Innolux PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our PESTLE Analysis of Innolux—concise yet powerful insights on political, economic, social, technological, legal, and environmental forces shaping the company’s future; perfect for investors and strategists seeking actionable intelligence. Download the full report for detailed risk assessments, opportunity maps, and ready-to-use slides to inform your next decision. Purchase now to access the complete analysis instantly.

Political factors

Geopolitical Cross-Strait Relations

The ongoing Taiwan–China tensions pose material risk to Innolux, which had 2024 revenue of NT$240.6 billion and operates fabs and assembly sites on both sides of the strait; sudden regulatory shifts or trade curbs could disrupt movement of glass substrates and finished panels, compressing 2024 gross margin (reported 12.8%) through higher logistics and inventory costs. Management must balance diplomatic sensitivities to protect assets and keep regional logistics intact, given that cross-strait shipments accounted for an estimated 18–22% of supply flows in 2023–24.

US-China Trade Restrictions

As a major supplier to global electronics brands, Innolux faces direct impact from US export controls on Chinese tech; in 2024 approximately 40% of its revenue was linked to customers exposed to these restrictions, forcing tighter compliance with US entity lists and hardware controls.

Although Taiwanese, Innolux’s China operations — over 60% of manufacturing capacity in 2023–24 — must adapt to evolving rules to preserve $3.5B+ in Western contracts.

Political pressure has led Innolux to reconfigure fabs and shift production to Taiwan and Southeast Asia to mitigate tariffs and maintain market access.

Taiwan Government Industrial Support

The Taiwanese government provided NT$48.3 billion in industrial subsidies to the display and semiconductor ecosystem in 2024, supporting R&D tax credits and grants that favor firms like Innolux; this funding accelerates development of MicroLED and semiconductor-packaging integration where Innolux reported R&D spending of NT$18.6 billion in 2024. Political shifts at local and national levels can alter budget allocations and infrastructure timelines, affecting the pace of cluster investments and competitive positioning versus Korean and Chinese rivals.

Global Supply Chain Diversification

Governments are allocating tens of billions to onshore electronics and semiconductor incentives; US CHIPS Act totals $280B (incl. $52B for semiconductors), EU announced €43B for chips—pressuring Innolux to diversify assembly beyond Greater China into India and Southeast Asia to reduce geopolitical concentration risk.

This shift is driven by national security and localization aims as countries seek domestic display and semiconductor ecosystems; Taiwan-sourced supply chain exposure remains a key political vulnerability for Innolux.

- US CHIPS Act overall funding: $280B (incl. $52B semiconductor incentives)

- EU chips investment: €43B announced

- Target diversification regions: India, Vietnam, Malaysia, Indonesia

International Trade Agreements

Taiwan's exclusion from major blocs like the CPTPP can raise tariffs for Innolux, which exported panels worth about US$6.2 billion in 2024, increasing unit costs versus competitors in CPTPP members.

Lack of formal diplomatic recognition complicates bilateral FTAs, potentially leaving Innolux with higher duties and reduced market access compared with rivals from China, Korea, or Japan.

Shifts in international trade policy—tariff changes or new trade deals—directly affect Innolux's competitiveness in emerging markets where duties can exceed 5–10% on display panels.

- 2024 exports US$6.2B; tariff exposure up to 10%

Innolux shifts capacity from China as geopolitics, subsidies and CHIPS funds reshape strategy

Taiwan–China tensions, US export controls and shifting trade policies materially risk Innolux’s cross-strait operations (2024 revenue NT$240.6B; gross margin 12.8%; exports US$6.2B), prompting capacity shifts to Taiwan/SE Asia (60% China capacity in 2023–24) and reliance on subsidies (Taiwan NT$48.3B; R&D NT$18.6B). Diversification driven by CHIPS/EU funds ($280B incl $52B; €43B) reduces geopolitical concentration.

| Metric | 2024 |

|---|---|

| Revenue | NT$240.6B |

| Gross margin | 12.8% |

| Exports | US$6.2B |

| R&D | NT$18.6B |

| Taiwan subsidies | NT$48.3B |

| China capacity | ~60% |

What is included in the product

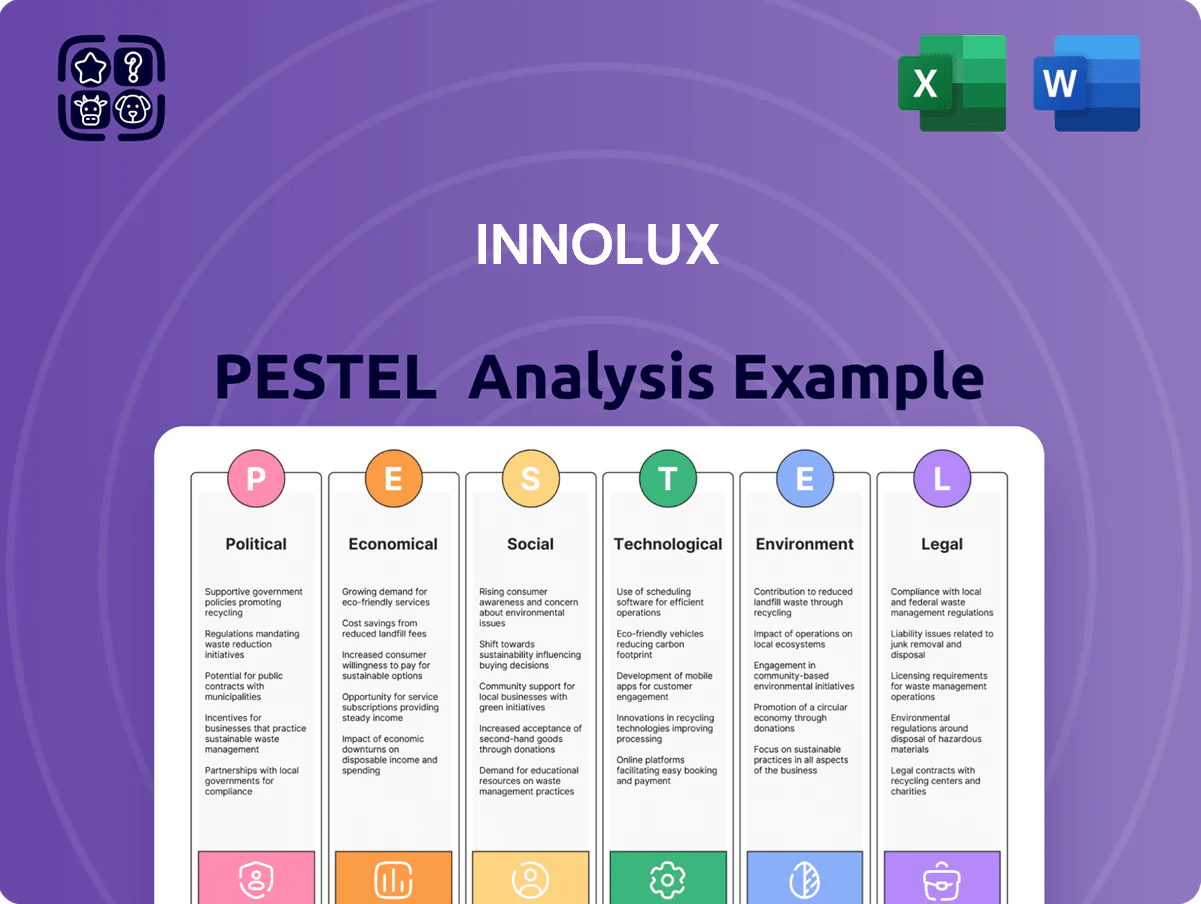

Explores how external macro-environmental factors uniquely affect Innolux across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities for executives, investors, and strategists.

Concise, PESTLE-segmented summary of Innolux’s external risks and opportunities that can be dropped into presentations or shared across teams for quick alignment during strategy and planning sessions.

Economic factors

Cyclical Nature of Panel Pricing

The display industry shows intense price volatility driven by crystal cycles of oversupply and demand swings, with LCD panel ASPs falling ~18% year-on-year in 2024 and spot prices dipping below manufacturing cost during 2H24.

Innolux must tightly manage capacity to avoid losses when panel prices tumble; the company cut utilization to ~75% in 2024 to limit negative margins.

Economic downturns in 2024–2025 pushed Innolux to prioritize high-value niches—automotive and industrial displays—which grew to ~22% of revenue in 2025, offsetting slim TV panel margins.

Global Consumer Purchasing Power

The demand for Innolux display modules closely tracks consumer disposable income; in 2024 household real disposable income in the US rose 1.8% while Eurozone incomes grew 0.6%, impacting purchases of smartphones, laptops and TVs.

Persistent inflation and higher rates—US CPI averaging 3.4% in 2024 and ECB policy rates near 3%—constrained discretionary spend, slowing premium display orders.

As global GDP growth stabilized to about 3.1% in 2025 and consumer electronics unit shipments rose ~4% late-2025, Innolux saw gradual recovery in premium module demand.

Currency Exchange Volatility

As a global exporter, Innolux is highly sensitive to TWD/USD and TWD/CNY swings; in 2024 the TWD moved about 2.8% vs USD and 4.1% vs CNY, amplifying translation risk given ~70% of revenue denominated in USD while significant costs remain in TWD and CNY.

The company employs forwards, options and natural hedges; hedging covered roughly 60–80% of forecasted FX exposure in 2024, but extreme moves—like a 5–10% TWD swing—can still cut operating margins materially.

Rising Raw Material and Energy Costs

Rising energy prices and constrained supply of rare gases like neon and krypton have increased Innolux’s COGS for LCD/OLED production; electricity accounts for roughly 20-30% of fab operating costs and neon/krypton spot prices spiked over 200% in 2021–2022, pressuring margins in 2024–25.

Innolux has invested in efficiency gains—reducing per-panel energy use by mid-single digits—and secured multi-year supply contracts, helping stabilize input costs and protect operating margins.

- Energy ≈20–30% of fab costs

- Neon/krypton prices surged >200% (2021–22)

- Innolux cut energy per panel mid-single digits

- Signed long-term supply contracts to smooth volatility

Growth in Automotive Display Market

The EV market grew 40% in 2023 to 16.5 million units global and is projected to exceed 30 million by 2026, boosting demand for automotive displays as vehicles digitize; Innolux stands to capture higher-value automotive panel orders with average ASPs 20–30% above TV panels.

Automotive panels yield longer lifecycles and higher margins—tiered margins around 10–15% vs 3–6% for TVs—offering revenue stability; Innolux shifted capex toward automotive, with R&D and capital spending for automotive rising to ~35% of total capex in 2024.

- Global EVs: 16.5M (2023), >30M by 2026 forecast

- Auto panel ASPs ~20–30% higher than TV

- Margins: automotive ~10–15% vs TV 3–6%

- Innolux automotive capex/R&D ~35% of total (2024)

Panel ASPs down 18% in 2024; Innolux pivots to auto—22% revenue in 2025

Panel ASPs fell ~18% YoY in 2024; Innolux cut utilization to ~75% and shifted to automotive/industrial (~22% revenue in 2025) to protect margins. US real disposable income +1.8% (2024); CPI US 3.4% (2024). TWD moved ~+2.8% vs USD (2024); hedging covered 60–80% exposure. Energy ≈20–30% fab costs; neon/krypton spiked >200% (2021–22); auto panels +20–30% ASPs, margins 10–15% vs TV 3–6%.

| Metric | Value |

|---|---|

| 2024 ASP change | -18% |

| Utilization 2024 | ~75% |

| Auto rev 2025 | ~22% |

| TWD vs USD (2024) | +2.8% |

Preview the Actual Deliverable

Innolux PESTLE Analysis

The preview shown here is the exact Innolux PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our PESTLE Analysis of Innolux—concise yet powerful insights on political, economic, social, technological, legal, and environmental forces shaping the company’s future; perfect for investors and strategists seeking actionable intelligence. Download the full report for detailed risk assessments, opportunity maps, and ready-to-use slides to inform your next decision. Purchase now to access the complete analysis instantly.

Political factors

Geopolitical Cross-Strait Relations

The ongoing Taiwan–China tensions pose material risk to Innolux, which had 2024 revenue of NT$240.6 billion and operates fabs and assembly sites on both sides of the strait; sudden regulatory shifts or trade curbs could disrupt movement of glass substrates and finished panels, compressing 2024 gross margin (reported 12.8%) through higher logistics and inventory costs. Management must balance diplomatic sensitivities to protect assets and keep regional logistics intact, given that cross-strait shipments accounted for an estimated 18–22% of supply flows in 2023–24.

US-China Trade Restrictions

As a major supplier to global electronics brands, Innolux faces direct impact from US export controls on Chinese tech; in 2024 approximately 40% of its revenue was linked to customers exposed to these restrictions, forcing tighter compliance with US entity lists and hardware controls.

Although Taiwanese, Innolux’s China operations — over 60% of manufacturing capacity in 2023–24 — must adapt to evolving rules to preserve $3.5B+ in Western contracts.

Political pressure has led Innolux to reconfigure fabs and shift production to Taiwan and Southeast Asia to mitigate tariffs and maintain market access.

Taiwan Government Industrial Support

The Taiwanese government provided NT$48.3 billion in industrial subsidies to the display and semiconductor ecosystem in 2024, supporting R&D tax credits and grants that favor firms like Innolux; this funding accelerates development of MicroLED and semiconductor-packaging integration where Innolux reported R&D spending of NT$18.6 billion in 2024. Political shifts at local and national levels can alter budget allocations and infrastructure timelines, affecting the pace of cluster investments and competitive positioning versus Korean and Chinese rivals.

Global Supply Chain Diversification

Governments are allocating tens of billions to onshore electronics and semiconductor incentives; US CHIPS Act totals $280B (incl. $52B for semiconductors), EU announced €43B for chips—pressuring Innolux to diversify assembly beyond Greater China into India and Southeast Asia to reduce geopolitical concentration risk.

This shift is driven by national security and localization aims as countries seek domestic display and semiconductor ecosystems; Taiwan-sourced supply chain exposure remains a key political vulnerability for Innolux.

- US CHIPS Act overall funding: $280B (incl. $52B semiconductor incentives)

- EU chips investment: €43B announced

- Target diversification regions: India, Vietnam, Malaysia, Indonesia

International Trade Agreements

Taiwan's exclusion from major blocs like the CPTPP can raise tariffs for Innolux, which exported panels worth about US$6.2 billion in 2024, increasing unit costs versus competitors in CPTPP members.

Lack of formal diplomatic recognition complicates bilateral FTAs, potentially leaving Innolux with higher duties and reduced market access compared with rivals from China, Korea, or Japan.

Shifts in international trade policy—tariff changes or new trade deals—directly affect Innolux's competitiveness in emerging markets where duties can exceed 5–10% on display panels.

- 2024 exports US$6.2B; tariff exposure up to 10%

Innolux shifts capacity from China as geopolitics, subsidies and CHIPS funds reshape strategy

Taiwan–China tensions, US export controls and shifting trade policies materially risk Innolux’s cross-strait operations (2024 revenue NT$240.6B; gross margin 12.8%; exports US$6.2B), prompting capacity shifts to Taiwan/SE Asia (60% China capacity in 2023–24) and reliance on subsidies (Taiwan NT$48.3B; R&D NT$18.6B). Diversification driven by CHIPS/EU funds ($280B incl $52B; €43B) reduces geopolitical concentration.

| Metric | 2024 |

|---|---|

| Revenue | NT$240.6B |

| Gross margin | 12.8% |

| Exports | US$6.2B |

| R&D | NT$18.6B |

| Taiwan subsidies | NT$48.3B |

| China capacity | ~60% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Innolux across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities for executives, investors, and strategists.

Concise, PESTLE-segmented summary of Innolux’s external risks and opportunities that can be dropped into presentations or shared across teams for quick alignment during strategy and planning sessions.

Economic factors

Cyclical Nature of Panel Pricing

The display industry shows intense price volatility driven by crystal cycles of oversupply and demand swings, with LCD panel ASPs falling ~18% year-on-year in 2024 and spot prices dipping below manufacturing cost during 2H24.

Innolux must tightly manage capacity to avoid losses when panel prices tumble; the company cut utilization to ~75% in 2024 to limit negative margins.

Economic downturns in 2024–2025 pushed Innolux to prioritize high-value niches—automotive and industrial displays—which grew to ~22% of revenue in 2025, offsetting slim TV panel margins.

Global Consumer Purchasing Power

The demand for Innolux display modules closely tracks consumer disposable income; in 2024 household real disposable income in the US rose 1.8% while Eurozone incomes grew 0.6%, impacting purchases of smartphones, laptops and TVs.

Persistent inflation and higher rates—US CPI averaging 3.4% in 2024 and ECB policy rates near 3%—constrained discretionary spend, slowing premium display orders.

As global GDP growth stabilized to about 3.1% in 2025 and consumer electronics unit shipments rose ~4% late-2025, Innolux saw gradual recovery in premium module demand.

Currency Exchange Volatility

As a global exporter, Innolux is highly sensitive to TWD/USD and TWD/CNY swings; in 2024 the TWD moved about 2.8% vs USD and 4.1% vs CNY, amplifying translation risk given ~70% of revenue denominated in USD while significant costs remain in TWD and CNY.

The company employs forwards, options and natural hedges; hedging covered roughly 60–80% of forecasted FX exposure in 2024, but extreme moves—like a 5–10% TWD swing—can still cut operating margins materially.

Rising Raw Material and Energy Costs

Rising energy prices and constrained supply of rare gases like neon and krypton have increased Innolux’s COGS for LCD/OLED production; electricity accounts for roughly 20-30% of fab operating costs and neon/krypton spot prices spiked over 200% in 2021–2022, pressuring margins in 2024–25.

Innolux has invested in efficiency gains—reducing per-panel energy use by mid-single digits—and secured multi-year supply contracts, helping stabilize input costs and protect operating margins.

- Energy ≈20–30% of fab costs

- Neon/krypton prices surged >200% (2021–22)

- Innolux cut energy per panel mid-single digits

- Signed long-term supply contracts to smooth volatility

Growth in Automotive Display Market

The EV market grew 40% in 2023 to 16.5 million units global and is projected to exceed 30 million by 2026, boosting demand for automotive displays as vehicles digitize; Innolux stands to capture higher-value automotive panel orders with average ASPs 20–30% above TV panels.

Automotive panels yield longer lifecycles and higher margins—tiered margins around 10–15% vs 3–6% for TVs—offering revenue stability; Innolux shifted capex toward automotive, with R&D and capital spending for automotive rising to ~35% of total capex in 2024.

- Global EVs: 16.5M (2023), >30M by 2026 forecast

- Auto panel ASPs ~20–30% higher than TV

- Margins: automotive ~10–15% vs TV 3–6%

- Innolux automotive capex/R&D ~35% of total (2024)

Panel ASPs down 18% in 2024; Innolux pivots to auto—22% revenue in 2025

Panel ASPs fell ~18% YoY in 2024; Innolux cut utilization to ~75% and shifted to automotive/industrial (~22% revenue in 2025) to protect margins. US real disposable income +1.8% (2024); CPI US 3.4% (2024). TWD moved ~+2.8% vs USD (2024); hedging covered 60–80% exposure. Energy ≈20–30% fab costs; neon/krypton spiked >200% (2021–22); auto panels +20–30% ASPs, margins 10–15% vs TV 3–6%.

| Metric | Value |

|---|---|

| 2024 ASP change | -18% |

| Utilization 2024 | ~75% |

| Auto rev 2025 | ~22% |

| TWD vs USD (2024) | +2.8% |

Preview the Actual Deliverable

Innolux PESTLE Analysis

The preview shown here is the exact Innolux PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.