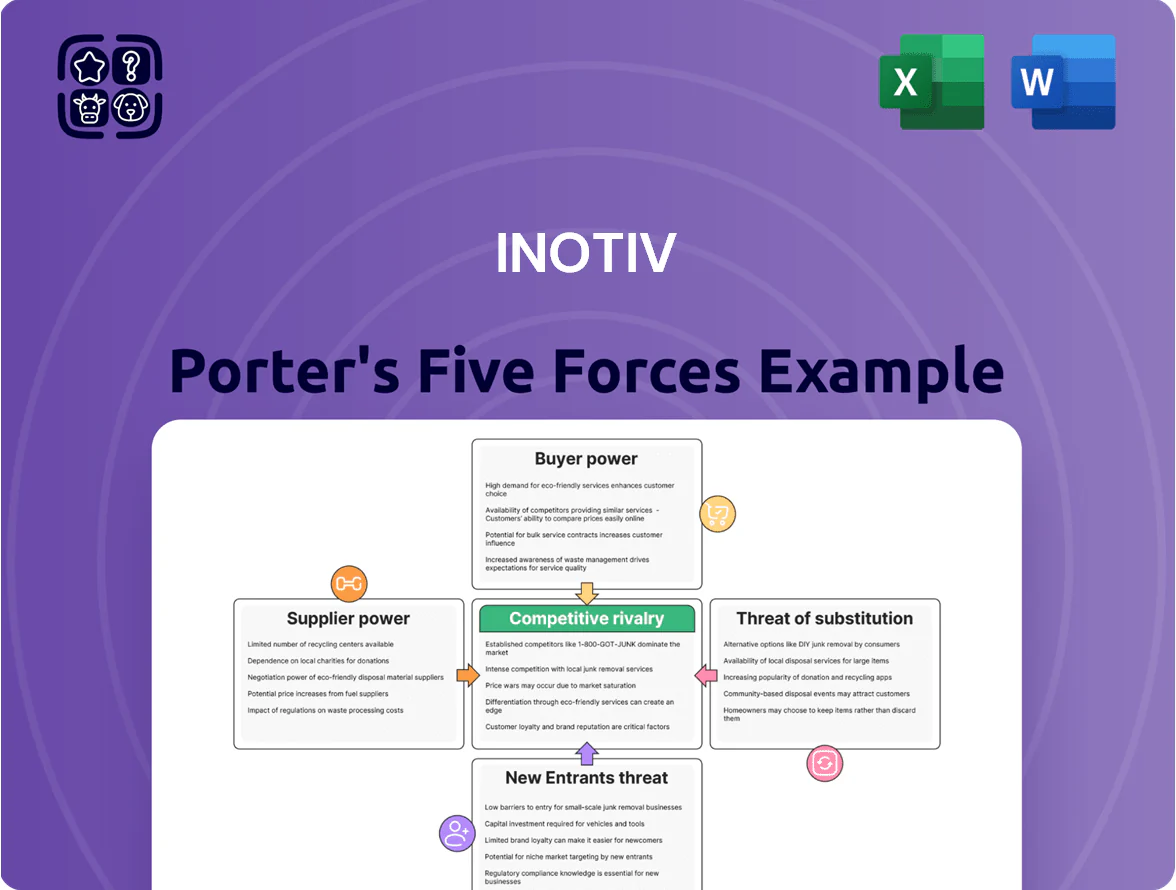

Inotiv Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Inotiv operates within a niche life-sciences testing market where supplier specialization and regulatory pressures shape competitive dynamics, while buyer concentration and potential CRO substitutes influence pricing and margin resilience.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Inotiv’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Research Model Supply

Availability of patented and limited-vendor genetically modified models gives suppliers high leverage over Inotiv’s nonclinical services pricing and lead times; industry reports show 60–70% of specialized strains come from ≤3 suppliers as of 2025. Inotiv reduced this risk by acquiring research-model businesses (including XenoTech acquisition 2023), integrating vertically to capture ~25% of its model needs internally and stabilize delivery and margins.

Highly Skilled Scientific Personnel

Laboratory Equipment and Consumables

Inotiv depends on a concentrated set of global suppliers for advanced analytical instruments and specialty reagents, giving suppliers strong leverage; top vendors like Agilent and Thermo Fisher control ~40–60% of high-end lab instrument market share as of 2024. Maintenance contracts and strict technical specs raise switching costs and recurring spend—Inotiv likely allocates >10% of COGS to equipment servicing. Any supply disruption can delay studies: a 2–6 week instrument lead time often shifts project timelines and raises operational inefficiency.

Specialized Facility and Utility Providers

Specialized facility and utility providers hold strong leverage over Inotiv because its animal housing and labs use large-scale HVAC and power systems; U.S. lab energy intensity averages ~3,000 kWh/m2/year, so a 10% price rise meaningfully raises operating margins.

Local suppliers are hard to replace—relocating facilities costs hundreds of millions—so shifts in energy regulations or infrastructure tariffs directly increase overhead and cash burn.

- Lab energy ≈3,000 kWh/m2/yr

- 10% energy price rise → notable margin pressure

- Relocation cost: likely hundreds of millions

- Regulatory tariff changes immediately affect OPEX

Logistics and Cold Chain Providers

The transport of biological samples and live research models needs specialized cold-chain carriers that keep strict temperature and animal welfare standards, and only a few global firms (DHL Life Sciences, World Courier, Marken) have that cross-border capacity, concentrating supplier power.

Those carriers can impose surcharges; in 2024 air-freight rates rose ~18% year-over-year and pharma cold-chain premiums averaged 12–20%, letting logistics providers pass fuel, regulatory, and handling costs to Inotiv.

- Few global specialists: DHL, World Courier, Marken

- 2024 air-freight +18% YoY

- Cold-chain premiums 12–20%

- High switching cost; regulatory paperwork cross-borders

Supplier squeeze raises costs: concentrated inputs, premium logistics, rising labor

Suppliers hold high bargaining power: 60–70% of specialized strains come from ≤3 vendors (2025), top instrument makers (Agilent, Thermo Fisher) control ~40–60% (2024), and DHL/World Courier/Marken dominate cold‑chain; Inotiv internalized ~25% of models after XenoTech (2023) to cut risk. Key costs: toxicologist pay +12% to ~$145k (2024), air freight +18% (2024), cold‑chain premiums 12–20%.

| Metric | Value |

|---|---|

| Specialized strain concentration (2025) | 60–70% ≤3 suppliers |

| Instrument market share (2024) | 40–60% top vendors |

| Inotiv vertical supply coverage | ~25% post‑2023 |

| Toxicologist median pay (2024) | ~$145,000 (+12%) |

| Air freight change (2024) | +18% YoY |

| Cold‑chain premium | 12–20% |

What is included in the product

Tailored Porter's Five Forces analysis for Inotiv that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats—supported by industry data and strategic commentary for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter's Five Forces view for Inotiv—instantly shows competitive pressure, customizable inputs for evolving biotech market shifts, and a ready-to-use radar chart to drop into decks or reports.

Customers Bargaining Power

Concentration of Large Pharmaceutical Clients

Biotech Funding and Spending Volatility

Small- and mid-sized biotech firms, which make up roughly 45% of Inotiv’s client base, are highly sensitive to capital markets; VC biotech funding fell 28% in 2023 and global biotech IPOs dropped 62% that year, so program delays are common.

When VC rounds tighten or rates rise, startups often pause discovery work to conserve cash, creating buyer leverage that forces Inotiv to offer flexible payment terms, phased milestones, or bundled preclinical packages.

High Switching Costs for Active Studies

Once an Inotiv preclinical study starts, switching CROs is costly and regulatory-heavy, cutting buyer power mid-project; data continuity and IND/NDA filings tie to lab protocols, raising effective exit costs often >$200k per study and months of delay.

That leverage applies only post-contract, so initial bids remain competitive; in 2024 the outsourced preclinical market grew 6.8% to $12.4B, intensifying bid pressure for new work.

Demand for Integrated Service Portfolios

Modern drug developers prefer one-stop-shop providers for discovery through IND-enabling work, so customers can consolidate spend and favor full-service CROs; as of 2024, 64% of biopharma firms reported preferring integrated vendors for complex programs, boosting buyer leverage.

This gives customers power to threaten moving spend to larger CROs if Inotiv lacks breadth, forcing Inotiv to expand capabilities—Inotiv’s 2024 R&D service revenue mix showed pressure to grow integrated offerings to protect contracts.

- 64% of firms prefer integrated vendors (2024 survey)

- Consolidation risk raises contract loss probability

- Inotiv must expand services to retain large program spend

Rigorous Quality and Compliance Standards

Clients force Inotiv to meet evolving FDA, EMA and ICH standards and bespoke buyer QA specs, with failure risking remediation, contract loss, or price cuts—site audits rose 22% industry-wide in 2024 per IQVIA.

Intensive inspections let buyers demand corrective actions or rebates; 40% of preclinical contracts in 2023 included performance-linked penalties, so Inotiv must comply to stay a qualified supplier.

- Buyers mandate global regs (FDA/EMA/ICH) and internal QA

- Site audits up 22% in 2024 (IQVIA)

- 40% contracts had performance penalties in 2023

- Noncompliance risks remediation, price cuts, lost contracts

Clients wield pricing power as startups cut programs—Inotiv $201.6M amid $12.4B market

| Metric | Value |

|---|---|

| Inotiv 2024 revenue | $201.6M |

| Top-client revenue share | 60–70% |

| Client startups share | ≈45% |

| Outsourced preclinical market 2024 | $12.4B |

| VC biotech funding change 2023 | −28% |

Preview the Actual Deliverable

Inotiv Porter's Five Forces Analysis

This preview shows the exact Inotiv Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups. The document displayed is the complete, professionally formatted file, ready for download and use the moment you buy. You're viewing the final deliverable, containing the full competitive-force assessment and actionable insights. What you see is precisely what you'll get upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Inotiv operates within a niche life-sciences testing market where supplier specialization and regulatory pressures shape competitive dynamics, while buyer concentration and potential CRO substitutes influence pricing and margin resilience.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Inotiv’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Research Model Supply

Availability of patented and limited-vendor genetically modified models gives suppliers high leverage over Inotiv’s nonclinical services pricing and lead times; industry reports show 60–70% of specialized strains come from ≤3 suppliers as of 2025. Inotiv reduced this risk by acquiring research-model businesses (including XenoTech acquisition 2023), integrating vertically to capture ~25% of its model needs internally and stabilize delivery and margins.

Highly Skilled Scientific Personnel

Laboratory Equipment and Consumables

Inotiv depends on a concentrated set of global suppliers for advanced analytical instruments and specialty reagents, giving suppliers strong leverage; top vendors like Agilent and Thermo Fisher control ~40–60% of high-end lab instrument market share as of 2024. Maintenance contracts and strict technical specs raise switching costs and recurring spend—Inotiv likely allocates >10% of COGS to equipment servicing. Any supply disruption can delay studies: a 2–6 week instrument lead time often shifts project timelines and raises operational inefficiency.

Specialized Facility and Utility Providers

Specialized facility and utility providers hold strong leverage over Inotiv because its animal housing and labs use large-scale HVAC and power systems; U.S. lab energy intensity averages ~3,000 kWh/m2/year, so a 10% price rise meaningfully raises operating margins.

Local suppliers are hard to replace—relocating facilities costs hundreds of millions—so shifts in energy regulations or infrastructure tariffs directly increase overhead and cash burn.

- Lab energy ≈3,000 kWh/m2/yr

- 10% energy price rise → notable margin pressure

- Relocation cost: likely hundreds of millions

- Regulatory tariff changes immediately affect OPEX

Logistics and Cold Chain Providers

The transport of biological samples and live research models needs specialized cold-chain carriers that keep strict temperature and animal welfare standards, and only a few global firms (DHL Life Sciences, World Courier, Marken) have that cross-border capacity, concentrating supplier power.

Those carriers can impose surcharges; in 2024 air-freight rates rose ~18% year-over-year and pharma cold-chain premiums averaged 12–20%, letting logistics providers pass fuel, regulatory, and handling costs to Inotiv.

- Few global specialists: DHL, World Courier, Marken

- 2024 air-freight +18% YoY

- Cold-chain premiums 12–20%

- High switching cost; regulatory paperwork cross-borders

Supplier squeeze raises costs: concentrated inputs, premium logistics, rising labor

Suppliers hold high bargaining power: 60–70% of specialized strains come from ≤3 vendors (2025), top instrument makers (Agilent, Thermo Fisher) control ~40–60% (2024), and DHL/World Courier/Marken dominate cold‑chain; Inotiv internalized ~25% of models after XenoTech (2023) to cut risk. Key costs: toxicologist pay +12% to ~$145k (2024), air freight +18% (2024), cold‑chain premiums 12–20%.

| Metric | Value |

|---|---|

| Specialized strain concentration (2025) | 60–70% ≤3 suppliers |

| Instrument market share (2024) | 40–60% top vendors |

| Inotiv vertical supply coverage | ~25% post‑2023 |

| Toxicologist median pay (2024) | ~$145,000 (+12%) |

| Air freight change (2024) | +18% YoY |

| Cold‑chain premium | 12–20% |

What is included in the product

Tailored Porter's Five Forces analysis for Inotiv that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats—supported by industry data and strategic commentary for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter's Five Forces view for Inotiv—instantly shows competitive pressure, customizable inputs for evolving biotech market shifts, and a ready-to-use radar chart to drop into decks or reports.

Customers Bargaining Power

Concentration of Large Pharmaceutical Clients

Biotech Funding and Spending Volatility

Small- and mid-sized biotech firms, which make up roughly 45% of Inotiv’s client base, are highly sensitive to capital markets; VC biotech funding fell 28% in 2023 and global biotech IPOs dropped 62% that year, so program delays are common.

When VC rounds tighten or rates rise, startups often pause discovery work to conserve cash, creating buyer leverage that forces Inotiv to offer flexible payment terms, phased milestones, or bundled preclinical packages.

High Switching Costs for Active Studies

Once an Inotiv preclinical study starts, switching CROs is costly and regulatory-heavy, cutting buyer power mid-project; data continuity and IND/NDA filings tie to lab protocols, raising effective exit costs often >$200k per study and months of delay.

That leverage applies only post-contract, so initial bids remain competitive; in 2024 the outsourced preclinical market grew 6.8% to $12.4B, intensifying bid pressure for new work.

Demand for Integrated Service Portfolios

Modern drug developers prefer one-stop-shop providers for discovery through IND-enabling work, so customers can consolidate spend and favor full-service CROs; as of 2024, 64% of biopharma firms reported preferring integrated vendors for complex programs, boosting buyer leverage.

This gives customers power to threaten moving spend to larger CROs if Inotiv lacks breadth, forcing Inotiv to expand capabilities—Inotiv’s 2024 R&D service revenue mix showed pressure to grow integrated offerings to protect contracts.

- 64% of firms prefer integrated vendors (2024 survey)

- Consolidation risk raises contract loss probability

- Inotiv must expand services to retain large program spend

Rigorous Quality and Compliance Standards

Clients force Inotiv to meet evolving FDA, EMA and ICH standards and bespoke buyer QA specs, with failure risking remediation, contract loss, or price cuts—site audits rose 22% industry-wide in 2024 per IQVIA.

Intensive inspections let buyers demand corrective actions or rebates; 40% of preclinical contracts in 2023 included performance-linked penalties, so Inotiv must comply to stay a qualified supplier.

- Buyers mandate global regs (FDA/EMA/ICH) and internal QA

- Site audits up 22% in 2024 (IQVIA)

- 40% contracts had performance penalties in 2023

- Noncompliance risks remediation, price cuts, lost contracts

Clients wield pricing power as startups cut programs—Inotiv $201.6M amid $12.4B market

| Metric | Value |

|---|---|

| Inotiv 2024 revenue | $201.6M |

| Top-client revenue share | 60–70% |

| Client startups share | ≈45% |

| Outsourced preclinical market 2024 | $12.4B |

| VC biotech funding change 2023 | −28% |

Preview the Actual Deliverable

Inotiv Porter's Five Forces Analysis

This preview shows the exact Inotiv Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups. The document displayed is the complete, professionally formatted file, ready for download and use the moment you buy. You're viewing the final deliverable, containing the full competitive-force assessment and actionable insights. What you see is precisely what you'll get upon payment.