Innolux Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

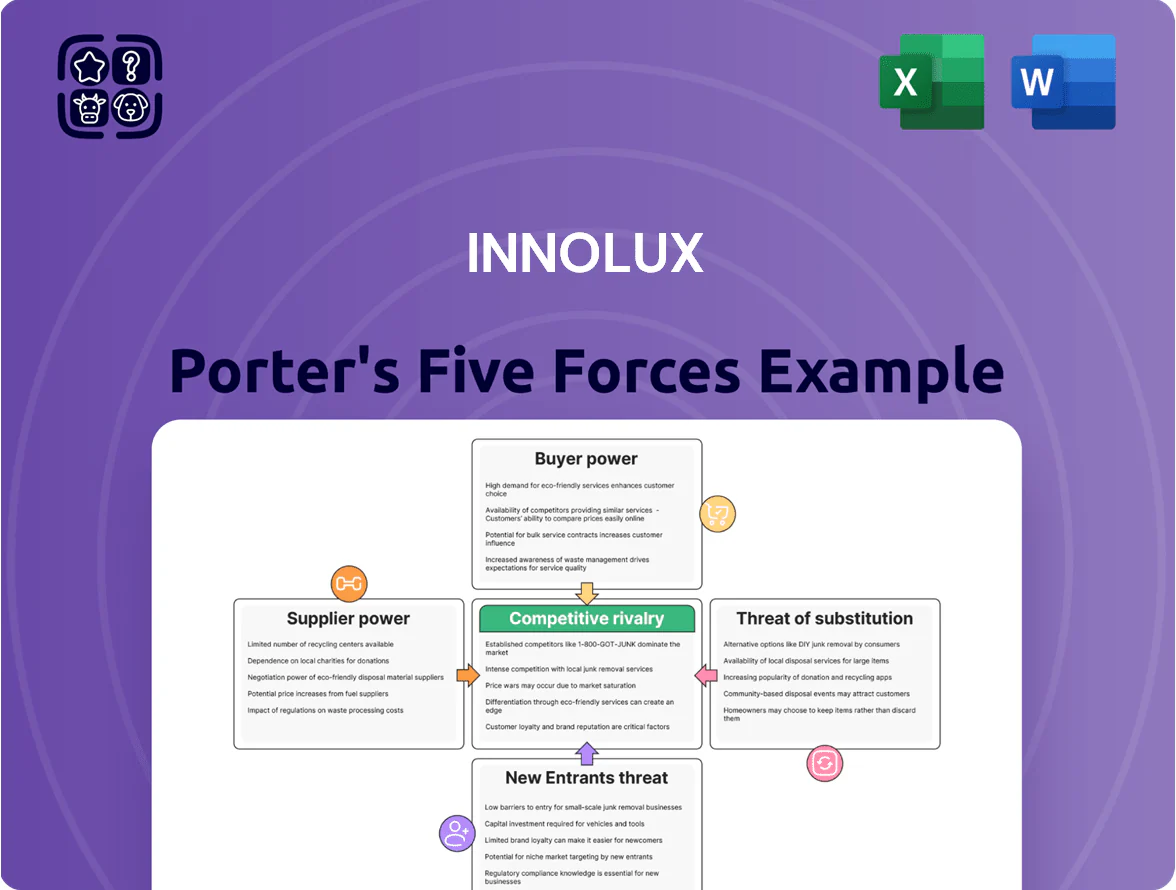

Innolux faces intense supplier leverage for key components, moderate buyer power amid OEM consolidation, and significant rivalry from LCD/OLED competitors and Chinese panel makers; barriers to entry are medium due to capital intensity but evolving tech, while substitutes (mini-LED, OLED) pose rising threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Innolux’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of glass substrate providers

The glass substrate market is highly concentrated: Corning, AGC (Asahi Glass), and NEG (Nippon Electric Glass) held roughly 70% of global supply in 2024, giving them strong leverage over Innolux.

They control critical quality specs and capacity, limiting Innolux’s ability to push prices down; raw glass accounts for about 15–20% of panel input costs.

Any production hiccup—Corning’s 2023 furnace outage cut supply by ~8%—can immediately bottleneck Innolux’s output and raise spot prices.

Limited sources for specialized driver ICs

Display driver ICs are critical and historically volatile: global driver IC shortages pushed fabs' lead times to 20–30 weeks in 2021–22 and spot prices rose 15–40% during silicon crunches, reducing panel makers' margins.

Innolux depends on specialized suppliers such as Novatek (market share ~25% of driver ICs in 2024) and Himax; these vendors can favor large clients or hike prices when capacity tightens, limiting Innolux’s bargaining room.

That supplier concentration constrains Innolux’s bill of materials control—if driver IC costs rise 10% it can cut gross margin by ~1–2 percentage points on typical LCD TV and monitor SKUs—and makes margin stability harder to guarantee.

High switching costs for production equipment

The specialized machinery for TFT-LCD fabrication is supplied by few global firms (e.g., Applied Materials, ASMPT, Tokyo Electron), so switching vendors can require >$200M in capex for new lines and 3–6 months of downtime for recalibration and retraining; this raises suppliers’ leverage on maintenance fees and upgrade pricing, seen in 2024 supplier-driven service revenues rising ~5–8% industry-wide.

Dependency on critical chemical and gas vendors

Manufacturing display panels needs high-purity chemicals, photoresists, and specialty gases that meet tight specs; in 2024 the global semiconductor-grade gas market was ~US$12.4B and top suppliers control >60% of supply, concentrating power.

Few certified vendors can reliably serve large fabs at scale, so suppliers push higher prices and long-term contracts; Innolux faces input-cost exposure—chemical spend can be 6–12% of COGS for advanced fabs.

- High-purity chemical market ~US$12.4B (2024)

- Top vendors >60% share

- Chemicals = 6–12% of fab COGS

- Risk: price hikes, supply lock-in

Vulnerability to energy and utility costs

Innolux runs energy-heavy fabs in Taiwan where state-linked utilities set rates; Taipower and regional water authorities act like near-monopolies, so Innolux has little bargaining room.

Rising electricity tariffs and a possible carbon tax boost COGS directly—Taipower raised rates ~7.5% in 2024 and Taiwan’s industrial power rate averages $0.12/kWh, so a 10% fuel cost rise can add materially to margins.

- Taipower quasi-monopoly limits rate negotiation

- Industrial power ~0.12 USD/kWh (2024)

- 2024 tariff hike ~7.5% increased COGS

- No viable supplier switching; carbon tax would further squeeze margins

High supplier concentration: glass, ICs & chemicals threaten margins with input shocks

Supplier power is high: glass makers Corning/AGC/NEG ~70% share (2024), driver-IC leaders Novatek/Himax ~25% each, high-purity chemicals market ~$12.4B with top vendors >60%, Taipower industrial rate ~$0.12/kWh (2024); input shocks (e.g., 2023 glass outage, 2021–22 IC lead times) can cut output and shave 1–2ppt gross margin.

| Item | 2024 stat |

|---|---|

| Glass suppliers | ~70% conc. |

| Driver ICs (Novatek) | ~25% mkt |

| Chemicals market | $12.4B; top >60% |

| Industrial power | $0.12/kWh; +7.5% tariff (2024) |

What is included in the product

Tailored exclusively for Innolux, this Porter's Five Forces analysis uncovers key competitive drivers, assesses supplier and buyer power, evaluates barriers to entry and substitution threats, and pinpoints disruptive forces and strategic vulnerabilities to inform investor and management decisions.

A concise Porter's Five Forces overview tailored for Innolux—quickly spot competitive pressures and pinpoint strategic levers to reduce supplier or buyer risks.

Customers Bargaining Power

High buyer concentration among global OEMs

A large share of Innolux’s sales comes from a handful of global OEMs; in 2024 about 58% of panel revenues were tied to top 5 customers, notably HP, Dell, and Lenovo, giving them strong volume leverage to push lower unit prices and extended payment terms.

Those buyers’ scale means losing one major contract could cut quarterly revenue by double digits—roughly 10–20%—and materially hurt margins and working capital.

Low switching costs for standardized products

Many consumer panels follow industry standards, so buyers can switch between Innolux, BOE, and LG Display on price or lead time; global LCD panel ASPs fell ~18% in 2024, raising price sensitivity.

Custom modules exist but are <5–10% of volumes, so low switching costs force Innolux into price competition to protect share, contributing to its 2024 gross margin of ~7–8%.

Threat of backward integration by tech giants

Major consumer electronics brands are moving to design displays in-house, cutting vendors out; Apple, for example, had $1.6B in MicroLED R&D by 2024 and aims to ship MicroLED devices by mid-2026, raising backward-integration risk for Innolux.

High price sensitivity in the consumer market

End-users for Innolux panels are highly price-sensitive: global TV ASPs fell about 6% in 2024 and smartphone average selling prices dropped 4% year-on-year, shifting demand to budget models.

Retailers and brand OEMs push cost cuts onto panel makers to protect margins in a crowded market; Innolux faced a 2024 gross margin squeeze, industry panel prices down ~8% from 2023.

Downturns amplify pressure—during 2023–2024 consumer electronics spending shifted toward low-end SKUs, increasing order volatility and forcing longer lead-time discounting.

- 2024 TV ASP −6%

- 2024 smartphone ASP −4%

- Industry panel prices −8% vs 2023

- Higher budget-SKU mix in 2023–24

Access to real-time market pricing data

Corporate buyers now use real-time panel price indices (e.g., AU Optronics index) and procurement platforms; 2024 average spot LCD panel price volatility was ±18% YoY, so buyers spot and reject above-market bids.

This transparency stops Innolux from using information gaps to keep margins; gross margin pressure showed a 2024 industry decline of ~220 basis points versus 2023.

Buyers cite these indices in contract talks to secure near-spot pricing; procurement teams reported saving 3–7% on panel costs in 2024 versus list prices.

- Real-time indices reduce price opacity

- 2024 panel price volatility ±18% YoY

- Industry gross margins fell ~220 bps in 2024

- Buyers saved 3–7% using market data

Buyers dominate: Top‑5 OEMs cut prices, margins fall 220bps; buyers saved 3–7% in 2024

Buyers hold strong power: top 5 OEMs drove ~58% of Innolux panel revenue in 2024, enabling price and payment demands; industry panel ASPs fell ~8% YoY and spot volatility was ±18%, cutting gross margins ~220 bps. Switchable, standardized panels and <5–10% custom volumes raise price sensitivity; buyer use of real‑time indices saved 3–7% in 2024.

| Metric | 2024 |

|---|---|

| Top‑5 revenue share | 58% |

| ASP change | −8% |

| Spot volatility | ±18% |

| Gross margin cng | −220 bps |

| Buyer savings | 3–7% |

Full Version Awaits

Innolux Porter's Five Forces Analysis

This preview shows the exact Innolux Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed is the same professionally written, fully formatted file ready for download and use the moment you buy.

No mockups: what you see is the complete, ready-to-use analysis available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Innolux faces intense supplier leverage for key components, moderate buyer power amid OEM consolidation, and significant rivalry from LCD/OLED competitors and Chinese panel makers; barriers to entry are medium due to capital intensity but evolving tech, while substitutes (mini-LED, OLED) pose rising threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Innolux’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of glass substrate providers

The glass substrate market is highly concentrated: Corning, AGC (Asahi Glass), and NEG (Nippon Electric Glass) held roughly 70% of global supply in 2024, giving them strong leverage over Innolux.

They control critical quality specs and capacity, limiting Innolux’s ability to push prices down; raw glass accounts for about 15–20% of panel input costs.

Any production hiccup—Corning’s 2023 furnace outage cut supply by ~8%—can immediately bottleneck Innolux’s output and raise spot prices.

Limited sources for specialized driver ICs

Display driver ICs are critical and historically volatile: global driver IC shortages pushed fabs' lead times to 20–30 weeks in 2021–22 and spot prices rose 15–40% during silicon crunches, reducing panel makers' margins.

Innolux depends on specialized suppliers such as Novatek (market share ~25% of driver ICs in 2024) and Himax; these vendors can favor large clients or hike prices when capacity tightens, limiting Innolux’s bargaining room.

That supplier concentration constrains Innolux’s bill of materials control—if driver IC costs rise 10% it can cut gross margin by ~1–2 percentage points on typical LCD TV and monitor SKUs—and makes margin stability harder to guarantee.

High switching costs for production equipment

The specialized machinery for TFT-LCD fabrication is supplied by few global firms (e.g., Applied Materials, ASMPT, Tokyo Electron), so switching vendors can require >$200M in capex for new lines and 3–6 months of downtime for recalibration and retraining; this raises suppliers’ leverage on maintenance fees and upgrade pricing, seen in 2024 supplier-driven service revenues rising ~5–8% industry-wide.

Dependency on critical chemical and gas vendors

Manufacturing display panels needs high-purity chemicals, photoresists, and specialty gases that meet tight specs; in 2024 the global semiconductor-grade gas market was ~US$12.4B and top suppliers control >60% of supply, concentrating power.

Few certified vendors can reliably serve large fabs at scale, so suppliers push higher prices and long-term contracts; Innolux faces input-cost exposure—chemical spend can be 6–12% of COGS for advanced fabs.

- High-purity chemical market ~US$12.4B (2024)

- Top vendors >60% share

- Chemicals = 6–12% of fab COGS

- Risk: price hikes, supply lock-in

Vulnerability to energy and utility costs

Innolux runs energy-heavy fabs in Taiwan where state-linked utilities set rates; Taipower and regional water authorities act like near-monopolies, so Innolux has little bargaining room.

Rising electricity tariffs and a possible carbon tax boost COGS directly—Taipower raised rates ~7.5% in 2024 and Taiwan’s industrial power rate averages $0.12/kWh, so a 10% fuel cost rise can add materially to margins.

- Taipower quasi-monopoly limits rate negotiation

- Industrial power ~0.12 USD/kWh (2024)

- 2024 tariff hike ~7.5% increased COGS

- No viable supplier switching; carbon tax would further squeeze margins

High supplier concentration: glass, ICs & chemicals threaten margins with input shocks

Supplier power is high: glass makers Corning/AGC/NEG ~70% share (2024), driver-IC leaders Novatek/Himax ~25% each, high-purity chemicals market ~$12.4B with top vendors >60%, Taipower industrial rate ~$0.12/kWh (2024); input shocks (e.g., 2023 glass outage, 2021–22 IC lead times) can cut output and shave 1–2ppt gross margin.

| Item | 2024 stat |

|---|---|

| Glass suppliers | ~70% conc. |

| Driver ICs (Novatek) | ~25% mkt |

| Chemicals market | $12.4B; top >60% |

| Industrial power | $0.12/kWh; +7.5% tariff (2024) |

What is included in the product

Tailored exclusively for Innolux, this Porter's Five Forces analysis uncovers key competitive drivers, assesses supplier and buyer power, evaluates barriers to entry and substitution threats, and pinpoints disruptive forces and strategic vulnerabilities to inform investor and management decisions.

A concise Porter's Five Forces overview tailored for Innolux—quickly spot competitive pressures and pinpoint strategic levers to reduce supplier or buyer risks.

Customers Bargaining Power

High buyer concentration among global OEMs

A large share of Innolux’s sales comes from a handful of global OEMs; in 2024 about 58% of panel revenues were tied to top 5 customers, notably HP, Dell, and Lenovo, giving them strong volume leverage to push lower unit prices and extended payment terms.

Those buyers’ scale means losing one major contract could cut quarterly revenue by double digits—roughly 10–20%—and materially hurt margins and working capital.

Low switching costs for standardized products

Many consumer panels follow industry standards, so buyers can switch between Innolux, BOE, and LG Display on price or lead time; global LCD panel ASPs fell ~18% in 2024, raising price sensitivity.

Custom modules exist but are <5–10% of volumes, so low switching costs force Innolux into price competition to protect share, contributing to its 2024 gross margin of ~7–8%.

Threat of backward integration by tech giants

Major consumer electronics brands are moving to design displays in-house, cutting vendors out; Apple, for example, had $1.6B in MicroLED R&D by 2024 and aims to ship MicroLED devices by mid-2026, raising backward-integration risk for Innolux.

High price sensitivity in the consumer market

End-users for Innolux panels are highly price-sensitive: global TV ASPs fell about 6% in 2024 and smartphone average selling prices dropped 4% year-on-year, shifting demand to budget models.

Retailers and brand OEMs push cost cuts onto panel makers to protect margins in a crowded market; Innolux faced a 2024 gross margin squeeze, industry panel prices down ~8% from 2023.

Downturns amplify pressure—during 2023–2024 consumer electronics spending shifted toward low-end SKUs, increasing order volatility and forcing longer lead-time discounting.

- 2024 TV ASP −6%

- 2024 smartphone ASP −4%

- Industry panel prices −8% vs 2023

- Higher budget-SKU mix in 2023–24

Access to real-time market pricing data

Corporate buyers now use real-time panel price indices (e.g., AU Optronics index) and procurement platforms; 2024 average spot LCD panel price volatility was ±18% YoY, so buyers spot and reject above-market bids.

This transparency stops Innolux from using information gaps to keep margins; gross margin pressure showed a 2024 industry decline of ~220 basis points versus 2023.

Buyers cite these indices in contract talks to secure near-spot pricing; procurement teams reported saving 3–7% on panel costs in 2024 versus list prices.

- Real-time indices reduce price opacity

- 2024 panel price volatility ±18% YoY

- Industry gross margins fell ~220 bps in 2024

- Buyers saved 3–7% using market data

Buyers dominate: Top‑5 OEMs cut prices, margins fall 220bps; buyers saved 3–7% in 2024

Buyers hold strong power: top 5 OEMs drove ~58% of Innolux panel revenue in 2024, enabling price and payment demands; industry panel ASPs fell ~8% YoY and spot volatility was ±18%, cutting gross margins ~220 bps. Switchable, standardized panels and <5–10% custom volumes raise price sensitivity; buyer use of real‑time indices saved 3–7% in 2024.

| Metric | 2024 |

|---|---|

| Top‑5 revenue share | 58% |

| ASP change | −8% |

| Spot volatility | ±18% |

| Gross margin cng | −220 bps |

| Buyer savings | 3–7% |

Full Version Awaits

Innolux Porter's Five Forces Analysis

This preview shows the exact Innolux Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed is the same professionally written, fully formatted file ready for download and use the moment you buy.

No mockups: what you see is the complete, ready-to-use analysis available instantly after payment.