Infrea Porter's Five Forces Analysis

From Overview to Strategy Blueprint

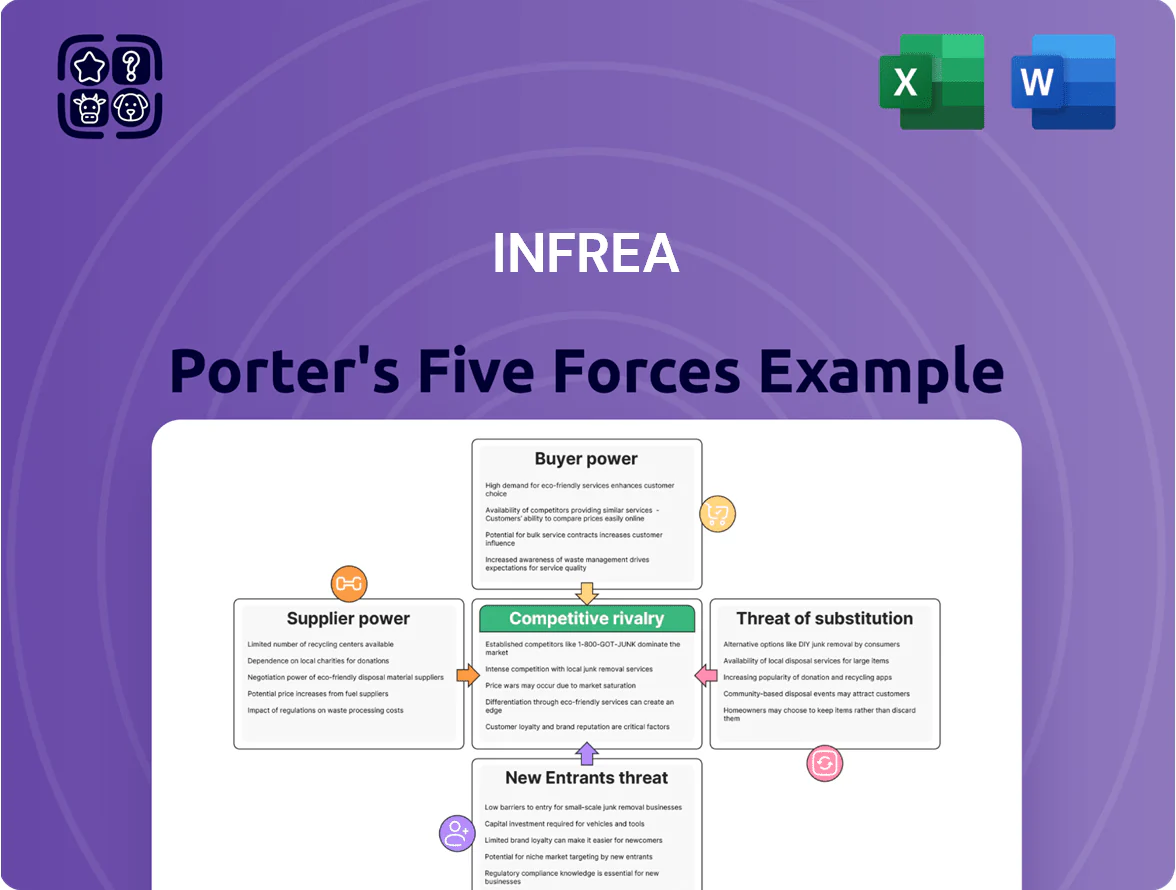

Infrea faces moderate supplier power and rising threat of new entrants due to niche infrastructure demand, while buyer bargaining and substitutes remain controlled by long-term contracts and specialized tech; competitive rivalry is intensifying with consolidation and margin pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Infrea’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Equipment Manufacturers

Infrea depends on a handful of global manufacturers for wind turbines, district-heating pipe systems, and advanced water filters, giving those suppliers strong leverage.

By late 2025, shortages in high-tech renewable components pushed turbine OEM order backlogs to ~24–30 months and premiums of 10–18% on contracts, raising procurement costs for Infrea.

That concentration risks project delays and cost overruns if supply chains break or priority goes to larger markets, potentially adding 5–12% to capex on affected projects.

Skilled Technical Labor Shortage

The Swedish infrastructure sector faces a shortage of specialized engineers and technicians for water and energy systems; Sweden had a 2024 shortfall of about 8,000 skilled construction and engineering workers, raising wage pressure.

Suppliers of specialist labor or the labor force can demand higher wages and contract terms, squeezing Infrea’s margins—average specialist wage growth in 2023–24 was ~4.5% annually.

Infrea must fund long-term partnerships and internal training; a 3‑year apprenticeship program costing ~SEK 2.5–3.5m could cut reliance on external hires by 30%.

Raw Material and Energy Input Volatility

For district heating assets, fuel costs—biomass, municipal waste—drive margins; global biomass prices rose ~18% from 2020–2024 and commodity volatility spiked in 2022–23, so suppliers wield real leverage over costs. Infrea offsets this by signing long-term supply contracts covering ~70–90% of volume, but typical price‑indexation clauses (linked to EUR/MWh or CPI) still pass increases to Infrea, leaving supplier power materially high into 2025.

Technology and Digital Infrastructure Providers

As grids digitize, specialized software vendors for grid management and asset monitoring hold rising leverage; the global smart grid software market hit $11.7B in 2024, up 12% y/y, concentrating vendor importance.

Subscription pricing and proprietary APIs create high switching costs—benchmarks show 55–70% of utility OPEX tied to SaaS contracts—so Infrea faces entrenched dependencies.

Reliance on specific platforms for uptime and analytics lets suppliers push harder on renewal pricing and SLAs, often raising contract value by 8–15% at renewal.

- Market size: $11.7B (2024)

- SaaS OPEX share: 55–70%

- Renewal price uplift: 8–15%

Regulatory and Compliance Service Providers

With Nordic environmental rules tightening through 2025, specialized consultancies and auditors are now essential for Infrea to keep water and waste licenses; their certifications are legally required and non-transferable.

The market has about 12 accredited firms across Norway, Sweden, Denmark, and Finland, letting them charge premiums—typical audit fees rose 18% in 2024, averaging €45–60k per major project.

Infrea faces supplier power risk: few suppliers, mandatory certification, rising fees, and limited switching options increase operating costs and regulatory exposure.

- ~12 accredited firms region-wide

- Audit fees +18% in 2024, €45–60k/project

- Certifications mandatory for licenses

- High switching costs and limited alternatives

Suppliers squeeze margins: 24–30m turbine backlogs, 10–18% premiums, rising capex

Suppliers hold high bargaining power: concentration in turbine, filter, and software vendors, plus 12 regional certifiers, caused 24–30 month turbine backlogs, 10–18% procurement premiums, 8–15% SaaS renewal uplifts, and audit fees up 18% (€45–60k) by 2024; labor shortages (8,000 deficit, 4.5% wage growth) add 5–12% capex risk.

| Metric | Value |

|---|---|

| Turbine backlog | 24–30 months |

| Procurement premium | 10–18% |

| SaaS renewal uplift | 8–15% |

| Audit fees | €45–60k (+18% 2024) |

| Labor shortfall (Sweden) | ~8,000 |

| Specialist wage growth | ~4.5% (2023–24) |

What is included in the product

Concise Porter's Five Forces analysis tailored for Infrea, uncovering competitive drivers, buyer/supplier leverage, entry barriers, substitutes, and emerging threats to inform strategic decisions and investor materials.

Infrea's Porter's Five Forces delivers a single-sheet, customizable SWOT-style view—quickly pinpoint competitive pressures and relieve decision-making friction for strategic planning.

Customers Bargaining Power

Municipal Procurement Power

Industrial Client Concentration

In recycling and renewable-energy lines, three industrial clients often supply over 60% of demand for comparable assets, so Infrea faces concentrated buyer power that pressures pricing and contract terms.

Large customers can demand price cuts or bespoke infrastructure, and in 2025 a lost contract worth 20% of an asset’s revenue could cut that asset’s EBITDA by roughly 12–18%.

Regulatory Price Caps and Oversight

Public Opinion and Political Pressure

As a provider of essential services, Infrea faces strong customer bargaining power channeled through public opinion and political actors; 2024 UK polling showed 68% oppose utility price rises, making regulators quick to act.

High visibility of tariffs means a 10%+ hike risks local government intervention or tariff freezes, so Infrea must balance margin targets with affordability to keep its social license.

- 68% public opposition to utility hikes (UK, 2024)

- 10%+ price rise often triggers political scrutiny

- Social license tied to affordability and visible service quality

Availability of Alternative Energy Solutions

Large commercial customers increasingly pursue self-generation—on-site solar and private microgrids—raising their bargaining power; global commercial solar capacity grew ~12% in 2024, and corporate PPAs hit a record 33 GW in 2023, showing a clear shift.

By threatening to cut dependence on Infrea’s centralized district heating or energy assets, customers can push for lower rates or flexible contracts; losing a 10% top-customer load could cut EBITDA by several points.

To retain customers, Infrea must offer value-added services—demand-response, resiliency guarantees, bundled energy-as-a-service—and prove superior reliability versus decentralized options, with targets like 99.99% uptime and integrated remote monitoring.

- Corporate on-site solar growth ~12% (2024)

- Corporate PPAs reached 33 GW (2023)

- Target reliability: 99.99% uptime

- Risk: 10% load loss → multi-point EBITDA hit

High municipal reliance and buyer concentration risk: losing contracts can cut EBITDA 12–18%

| Metric | Value |

|---|---|

| Municipal revenue share (2024) | 62% of SEK 1.1bn |

| Municipal contract margins (2023) | 6–8% |

| Industrial buyer concentration | >60% for some assets |

| Regulatory return caps (2024–25) | 3–5% real |

| Public opposition to hikes (UK, 2024) | 68% |

| Impact of lost contract | EBITDA −12–18% (10–20% revenue) |

Full Version Awaits

Infrea Porter's Five Forces Analysis

This preview shows the exact Infrea Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

You're looking at the full, professionally formatted document; once you buy, this identical file will be available for instant download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Infrea faces moderate supplier power and rising threat of new entrants due to niche infrastructure demand, while buyer bargaining and substitutes remain controlled by long-term contracts and specialized tech; competitive rivalry is intensifying with consolidation and margin pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Infrea’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Equipment Manufacturers

Infrea depends on a handful of global manufacturers for wind turbines, district-heating pipe systems, and advanced water filters, giving those suppliers strong leverage.

By late 2025, shortages in high-tech renewable components pushed turbine OEM order backlogs to ~24–30 months and premiums of 10–18% on contracts, raising procurement costs for Infrea.

That concentration risks project delays and cost overruns if supply chains break or priority goes to larger markets, potentially adding 5–12% to capex on affected projects.

Skilled Technical Labor Shortage

The Swedish infrastructure sector faces a shortage of specialized engineers and technicians for water and energy systems; Sweden had a 2024 shortfall of about 8,000 skilled construction and engineering workers, raising wage pressure.

Suppliers of specialist labor or the labor force can demand higher wages and contract terms, squeezing Infrea’s margins—average specialist wage growth in 2023–24 was ~4.5% annually.

Infrea must fund long-term partnerships and internal training; a 3‑year apprenticeship program costing ~SEK 2.5–3.5m could cut reliance on external hires by 30%.

Raw Material and Energy Input Volatility

For district heating assets, fuel costs—biomass, municipal waste—drive margins; global biomass prices rose ~18% from 2020–2024 and commodity volatility spiked in 2022–23, so suppliers wield real leverage over costs. Infrea offsets this by signing long-term supply contracts covering ~70–90% of volume, but typical price‑indexation clauses (linked to EUR/MWh or CPI) still pass increases to Infrea, leaving supplier power materially high into 2025.

Technology and Digital Infrastructure Providers

As grids digitize, specialized software vendors for grid management and asset monitoring hold rising leverage; the global smart grid software market hit $11.7B in 2024, up 12% y/y, concentrating vendor importance.

Subscription pricing and proprietary APIs create high switching costs—benchmarks show 55–70% of utility OPEX tied to SaaS contracts—so Infrea faces entrenched dependencies.

Reliance on specific platforms for uptime and analytics lets suppliers push harder on renewal pricing and SLAs, often raising contract value by 8–15% at renewal.

- Market size: $11.7B (2024)

- SaaS OPEX share: 55–70%

- Renewal price uplift: 8–15%

Regulatory and Compliance Service Providers

With Nordic environmental rules tightening through 2025, specialized consultancies and auditors are now essential for Infrea to keep water and waste licenses; their certifications are legally required and non-transferable.

The market has about 12 accredited firms across Norway, Sweden, Denmark, and Finland, letting them charge premiums—typical audit fees rose 18% in 2024, averaging €45–60k per major project.

Infrea faces supplier power risk: few suppliers, mandatory certification, rising fees, and limited switching options increase operating costs and regulatory exposure.

- ~12 accredited firms region-wide

- Audit fees +18% in 2024, €45–60k/project

- Certifications mandatory for licenses

- High switching costs and limited alternatives

Suppliers squeeze margins: 24–30m turbine backlogs, 10–18% premiums, rising capex

Suppliers hold high bargaining power: concentration in turbine, filter, and software vendors, plus 12 regional certifiers, caused 24–30 month turbine backlogs, 10–18% procurement premiums, 8–15% SaaS renewal uplifts, and audit fees up 18% (€45–60k) by 2024; labor shortages (8,000 deficit, 4.5% wage growth) add 5–12% capex risk.

| Metric | Value |

|---|---|

| Turbine backlog | 24–30 months |

| Procurement premium | 10–18% |

| SaaS renewal uplift | 8–15% |

| Audit fees | €45–60k (+18% 2024) |

| Labor shortfall (Sweden) | ~8,000 |

| Specialist wage growth | ~4.5% (2023–24) |

What is included in the product

Concise Porter's Five Forces analysis tailored for Infrea, uncovering competitive drivers, buyer/supplier leverage, entry barriers, substitutes, and emerging threats to inform strategic decisions and investor materials.

Infrea's Porter's Five Forces delivers a single-sheet, customizable SWOT-style view—quickly pinpoint competitive pressures and relieve decision-making friction for strategic planning.

Customers Bargaining Power

Municipal Procurement Power

Industrial Client Concentration

In recycling and renewable-energy lines, three industrial clients often supply over 60% of demand for comparable assets, so Infrea faces concentrated buyer power that pressures pricing and contract terms.

Large customers can demand price cuts or bespoke infrastructure, and in 2025 a lost contract worth 20% of an asset’s revenue could cut that asset’s EBITDA by roughly 12–18%.

Regulatory Price Caps and Oversight

Public Opinion and Political Pressure

As a provider of essential services, Infrea faces strong customer bargaining power channeled through public opinion and political actors; 2024 UK polling showed 68% oppose utility price rises, making regulators quick to act.

High visibility of tariffs means a 10%+ hike risks local government intervention or tariff freezes, so Infrea must balance margin targets with affordability to keep its social license.

- 68% public opposition to utility hikes (UK, 2024)

- 10%+ price rise often triggers political scrutiny

- Social license tied to affordability and visible service quality

Availability of Alternative Energy Solutions

Large commercial customers increasingly pursue self-generation—on-site solar and private microgrids—raising their bargaining power; global commercial solar capacity grew ~12% in 2024, and corporate PPAs hit a record 33 GW in 2023, showing a clear shift.

By threatening to cut dependence on Infrea’s centralized district heating or energy assets, customers can push for lower rates or flexible contracts; losing a 10% top-customer load could cut EBITDA by several points.

To retain customers, Infrea must offer value-added services—demand-response, resiliency guarantees, bundled energy-as-a-service—and prove superior reliability versus decentralized options, with targets like 99.99% uptime and integrated remote monitoring.

- Corporate on-site solar growth ~12% (2024)

- Corporate PPAs reached 33 GW (2023)

- Target reliability: 99.99% uptime

- Risk: 10% load loss → multi-point EBITDA hit

High municipal reliance and buyer concentration risk: losing contracts can cut EBITDA 12–18%

| Metric | Value |

|---|---|

| Municipal revenue share (2024) | 62% of SEK 1.1bn |

| Municipal contract margins (2023) | 6–8% |

| Industrial buyer concentration | >60% for some assets |

| Regulatory return caps (2024–25) | 3–5% real |

| Public opposition to hikes (UK, 2024) | 68% |

| Impact of lost contract | EBITDA −12–18% (10–20% revenue) |

Full Version Awaits

Infrea Porter's Five Forces Analysis

This preview shows the exact Infrea Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

You're looking at the full, professionally formatted document; once you buy, this identical file will be available for instant download and use.