Ingram Industries PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Ingram Industries faces a dynamic external landscape—from regulatory shifts in maritime and logistics policy to tech-led efficiency gains and rising ESG expectations—that could reshape its growth trajectory and risk profile; our concise PESTLE spotlights these drivers and their strategic implications. Purchase the full analysis for a detailed, ready-to-use brief that equips investors and strategists to act with confidence.

Political factors

U.S. Inland Waterway Infrastructure Funding

The federal commitment to locks and dams via the Inland Waterways Trust Fund, which held about $1.2 billion as of FY2024, is critical for Ingram Marine Group’s operations and fleet uptime.

Legislative implementation of the Infrastructure Investment and Jobs Act continues to fund barge-channel modernization through 2025, supporting projected transit efficiency gains of up to 10% on key corridors.

Political shifts in budget priorities risk delaying maintenance—FY2023 saw a 15% backlog increase—and such delays would reduce reliability of commodity transport and raise operating costs for Ingram.

Global Trade Policy and Tariffs

As a major transporter of agricultural products and dry bulk, Ingram Industries is sensitive to international trade agreements and retaliatory tariffs; U.S. ag exports fell 8% in 2024 vs 2023 amid trade frictions, reducing inland river tonnage and barge utilization rates.

Book Bans and Educational Censorship

Ingram Content Group faces rising state-level book ban laws—over 1,600 education-related restrictions proposed in 2023–2025 nationwide—forcing navigation of heterogeneous regulations while preserving neutrality as a distributor; these battles have already shifted procurement, with some districts reducing orders of contested titles by up to 22% and public library circulation declining 6% in affected counties, impacting Ingram’s K–12 and library sales segments.

Postal Service Reform and Subsidies

The financial strain on the U.S. Postal Service—FY2024 reported a $9.5 billion net loss—and proposals to raise USPS retail and commercial rates directly affect Ingram’s book distribution margins, where shipping can be 15–25% of unit cost. International postal restructurings and subsidies in key markets (EU transport subsidies ~€80bn in 2023) also shift cross-border fulfillment expenses. Ongoing political debates on USPS modernization or partial privatization could materially change contract terms and logistics pricing for Ingram.

- USPS FY2024 net loss $9.5B; potential rate hikes raise unit shipping costs

- Shipping = ~15–25% of physical book unit cost

- EU transport subsidies ~€80B (2023) affect international rates

- Privatization/modernization debates pose contractual/pricing risk

Maritime Labor and Union Regulations

- Labor costs ~18–22% of operating expenses (2024)

- Potential 5–12% cost impact from policy shifts

- Monitor NLRB/DOL appointments for regulatory risk

Public funding cushions river freight as trade, USPS losses and labor risks squeeze margins

Federal funding (Inland Waterways Trust Fund ~$1.2B FY2024) and IIJA modernization (through 2025) support Ingram Marine’s uptime, while budget shifts that raised maintenance backlogs 15% in FY2023 threaten efficiency; trade tensions cut U.S. ag exports 8% in 2024, lowering barge volumes; USPS FY2024 $9.5B loss and potential rate hikes raise book distribution costs (shipping = 15–25% of unit cost); labor policy/NLRB shifts could increase crew costs 5–12% (labor = 18–22% of towing OPEX 2024).

| Factor | Metric | 2023–2024 Data |

|---|---|---|

| Inland Waterways Fund | Balance | $1.2B (FY2024) |

| Maintenance backlog | Change | +15% (FY2023) |

| Ag exports | YoY change | -8% (2024 vs 2023) |

| USPS | Net loss | $9.5B (FY2024) |

| Shipping cost impact | % of unit cost | 15–25% |

| Labor | % of towing OPEX | 18–22% (2024) |

| Policy risk | Potential cost rise | +5–12% |

What is included in the product

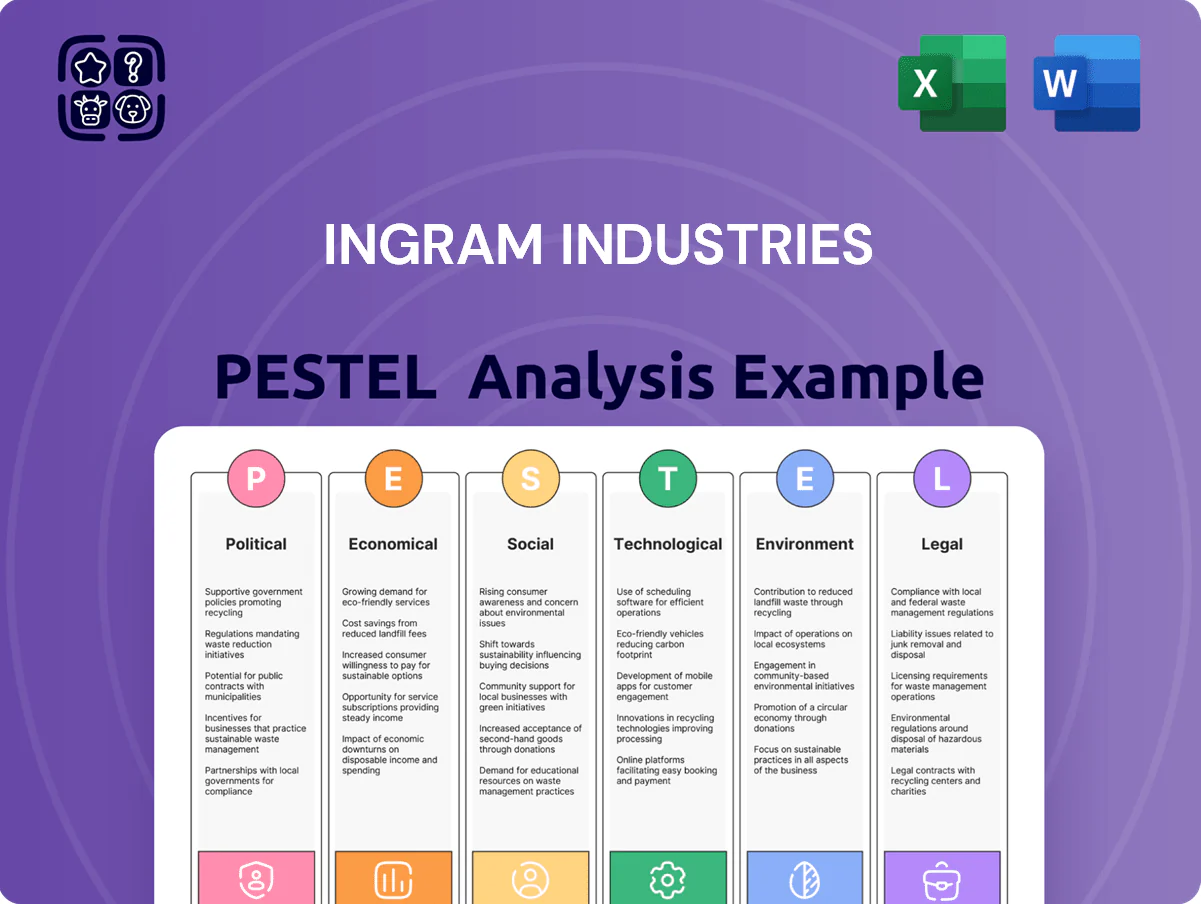

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Ingram Industries’ transport, distribution, and logistics operations, with data-backed trends and region-specific regulatory context.

A concise Ingram Industries PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations, and modifiable with notes to align teams and support strategic risk discussions.

Economic factors

Fluctuations in Commodity Prices

Demand for Ingram Industries' barge services closely tracks commodity prices for coal, grain and steel; U.S. grain exports rose 12% in 2024 to ~58 million tonnes, lifting inland barge utilization to ~84% and enabling higher charter rates.

By contrast, a 6% decline in U.S. construction spending in 2024 and weaker energy sector activity drove inland fleet overcapacity, pressuring spot rates and compressing revenue per barge.

Interest Rate Environment and Capital Expenditure

As a capital-intensive operator, Ingram's modernization of its river fleet and distribution centers depends on borrowing costs; US benchmark rates averaging 4.5–5.0% in 2024–2025 raise weighted-average cost of capital and increase annual interest expense on new debt by millions versus 2021 levels.

Prolonged high rates through 2025 can delay orders for next-gen vessels and automation projects as higher debt-service burdens compress free cash flow and extend payback periods.

Economic cycles also affect private equity availability—dry powder fell to about $1.2 trillion globally in 2024 from peak levels, tightening alternative financing for Ingram's large-scale investments.

Consumer Spending on Media and Books

Ingram Content Group's revenue is sensitive to discretionary spending; US consumer book sales fell 5.5% in 2023 to about $26.2 billion, pressuring physical retail and distribution volumes. Economic downturns drive readers toward digital formats and library borrowing—US library lending grew 8% in 2024—reducing unit print orders. Ingram must optimize its $1+ billion logistics footprint and inventory to hinge on variable print demand and rising digital distribution.

Fuel Price Volatility

Operating one of the largest U.S. barge fleets makes Ingram highly exposed to diesel and marine fuel; U.S. on-highway diesel averaged about 4.02 USD/gal in 2024, up 8% vs 2023, heightening operating cost risk for the marine segment.

Fuel surcharges offset some volatility—Ingram reported fuel recovery mechanisms covering roughly 60–80% of fuel-cost swings in recent contracts—but sudden spikes can compress margins until surcharges reset.

Instability in major oil-producing regions (e.g., 2024 OPEC+ supply adjustments) increases probability of short-term price shocks, complicating expense forecasting and cash-flow planning for the fleet.

- 2024 U.S. diesel avg 4.02 USD/gal (+8% vs 2023)

- Fuel recovery typically 60–80% of cost swings

- OPEC+ supply moves drive short-term price shock risk

E-commerce Growth and Logistics Costs

The rapid e-commerce surge—global online retail sales reached about $5.7 trillion in 2023 and grew ~8% in 2024—has intensified demand for warehouse labor and last-mile delivery, pushing US logistics wages up ~6–8% year-over-year and increasing fulfillment costs by an estimated 4–7% for distributors like Ingram.

Higher labor and fulfillment expenses compress margins in Ingram’s content distribution, forcing continuous supply-chain optimization to compete with Amazon and Walmart, which operate integrated logistics networks and account for over 40% of US e-commerce market share.

- Rising logistics wages: +6–8% (2024)

- Fulfillment cost increase: +4–7%

- Global e-commerce sales: ~$5.7T (2023)

- Amazon/Walmart share: >40% US e-commerce

Ingram: Strong 2024 grain boom lifts utilization & rates amid rising fuel, wages, rates

Economic swings drive Ingram: 2024 grain exports +12% to ~58Mt boosting barge utilization ~84% and charter rates, while 2024 construction spend -6% created fleet overcapacity; US diesel avg $4.02/gal (+8% vs 2023) with fuel recovery ~60–80%; borrowing costs (2024–25 rates 4.5–5.0%) raise WACC and delay capex; logistics wages +6–8% and fulfillment costs +4–7%.

| Metric | 2024 |

|---|---|

| Grain exports | ~58Mt (+12%) |

| Barge utilization | ~84% |

| Diesel | $4.02/gal (+8%) |

| Rates | 4.5–5.0% |

| Wages | +6–8% |

What You See Is What You Get

Ingram Industries PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Ingram Industries PESTLE analysis covers political, economic, social, technological, legal, and environmental factors with actionable insights and clear structure. No placeholders or teasers—what you see is the final, professional file available for immediate download after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Ingram Industries faces a dynamic external landscape—from regulatory shifts in maritime and logistics policy to tech-led efficiency gains and rising ESG expectations—that could reshape its growth trajectory and risk profile; our concise PESTLE spotlights these drivers and their strategic implications. Purchase the full analysis for a detailed, ready-to-use brief that equips investors and strategists to act with confidence.

Political factors

U.S. Inland Waterway Infrastructure Funding

The federal commitment to locks and dams via the Inland Waterways Trust Fund, which held about $1.2 billion as of FY2024, is critical for Ingram Marine Group’s operations and fleet uptime.

Legislative implementation of the Infrastructure Investment and Jobs Act continues to fund barge-channel modernization through 2025, supporting projected transit efficiency gains of up to 10% on key corridors.

Political shifts in budget priorities risk delaying maintenance—FY2023 saw a 15% backlog increase—and such delays would reduce reliability of commodity transport and raise operating costs for Ingram.

Global Trade Policy and Tariffs

As a major transporter of agricultural products and dry bulk, Ingram Industries is sensitive to international trade agreements and retaliatory tariffs; U.S. ag exports fell 8% in 2024 vs 2023 amid trade frictions, reducing inland river tonnage and barge utilization rates.

Book Bans and Educational Censorship

Ingram Content Group faces rising state-level book ban laws—over 1,600 education-related restrictions proposed in 2023–2025 nationwide—forcing navigation of heterogeneous regulations while preserving neutrality as a distributor; these battles have already shifted procurement, with some districts reducing orders of contested titles by up to 22% and public library circulation declining 6% in affected counties, impacting Ingram’s K–12 and library sales segments.

Postal Service Reform and Subsidies

The financial strain on the U.S. Postal Service—FY2024 reported a $9.5 billion net loss—and proposals to raise USPS retail and commercial rates directly affect Ingram’s book distribution margins, where shipping can be 15–25% of unit cost. International postal restructurings and subsidies in key markets (EU transport subsidies ~€80bn in 2023) also shift cross-border fulfillment expenses. Ongoing political debates on USPS modernization or partial privatization could materially change contract terms and logistics pricing for Ingram.

- USPS FY2024 net loss $9.5B; potential rate hikes raise unit shipping costs

- Shipping = ~15–25% of physical book unit cost

- EU transport subsidies ~€80B (2023) affect international rates

- Privatization/modernization debates pose contractual/pricing risk

Maritime Labor and Union Regulations

- Labor costs ~18–22% of operating expenses (2024)

- Potential 5–12% cost impact from policy shifts

- Monitor NLRB/DOL appointments for regulatory risk

Public funding cushions river freight as trade, USPS losses and labor risks squeeze margins

Federal funding (Inland Waterways Trust Fund ~$1.2B FY2024) and IIJA modernization (through 2025) support Ingram Marine’s uptime, while budget shifts that raised maintenance backlogs 15% in FY2023 threaten efficiency; trade tensions cut U.S. ag exports 8% in 2024, lowering barge volumes; USPS FY2024 $9.5B loss and potential rate hikes raise book distribution costs (shipping = 15–25% of unit cost); labor policy/NLRB shifts could increase crew costs 5–12% (labor = 18–22% of towing OPEX 2024).

| Factor | Metric | 2023–2024 Data |

|---|---|---|

| Inland Waterways Fund | Balance | $1.2B (FY2024) |

| Maintenance backlog | Change | +15% (FY2023) |

| Ag exports | YoY change | -8% (2024 vs 2023) |

| USPS | Net loss | $9.5B (FY2024) |

| Shipping cost impact | % of unit cost | 15–25% |

| Labor | % of towing OPEX | 18–22% (2024) |

| Policy risk | Potential cost rise | +5–12% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Ingram Industries’ transport, distribution, and logistics operations, with data-backed trends and region-specific regulatory context.

A concise Ingram Industries PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations, and modifiable with notes to align teams and support strategic risk discussions.

Economic factors

Fluctuations in Commodity Prices

Demand for Ingram Industries' barge services closely tracks commodity prices for coal, grain and steel; U.S. grain exports rose 12% in 2024 to ~58 million tonnes, lifting inland barge utilization to ~84% and enabling higher charter rates.

By contrast, a 6% decline in U.S. construction spending in 2024 and weaker energy sector activity drove inland fleet overcapacity, pressuring spot rates and compressing revenue per barge.

Interest Rate Environment and Capital Expenditure

As a capital-intensive operator, Ingram's modernization of its river fleet and distribution centers depends on borrowing costs; US benchmark rates averaging 4.5–5.0% in 2024–2025 raise weighted-average cost of capital and increase annual interest expense on new debt by millions versus 2021 levels.

Prolonged high rates through 2025 can delay orders for next-gen vessels and automation projects as higher debt-service burdens compress free cash flow and extend payback periods.

Economic cycles also affect private equity availability—dry powder fell to about $1.2 trillion globally in 2024 from peak levels, tightening alternative financing for Ingram's large-scale investments.

Consumer Spending on Media and Books

Ingram Content Group's revenue is sensitive to discretionary spending; US consumer book sales fell 5.5% in 2023 to about $26.2 billion, pressuring physical retail and distribution volumes. Economic downturns drive readers toward digital formats and library borrowing—US library lending grew 8% in 2024—reducing unit print orders. Ingram must optimize its $1+ billion logistics footprint and inventory to hinge on variable print demand and rising digital distribution.

Fuel Price Volatility

Operating one of the largest U.S. barge fleets makes Ingram highly exposed to diesel and marine fuel; U.S. on-highway diesel averaged about 4.02 USD/gal in 2024, up 8% vs 2023, heightening operating cost risk for the marine segment.

Fuel surcharges offset some volatility—Ingram reported fuel recovery mechanisms covering roughly 60–80% of fuel-cost swings in recent contracts—but sudden spikes can compress margins until surcharges reset.

Instability in major oil-producing regions (e.g., 2024 OPEC+ supply adjustments) increases probability of short-term price shocks, complicating expense forecasting and cash-flow planning for the fleet.

- 2024 U.S. diesel avg 4.02 USD/gal (+8% vs 2023)

- Fuel recovery typically 60–80% of cost swings

- OPEC+ supply moves drive short-term price shock risk

E-commerce Growth and Logistics Costs

The rapid e-commerce surge—global online retail sales reached about $5.7 trillion in 2023 and grew ~8% in 2024—has intensified demand for warehouse labor and last-mile delivery, pushing US logistics wages up ~6–8% year-over-year and increasing fulfillment costs by an estimated 4–7% for distributors like Ingram.

Higher labor and fulfillment expenses compress margins in Ingram’s content distribution, forcing continuous supply-chain optimization to compete with Amazon and Walmart, which operate integrated logistics networks and account for over 40% of US e-commerce market share.

- Rising logistics wages: +6–8% (2024)

- Fulfillment cost increase: +4–7%

- Global e-commerce sales: ~$5.7T (2023)

- Amazon/Walmart share: >40% US e-commerce

Ingram: Strong 2024 grain boom lifts utilization & rates amid rising fuel, wages, rates

Economic swings drive Ingram: 2024 grain exports +12% to ~58Mt boosting barge utilization ~84% and charter rates, while 2024 construction spend -6% created fleet overcapacity; US diesel avg $4.02/gal (+8% vs 2023) with fuel recovery ~60–80%; borrowing costs (2024–25 rates 4.5–5.0%) raise WACC and delay capex; logistics wages +6–8% and fulfillment costs +4–7%.

| Metric | 2024 |

|---|---|

| Grain exports | ~58Mt (+12%) |

| Barge utilization | ~84% |

| Diesel | $4.02/gal (+8%) |

| Rates | 4.5–5.0% |

| Wages | +6–8% |

What You See Is What You Get

Ingram Industries PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Ingram Industries PESTLE analysis covers political, economic, social, technological, legal, and environmental factors with actionable insights and clear structure. No placeholders or teasers—what you see is the final, professional file available for immediate download after payment.