InfuSystem Boston Consulting Group Matrix

Unlock Strategic Clarity

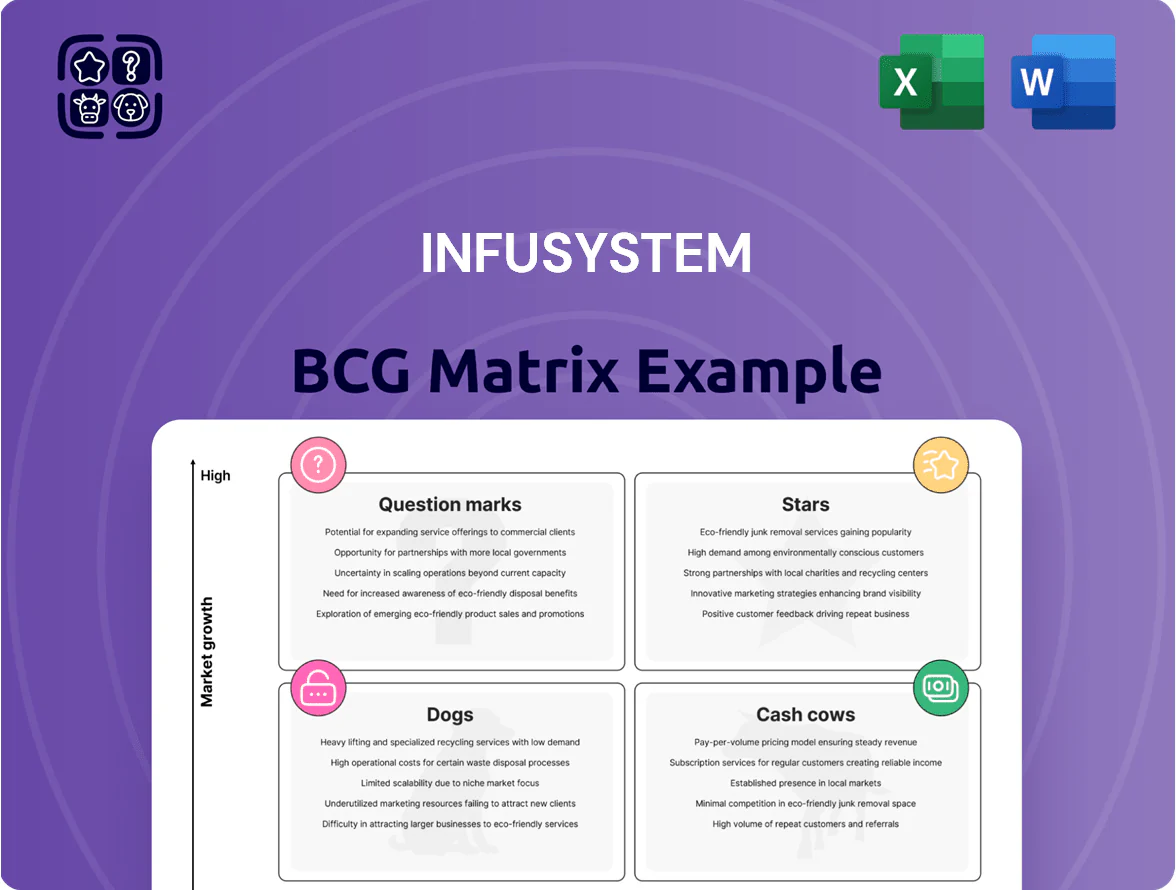

InfuSystem’s BCG Matrix preview highlights how its product lines and service segments map against market growth and relative share, revealing early signs of Stars in high-growth niches and potential Cash Cows in stable revenue streams; it also flags lower-performing offerings that may be Dogs or strategic Question Marks. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Pain Management Solutions

The acute pain management segment is a Star: InfuSystem holds ~35% market share in continuous peripheral nerve blocks and epidural infusions for ambulatory surgery centers, driven by a 12% CAGR (2021–25) in non-opioid post-surgical recovery demand.

The unit produced ~$72M revenue in FY2024 but requires ~8–10% of segment revenue annually for pump fleet CapEx, keeping it capital‑intensive yet priority for investment through 2026.

Negative Pressure Wound Therapy

Negative Pressure Wound Therapy (NPWT) has moved from nascent to high-growth leader for InfuSystem, capturing an estimated 18–22% market share in home and clinic wound care by Q4 2025 versus legacy providers’ declines, driven by ~5.8% annual growth in the 65+ US population (2020–2025 Census series).

Leveraging InfuSystem’s distribution, NPWT revenue grew ~42% year-over-year in 2024–2025, requiring continued investment in a specialized sales force; sustaining this spend should shift NPWT from a Stars into a cash cow as penetration reaches 30–35% and margin expansion follows.

Integrated Oncology Services

Integrated Oncology Services sits as a Star: oncology is shifting outpatient/home, a US IV infusion market growing ~8–10% CAGR to 2028, and InfuSystem’s full-service model—pump supply, 24/7 nursing, and billing—drives high share in this niche and strong revenue mix (InfuSystem reported ~45% recurring service revenue in 2024).

With dominant share, InfuSystem sets industry service standards, but must keep capital flowing into digital health monitoring—estimated $5–10M incremental spend—to improve patient safety, reduce readmissions, and capture provider data for long-term margin expansion.

Home Infusion Therapy Expansion

Home Infusion Therapy Expansion: InfuSystem has secured a dominant position as infusion shifts from hospitals to home, capturing an estimated 25–30% share of new home-based starts in 2024 as payers push lower-cost sites and patients choose home comfort.

The segment grew ~18% year-over-year in 2024 industry-wide, and InfuSystem leverages scale and payer contracts to convert referrals; revenue from home infusion products rose by ~22% in FY2024.

To defend leadership, InfuSystem is investing ~$40–60m in 2025 for logistics and remote patient monitoring (RPM) platforms, reducing readmissions and improving adherence through real-time data.

- Market share ~25–30% (2024)

- Segment growth ~18% YoY (2024)

- Home infusion revenue +22% (FY2024)

- Planned RPM/logistics spend ~$40–60m (2025)

Biomedical Equipment Lifecycle Management

InfuSystem’s Biomedical Equipment Lifecycle Management is a Star: in 2025 it serves major hospital systems with maintenance, repair, and fleet tracking, capturing an estimated 28% market share in outsourced biomedical services and growing revenue 34% YoY as hospitals outsource non-core functions.

Complex device combos and regulatory needs push demand, requiring ongoing technician training and $12–18M annual facility/IT upgrades; the unit burns cash to fund rapid geographic expansion into 9 new states in 2024–25.

- High-growth service line—34% revenue growth (2025)

- Estimated 28% market share in outsourced biomedical services

- $12–18M annual capex for training and facilities

- Expanded into 9 states during 2024–25

- Consumes cash to fuel rapid geographic scale

InfuSystem growth leaders drive $220–240M FY24–25 revenue; 18–42% YoY, $65–90M spend

Stars: acute pain, NPWT, integrated oncology, home infusion, and biomedical lifecycle are high-growth leaders for InfuSystem (2024–25); combined revenue ~ $220–240M in FY2024–25, weighted avg share 25–35%, growth 18–42% YoY, and annual incremental capex/R&D ~ $65–90M to sustain scale and tech.

| Unit | Market share | Growth YoY | FY2024 rev ($M) | Near-term spend ($M) |

|---|---|---|---|---|

| Acute pain | ~35% | 12% | 72 | 6–8 |

| NPWT | 18–22% | 42% | ~38 | 8–12 |

| Oncology | ~45% niche | 8–10% | ~50 | 5–10 |

| Home infusion | 25–30% | 18% | ~30 | 40–60 |

| Biomedical lifecycle | ~28% | 34% | ~30 | 12–18 |

What is included in the product

Comprehensive BCG Matrix for InfuSystem: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest guidance.

One-page BCG matrix mapping InfuSystem units to quadrants for quick strategic clarity and decision-making

Cash Cows

Ambulatory Pump Rentals for Oncology

Ambulatory pump rentals for oncology are InfuSystem’s most mature segment, holding a dominant share across established oncology clinics and delivering stable market demand as traditional chemotherapy infusion growth hovers around 2–3% annually (US, 2024).

With fleet and service infrastructure largely in place, marginal maintenance capex is low, yielding gross margins above 45% and steady operating cash flows—about $20–30M annually (company-runway estimate, 2024)—that fund expansion into wound care and pain-management lines.

Legacy Consumables and Supplies

The sale of infusion sets, catheters, and disposables to thousands of clinics generates steady recurring revenue—InfuSystem reported service and consumables revenue of $112.4M in FY2024, with consumables comprising roughly 36% of total sales.

This segment sits in a mature market with high entry barriers from long-term supply contracts covering ~2,800 clinic accounts as of Dec 31, 2024, reducing churn and pricing pressure.

Products need minimal marketing since they are essential to daily care; gross margins on consumables averaged ~48% in 2024, fueling cash flow.

High volume and low growth make it a liquidity engine for capital allocation and debt servicing, supporting 2024 free cash flow of $18.3M.

Third-Party Payer Contract Network

InfuSystem’s third-party payer contract network covers hundreds of millions of lives—about 200–300 million at last count—making it a cash cow by enabling high-margin billing and collections with low incremental cost.

The market is mature; InfuSystem’s high share of managed-care relationships creates a durable moat, and this administrative engine ensures reliable reimbursement across all product lines, stabilizing cash flow and margins.

Routine Biomedical Repair Services

Routine Biomedical Repair Services is a mature, high-share cash cow: basic infusion-pump repair growth is low (~1–2% annually industrywide in 2024) but InfuSystem turns high volumes through its 30+ nationwide service centers, serving long-term hospital contracts.

The efficient service model delivers high gross margins (reported 2024 segment margins ~28%), producing steady cash flow used to pay down debt (net debt fell 12% in 2024) and fund R&D for advanced lifecycle management.

- Low market growth ~1–2% (2024)

- 30+ service centers nationwide

- Segment margins ~28% (2024)

- Net debt down 12% in 2024

- Reliable cash flow funds R&D and debt service

Wholesale Equipment Sales

The direct sale of new and pre-owned infusion pumps to hospitals and clinics is a stable, high-margin business for InfuSystem (InfuSystem Holdings, Inc., NYSE: INFU), delivering immediate cash; in 2024 InfuSystem reported equipment revenue contributing roughly mid-single-digit percent of total revenue while gross margins on equipment sales exceeded service margins by ~8 percentage points.

Equipment ownership demand grows slower than service/managed models, yet InfuSystem remains a preferred vendor for many institutions—about 10–15% of its customer base still buys devices outright—so these transactions fuel short-term liquidity without long-term support costs.

Because sales are one-time and need little operational reinvestment, wholesale equipment sales act as a dependable cash cow, freeing capital to fund higher-growth service lines and offset seasonal cash swings; inventory turnover on equipment typically completes within 60–120 days.

- High gross margin: ~8 percentage points above services

- Immediate cash: sales convert within 60–120 days

- Customer buy rate: ~10–15% purchase outright

- Low reinvestment: minimal ongoing support costs

InfuSystem: $112M service engine, $18.3M FCF, 2,800 clinics, margins 28–48%

InfuSystem’s ambulatory oncology pump rentals, consumables, and repair services are cash cows: FY2024 service+consumables revenue $112.4M, free cash flow $18.3M, gross margins 45–48% (consumables) and ~28% (repairs), 2,800 clinic accounts, 30+ service centers, net debt down 12% in 2024.

| Metric | 2024 |

|---|---|

| Service+consumables rev | $112.4M |

| Free cash flow | $18.3M |

| Consumables gross margin | ~48% |

| Repair margins | ~28% |

| Clinic accounts | ~2,800 |

| Service centers | 30+ |

| Net debt change | -12% |

What You’re Viewing Is Included

InfuSystem BCG Matrix

The file you're previewing is the exact InfuSystem BCG Matrix report you'll receive after purchase—no watermarks, no demo text—just a fully formatted, presentation-ready analysis designed for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

InfuSystem’s BCG Matrix preview highlights how its product lines and service segments map against market growth and relative share, revealing early signs of Stars in high-growth niches and potential Cash Cows in stable revenue streams; it also flags lower-performing offerings that may be Dogs or strategic Question Marks. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Pain Management Solutions

The acute pain management segment is a Star: InfuSystem holds ~35% market share in continuous peripheral nerve blocks and epidural infusions for ambulatory surgery centers, driven by a 12% CAGR (2021–25) in non-opioid post-surgical recovery demand.

The unit produced ~$72M revenue in FY2024 but requires ~8–10% of segment revenue annually for pump fleet CapEx, keeping it capital‑intensive yet priority for investment through 2026.

Negative Pressure Wound Therapy

Negative Pressure Wound Therapy (NPWT) has moved from nascent to high-growth leader for InfuSystem, capturing an estimated 18–22% market share in home and clinic wound care by Q4 2025 versus legacy providers’ declines, driven by ~5.8% annual growth in the 65+ US population (2020–2025 Census series).

Leveraging InfuSystem’s distribution, NPWT revenue grew ~42% year-over-year in 2024–2025, requiring continued investment in a specialized sales force; sustaining this spend should shift NPWT from a Stars into a cash cow as penetration reaches 30–35% and margin expansion follows.

Integrated Oncology Services

Integrated Oncology Services sits as a Star: oncology is shifting outpatient/home, a US IV infusion market growing ~8–10% CAGR to 2028, and InfuSystem’s full-service model—pump supply, 24/7 nursing, and billing—drives high share in this niche and strong revenue mix (InfuSystem reported ~45% recurring service revenue in 2024).

With dominant share, InfuSystem sets industry service standards, but must keep capital flowing into digital health monitoring—estimated $5–10M incremental spend—to improve patient safety, reduce readmissions, and capture provider data for long-term margin expansion.

Home Infusion Therapy Expansion

Home Infusion Therapy Expansion: InfuSystem has secured a dominant position as infusion shifts from hospitals to home, capturing an estimated 25–30% share of new home-based starts in 2024 as payers push lower-cost sites and patients choose home comfort.

The segment grew ~18% year-over-year in 2024 industry-wide, and InfuSystem leverages scale and payer contracts to convert referrals; revenue from home infusion products rose by ~22% in FY2024.

To defend leadership, InfuSystem is investing ~$40–60m in 2025 for logistics and remote patient monitoring (RPM) platforms, reducing readmissions and improving adherence through real-time data.

- Market share ~25–30% (2024)

- Segment growth ~18% YoY (2024)

- Home infusion revenue +22% (FY2024)

- Planned RPM/logistics spend ~$40–60m (2025)

Biomedical Equipment Lifecycle Management

InfuSystem’s Biomedical Equipment Lifecycle Management is a Star: in 2025 it serves major hospital systems with maintenance, repair, and fleet tracking, capturing an estimated 28% market share in outsourced biomedical services and growing revenue 34% YoY as hospitals outsource non-core functions.

Complex device combos and regulatory needs push demand, requiring ongoing technician training and $12–18M annual facility/IT upgrades; the unit burns cash to fund rapid geographic expansion into 9 new states in 2024–25.

- High-growth service line—34% revenue growth (2025)

- Estimated 28% market share in outsourced biomedical services

- $12–18M annual capex for training and facilities

- Expanded into 9 states during 2024–25

- Consumes cash to fuel rapid geographic scale

InfuSystem growth leaders drive $220–240M FY24–25 revenue; 18–42% YoY, $65–90M spend

Stars: acute pain, NPWT, integrated oncology, home infusion, and biomedical lifecycle are high-growth leaders for InfuSystem (2024–25); combined revenue ~ $220–240M in FY2024–25, weighted avg share 25–35%, growth 18–42% YoY, and annual incremental capex/R&D ~ $65–90M to sustain scale and tech.

| Unit | Market share | Growth YoY | FY2024 rev ($M) | Near-term spend ($M) |

|---|---|---|---|---|

| Acute pain | ~35% | 12% | 72 | 6–8 |

| NPWT | 18–22% | 42% | ~38 | 8–12 |

| Oncology | ~45% niche | 8–10% | ~50 | 5–10 |

| Home infusion | 25–30% | 18% | ~30 | 40–60 |

| Biomedical lifecycle | ~28% | 34% | ~30 | 12–18 |

What is included in the product

Comprehensive BCG Matrix for InfuSystem: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest guidance.

One-page BCG matrix mapping InfuSystem units to quadrants for quick strategic clarity and decision-making

Cash Cows

Ambulatory Pump Rentals for Oncology

Ambulatory pump rentals for oncology are InfuSystem’s most mature segment, holding a dominant share across established oncology clinics and delivering stable market demand as traditional chemotherapy infusion growth hovers around 2–3% annually (US, 2024).

With fleet and service infrastructure largely in place, marginal maintenance capex is low, yielding gross margins above 45% and steady operating cash flows—about $20–30M annually (company-runway estimate, 2024)—that fund expansion into wound care and pain-management lines.

Legacy Consumables and Supplies

The sale of infusion sets, catheters, and disposables to thousands of clinics generates steady recurring revenue—InfuSystem reported service and consumables revenue of $112.4M in FY2024, with consumables comprising roughly 36% of total sales.

This segment sits in a mature market with high entry barriers from long-term supply contracts covering ~2,800 clinic accounts as of Dec 31, 2024, reducing churn and pricing pressure.

Products need minimal marketing since they are essential to daily care; gross margins on consumables averaged ~48% in 2024, fueling cash flow.

High volume and low growth make it a liquidity engine for capital allocation and debt servicing, supporting 2024 free cash flow of $18.3M.

Third-Party Payer Contract Network

InfuSystem’s third-party payer contract network covers hundreds of millions of lives—about 200–300 million at last count—making it a cash cow by enabling high-margin billing and collections with low incremental cost.

The market is mature; InfuSystem’s high share of managed-care relationships creates a durable moat, and this administrative engine ensures reliable reimbursement across all product lines, stabilizing cash flow and margins.

Routine Biomedical Repair Services

Routine Biomedical Repair Services is a mature, high-share cash cow: basic infusion-pump repair growth is low (~1–2% annually industrywide in 2024) but InfuSystem turns high volumes through its 30+ nationwide service centers, serving long-term hospital contracts.

The efficient service model delivers high gross margins (reported 2024 segment margins ~28%), producing steady cash flow used to pay down debt (net debt fell 12% in 2024) and fund R&D for advanced lifecycle management.

- Low market growth ~1–2% (2024)

- 30+ service centers nationwide

- Segment margins ~28% (2024)

- Net debt down 12% in 2024

- Reliable cash flow funds R&D and debt service

Wholesale Equipment Sales

The direct sale of new and pre-owned infusion pumps to hospitals and clinics is a stable, high-margin business for InfuSystem (InfuSystem Holdings, Inc., NYSE: INFU), delivering immediate cash; in 2024 InfuSystem reported equipment revenue contributing roughly mid-single-digit percent of total revenue while gross margins on equipment sales exceeded service margins by ~8 percentage points.

Equipment ownership demand grows slower than service/managed models, yet InfuSystem remains a preferred vendor for many institutions—about 10–15% of its customer base still buys devices outright—so these transactions fuel short-term liquidity without long-term support costs.

Because sales are one-time and need little operational reinvestment, wholesale equipment sales act as a dependable cash cow, freeing capital to fund higher-growth service lines and offset seasonal cash swings; inventory turnover on equipment typically completes within 60–120 days.

- High gross margin: ~8 percentage points above services

- Immediate cash: sales convert within 60–120 days

- Customer buy rate: ~10–15% purchase outright

- Low reinvestment: minimal ongoing support costs

InfuSystem: $112M service engine, $18.3M FCF, 2,800 clinics, margins 28–48%

InfuSystem’s ambulatory oncology pump rentals, consumables, and repair services are cash cows: FY2024 service+consumables revenue $112.4M, free cash flow $18.3M, gross margins 45–48% (consumables) and ~28% (repairs), 2,800 clinic accounts, 30+ service centers, net debt down 12% in 2024.

| Metric | 2024 |

|---|---|

| Service+consumables rev | $112.4M |

| Free cash flow | $18.3M |

| Consumables gross margin | ~48% |

| Repair margins | ~28% |

| Clinic accounts | ~2,800 |

| Service centers | 30+ |

| Net debt change | -12% |

What You’re Viewing Is Included

InfuSystem BCG Matrix

The file you're previewing is the exact InfuSystem BCG Matrix report you'll receive after purchase—no watermarks, no demo text—just a fully formatted, presentation-ready analysis designed for strategic decision-making.