Ingevity Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

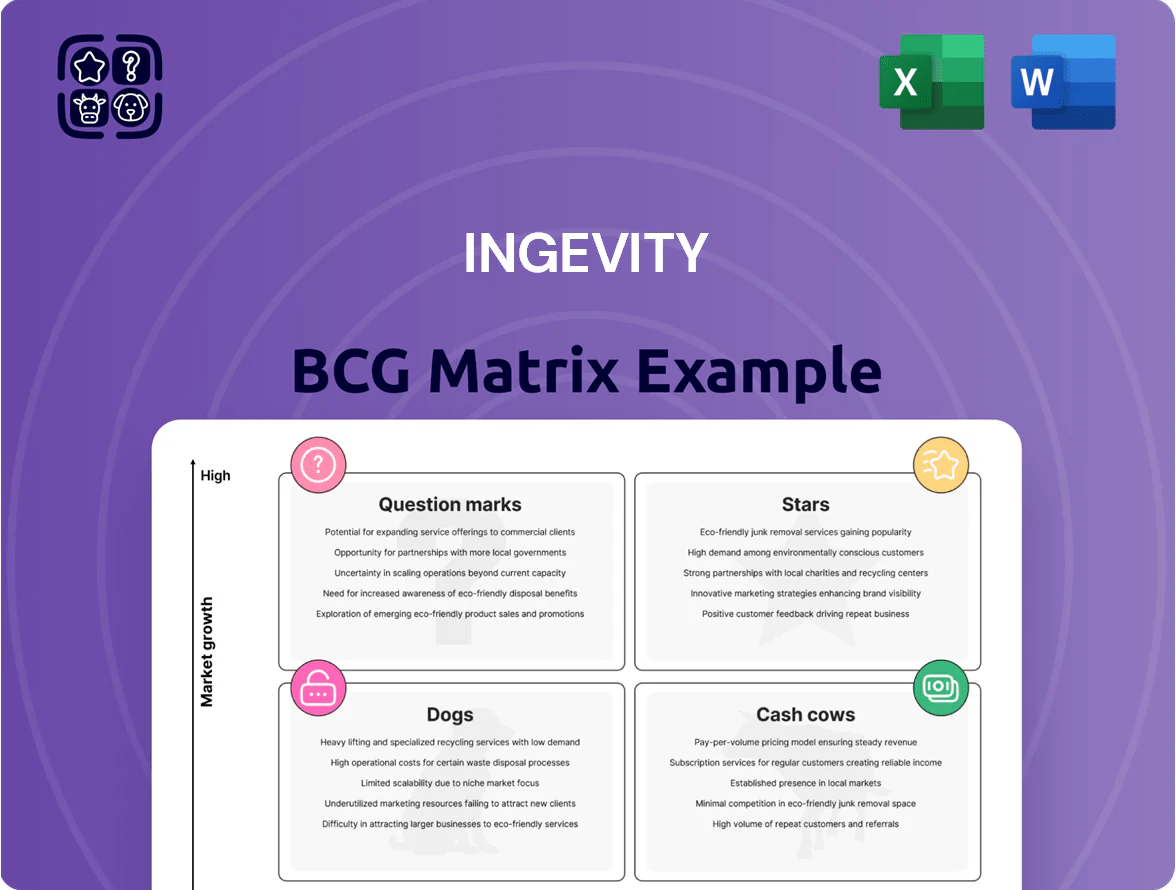

Ingevity’s BCG Matrix preview highlights how its product lines map across growth and market-share dimensions, revealing preliminary Stars, Cash Cows, Question Marks, and Dogs that shape strategic choices and capital allocation. This snapshot shows where the company earns steady cash, where it must invest to capture growth, and where divestment may be prudent. Dive deeper into the full BCG Matrix to get quadrant-by-quadrant data, actionable recommendations, and editable Word and Excel deliverables you can use to drive smarter investment and product decisions—purchase now.

Stars

Gasoline Emissions Control for Hybrids

Ingevity holds roughly 60–70% global market share in high-capacity activated carbon canisters for hybrid EVs, with segment revenues near $400m in 2024 and projected CAGR ~12% through 2028 as hybrid adoption rises to ~25% of new sales by 2025.

Stricter regs in US, EU, China push demand for higher-performance canisters; Ingevity’s R&D spend of about $30m in 2024 supports advanced sorbents and capacity scaling.

Maintaining leadership requires ongoing capex—estimated $50–80m over 2025–26—for new lines and product qualification as evaporative systems grow more complex.

Caprolactone for Sustainable Bioplastics

Caprolactone for Sustainable Bioplastics sits in Ingevity’s Stars quadrant: Capa polycaprolactone sales grew ~38% YoY in 2024 to ~$210M, driven by packaging and compostable goods amid 60+ national single-use plastic bans by end-2025.

Global demand forecasts show biodegradable polymers rising at a 17% CAGR to 2030; Ingevity’s lead market share (~22% in 2024) requires planned capex of $250–350M through 2027 to double production capacity and meet OEM contracts.

Advanced Adhesives for Electric Vehicles

Ingevity holds a dominant niche supplying polyols and resins for EV structural adhesives and battery thermal management, capturing an estimated 25–30% share of that specialty market as of 2025 and aligning with a global EV adhesives TAM growing ~18% CAGR to 2030.

These materials cut vehicle weight and improve battery safety—impacting range and thermal runaway risk—so revenue from this segment rose ~22% YoY in 2024, now ~ $120M annually.

To defend this high-share, high-growth position Ingevity must keep investing in application development and scale, or face margin pressure as larger chemical players target the space.

Performance Paving for Green Infrastructure

Evotherm, Ingevity’s warm-mix asphalt (WMA) tech, is a Star as 2024–25 public works target 20–30% lower CO2 on major road builds; Evotherm lowers paving temps ~30–50% and cuts energy use ~15–25%, keeping Ingevity top supplier in US federal/state projects.

Sustained marketing plus on-site technical support are needed to push Evotherm toward being the default spec in major contracts; sales growth 2023–24 showed mid-teens CAGR and margins beat core additives.

- Evotherm cuts paving temp 30–50%

- Energy savings ~15–25%

- 2023–24 sales mid-teens CAGR

- Targets 20–30% CO2 reduction in public works

- Requires continued marketing + field support

High-Performance Coatings for Renewable Energy

Specialty resins for protective coatings on wind turbines and solar arrays are a Stars segment for Ingevity, combining >20% CAGR demand in renewables coatings to 2026 with the company’s strong market share in durable chemistries.

Transition to renewables intensifying: global wind and solar capacity grew ~9% and 12% in 2024, driving >$200M revenue opportunity in coatings by 2026 for Ingevity’s technical resins.

Ongoing innovation needed to meet next-gen hardware specs—salt-spray, UV, and abrasion standards—so R&D spend must stay elevated to sustain growth and margins.

- High-growth (>20% CAGR) renewables coatings to 2026

- Estimated >$200M addressable revenue by 2026

- Requires continuous R&D on corrosion, UV, abrasion

- Strong market share in durable specialty resins

Ingevity's High‑Growth Portfolio: Canisters, PCL, Adhesives & Renewables Fueling Rapid Expansion

Ingevity’s Stars: activated-carbon EV canisters (~$400M, 60–70% share, CAGR ~12% to 2028), caprolactone PCL (~$210M in 2024, 38% YoY, 22% share, require $250–350M capex to 2027), EV adhesives (~$120M, 25–30% niche share, 18% TAM CAGR), Evotherm WMA (mid-teens CAGR, cuts temps 30–50%, energy −15–25%), renewables resins (>20% CAGR, >$200M opportunity by 2026)

| Segment | 2024 rev | share | CAGR/notes |

|---|---|---|---|

| Canisters | $400M | 60–70% | ~12% to 2028 |

| PCL | $210M | 22% | 38% YoY; capex $250–350M |

| Adhesives | $120M | 25–30% | 18% TAM CAGR |

| Evotherm | n/a | leading | mid‑teens CAGR; temp −30–50% |

| Renewables resins | >$200M (2026) | strong | >20% to 2026 |

What is included in the product

Comprehensive BCG Matrix review of Ingevity’s portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Ingevity BCG Matrix placing each business unit in a quadrant for clear strategic prioritization

Cash Cows

Automotive Carbon for Internal Combustion Engines

Ingevity controls roughly 40% of the global activated carbon market for gasoline vehicle emissions, delivering about $220 million in annual EBITDA from this ICE business in 2024.

The ICE segment is mature with low single-digit volume decline annually, yet margins remain strong and capital expenditure needs are minimal.

These steady cash flows funded 2024–25 R&D and capex of $140 million into sustainable adsorbents and battery materials.

Tall Oil Fatty Acid (TOFA) for Industrial Use

The Performance Chemicals segment sells Tall Oil Fatty Acid (TOFA) into mature industrial markets—lubricants, soaps—generating stable, high-margin cash in a low-growth sector; TOFA contributed about $110m in revenue and ~18% segment EBITDA margin in 2024.

As a kraft pulp byproduct, TOFA offers predictable volumes and low incremental cost, so Ingevity targets >90% plant uptime and incremental cost cuts (goal: $8–12/ton) to maximize free cash flow from this legacy stream.

Oilfield Chemicals for Conventional Drilling

Ingevity supplies chemical additives for conventional oil drilling, holding roughly 20%–25% share in North American drilling fluids as of 2025, keeping stable revenue of about $150M–$200M annually from this line.

Growth is limited by the 2019–2025 industry pivot to renewables, yet Ingevity’s long-term contracts and scale secure market dominance and predictable margins near 18% EBITDA.

Cash from this business funds debt service—Ingevity had $400M net debt at end-2024—and supports dividends and share buybacks, sending steady free cash flow to shareholders.

Inks and Coatings for Traditional Media

Ingevity’s resins for commercial printing and packaging inks sit in a mature, stable market where the company holds solid margins—segment EBITDA margins were ~18% in FY2024—driving predictable cash flow despite digital media trends.

Physical packaging demand stayed resilient: global packaging volumes rose ~2.5% in 2024, letting this unit run with low capital intensity and >ROIC vs WACC, funding R&D and higher-risk growth moves.

- Resins = mature market, ~18% EBITDA (FY2024)

- Packaging volumes +2.5% (2024)

- Low capex, high cash conversion

- Reliable funding source for growth/R&D

Pavement Preservation Chemicals

Ingevity’s pavement preservation chemicals, used for road maintenance and sealants, hold a dominant market share in a stable, low-growth segment—municipal spend drives predictable annual demand and contributed roughly $200–250M in recurring revenue in 2024.

These products require minimal promotion, yield steady cash flow with EBITDA margins near 20–25% in 2024, and management should prioritize sustaining production and supply reliability over expansion.

- High market share in municipal maintenance

- Stable, low-growth demand; ~$200–250M recurring revenue (2024)

- EBITDA margins ~20–25% (2024)

- Focus: maintain productivity and supply continuity

Ingevity’s steady cash cows fund R&D, debt paydown, dividends and buybacks

Ingevity’s cash cows—activated carbon for gasoline (≈40% share, $220M EBITDA 2024), TOFA ($110M revenue, ~18% EBITDA 2024), drilling fluids ($150–$200M revenue, ~18% EBITDA 2025), resins (~18% EBITDA 2024), and pavement chemicals ($200–$250M revenue, 20–25% EBITDA 2024)—generate steady, low‑capex free cash flow funding R&D, debt service ($400M net debt end‑2024), dividends, and buybacks.

| Business | 2024–25 | EBITDA% |

|---|---|---|

| Activated carbon | $220M EBITDA | — |

| TOFA | $110M rev | 18% |

| Drilling fluids | $150–$200M rev | 18% |

| Resins | — | 18% |

| Pavement | $200–$250M rev | 20–25% |

Delivered as Shown

Ingevity BCG Matrix

The file you're previewing is the exact Ingevity BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document. This preview matches the final downloadable file, crafted with market-backed insights and clear visuals for strategic decisions. Upon purchase you’ll get the same editable, printable report delivered instantly to your inbox—ready to present, share, or integrate into your planning without further edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Ingevity’s BCG Matrix preview highlights how its product lines map across growth and market-share dimensions, revealing preliminary Stars, Cash Cows, Question Marks, and Dogs that shape strategic choices and capital allocation. This snapshot shows where the company earns steady cash, where it must invest to capture growth, and where divestment may be prudent. Dive deeper into the full BCG Matrix to get quadrant-by-quadrant data, actionable recommendations, and editable Word and Excel deliverables you can use to drive smarter investment and product decisions—purchase now.

Stars

Gasoline Emissions Control for Hybrids

Ingevity holds roughly 60–70% global market share in high-capacity activated carbon canisters for hybrid EVs, with segment revenues near $400m in 2024 and projected CAGR ~12% through 2028 as hybrid adoption rises to ~25% of new sales by 2025.

Stricter regs in US, EU, China push demand for higher-performance canisters; Ingevity’s R&D spend of about $30m in 2024 supports advanced sorbents and capacity scaling.

Maintaining leadership requires ongoing capex—estimated $50–80m over 2025–26—for new lines and product qualification as evaporative systems grow more complex.

Caprolactone for Sustainable Bioplastics

Caprolactone for Sustainable Bioplastics sits in Ingevity’s Stars quadrant: Capa polycaprolactone sales grew ~38% YoY in 2024 to ~$210M, driven by packaging and compostable goods amid 60+ national single-use plastic bans by end-2025.

Global demand forecasts show biodegradable polymers rising at a 17% CAGR to 2030; Ingevity’s lead market share (~22% in 2024) requires planned capex of $250–350M through 2027 to double production capacity and meet OEM contracts.

Advanced Adhesives for Electric Vehicles

Ingevity holds a dominant niche supplying polyols and resins for EV structural adhesives and battery thermal management, capturing an estimated 25–30% share of that specialty market as of 2025 and aligning with a global EV adhesives TAM growing ~18% CAGR to 2030.

These materials cut vehicle weight and improve battery safety—impacting range and thermal runaway risk—so revenue from this segment rose ~22% YoY in 2024, now ~ $120M annually.

To defend this high-share, high-growth position Ingevity must keep investing in application development and scale, or face margin pressure as larger chemical players target the space.

Performance Paving for Green Infrastructure

Evotherm, Ingevity’s warm-mix asphalt (WMA) tech, is a Star as 2024–25 public works target 20–30% lower CO2 on major road builds; Evotherm lowers paving temps ~30–50% and cuts energy use ~15–25%, keeping Ingevity top supplier in US federal/state projects.

Sustained marketing plus on-site technical support are needed to push Evotherm toward being the default spec in major contracts; sales growth 2023–24 showed mid-teens CAGR and margins beat core additives.

- Evotherm cuts paving temp 30–50%

- Energy savings ~15–25%

- 2023–24 sales mid-teens CAGR

- Targets 20–30% CO2 reduction in public works

- Requires continued marketing + field support

High-Performance Coatings for Renewable Energy

Specialty resins for protective coatings on wind turbines and solar arrays are a Stars segment for Ingevity, combining >20% CAGR demand in renewables coatings to 2026 with the company’s strong market share in durable chemistries.

Transition to renewables intensifying: global wind and solar capacity grew ~9% and 12% in 2024, driving >$200M revenue opportunity in coatings by 2026 for Ingevity’s technical resins.

Ongoing innovation needed to meet next-gen hardware specs—salt-spray, UV, and abrasion standards—so R&D spend must stay elevated to sustain growth and margins.

- High-growth (>20% CAGR) renewables coatings to 2026

- Estimated >$200M addressable revenue by 2026

- Requires continuous R&D on corrosion, UV, abrasion

- Strong market share in durable specialty resins

Ingevity's High‑Growth Portfolio: Canisters, PCL, Adhesives & Renewables Fueling Rapid Expansion

Ingevity’s Stars: activated-carbon EV canisters (~$400M, 60–70% share, CAGR ~12% to 2028), caprolactone PCL (~$210M in 2024, 38% YoY, 22% share, require $250–350M capex to 2027), EV adhesives (~$120M, 25–30% niche share, 18% TAM CAGR), Evotherm WMA (mid-teens CAGR, cuts temps 30–50%, energy −15–25%), renewables resins (>20% CAGR, >$200M opportunity by 2026)

| Segment | 2024 rev | share | CAGR/notes |

|---|---|---|---|

| Canisters | $400M | 60–70% | ~12% to 2028 |

| PCL | $210M | 22% | 38% YoY; capex $250–350M |

| Adhesives | $120M | 25–30% | 18% TAM CAGR |

| Evotherm | n/a | leading | mid‑teens CAGR; temp −30–50% |

| Renewables resins | >$200M (2026) | strong | >20% to 2026 |

What is included in the product

Comprehensive BCG Matrix review of Ingevity’s portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Ingevity BCG Matrix placing each business unit in a quadrant for clear strategic prioritization

Cash Cows

Automotive Carbon for Internal Combustion Engines

Ingevity controls roughly 40% of the global activated carbon market for gasoline vehicle emissions, delivering about $220 million in annual EBITDA from this ICE business in 2024.

The ICE segment is mature with low single-digit volume decline annually, yet margins remain strong and capital expenditure needs are minimal.

These steady cash flows funded 2024–25 R&D and capex of $140 million into sustainable adsorbents and battery materials.

Tall Oil Fatty Acid (TOFA) for Industrial Use

The Performance Chemicals segment sells Tall Oil Fatty Acid (TOFA) into mature industrial markets—lubricants, soaps—generating stable, high-margin cash in a low-growth sector; TOFA contributed about $110m in revenue and ~18% segment EBITDA margin in 2024.

As a kraft pulp byproduct, TOFA offers predictable volumes and low incremental cost, so Ingevity targets >90% plant uptime and incremental cost cuts (goal: $8–12/ton) to maximize free cash flow from this legacy stream.

Oilfield Chemicals for Conventional Drilling

Ingevity supplies chemical additives for conventional oil drilling, holding roughly 20%–25% share in North American drilling fluids as of 2025, keeping stable revenue of about $150M–$200M annually from this line.

Growth is limited by the 2019–2025 industry pivot to renewables, yet Ingevity’s long-term contracts and scale secure market dominance and predictable margins near 18% EBITDA.

Cash from this business funds debt service—Ingevity had $400M net debt at end-2024—and supports dividends and share buybacks, sending steady free cash flow to shareholders.

Inks and Coatings for Traditional Media

Ingevity’s resins for commercial printing and packaging inks sit in a mature, stable market where the company holds solid margins—segment EBITDA margins were ~18% in FY2024—driving predictable cash flow despite digital media trends.

Physical packaging demand stayed resilient: global packaging volumes rose ~2.5% in 2024, letting this unit run with low capital intensity and >ROIC vs WACC, funding R&D and higher-risk growth moves.

- Resins = mature market, ~18% EBITDA (FY2024)

- Packaging volumes +2.5% (2024)

- Low capex, high cash conversion

- Reliable funding source for growth/R&D

Pavement Preservation Chemicals

Ingevity’s pavement preservation chemicals, used for road maintenance and sealants, hold a dominant market share in a stable, low-growth segment—municipal spend drives predictable annual demand and contributed roughly $200–250M in recurring revenue in 2024.

These products require minimal promotion, yield steady cash flow with EBITDA margins near 20–25% in 2024, and management should prioritize sustaining production and supply reliability over expansion.

- High market share in municipal maintenance

- Stable, low-growth demand; ~$200–250M recurring revenue (2024)

- EBITDA margins ~20–25% (2024)

- Focus: maintain productivity and supply continuity

Ingevity’s steady cash cows fund R&D, debt paydown, dividends and buybacks

Ingevity’s cash cows—activated carbon for gasoline (≈40% share, $220M EBITDA 2024), TOFA ($110M revenue, ~18% EBITDA 2024), drilling fluids ($150–$200M revenue, ~18% EBITDA 2025), resins (~18% EBITDA 2024), and pavement chemicals ($200–$250M revenue, 20–25% EBITDA 2024)—generate steady, low‑capex free cash flow funding R&D, debt service ($400M net debt end‑2024), dividends, and buybacks.

| Business | 2024–25 | EBITDA% |

|---|---|---|

| Activated carbon | $220M EBITDA | — |

| TOFA | $110M rev | 18% |

| Drilling fluids | $150–$200M rev | 18% |

| Resins | — | 18% |

| Pavement | $200–$250M rev | 20–25% |

Delivered as Shown

Ingevity BCG Matrix

The file you're previewing is the exact Ingevity BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document. This preview matches the final downloadable file, crafted with market-backed insights and clear visuals for strategic decisions. Upon purchase you’ll get the same editable, printable report delivered instantly to your inbox—ready to present, share, or integrate into your planning without further edits.