.1 GW 2025, NZD 450m funding).

| Asset | Key metric |

|---|---|

| CDC | 38% share, NZD 420m |

| One NZ | 38% share, ARPU NZD 45.2 |

| Console | 18% share, NZD 62m |

| Kao | 120+ MW, £260m |

| Gurīn | 1.1 GW, NZD 450m |

What is included in the product

Comprehensive BCG analysis of Infratil’s units with strategic recommendations per quadrant, noting competitive strengths, risks and macro trends.

One-page Infratil BCG Matrix positioning each asset by growth and share for quick executive decisions.

Cash Cows

Wellington Airport

Wellington Airport, a strategic monopoly in central New Zealand, delivered stable cash flows with FY2025 passenger volumes at ~6.1 million—back to ~99% of 2019 levels—supporting FY2025 operating EBITDA margin near 62% and low growth capex (~NZD40m guidance).

RHCNZ Medical Imaging

RHCNZ Medical Imaging holds ~45% share of New Zealand’s diagnostic imaging market (2024 NZ Ministry of Health data), delivering steady demand and low single-digit volume growth.

Established network of 60+ clinics and multi-year contracts produced NZD 48m EBITDA and NZD 30m free cash flow in FY2024, per Infratil FY2024 report.

Maintenance capex ran ~NZD 6m (FY2024), so RHCNZ is a reliable liquidity source funding Infratil’s higher-risk initiatives.

Qscan Group

Qscan Group holds a strong position in Australia’s diagnostic-imaging market, serving an aging population and classified as an essential healthcare service, which supports stable demand.

By late 2025 Qscan had reduced clinic overlap and raised utilization, delivering EBITDA margins around 28% and annual free cash flow near A$45–50m, per Infratil disclosures.

As a defensive asset, Qscan generates steady cash irrespective of economic cycles, matching the BCG Cash Cow profile and funding Infratil’s growth or dividends.

Mature Renewable Assets

Infratil’s mature New Zealand wind and hydro assets run with near-zero marginal costs and held ~35–40% market share in market regions in 2024, delivering stable EBITDA margins around 60% and generating NZD 220–260m cash annually in 2024.

These sites are backed by long-term power purchase agreements (PPAs) averaging 10–15 years and operate within a stable regulatory framework that limits new entrant risk.

Cash flow is primarily directed to service corporate debt—Infratil reported net debt NZD 1.8bn at 30 Sep 2024—and to fund development of Question Marks (emerging renewables and tech investments).

- Mature assets: low marginal cost, ~60% EBITDA margin

- Market share: ~35–40% in key NZ regions (2024)

- Cash generation: NZD 220–260m p.a. (2024)

- Uses: service NZD 1.8bn net debt; fund Question Marks

RetireAustralia

RetireAustralia, operating in Australia’s mature senior living sector, delivers stable occupancy ~92% in FY2024 and management fee income of ~A$85m, providing steady cash flow to Infratil.

Scale drives efficiencies: 60+ villages and ~7,500 units produce high cash conversion (operating cash margin ~28% in 2024), while modest annual revenue growth (~3–4%) trails digital infra.

Market leadership in NSW and Victoria ensures predictable capital returns for Infratil, funding higher-growth segments without raising external debt.

- Occupancy ~92% (FY2024)

- Management fees ~A$85m (2024)

- 60+ villages, ~7,500 units

- Operating cash margin ~28% (2024)

- Revenue growth ~3–4% p.a.

Infratil’s high‑margin cash engines: NZ airports, renewables, Qscan, RHCNZ, RetireAus

Infratil Cash Cows: Wellington Airport, RHCNZ, Qscan, NZ wind/hydro, RetireAustralia generate stable, high-margin cash (EBITDA margins ~28–62%), annual cash ~NZD 220–260m plus A$45–50m (Qscan) and A$85m fees (RetireAustralia); net debt NZD 1.8bn (30 Sep 2024); cash funds debt service and growth.

| Asset | Key metrics |

|---|---|

| WLG | 6.1m pax FY25, 62% EBITDA |

| RHCNZ | 45% share, NZD48m EBITDA |

| Qscan | A$45–50m FCF, 28% EBITDA |

| Renewables | NZD220–260m cash, 60% EBITDA |

| RetireAus | 92% occ, A$85m fees |

Full Transparency, Always

Infratil BCG Matrix

The file you're previewing is the exact Infratil BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document tailored for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Infratil’s BCG Matrix preview highlights how its core infrastructure assets likely span Cash Cows (steady utilities and airports) and potential Stars (growing renewable energy platforms), while showing where selective divestment could trim underperforming holdings. This snapshot hints at capital allocation levers and risk concentrations across the portfolio—critical for investors and strategists alike. Purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and a downloadable Word + Excel package to act on these insights immediately.

Stars

CDC Data Centres

CDC Data Centres remains Infratil’s primary growth engine, holding ~38% market share in sovereign data centre capacity across Australia and New Zealand by Q3 2025 and driving LTM revenue of NZD 420m.

Surging generative AI and cloud demand pushed CDC to add ~120 MW of capacity in 2024–25, requiring capex of NZD 560m and lifting EBITDA margins to ~48%.

High growth class placement in the BCG Matrix is clear: strong market share in a high-growth sector, but ongoing heavy capital intensity keeps cash conversion and dividend contributions constrained.

One New Zealand

One NZ, New Zealand’s leading mobile and digital services provider, is a Star in Infratil’s BCG matrix after 5G rollout and integrated solutions lifted service ARPU to NZD 45.2 in FY2024 and mobile market share to ~38% as of Dec 2024.

Heavy capex—NZD 620m on 5G, satellite-to-mobile trials, and NZD 180m on enterprise fiber in 2024—supports high growth and premium pricing in a digital-first economy, making One NZ a portfolio cornerstone.

Console Connect

Console Connect, Infratil’s software-defined interconnection platform, held an estimated 18% share of the global automated networking market by end-2025 and reported revenue growth of 27% YoY in 2025 (~NZD 62m), classifying it as a Star in the BCG matrix.

Operating in the cloud-to-cloud connectivity segment—which grew ~22% CAGR 2020–2025 to USD 7.4bn—Console Connect needs sustained capex and R&D to fend off global rivals and preserve margin expansion.

The platform’s value rises with multi-cloud complexity: by 2025 enterprises ran an average 3.2 clouds, increasing demand for dynamic interconnection and strengthening Console Connect’s strategic role in global digital infrastructure.

Kao Data

Kao Data is a Star in Infratil’s BCG matrix, serving the UK high-performance computing (HPC) market with industrial-scale AI capacity; by Dec 2025 it operated 120+ MW of commissioned capacity across London, Thames Valley, and Manchester, capturing ~18% of the UK AI colocation market.

Its regional expansion into UK hubs by late 2025 secured strong positioning in the fast-growing European data corridor, with revenue growth ~42% YoY in 2024–25 and >90% average rack utilization from tier-one cloud and AI clients.

It remains cash-hungry for facility builds—capex ~£260m 2023–25—but high utilization and multi-year contracts validate leadership and pathway to margin improvement as scale amortizes costs.

- 120+ MW capacity by Dec 2025

- ~18% UK AI colocation share

- ~42% revenue growth 2024–25

- 90% rack utilization

- £260m capex 2023–25

Gurīn Energy

Gurīn Energy sits in Infratil’s BCG Matrix Star quadrant as its Asian solar and wind pipeline nears operational scale, with 2025 consolidated capacity reaching ~1.1 GW and expected 35% EBITDA CAGR through 2027.

Rapid electrification in Indonesia and Thailand boosts demand—regional renewables growth projected at ~9% CAGR 2024–30—giving Gurīn a strong market tailwind.

Infratil’s funding—NZD 450m since 2023—helped capture ~12% of new utility-scale renewables capacity awards versus legacy utilities.

- 2025 capacity ~1.1 GW

- EBITDA CAGR 35% (2025–27)

- Regional renewables growth ~9% CAGR (2024–30)

- Infratil funding NZD 450m since 2023

- Market share ~12% of new capacity awards

Infratil’s Growth Engines: Data Centres, 5G, Networking, AI Power & Renewables

Infratil Stars: CDC Data Centres (38% ANZ sovereign share, LTM revenue NZD 420m, NZD 560m capex 2024–25); One NZ (38% mobile share, ARPU NZD 45.2, NZD 620m 5G capex 2024); Console Connect (18% automated networking, 27% revenue growth 2025, NZD 62m revenue); Kao Data (120+ MW, ~18% UK AI colocation, £260m capex 2023–25); Gurīn (1.1 GW 2025, NZD 450m funding).

| Asset | Key metric |

|---|---|

| CDC | 38% share, NZD 420m |

| One NZ | 38% share, ARPU NZD 45.2 |

| Console | 18% share, NZD 62m |

| Kao | 120+ MW, £260m |

| Gurīn | 1.1 GW, NZD 450m |

What is included in the product

Comprehensive BCG analysis of Infratil’s units with strategic recommendations per quadrant, noting competitive strengths, risks and macro trends.

One-page Infratil BCG Matrix positioning each asset by growth and share for quick executive decisions.

Cash Cows

Wellington Airport

Wellington Airport, a strategic monopoly in central New Zealand, delivered stable cash flows with FY2025 passenger volumes at ~6.1 million—back to ~99% of 2019 levels—supporting FY2025 operating EBITDA margin near 62% and low growth capex (~NZD40m guidance).

RHCNZ Medical Imaging

RHCNZ Medical Imaging holds ~45% share of New Zealand’s diagnostic imaging market (2024 NZ Ministry of Health data), delivering steady demand and low single-digit volume growth.

Established network of 60+ clinics and multi-year contracts produced NZD 48m EBITDA and NZD 30m free cash flow in FY2024, per Infratil FY2024 report.

Maintenance capex ran ~NZD 6m (FY2024), so RHCNZ is a reliable liquidity source funding Infratil’s higher-risk initiatives.

Qscan Group

Qscan Group holds a strong position in Australia’s diagnostic-imaging market, serving an aging population and classified as an essential healthcare service, which supports stable demand.

By late 2025 Qscan had reduced clinic overlap and raised utilization, delivering EBITDA margins around 28% and annual free cash flow near A$45–50m, per Infratil disclosures.

As a defensive asset, Qscan generates steady cash irrespective of economic cycles, matching the BCG Cash Cow profile and funding Infratil’s growth or dividends.

Mature Renewable Assets

Infratil’s mature New Zealand wind and hydro assets run with near-zero marginal costs and held ~35–40% market share in market regions in 2024, delivering stable EBITDA margins around 60% and generating NZD 220–260m cash annually in 2024.

These sites are backed by long-term power purchase agreements (PPAs) averaging 10–15 years and operate within a stable regulatory framework that limits new entrant risk.

Cash flow is primarily directed to service corporate debt—Infratil reported net debt NZD 1.8bn at 30 Sep 2024—and to fund development of Question Marks (emerging renewables and tech investments).

- Mature assets: low marginal cost, ~60% EBITDA margin

- Market share: ~35–40% in key NZ regions (2024)

- Cash generation: NZD 220–260m p.a. (2024)

- Uses: service NZD 1.8bn net debt; fund Question Marks

RetireAustralia

RetireAustralia, operating in Australia’s mature senior living sector, delivers stable occupancy ~92% in FY2024 and management fee income of ~A$85m, providing steady cash flow to Infratil.

Scale drives efficiencies: 60+ villages and ~7,500 units produce high cash conversion (operating cash margin ~28% in 2024), while modest annual revenue growth (~3–4%) trails digital infra.

Market leadership in NSW and Victoria ensures predictable capital returns for Infratil, funding higher-growth segments without raising external debt.

- Occupancy ~92% (FY2024)

- Management fees ~A$85m (2024)

- 60+ villages, ~7,500 units

- Operating cash margin ~28% (2024)

- Revenue growth ~3–4% p.a.

Infratil’s high‑margin cash engines: NZ airports, renewables, Qscan, RHCNZ, RetireAus

Infratil Cash Cows: Wellington Airport, RHCNZ, Qscan, NZ wind/hydro, RetireAustralia generate stable, high-margin cash (EBITDA margins ~28–62%), annual cash ~NZD 220–260m plus A$45–50m (Qscan) and A$85m fees (RetireAustralia); net debt NZD 1.8bn (30 Sep 2024); cash funds debt service and growth.

| Asset | Key metrics |

|---|---|

| WLG | 6.1m pax FY25, 62% EBITDA |

| RHCNZ | 45% share, NZD48m EBITDA |

| Qscan | A$45–50m FCF, 28% EBITDA |

| Renewables | NZD220–260m cash, 60% EBITDA |

| RetireAus | 92% occ, A$85m fees |

Full Transparency, Always

Infratil BCG Matrix

The file you're previewing is the exact Infratil BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document tailored for strategic decision-making.