Insperity Porter's Five Forces Analysis

From Overview to Strategy Blueprint

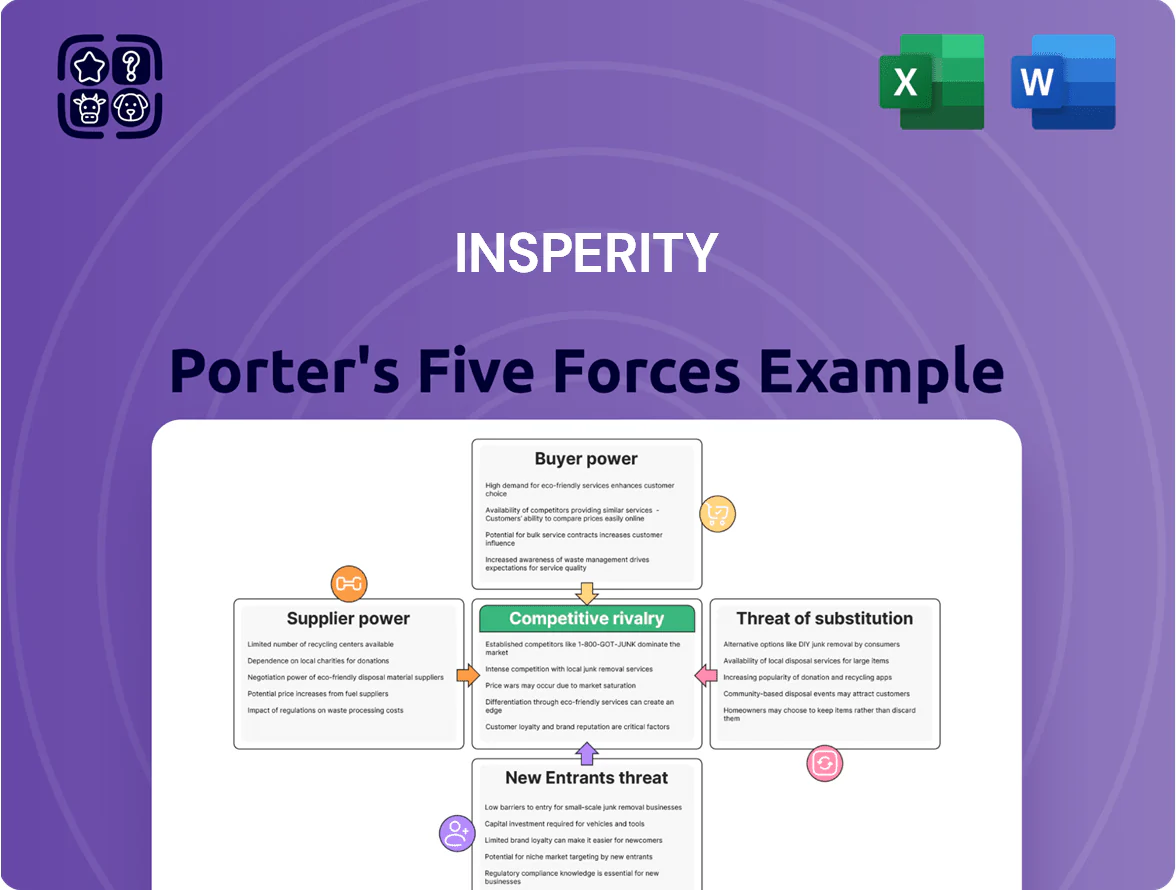

Insperity faces moderate buyer power and pricing pressure, fragmented supplier influence, and rising competitive intensity from HR tech disruptors—while regulatory shifts and scale advantages shape long-term barriers to entry.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Insperity’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Insurance Carrier Concentration

Insperity depends on a few large carriers—notably UnitedHealthcare, which covered about 28% of employer-sponsored medical plans in 2024—for core benefits, giving suppliers strong leverage over pricing and plan terms.

If a main carrier hikes premiums or tightens networks, Insperity has limited short-term alternatives, risking margin compression or client price increases; in 2024 medical cost inflation rose ~6.5%, widening that risk.

Technology and Software Vendors

Insperity relies on specialized third-party software for cloud, cybersecurity, and HRIS modules, and by end-2025 HR tech spend grew ~12% CAGR with US HR SaaS market ≈ $45B, increasing supplier leverage.

High switching costs, integration risk, and regulatory uptime needs give vendors bargaining power; a major outage could affect Insperity’s ~340,000 client employee records, so tight vendor SLAs and partnerships are critical.

Specialized Human Capital

The supply of certified HR pros, risk managers, and specialized sales staff is crucial to Insperity’s high-touch model; in 2024 the U.S. professional and business services sector saw wage growth of 4.1% year-over-year, pressuring margins.

In a tight labor market with 2.9% unemployment for management occupations (BLS, 2024), these specialists can demand higher pay and benefits, raising labor costs for Insperity.

Because Insperity’s brand depends on expert guidance, scarcity of top-tier talent increases wage inflation risk; SG&A rose 6.8% in FY2024, highlighting sensitivity to staffing costs.

Regulatory and Compliance Entities

Regulatory and compliance bodies act as noncommercial suppliers of the legal framework Insperity must follow; changes in federal/state labor laws, tax codes, or healthcare rules force ongoing legal and tech investment—Insperity spent about $84.6m on general and administrative expenses tied to compliance in FY2024.

Insperity is a price-taker for compliance costs: rule changes can raise SUTA, ACA, or FLSA-related costs overnight, squeezing margins and requiring rapid policy updates and client communication.

Financial Service Partners

Insperity depends on banks and payment processors to move over $30 billion in annual payroll (2024 company filings); these suppliers exert leverage via per-transaction fees and compliance/tech specs for secure, real-time transfers.

A fee rise of 10–20% or a tech outage at a partner would raise payroll costs and delay payments, directly hurting margins and client retention.

- 2024 payroll volume: ~$30B

- Key levers: per-transaction fees, API/security requirements

- Impact: fee hikes or outages → higher costs, slower payroll, churn

Insperity margins under squeeze: carrier power, payroll fees & rising compliance costs

Insperity faces high supplier power: major carriers (UnitedHealthcare ~28% of employer plans, 2024) and payment processors for ~$30B payroll (2024) can raise fees or limit networks, squeezing margins; specialist HR tech spend grew ~12% CAGR to a ~ $45B US HR SaaS market (2025), and FY2024 compliance G&A ~$84.6m adds fixed cost pressure.

| Item | Metric |

|---|---|

| UnitedHealthcare share | ~28% (2024) |

| Payroll volume | ~$30B (2024) |

| HR SaaS market | ~$45B (2025) |

| Compliance G&A | $84.6M (FY2024) |

What is included in the product

Tailored Porter’s Five Forces analysis for Insperity that uncovers competitive intensity, buyer/supplier power, threat of substitutes and entrants, and highlights disruptive trends and strategic levers to protect margins and grow market share.

One-sheet Porter's Five Forces for Insperity—quickly spot competitive pressures and prioritize HR-tech or service pivots to reduce risk and protect margins.

Customers Bargaining Power

Client Switching Costs

Small and medium businesses face moderate-to-high switching costs from Insperity because migrating sensitive employee records, re-enrolling benefits, and integrating new payroll systems typically takes 3–6 months and can cost 10–25% of annual HR spend; this operational friction and risk of payroll errors gives Insperity measurable pricing power as many clients prefer continuity over a complex migration.

Price Sensitivity of SMBs

SMB clients show high price sensitivity to administrative fees; a 2024 Intuit survey found 62% of small firms cite costs as the top HR outsourcing barrier, and Insperity’s 2024 revenue mix (82% services fees) means fee changes hit volumes fast.

Clients can easily compare Insperity pricing to digital-only rivals like Gusto and Rippling, which grew SMB market share ~10–18% annually through 2022–24, increasing benchmarking pressure.

This sensitivity constrains Insperity from aggressive fee hikes: a 1% fee lift could trigger >2% churn among microbusinesses based on industry churn elasticity estimates, hurting margin recovery.

Information Transparency and Benchmarking

By end-2025, online review platforms and pricing tools let buyers benchmark Insperity (NYSE: NSP) against rivals; 63% of HR buyers cited reviews as decisive in 2024, per Gartner. Market-rate transparency for PEO services (avg. fee range 2.5–6% of payroll) and feature comparisons shift leverage to customers. Decision-makers use competing quotes to negotiate lower renewal rates or demand extra services, raising churn pressure on Insperity.

Service Bundling and Customization Demands

Customers now prefer flexible, modular HR packages over one-size-fits-all PEO bundles; 42% of enterprise buyers in a 2024 Deloitte HR Services survey rated customization as a top purchase driver.

Large clients can demand custom reporting, specific API integrations, or tiered service levels, giving them strong bargaining power—Insperity reported 2024 revenue of $5.2B, with mid-market clients driving retention risks if needs unmet.

If Insperity fails to offer granular control, clients may shift to competitors offering à la carte services or tech-first platforms that reported 18% faster client acquisition in 2023.

- 42% of enterprises want customization

- 2024 revenue: $5.2B (Insperity)

- Demand: custom reporting, API integrations, tiered service

- Competitors: 18% faster client acquisition (2023)

Client Concentration and Volume

Insperity serves over 125,000 clients but losing several larger mid-market accounts at once could dent regional revenue targets; a single large client can represent millions in annual service fees and thousands of worksite employees (WSEs) contributing to PEO revenues.

Those large clients negotiate lower fees because they supply high WSE volumes; their option to re-insource HR or switch PEOs raises bargaining power and compresses margins during renewals.

High customer leverage: cost-sensitive, modularity-demanding market pressures Insperity

Customers have moderate-to-high bargaining power: switching costs (3–6 months, 10–25% HR spend) and Insperity’s $5.2B 2024 scale limit churn, but price sensitivity (62% cite cost), easy vendor comparison (Gusto/Rippling growth 10–18% 2022–24), demand for modularity (42% want customization), and large-client volume leverage raise renewal pressure.

| Metric | Value |

|---|---|

| 2024 Revenue | $5.2B |

| Clients | ~125,000 (2025) |

| Switch cost | 3–6 months; 10–25% HR spend |

| Price sensitivity | 62% cite cost (2024) |

| Customization demand | 42% (2024) |

Preview the Actual Deliverable

Insperity Porter's Five Forces Analysis

This preview shows the exact Insperity Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full, professionally formatted file you’ll get—ready for download and use the moment you buy.

No mockups or samples: this is the final deliverable, available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Insperity faces moderate buyer power and pricing pressure, fragmented supplier influence, and rising competitive intensity from HR tech disruptors—while regulatory shifts and scale advantages shape long-term barriers to entry.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Insperity’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Insurance Carrier Concentration

Insperity depends on a few large carriers—notably UnitedHealthcare, which covered about 28% of employer-sponsored medical plans in 2024—for core benefits, giving suppliers strong leverage over pricing and plan terms.

If a main carrier hikes premiums or tightens networks, Insperity has limited short-term alternatives, risking margin compression or client price increases; in 2024 medical cost inflation rose ~6.5%, widening that risk.

Technology and Software Vendors

Insperity relies on specialized third-party software for cloud, cybersecurity, and HRIS modules, and by end-2025 HR tech spend grew ~12% CAGR with US HR SaaS market ≈ $45B, increasing supplier leverage.

High switching costs, integration risk, and regulatory uptime needs give vendors bargaining power; a major outage could affect Insperity’s ~340,000 client employee records, so tight vendor SLAs and partnerships are critical.

Specialized Human Capital

The supply of certified HR pros, risk managers, and specialized sales staff is crucial to Insperity’s high-touch model; in 2024 the U.S. professional and business services sector saw wage growth of 4.1% year-over-year, pressuring margins.

In a tight labor market with 2.9% unemployment for management occupations (BLS, 2024), these specialists can demand higher pay and benefits, raising labor costs for Insperity.

Because Insperity’s brand depends on expert guidance, scarcity of top-tier talent increases wage inflation risk; SG&A rose 6.8% in FY2024, highlighting sensitivity to staffing costs.

Regulatory and Compliance Entities

Regulatory and compliance bodies act as noncommercial suppliers of the legal framework Insperity must follow; changes in federal/state labor laws, tax codes, or healthcare rules force ongoing legal and tech investment—Insperity spent about $84.6m on general and administrative expenses tied to compliance in FY2024.

Insperity is a price-taker for compliance costs: rule changes can raise SUTA, ACA, or FLSA-related costs overnight, squeezing margins and requiring rapid policy updates and client communication.

Financial Service Partners

Insperity depends on banks and payment processors to move over $30 billion in annual payroll (2024 company filings); these suppliers exert leverage via per-transaction fees and compliance/tech specs for secure, real-time transfers.

A fee rise of 10–20% or a tech outage at a partner would raise payroll costs and delay payments, directly hurting margins and client retention.

- 2024 payroll volume: ~$30B

- Key levers: per-transaction fees, API/security requirements

- Impact: fee hikes or outages → higher costs, slower payroll, churn

Insperity margins under squeeze: carrier power, payroll fees & rising compliance costs

Insperity faces high supplier power: major carriers (UnitedHealthcare ~28% of employer plans, 2024) and payment processors for ~$30B payroll (2024) can raise fees or limit networks, squeezing margins; specialist HR tech spend grew ~12% CAGR to a ~ $45B US HR SaaS market (2025), and FY2024 compliance G&A ~$84.6m adds fixed cost pressure.

| Item | Metric |

|---|---|

| UnitedHealthcare share | ~28% (2024) |

| Payroll volume | ~$30B (2024) |

| HR SaaS market | ~$45B (2025) |

| Compliance G&A | $84.6M (FY2024) |

What is included in the product

Tailored Porter’s Five Forces analysis for Insperity that uncovers competitive intensity, buyer/supplier power, threat of substitutes and entrants, and highlights disruptive trends and strategic levers to protect margins and grow market share.

One-sheet Porter's Five Forces for Insperity—quickly spot competitive pressures and prioritize HR-tech or service pivots to reduce risk and protect margins.

Customers Bargaining Power

Client Switching Costs

Small and medium businesses face moderate-to-high switching costs from Insperity because migrating sensitive employee records, re-enrolling benefits, and integrating new payroll systems typically takes 3–6 months and can cost 10–25% of annual HR spend; this operational friction and risk of payroll errors gives Insperity measurable pricing power as many clients prefer continuity over a complex migration.

Price Sensitivity of SMBs

SMB clients show high price sensitivity to administrative fees; a 2024 Intuit survey found 62% of small firms cite costs as the top HR outsourcing barrier, and Insperity’s 2024 revenue mix (82% services fees) means fee changes hit volumes fast.

Clients can easily compare Insperity pricing to digital-only rivals like Gusto and Rippling, which grew SMB market share ~10–18% annually through 2022–24, increasing benchmarking pressure.

This sensitivity constrains Insperity from aggressive fee hikes: a 1% fee lift could trigger >2% churn among microbusinesses based on industry churn elasticity estimates, hurting margin recovery.

Information Transparency and Benchmarking

By end-2025, online review platforms and pricing tools let buyers benchmark Insperity (NYSE: NSP) against rivals; 63% of HR buyers cited reviews as decisive in 2024, per Gartner. Market-rate transparency for PEO services (avg. fee range 2.5–6% of payroll) and feature comparisons shift leverage to customers. Decision-makers use competing quotes to negotiate lower renewal rates or demand extra services, raising churn pressure on Insperity.

Service Bundling and Customization Demands

Customers now prefer flexible, modular HR packages over one-size-fits-all PEO bundles; 42% of enterprise buyers in a 2024 Deloitte HR Services survey rated customization as a top purchase driver.

Large clients can demand custom reporting, specific API integrations, or tiered service levels, giving them strong bargaining power—Insperity reported 2024 revenue of $5.2B, with mid-market clients driving retention risks if needs unmet.

If Insperity fails to offer granular control, clients may shift to competitors offering à la carte services or tech-first platforms that reported 18% faster client acquisition in 2023.

- 42% of enterprises want customization

- 2024 revenue: $5.2B (Insperity)

- Demand: custom reporting, API integrations, tiered service

- Competitors: 18% faster client acquisition (2023)

Client Concentration and Volume

Insperity serves over 125,000 clients but losing several larger mid-market accounts at once could dent regional revenue targets; a single large client can represent millions in annual service fees and thousands of worksite employees (WSEs) contributing to PEO revenues.

Those large clients negotiate lower fees because they supply high WSE volumes; their option to re-insource HR or switch PEOs raises bargaining power and compresses margins during renewals.

High customer leverage: cost-sensitive, modularity-demanding market pressures Insperity

Customers have moderate-to-high bargaining power: switching costs (3–6 months, 10–25% HR spend) and Insperity’s $5.2B 2024 scale limit churn, but price sensitivity (62% cite cost), easy vendor comparison (Gusto/Rippling growth 10–18% 2022–24), demand for modularity (42% want customization), and large-client volume leverage raise renewal pressure.

| Metric | Value |

|---|---|

| 2024 Revenue | $5.2B |

| Clients | ~125,000 (2025) |

| Switch cost | 3–6 months; 10–25% HR spend |

| Price sensitivity | 62% cite cost (2024) |

| Customization demand | 42% (2024) |

Preview the Actual Deliverable

Insperity Porter's Five Forces Analysis

This preview shows the exact Insperity Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full, professionally formatted file you’ll get—ready for download and use the moment you buy.

No mockups or samples: this is the final deliverable, available instantly after payment.