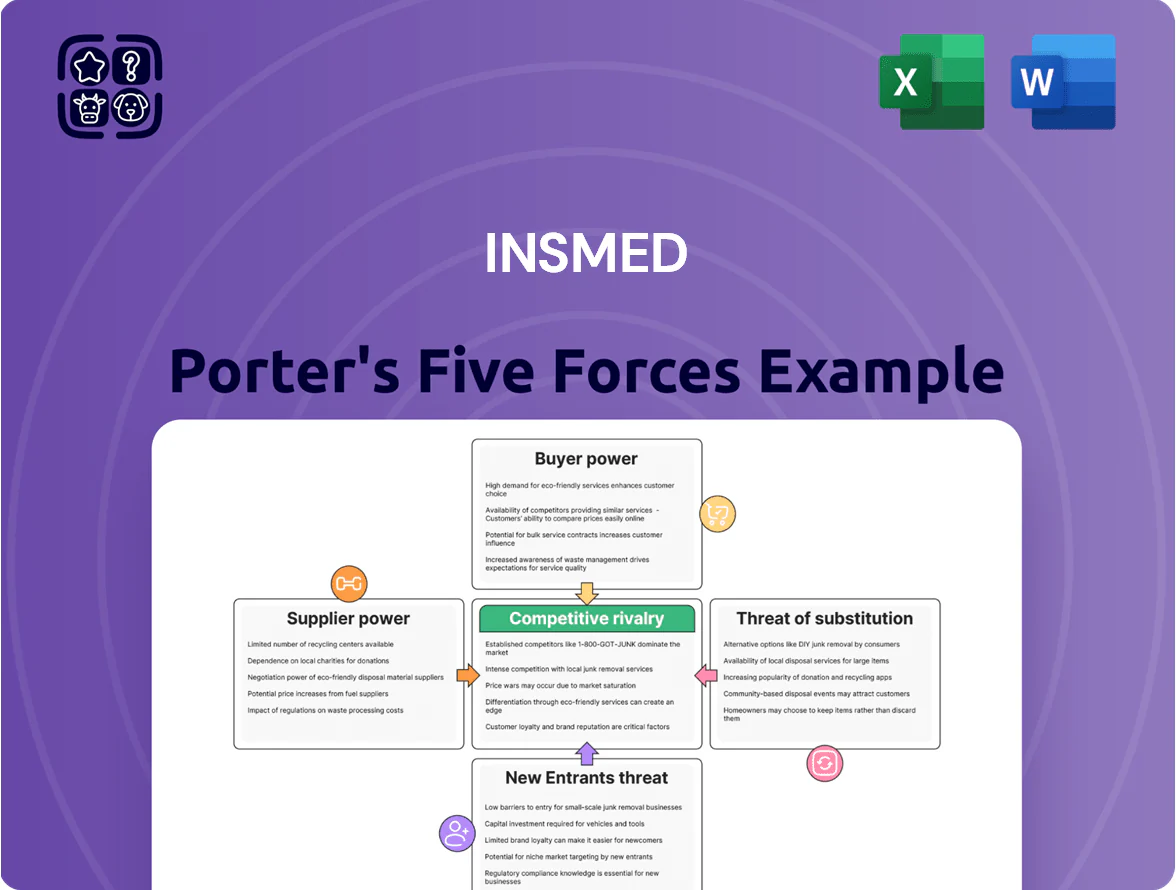

Insmed Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Insmed faces moderate supplier power, high regulatory barriers, and intense competition for niche pulmonary therapies, while substitutes and buyer bargaining vary by payer dynamics and clinical differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Insmed’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Manufacturing and CMO Dependency

Insmed depends on third-party contract manufacturing organizations (CMOs) for complex liposomal drug ARIKAYCE, and those CMOs hold rare technical know-how and specialized facilities, giving them strong negotiating leverage.

By end-2025, global high-quality biologic capacity utilization exceeded 85% and CMOs saw average price increases of 6–8% in 2024–25, keeping supplier power elevated in the rare-disease niche.

Limited Sources for Raw Materials and APIs

The production of Insmed’s inhaled and systemic biologics depends on a narrow set of suppliers for active pharmaceutical ingredients (APIs) and specialized lipids; in 2024, 60–70% of critical inputs for rare-disease biologics came from fewer than five qualified vendors, raising supplier leverage.

Supply disruptions can delay launch timelines by months and cut revenue—Insmed reported clinical supply constraints in 2023 that shifted expected commercialization by ~6–9 months—so vendor risk is material.

To mitigate price swings and shortages, Insmed must lock long-term contracts and dual-source where possible; securing multi-year supply agreements and safety-stock targets (e.g., 6–12 months on-hand) lowers interruption risk.

High Regulatory and Switching Costs

Switching suppliers in biopharma forces new stability testing, process validation, and FDA inspections that can take 12–24 months and cost $5–20m, creating a strong lock-in for Insmed.

Those regulatory and timeline barriers let incumbent suppliers keep pricing power; a single active pharmaceutical ingredient (API) supplier can affect margins by 3–7 percentage points on a specialty drug’s gross margin.

This supplier strength persists across the drug lifecycle, from commercial scale-up to post-approval changes, raising sourcing risk for Insmed.

Specialized Distribution and Logistics Partners

The distribution of pulmonary medicines like Insmed’s Arikayce often needs cold-chain and specialized handling to preserve product integrity; failure rates in cold-chain shipments average 2–5% globally, raising spoilage costs.

Only a handful of global logistics firms meet rare-disease regulatory standards; the top 5 cold-chain providers control roughly 60% of market capacity, giving them leverage over pricing and contract terms.

Insmed faces concentration risk: logistics can add 8–15% to product COGS (cost of goods sold) for biologics and rare-disease inhaled therapies, so suppliers can materially affect margins.

- Cold-chain failure 2–5%

- Top 5 providers ~60% capacity

- Logistics add 8–15% to COGS

Competition for Specialized Scientific Talent

The pool of researchers and clinical experts in rare pulmonary diseases is small and intensely contested by Big Pharma; Insmed competes directly with companies like AstraZeneca and GSK for this talent, raising hiring costs and time-to-hire.

Specialized labor costs rose ~12% in US biotech hubs in 2024, boosting the bargaining power of this workforce and pressuring Insmed’s R&D margins and timelines.

- Limited talent pool: few specialists in rare pulmonary disease

- Competitive rivals: larger pharma poaches staff

- Cost pressure: ~12% wage rise in 2024 biotech hubs

- Impact: higher R&D costs, longer recruitment, risk to pipeline

Insmed at risk: supplier concentration and CMO hikes threaten margins, launches, and costs

Insmed faces high supplier power: CMOs and a few API/lipid vendors hold specialized capacity and know-how, with global biologic capacity >85% in 2025 and CMO price rises of 6–8% in 2024–25, creating lock-in that can cut gross margins 3–7 pts and delay launches by 6–24 months. Logistics and cold-chain concentration (top 5 ~60% capacity; failure 2–5%) add 8–15% to COGS; specialized talent costs rose ~12% in 2024.

| Metric | 2024–25 |

|---|---|

| Biologic capacity utilization | >85% |

| CMO price increase | 6–8% |

| API/vendor concentration | 60–70% inputs from <5 vendors |

| Launch delay from supply issues | 6–24 months |

| Gross margin impact | 3–7 pts |

| Cold-chain failure | 2–5% |

| Top5 logistics share | ~60% |

| Logistics cost to COGS | 8–15% |

| Specialized labor wage rise | ~12% |

What is included in the product

Tailored Porter's Five Forces analysis for Insmed that uncovers competitive dynamics, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share and profitability.

A concise Porter's Five Forces snapshot for Insmed—highlighting bargaining power, competitive rivalry, and regulatory threats to speed strategic decisions and investor pitches.

Customers Bargaining Power

Concentration of Third-Party Payers

The primary customers for Insmed are large insurers and pharmacy benefit managers (PBMs) that control reimbursement; top three PBMs covered ~80% of US lives by 2024, giving them huge leverage. These buyers extract double-digit rebates and discounts, cutting Insmed’s net price and margins; Insmed reported a 2024 net realized price decline of ~12% for specialty products. By late 2025 payer consolidation further centralized purchasing power, making formulary placement a critical, tough negotiation.

Government Reimbursement and Pricing Policies

Government programs like Medicare and single-payer systems buy a large share of rare-disease drugs; in 2024 Medicare Part B/Part D spending on orphan drugs exceeded $22.5B, so payers drive hard bargains. These agencies can impose price caps or demand value-based contracts linking pay to outcomes—Insmed must prove superior efficacy to defend list prices amid shrinking public health budgets and 2023–25 cost-containment measures.

Physician Influence and Prescription Patterns

Specialized pulmonologists are gatekeepers for NTM lung disease prescriptions, guiding use of Insmed’s Arikayce (amikacin liposome inhalation suspension) where indicated; however, restrictive payer formularies now block access for roughly 30–40% of Medicare Part D and commercial plans as of 2024, cutting prescribing freedom. Insmed must fund medical education and publish real-world outcome data—recent 2023 registry results showed a 45% culture conversion at 12 months—to keep clinicians aligned with their therapy.

Patient Advocacy Group Influence

Patient advocacy groups in rare disease markets meaningfully shift bargaining power by influencing regulators and payers; in 2024 over 60% of FDA rare disease approvals cited patient input, boosting their leverage over Insmed.

They pressure for affordable access and can prompt price concessions or broader patient-assistance programs; in 2023 nonprofit funding helped secure coverage expansions for therapies affecting ~120,000 US patients.

Their collective voice acts as buyer power, forcing concessions on list price discounts and copay support, increasing payer negotiation costs and potentially compressing Insmed’s margins.

- 60%+ FDA rare approvals cited patient input (2024)

- 2023 advocacy-driven coverage expansions impacted ~120,000 US patients

- Raises likelihood of price concessions and expanded assistance programs

Availability of Clinical Comparative Data

As 2025 real-world data increase, payers use efficacy and cost-effectiveness comparisons to push down prices when Insmed’s NTM drug lacks clear superiority; a 2024 systematic review showed variable cure rates 30–60%, giving payers leverage.

Insmed needs ongoing registry and post‑market studies—expect 12–24 month real-world cohorts and incremental‑cost analyses—to defend a premium and preserve formulary access.

- Payers compare efficacy/cost; cure rates 30–60% (2024 review)

PBM Power Slashes Prices & Access: Top‑3 Cover ~80% as Net Prices Fall 12%

Buyers (PBMs/insurers, Medicare) hold strong leverage—top 3 PBMs covered ~80% of US lives by 2024, driving double-digit rebates; Insmed reported ~12% net price decline in 2024. Payer/formulary restrictions block 30–40% of plans; real-world cure rates 30–60% (2024) empower price pressure. Patient groups (2023: ~120,000 patients aided) push access concessions.

| Metric | Value |

|---|---|

| Top-3 PBM coverage | ~80% (2024) |

| Net price change | -12% (2024) |

| Formulary blocks | 30–40% plans (2024) |

| Cure rates | 30–60% (2024) |

| Advocacy impact | ~120,000 patients (2023) |

Same Document Delivered

Insmed Porter's Five Forces Analysis

This preview shows the exact Insmed Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

You're viewing the final document: the same comprehensive assessment of competitive rivalry, buyer and supplier power, threat of entrants, and substitutes that will be available for instant download upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Insmed faces moderate supplier power, high regulatory barriers, and intense competition for niche pulmonary therapies, while substitutes and buyer bargaining vary by payer dynamics and clinical differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Insmed’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Manufacturing and CMO Dependency

Insmed depends on third-party contract manufacturing organizations (CMOs) for complex liposomal drug ARIKAYCE, and those CMOs hold rare technical know-how and specialized facilities, giving them strong negotiating leverage.

By end-2025, global high-quality biologic capacity utilization exceeded 85% and CMOs saw average price increases of 6–8% in 2024–25, keeping supplier power elevated in the rare-disease niche.

Limited Sources for Raw Materials and APIs

The production of Insmed’s inhaled and systemic biologics depends on a narrow set of suppliers for active pharmaceutical ingredients (APIs) and specialized lipids; in 2024, 60–70% of critical inputs for rare-disease biologics came from fewer than five qualified vendors, raising supplier leverage.

Supply disruptions can delay launch timelines by months and cut revenue—Insmed reported clinical supply constraints in 2023 that shifted expected commercialization by ~6–9 months—so vendor risk is material.

To mitigate price swings and shortages, Insmed must lock long-term contracts and dual-source where possible; securing multi-year supply agreements and safety-stock targets (e.g., 6–12 months on-hand) lowers interruption risk.

High Regulatory and Switching Costs

Switching suppliers in biopharma forces new stability testing, process validation, and FDA inspections that can take 12–24 months and cost $5–20m, creating a strong lock-in for Insmed.

Those regulatory and timeline barriers let incumbent suppliers keep pricing power; a single active pharmaceutical ingredient (API) supplier can affect margins by 3–7 percentage points on a specialty drug’s gross margin.

This supplier strength persists across the drug lifecycle, from commercial scale-up to post-approval changes, raising sourcing risk for Insmed.

Specialized Distribution and Logistics Partners

The distribution of pulmonary medicines like Insmed’s Arikayce often needs cold-chain and specialized handling to preserve product integrity; failure rates in cold-chain shipments average 2–5% globally, raising spoilage costs.

Only a handful of global logistics firms meet rare-disease regulatory standards; the top 5 cold-chain providers control roughly 60% of market capacity, giving them leverage over pricing and contract terms.

Insmed faces concentration risk: logistics can add 8–15% to product COGS (cost of goods sold) for biologics and rare-disease inhaled therapies, so suppliers can materially affect margins.

- Cold-chain failure 2–5%

- Top 5 providers ~60% capacity

- Logistics add 8–15% to COGS

Competition for Specialized Scientific Talent

The pool of researchers and clinical experts in rare pulmonary diseases is small and intensely contested by Big Pharma; Insmed competes directly with companies like AstraZeneca and GSK for this talent, raising hiring costs and time-to-hire.

Specialized labor costs rose ~12% in US biotech hubs in 2024, boosting the bargaining power of this workforce and pressuring Insmed’s R&D margins and timelines.

- Limited talent pool: few specialists in rare pulmonary disease

- Competitive rivals: larger pharma poaches staff

- Cost pressure: ~12% wage rise in 2024 biotech hubs

- Impact: higher R&D costs, longer recruitment, risk to pipeline

Insmed at risk: supplier concentration and CMO hikes threaten margins, launches, and costs

Insmed faces high supplier power: CMOs and a few API/lipid vendors hold specialized capacity and know-how, with global biologic capacity >85% in 2025 and CMO price rises of 6–8% in 2024–25, creating lock-in that can cut gross margins 3–7 pts and delay launches by 6–24 months. Logistics and cold-chain concentration (top 5 ~60% capacity; failure 2–5%) add 8–15% to COGS; specialized talent costs rose ~12% in 2024.

| Metric | 2024–25 |

|---|---|

| Biologic capacity utilization | >85% |

| CMO price increase | 6–8% |

| API/vendor concentration | 60–70% inputs from <5 vendors |

| Launch delay from supply issues | 6–24 months |

| Gross margin impact | 3–7 pts |

| Cold-chain failure | 2–5% |

| Top5 logistics share | ~60% |

| Logistics cost to COGS | 8–15% |

| Specialized labor wage rise | ~12% |

What is included in the product

Tailored Porter's Five Forces analysis for Insmed that uncovers competitive dynamics, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share and profitability.

A concise Porter's Five Forces snapshot for Insmed—highlighting bargaining power, competitive rivalry, and regulatory threats to speed strategic decisions and investor pitches.

Customers Bargaining Power

Concentration of Third-Party Payers

The primary customers for Insmed are large insurers and pharmacy benefit managers (PBMs) that control reimbursement; top three PBMs covered ~80% of US lives by 2024, giving them huge leverage. These buyers extract double-digit rebates and discounts, cutting Insmed’s net price and margins; Insmed reported a 2024 net realized price decline of ~12% for specialty products. By late 2025 payer consolidation further centralized purchasing power, making formulary placement a critical, tough negotiation.

Government Reimbursement and Pricing Policies

Government programs like Medicare and single-payer systems buy a large share of rare-disease drugs; in 2024 Medicare Part B/Part D spending on orphan drugs exceeded $22.5B, so payers drive hard bargains. These agencies can impose price caps or demand value-based contracts linking pay to outcomes—Insmed must prove superior efficacy to defend list prices amid shrinking public health budgets and 2023–25 cost-containment measures.

Physician Influence and Prescription Patterns

Specialized pulmonologists are gatekeepers for NTM lung disease prescriptions, guiding use of Insmed’s Arikayce (amikacin liposome inhalation suspension) where indicated; however, restrictive payer formularies now block access for roughly 30–40% of Medicare Part D and commercial plans as of 2024, cutting prescribing freedom. Insmed must fund medical education and publish real-world outcome data—recent 2023 registry results showed a 45% culture conversion at 12 months—to keep clinicians aligned with their therapy.

Patient Advocacy Group Influence

Patient advocacy groups in rare disease markets meaningfully shift bargaining power by influencing regulators and payers; in 2024 over 60% of FDA rare disease approvals cited patient input, boosting their leverage over Insmed.

They pressure for affordable access and can prompt price concessions or broader patient-assistance programs; in 2023 nonprofit funding helped secure coverage expansions for therapies affecting ~120,000 US patients.

Their collective voice acts as buyer power, forcing concessions on list price discounts and copay support, increasing payer negotiation costs and potentially compressing Insmed’s margins.

- 60%+ FDA rare approvals cited patient input (2024)

- 2023 advocacy-driven coverage expansions impacted ~120,000 US patients

- Raises likelihood of price concessions and expanded assistance programs

Availability of Clinical Comparative Data

As 2025 real-world data increase, payers use efficacy and cost-effectiveness comparisons to push down prices when Insmed’s NTM drug lacks clear superiority; a 2024 systematic review showed variable cure rates 30–60%, giving payers leverage.

Insmed needs ongoing registry and post‑market studies—expect 12–24 month real-world cohorts and incremental‑cost analyses—to defend a premium and preserve formulary access.

- Payers compare efficacy/cost; cure rates 30–60% (2024 review)

PBM Power Slashes Prices & Access: Top‑3 Cover ~80% as Net Prices Fall 12%

Buyers (PBMs/insurers, Medicare) hold strong leverage—top 3 PBMs covered ~80% of US lives by 2024, driving double-digit rebates; Insmed reported ~12% net price decline in 2024. Payer/formulary restrictions block 30–40% of plans; real-world cure rates 30–60% (2024) empower price pressure. Patient groups (2023: ~120,000 patients aided) push access concessions.

| Metric | Value |

|---|---|

| Top-3 PBM coverage | ~80% (2024) |

| Net price change | -12% (2024) |

| Formulary blocks | 30–40% plans (2024) |

| Cure rates | 30–60% (2024) |

| Advocacy impact | ~120,000 patients (2023) |

Same Document Delivered

Insmed Porter's Five Forces Analysis

This preview shows the exact Insmed Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

You're viewing the final document: the same comprehensive assessment of competitive rivalry, buyer and supplier power, threat of entrants, and substitutes that will be available for instant download upon payment.