Ingram Industries Porter's Five Forces Analysis

Don't Miss the Bigger Picture

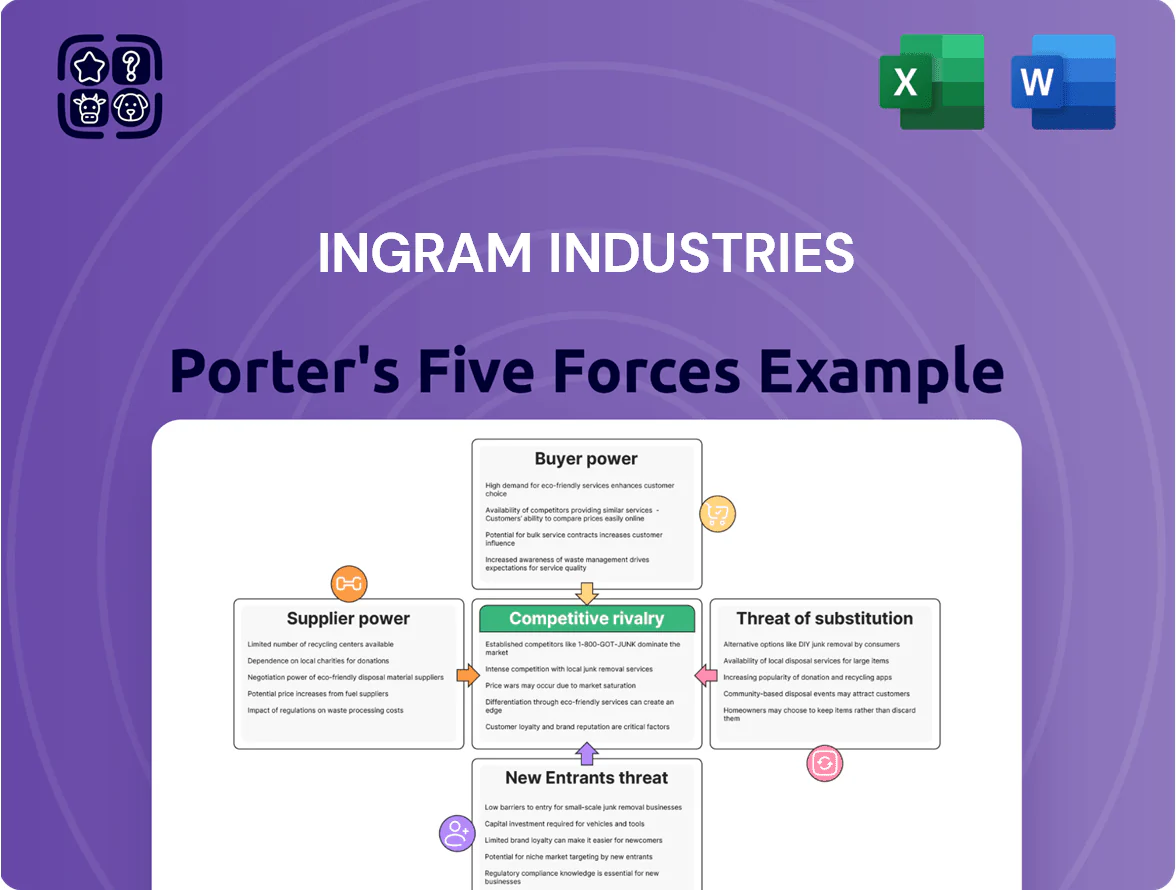

Ingram Industries faces moderate buyer power and significant rivalry amid capital-intensive logistics and marine sectors, while supplier leverage and regulatory hurdles shape strategic margins; substitutes and new entrants exert limited but growing pressure due to technology and sustainability trends. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Ingram Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Publishing Houses

The content distribution arm depends heavily on the Big Five publishers (Penguin Random House, HarperCollins, Simon & Schuster, Hachette, Macmillan), who together control roughly 70–80% of US trade book market share, giving them outsized leverage over Ingram’s catalog relevance.

Because bestseller titles drive retail traffic, these suppliers can dictate wholesale prices and return policies; Ingram faces margin pressure when publishers raise list prices or tighten discounts.

By late 2025 continued consolidation—several mega-deals since 2021—has increased publishers’ negotiating power, enabling tougher credit terms and price floors that can cut distributor gross margins by several hundred basis points.

Fuel and Energy Market Volatility

Ingram Marine Group is highly exposed to diesel and bunker fuel price swings set by global oil markets; bunker fuel averaged about $620/ton in 2024, raising barge operating costs by an estimated 8–12% year-over-year.

The fleet has limited fuel-switching options, so Ingram acts as a price taker and must pass or absorb costs, pressuring margins.

Oil volatility forced wider hedging: industry reports show 40–60% of fuel needs hedged in 2024 to stabilize cash flow.

Specialized Marine Equipment Manufacturers

The small pool of shipyards able to build high-quality inland barges and towboats gives suppliers strong bargaining power; about 60% of U.S. inland barge hulls in 2024 were built by three yards, concentrating leverage.

Persistent shortages for specialized marine-grade steel and diesel main engines through 2025 pushed lead times from 9–12 months to 14–20 months and raised new-build capex by ~18% versus 2020.

As a result, Ingram Industries faces constrained fleet growth: replacing a 10-vessel cohort could cost an extra $45–60m and take 12–24 months longer than pre-2020 norms, limiting rapid expansion.

Technological Infrastructure Vendors

Technological infrastructure vendors—specialized software developers and cloud providers—are critical to Ingram Industries’ digital asset management, underpinning Print-on-Demand and digital fulfillment operations.

These suppliers hold steady bargaining power because migrating large-scale databases risks multi-month downtime and costs often exceeding $10–30 million for enterprise migrations; cloud spend represented ~18% of Ingram’s digital ops budget in 2024.

- Critical backbone: software + cloud

- High switching cost: $10–30M migration

- Stable leverage: long-term SLAs common

- 2024: ~18% digital ops spend on cloud

Paper and Raw Material Suppliers

Paper pulp and specialty inks drive cost for Ingram’s Lightning Source; paper accounted for roughly 35–45% of unit COGS in trade book printing industry estimates in 2024, and pulp prices rose ~22% year-over-year through 2023–24.

Stricter EU and US environmental rules and China capacity shifts tightened supply, raising lead times and forcing Ingram to lock multi-year contracts and pay 3–6% premia for certified fibers to stay cost-competitive with offset printing.

Managing supplier concentration and vertical sourcing options is key to avoid margin erosion and maintain Lightning Source’s speed advantage.

- Paper = ~35–45% of printing COGS (2024 est.)

- Pulp prices +22% YoY (2023–24)

- 3–6% premium for certified fibers

- Multi-year contracts reduce lead-time risk

Supplier Concentration Squeezes Margins: Publishers, Pulp, Fuel & Shipyards Drive Costs

Suppliers exert high bargaining power: Big Five publishers control ~70–80% US trade share, paper/pulp = ~35–45% of printing COGS with pulp +22% YoY (2023–24), bunker fuel averaged $620/ton in 2024 (8–12% barge cost impact), and three shipyards built ~60% of inland hulls in 2024, forcing multi-year contracts, hedging, and margin pressure.

| Supplier | Key stat | Impact on Ingram |

|---|---|---|

| Big Five publishers | 70–80% US trade share | Price/terms leverage |

| Paper/pulp | 35–45% COGS; +22% YoY | Higher printing costs |

| Bunker fuel | $620/ton (2024) | 8–12% barge cost rise |

| Shipyards | 3 yards = ~60% hulls (2024) | Long lead times, capex up |

What is included in the product

Tailored exclusively for Ingram Industries, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats shaping its market position.

A concise Porter's Five Forces one-sheet for Ingram Industries—quickly highlights competitive threats and supplier/buyer leverage to speed strategic decisions.

Customers Bargaining Power

Retail Giant Dominance

Commodity Producer Leverage

Large industrial and agricultural shippers move millions of tons—US inland barge traffic was 654 million short tons in 2023—so these buyers extract strong leverage over Ingram Industries via long-term contracting and spot-pressure; top grain exporters and coal firms can demand sub-2% annual rate increases or shift to rail/truck if barge rates spike 15%+, and some consider vertical integration to secure capacity and cut transport spend.

Institutional Budget Constraints

Libraries and educational institutions, which buy heavily from Ingram Content Group, face tight government and donor budgets—US public library spending fell 2.3% in real terms 2020–2023, increasing price sensitivity and demand for discounts.

These buyers often join consortia; the Research Libraries UK consortium negotiated 15–25% savings in 2022, pressuring Ingram on margins.

Their move toward digital lending—US library e-lending rose ~40% 2019–2024—forces Ingram to adjust pricing for metered models and platform fees to retain institutional revenue.

Independent Bookstore Collective Power

Ingram must weigh higher servicing costs for fragmented accounts against preserving retail diversity that supports long-term title discovery and steady publisher demand.

- Independent stores: ~2,000 US locations (2024)

Direct-to-Consumer Shifts

- Direct sales 18% of US trade book revenue (2024)

- Direct-to-consumer rise increases distributor bypass options

- Ingram boosted analytics and metadata services

- Service revenue growth mid-single digits in 2023

Consolidation and DTC pressure squeeze distributors as Amazon, e-lending reshape books

| Metric | Value |

|---|---|

| Amazon share (2024) | 18–22% |

| Inland barge (2023) | 654M short tons |

| Ingram margin change | -140 bps (2021–2024) |

| Cost absorption (2023–2025) | 60–70% |

| Library e-lending growth | +40% (2019–2024) |

| Direct sales share (2024) | 18% |

Preview the Actual Deliverable

Ingram Industries Porter's Five Forces Analysis

This preview shows the exact Ingram Industries Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples.

The document displayed is the same professionally written, fully formatted file ready for download and use the moment you buy.

No mockups: what you’re previewing is the complete, ready-to-use deliverable available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Ingram Industries faces moderate buyer power and significant rivalry amid capital-intensive logistics and marine sectors, while supplier leverage and regulatory hurdles shape strategic margins; substitutes and new entrants exert limited but growing pressure due to technology and sustainability trends. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Ingram Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Publishing Houses

The content distribution arm depends heavily on the Big Five publishers (Penguin Random House, HarperCollins, Simon & Schuster, Hachette, Macmillan), who together control roughly 70–80% of US trade book market share, giving them outsized leverage over Ingram’s catalog relevance.

Because bestseller titles drive retail traffic, these suppliers can dictate wholesale prices and return policies; Ingram faces margin pressure when publishers raise list prices or tighten discounts.

By late 2025 continued consolidation—several mega-deals since 2021—has increased publishers’ negotiating power, enabling tougher credit terms and price floors that can cut distributor gross margins by several hundred basis points.

Fuel and Energy Market Volatility

Ingram Marine Group is highly exposed to diesel and bunker fuel price swings set by global oil markets; bunker fuel averaged about $620/ton in 2024, raising barge operating costs by an estimated 8–12% year-over-year.

The fleet has limited fuel-switching options, so Ingram acts as a price taker and must pass or absorb costs, pressuring margins.

Oil volatility forced wider hedging: industry reports show 40–60% of fuel needs hedged in 2024 to stabilize cash flow.

Specialized Marine Equipment Manufacturers

The small pool of shipyards able to build high-quality inland barges and towboats gives suppliers strong bargaining power; about 60% of U.S. inland barge hulls in 2024 were built by three yards, concentrating leverage.

Persistent shortages for specialized marine-grade steel and diesel main engines through 2025 pushed lead times from 9–12 months to 14–20 months and raised new-build capex by ~18% versus 2020.

As a result, Ingram Industries faces constrained fleet growth: replacing a 10-vessel cohort could cost an extra $45–60m and take 12–24 months longer than pre-2020 norms, limiting rapid expansion.

Technological Infrastructure Vendors

Technological infrastructure vendors—specialized software developers and cloud providers—are critical to Ingram Industries’ digital asset management, underpinning Print-on-Demand and digital fulfillment operations.

These suppliers hold steady bargaining power because migrating large-scale databases risks multi-month downtime and costs often exceeding $10–30 million for enterprise migrations; cloud spend represented ~18% of Ingram’s digital ops budget in 2024.

- Critical backbone: software + cloud

- High switching cost: $10–30M migration

- Stable leverage: long-term SLAs common

- 2024: ~18% digital ops spend on cloud

Paper and Raw Material Suppliers

Paper pulp and specialty inks drive cost for Ingram’s Lightning Source; paper accounted for roughly 35–45% of unit COGS in trade book printing industry estimates in 2024, and pulp prices rose ~22% year-over-year through 2023–24.

Stricter EU and US environmental rules and China capacity shifts tightened supply, raising lead times and forcing Ingram to lock multi-year contracts and pay 3–6% premia for certified fibers to stay cost-competitive with offset printing.

Managing supplier concentration and vertical sourcing options is key to avoid margin erosion and maintain Lightning Source’s speed advantage.

- Paper = ~35–45% of printing COGS (2024 est.)

- Pulp prices +22% YoY (2023–24)

- 3–6% premium for certified fibers

- Multi-year contracts reduce lead-time risk

Supplier Concentration Squeezes Margins: Publishers, Pulp, Fuel & Shipyards Drive Costs

Suppliers exert high bargaining power: Big Five publishers control ~70–80% US trade share, paper/pulp = ~35–45% of printing COGS with pulp +22% YoY (2023–24), bunker fuel averaged $620/ton in 2024 (8–12% barge cost impact), and three shipyards built ~60% of inland hulls in 2024, forcing multi-year contracts, hedging, and margin pressure.

| Supplier | Key stat | Impact on Ingram |

|---|---|---|

| Big Five publishers | 70–80% US trade share | Price/terms leverage |

| Paper/pulp | 35–45% COGS; +22% YoY | Higher printing costs |

| Bunker fuel | $620/ton (2024) | 8–12% barge cost rise |

| Shipyards | 3 yards = ~60% hulls (2024) | Long lead times, capex up |

What is included in the product

Tailored exclusively for Ingram Industries, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats shaping its market position.

A concise Porter's Five Forces one-sheet for Ingram Industries—quickly highlights competitive threats and supplier/buyer leverage to speed strategic decisions.

Customers Bargaining Power

Retail Giant Dominance

Commodity Producer Leverage

Large industrial and agricultural shippers move millions of tons—US inland barge traffic was 654 million short tons in 2023—so these buyers extract strong leverage over Ingram Industries via long-term contracting and spot-pressure; top grain exporters and coal firms can demand sub-2% annual rate increases or shift to rail/truck if barge rates spike 15%+, and some consider vertical integration to secure capacity and cut transport spend.

Institutional Budget Constraints

Libraries and educational institutions, which buy heavily from Ingram Content Group, face tight government and donor budgets—US public library spending fell 2.3% in real terms 2020–2023, increasing price sensitivity and demand for discounts.

These buyers often join consortia; the Research Libraries UK consortium negotiated 15–25% savings in 2022, pressuring Ingram on margins.

Their move toward digital lending—US library e-lending rose ~40% 2019–2024—forces Ingram to adjust pricing for metered models and platform fees to retain institutional revenue.

Independent Bookstore Collective Power

Ingram must weigh higher servicing costs for fragmented accounts against preserving retail diversity that supports long-term title discovery and steady publisher demand.

- Independent stores: ~2,000 US locations (2024)

Direct-to-Consumer Shifts

- Direct sales 18% of US trade book revenue (2024)

- Direct-to-consumer rise increases distributor bypass options

- Ingram boosted analytics and metadata services

- Service revenue growth mid-single digits in 2023

Consolidation and DTC pressure squeeze distributors as Amazon, e-lending reshape books

| Metric | Value |

|---|---|

| Amazon share (2024) | 18–22% |

| Inland barge (2023) | 654M short tons |

| Ingram margin change | -140 bps (2021–2024) |

| Cost absorption (2023–2025) | 60–70% |

| Library e-lending growth | +40% (2019–2024) |

| Direct sales share (2024) | 18% |

Preview the Actual Deliverable

Ingram Industries Porter's Five Forces Analysis

This preview shows the exact Ingram Industries Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples.

The document displayed is the same professionally written, fully formatted file ready for download and use the moment you buy.

No mockups: what you’re previewing is the complete, ready-to-use deliverable available instantly after payment.