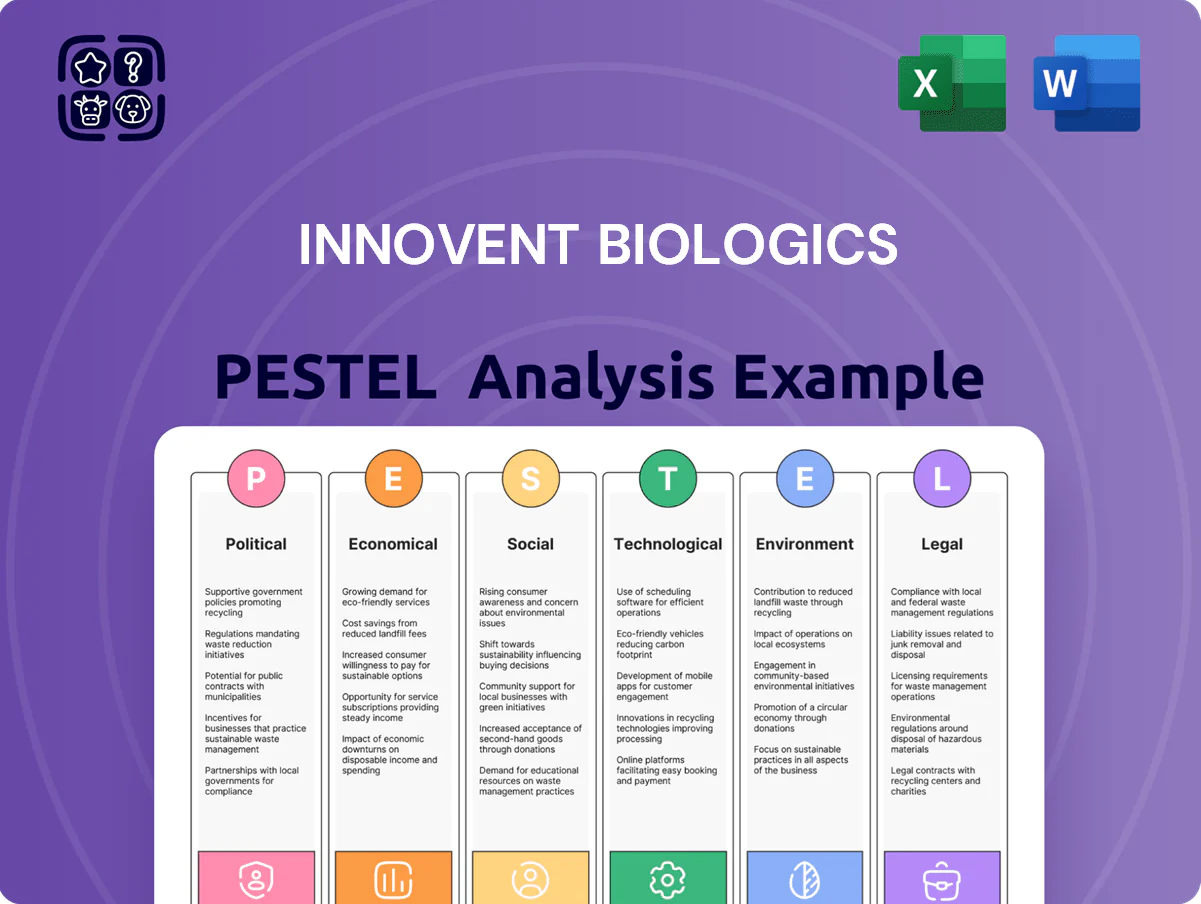

Innovent Biologics PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis pinpoints how regulatory shifts, pricing pressures, and rapid biotech innovation are shaping Innovent Biologics’ strategic outlook—essential reading for investors and strategists seeking actionable context. Purchase the full report to access detailed regulatory risk assessments, market forecasts, and technology trend implications you can deploy immediately.

Political factors

Geopolitical Trade Relations

The US-China tensions directly affect Innovent’s global expansion, with US biotech venture flow to China dropping 28% in 2024 and cross-border deals slowing; this pressures Innovent’s partnership pipeline and licensing prospects. Legislative moves such as the 2023 BIOSECURE Act tighten US scrutiny of Chinese biotech collaboration and export controls, impacting supply-chain access and clinical trial data sharing. To mitigate sudden regulatory shifts, Innovent must diversify markets—EMEA and ASEAN contributed 18% of its 2024 revenue—reducing reliance on any single jurisdiction.

Domestic Healthcare Reform

The Healthy China 2030 plan, targeting universal basic healthcare and a 65% increase in R&D funding by 2030, boosts Innovent’s market for innovative biologics, supporting pipeline translation into clinical adoption.

Centralized procurement and NRDL price negotiations have cut reimbursed biologic prices by up to 60% in recent rounds, pressuring margins on high-volume products sold domestically.

Innovent must align R&D and pricing strategies with state priorities—chronic disease, oncology, biosimilars—to secure NRDL inclusion and sustain revenue growth in China’s public health system.

Subsidies and Tax Incentives

Innovent benefits from Chinese government support—R&D tax credits and grants totaling over RMB 10 billion in biotech funding nationally in 2024—lowering costs of lengthy trials and enabling localization of biologics manufacturing such as its Suzhou facility expansion.

Global Regulatory Harmonization

As Innovent pursues FDA and EMA approvals, alignment between China NMPA and international regulators is crucial; in 2024 cross-border reliance pilot programs cut review times by up to 30% in some jurisdictions, potentially accelerating Innovent's market entry for biologics with global sales estimates in hundreds of millions USD per asset.

Political cooperation on data-sharing and mutual recognition could reduce redundant Phase III requirements, while rising protectionism—seen in 2023–24 trade restrictions—risks adding 12–24 months to approval timelines and delaying revenue recognition.

- Harmonization can shorten review timelines ~30%

- Protectionism may add 12–24 months to approvals

- Faster approvals could unlock >$100M/year per successful asset

Biosecurity and Data Sovereignty

New Chinese rules on human genetic resources and healthcare data force stricter consent, storage and cross-border transfer controls, raising compliance costs for Innovent estimated at >¥50m annually in recent sector reports (2024–25).

Heightened national biosecurity scrutiny requires security reviews for overseas collaborations; approvals can add months to timelines and risk delaying trials and licensing with partners like Eli Lilly and Sinopharm.

Innovent must adjust contracts, bolster data governance and legal teams to preserve its international R&D model while avoiding fines or project stoppages.

- Compliance costs >¥50m/year (industry 2024–25 estimates)

- Cross-border security reviews add months to project timelines

- Risk to partnerships and trial timelines with global pharma

- Need for stronger data governance and legal capacity

US-China biotech showdown: deal flow down 28%, prices cut 60%, compliance costs surge

US-China tensions cut US-to-China biotech venture flow 28% in 2024, slowing cross-border deals and pressuring Innovent’s licensing; NRDL price rounds trimmed reimbursed biologic prices up to 60%, squeezing margins; Healthy China 2030 and RMB 10bn+ biotech funding in 2024 boost R&D and market uptake; data/security rules and BIOSECURE-like laws raise compliance >¥50m/yr and may add 12–24 months to approvals.

| Metric | 2024–25 Value |

|---|---|

| US→China venture flow change | -28% |

| NRDL price cuts (max) | -60% |

| National biotech funding | RMB 10+ billion |

| Estimated compliance cost | ¥50m+/yr |

| Approval delay risk | +12–24 months |

What is included in the product

Explores how macro-environmental forces uniquely impact Innovent Biologics across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Innovent Biologics distilled for quick use in meetings or presentations, highlighting external risks and opportunities across political, economic, social, technological, legal, and environmental factors.

Economic factors

NRDL Pricing Pressures

Capital Market Volatility

As a Hong Kong Stock Exchange–listed biotech, Innovent is exposed to swings in global investor sentiment; the MSCI World Biotech index fell about 12% in 2024, pressuring sector valuations. Elevated policy rates—US Fed funds around 5.25%–5.50% in 2024—tightened venture capital and made follow-on offerings costlier, constraining funding for Innovent’s >40-program pipeline. Strong cash reserves and a credible path to profitability are critical to secure long-term institutional holders and reduce dilution risk.

R and D Investment Costs

Rising costs to develop novel biologics—average global R&D per successful biologic now exceeds $2.6bn—strain Innovent’s capital as oncology/metabolic programs demand larger, longer studies.

To curb a high burn rate (Innovent’s 2024 operating cash outflow was about RMB 3.1bn), prioritization of candidates with top commercial potential and strategic partnerships is essential.

Economic efficiency in trial management and selective use of CROs can cut timelines and costs; outsourced trials commonly reduce phase costs by 15–25%, improving ROIC on R&D spend.

Emerging Market Expansion

Innovent is expanding into emerging markets—driven by rising middle-class healthcare spending and demand for affordable biologics—targeting regions where biologics market CAGR often exceeds 8–12% (e.g., China/India LATAM growth); these markets offer volume upside but carry FX risk and uneven infrastructure that can affect launch speed and reimbursement.

Success hinges on flexible, locally tiered pricing tied to GDP per capita and payer mix; Innovent reported 2024 international revenue growth of ~20% year-on-year, underscoring early traction but exposure to currency volatility.

- High volume potential: EM biologics CAGR ~8–12%

- Risks: currency swings, uneven healthcare infrastructure

- Strategy: flexible, tiered pricing by GDP per capita and payer mix

- Signal: Innovent ~20% international revenue growth in 2024

Manufacturing Efficiency Gains

The transition from small-scale clinical production to large-scale commercial manufacturing is a major margin driver for Innovent, where scale can cut per-unit costs by an estimated 25–40% once plants operate at >70% capacity; commercial revenue from 2024–25 biologics ramp supports that shift.

Investments in stainless-steel bioreactors and continuous processes aim to lower unit costs for antibodies by leveraging higher yields and reduced downtime, targeting a 15–30% manufacturing cost reduction versus batch wet‑lab processing.

Lowering production costs is the primary competitiveness lever versus domestic biosimilars and global innovators; maintaining gross margins near peer median (40–50% for leading biologics players in 2024) depends on these efficiency gains.

- Scale economies: potential 25–40% per-unit cost cut at >70% capacity

- Technology uplift: 15–30% cost reduction from continuous/stainless-steel upgrades

- Margin target: sustain gross margins toward industry median 40–50% (2024)

Volume up, margins squeezed—2024 cuts, 25% COGS target, R&D & cash strain

2024 R&D 18% of revenue; operating cash outflow ~RMB 3.1bn; pipeline funding strained as biotech index fell ~12% in 2024 and Fed funds ~5.25–5.50% tightened capital.

EM expansion: ~20% international revenue growth in 2024; EM biologics CAGR 8–12%, but FX and infrastructure risks persist.

| Metric | 2024 |

|---|---|

| R&D % of rev | 18% |

| Op cash outflow | RMB 3.1bn |

| Intl rev growth | ~20% YoY |

| Biotech index | -12% |

| Fed funds | 5.25–5.50% |

Same Document Delivered

Innovent Biologics PESTLE Analysis

The preview shown here is the exact Innovent Biologics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis pinpoints how regulatory shifts, pricing pressures, and rapid biotech innovation are shaping Innovent Biologics’ strategic outlook—essential reading for investors and strategists seeking actionable context. Purchase the full report to access detailed regulatory risk assessments, market forecasts, and technology trend implications you can deploy immediately.

Political factors

Geopolitical Trade Relations

The US-China tensions directly affect Innovent’s global expansion, with US biotech venture flow to China dropping 28% in 2024 and cross-border deals slowing; this pressures Innovent’s partnership pipeline and licensing prospects. Legislative moves such as the 2023 BIOSECURE Act tighten US scrutiny of Chinese biotech collaboration and export controls, impacting supply-chain access and clinical trial data sharing. To mitigate sudden regulatory shifts, Innovent must diversify markets—EMEA and ASEAN contributed 18% of its 2024 revenue—reducing reliance on any single jurisdiction.

Domestic Healthcare Reform

The Healthy China 2030 plan, targeting universal basic healthcare and a 65% increase in R&D funding by 2030, boosts Innovent’s market for innovative biologics, supporting pipeline translation into clinical adoption.

Centralized procurement and NRDL price negotiations have cut reimbursed biologic prices by up to 60% in recent rounds, pressuring margins on high-volume products sold domestically.

Innovent must align R&D and pricing strategies with state priorities—chronic disease, oncology, biosimilars—to secure NRDL inclusion and sustain revenue growth in China’s public health system.

Subsidies and Tax Incentives

Innovent benefits from Chinese government support—R&D tax credits and grants totaling over RMB 10 billion in biotech funding nationally in 2024—lowering costs of lengthy trials and enabling localization of biologics manufacturing such as its Suzhou facility expansion.

Global Regulatory Harmonization

As Innovent pursues FDA and EMA approvals, alignment between China NMPA and international regulators is crucial; in 2024 cross-border reliance pilot programs cut review times by up to 30% in some jurisdictions, potentially accelerating Innovent's market entry for biologics with global sales estimates in hundreds of millions USD per asset.

Political cooperation on data-sharing and mutual recognition could reduce redundant Phase III requirements, while rising protectionism—seen in 2023–24 trade restrictions—risks adding 12–24 months to approval timelines and delaying revenue recognition.

- Harmonization can shorten review timelines ~30%

- Protectionism may add 12–24 months to approvals

- Faster approvals could unlock >$100M/year per successful asset

Biosecurity and Data Sovereignty

New Chinese rules on human genetic resources and healthcare data force stricter consent, storage and cross-border transfer controls, raising compliance costs for Innovent estimated at >¥50m annually in recent sector reports (2024–25).

Heightened national biosecurity scrutiny requires security reviews for overseas collaborations; approvals can add months to timelines and risk delaying trials and licensing with partners like Eli Lilly and Sinopharm.

Innovent must adjust contracts, bolster data governance and legal teams to preserve its international R&D model while avoiding fines or project stoppages.

- Compliance costs >¥50m/year (industry 2024–25 estimates)

- Cross-border security reviews add months to project timelines

- Risk to partnerships and trial timelines with global pharma

- Need for stronger data governance and legal capacity

US-China biotech showdown: deal flow down 28%, prices cut 60%, compliance costs surge

US-China tensions cut US-to-China biotech venture flow 28% in 2024, slowing cross-border deals and pressuring Innovent’s licensing; NRDL price rounds trimmed reimbursed biologic prices up to 60%, squeezing margins; Healthy China 2030 and RMB 10bn+ biotech funding in 2024 boost R&D and market uptake; data/security rules and BIOSECURE-like laws raise compliance >¥50m/yr and may add 12–24 months to approvals.

| Metric | 2024–25 Value |

|---|---|

| US→China venture flow change | -28% |

| NRDL price cuts (max) | -60% |

| National biotech funding | RMB 10+ billion |

| Estimated compliance cost | ¥50m+/yr |

| Approval delay risk | +12–24 months |

What is included in the product

Explores how macro-environmental forces uniquely impact Innovent Biologics across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Innovent Biologics distilled for quick use in meetings or presentations, highlighting external risks and opportunities across political, economic, social, technological, legal, and environmental factors.

Economic factors

NRDL Pricing Pressures

Capital Market Volatility

As a Hong Kong Stock Exchange–listed biotech, Innovent is exposed to swings in global investor sentiment; the MSCI World Biotech index fell about 12% in 2024, pressuring sector valuations. Elevated policy rates—US Fed funds around 5.25%–5.50% in 2024—tightened venture capital and made follow-on offerings costlier, constraining funding for Innovent’s >40-program pipeline. Strong cash reserves and a credible path to profitability are critical to secure long-term institutional holders and reduce dilution risk.

R and D Investment Costs

Rising costs to develop novel biologics—average global R&D per successful biologic now exceeds $2.6bn—strain Innovent’s capital as oncology/metabolic programs demand larger, longer studies.

To curb a high burn rate (Innovent’s 2024 operating cash outflow was about RMB 3.1bn), prioritization of candidates with top commercial potential and strategic partnerships is essential.

Economic efficiency in trial management and selective use of CROs can cut timelines and costs; outsourced trials commonly reduce phase costs by 15–25%, improving ROIC on R&D spend.

Emerging Market Expansion

Innovent is expanding into emerging markets—driven by rising middle-class healthcare spending and demand for affordable biologics—targeting regions where biologics market CAGR often exceeds 8–12% (e.g., China/India LATAM growth); these markets offer volume upside but carry FX risk and uneven infrastructure that can affect launch speed and reimbursement.

Success hinges on flexible, locally tiered pricing tied to GDP per capita and payer mix; Innovent reported 2024 international revenue growth of ~20% year-on-year, underscoring early traction but exposure to currency volatility.

- High volume potential: EM biologics CAGR ~8–12%

- Risks: currency swings, uneven healthcare infrastructure

- Strategy: flexible, tiered pricing by GDP per capita and payer mix

- Signal: Innovent ~20% international revenue growth in 2024

Manufacturing Efficiency Gains

The transition from small-scale clinical production to large-scale commercial manufacturing is a major margin driver for Innovent, where scale can cut per-unit costs by an estimated 25–40% once plants operate at >70% capacity; commercial revenue from 2024–25 biologics ramp supports that shift.

Investments in stainless-steel bioreactors and continuous processes aim to lower unit costs for antibodies by leveraging higher yields and reduced downtime, targeting a 15–30% manufacturing cost reduction versus batch wet‑lab processing.

Lowering production costs is the primary competitiveness lever versus domestic biosimilars and global innovators; maintaining gross margins near peer median (40–50% for leading biologics players in 2024) depends on these efficiency gains.

- Scale economies: potential 25–40% per-unit cost cut at >70% capacity

- Technology uplift: 15–30% cost reduction from continuous/stainless-steel upgrades

- Margin target: sustain gross margins toward industry median 40–50% (2024)

Volume up, margins squeezed—2024 cuts, 25% COGS target, R&D & cash strain

2024 R&D 18% of revenue; operating cash outflow ~RMB 3.1bn; pipeline funding strained as biotech index fell ~12% in 2024 and Fed funds ~5.25–5.50% tightened capital.

EM expansion: ~20% international revenue growth in 2024; EM biologics CAGR 8–12%, but FX and infrastructure risks persist.

| Metric | 2024 |

|---|---|

| R&D % of rev | 18% |

| Op cash outflow | RMB 3.1bn |

| Intl rev growth | ~20% YoY |

| Biotech index | -12% |

| Fed funds | 5.25–5.50% |

Same Document Delivered

Innovent Biologics PESTLE Analysis

The preview shown here is the exact Innovent Biologics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.