Inter&Co Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

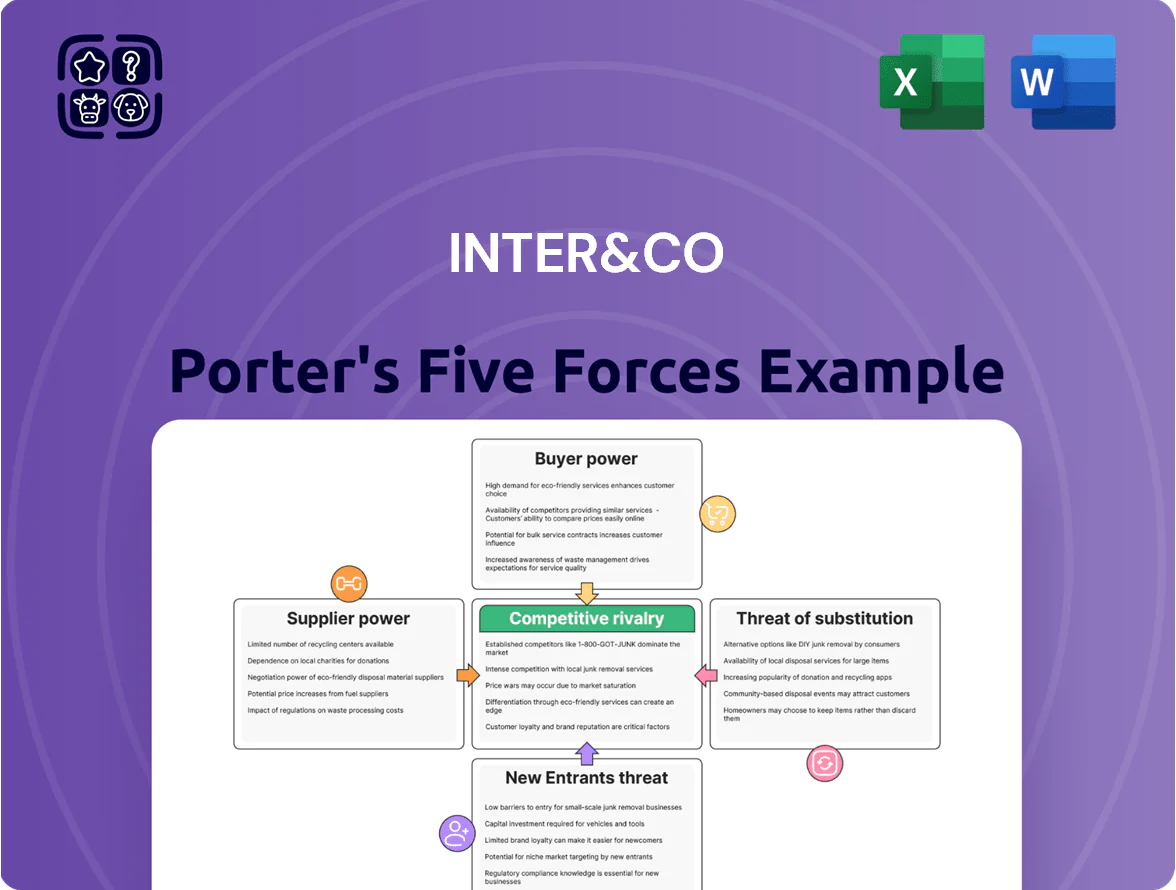

Inter&Co’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threats from entrants and substitutes, and how these forces shape margins and strategy.

Suppliers Bargaining Power

Cloud Infrastructure and Technology Providers

Inter&Co depends on major cloud providers such as Amazon Web Services (AWS) for uptime and scalability; AWS had 32% global IaaS market share in 2024, underscoring concentrated supplier power.

That concentration gives suppliers moderate leverage on pricing and SLAs, as top three providers held ~66% of cloud market in 2024, affecting contract terms.

Inter&Co’s multi-cloud strategy and ability to shift workloads limits lock-in, cutting outage risk and negotiating leverage—migration tools reduced multi-cloud switch costs by an estimated 15–25% in recent case studies.

Financial Market Infrastructure and Regulators

The Central Bank of Brazil and B3 provide the regulatory and technical rails Inter&Co depends on, setting capital rules, settlement windows, and PIX/TEF protocols; in 2024 the Central Bank’s Basel III capital buffer guidance raised minimum CET1 targets by ~1.0 percentage point for large banks, which raises funding costs for intermediated digital products.

Payment Network Rails

Global networks Visa and Mastercard supply the rails for Inter&Co’s debit and credit cards, giving them high supplier power because of near-universal acceptance and PCI DSS-level security that a single bank can’t match.

Inter&Co must negotiate interchange fees—Visa and Mastercard set global averages around 1.2–2.5% for consumer cards in 2024—so margin pressure is constant and switching costs are high.

Specialized Tech Talent and Human Capital

The supply of senior software engineers, data scientists, and cybersecurity experts is a strategic bottleneck for Inter&Co; Brazil produced ~70,000 new ICT graduates in 2023 but demand from fintechs keeps vacancy rates above 8% in São Paulo as of 2024.

These specialists command higher pay and remote-friendly terms—senior engineers in Brazil earned median R$240k in 2024—giving suppliers strong bargaining power over compensation and benefits.

Inter&Co must invest in employer brand, continuous learning, and equity/bonus schemes to retain talent crucial for its Super App roadmap and to avoid 15–25% annual tech attrition seen in regional fintechs.

- Brazil: ~70,000 ICT grads (2023)

- São Paulo tech vacancy rate >8% (2024)

- Senior engineer median pay R$240k (2024)

- Tech attrition 15–25% in regional fintechs

- Actions: employer brand, training, equity

Third-Party Marketplace Merchants

The Inter Shop ecosystem relies on thousands of retail partners; small merchants hold little leverage, but large anchors and brands (top 100 merchants representing ~40% of GMV in 2024) can demand higher cashback or integration priority.

Keeping a diverse merchant mix lets Inter&Co cap commissions (average take-rate 8% in 2024) and preserve consumer choice, so loss of a major brand could raise costs and reduce user retention.

- Top 100 merchants ≈ 40% GMV (2024)

- Average take-rate 8% (2024)

- Small merchants = low leverage

- Anchor brands = negotiation power

Suppliers wield strong leverage: cloud, card nets, regulators, talent, top merchants

Suppliers exert moderate-to-strong power: cloud (AWS 32% IaaS 2024; top3 ≈66%), card networks set interchange (1.2–2.5% 2024), regulators raise CET1 ~+1.0pp (2024), talent shortage (Brazil 70k ICT grads 2023; SP vacancy >8% 2024; senior pay R$240k 2024) and top 100 merchants ≈40% GMV concentrate bargaining.

| Supplier | Key metric (2023–24) |

|---|---|

| Cloud | AWS 32% IaaS; top3 ≈66% |

| Card nets | Interchange 1.2–2.5% |

| Regulator | CET1 +1.0pp (2024 guidance) |

| Talent | 70k grads; SP vacancy >8%; R$240k med pay |

| Merchants | Top100 ≈40% GMV; take-rate 8% |

What is included in the product

Tailored exclusively for Inter&Co, this Porter's Five Forces analysis uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and disruptive threats with strategic commentary and industry-backed insights.

Concise one-sheet Porter's Five Forces summary that clarifies competitive pressures instantly, with customizable force levels and a ready-to-use spider chart for fast inclusion in pitch decks or executive reports.

Customers Bargaining Power

Low Switching Costs in Digital Banking

Open Finance and Pix let Brazilian users move funds almost instantly; by 2025 Pix processes ~11.5 billion monthly transactions, so Inter&Co must keep service high to avoid churn.

Account opening/closure times dropped to minutes with APIs and instant transfers, giving customers leverage to demand better rates and features.

High Sensitivity to Fees and Interest Rates

Brazilian retail customers show high price sensitivity, with 58% using comparison platforms for fees and 65% favoring zero-fee accounts as of 2025, forcing banks to match zero-fee offers to retain volumes. Deposit APY comparisons drive flows—digital wallets and neo-banks advertise up to 12% annual yield on short-term products in 2025—so Inter&Co cannot raise rates without losing customers. Credit-cost sensitivity is high: average household compares APRs across 3+ apps before borrowing, limiting Inter&Co’s pricing power. Inter&Co must therefore chase operational efficiency to sustain margins while offering competitive rates and near-zero fees.

Access to Real-Time Information and Reviews

Modern users post on social media and review sites; 92% of consumers consult online reviews before buying and a single viral complaint can reach 100,000+ people in hours. This transparency gives customers collective power—repeated outages or poor support can cut net promoter score and lower retention by 15–30%. Inter&Co must prioritize UX, real-time monitoring, and proactive communication to contain reputational risk.

Demand for Integrated Super App Functionality

Customers now expect one app for banking, shopping, and investments, and 62% of US digital consumers in 2024 said they'd switch to platforms offering integrated financial services (McKinsey, 2024), forcing Inter&Co to rapidly add verticals to retain users.

This puts power with customers: they consolidate their financial life where utility is highest, so Inter&Co must prioritize cross-product UX, partner deals, and M&A to avoid churn and revenue loss.

- 62% of US digital consumers want integrated services

- Integrated users spend 2.5x more on-platform (2024 industry avg)

- Failure to integrate raises churn risk and opens room for specialist apps

Sophistication of Professional and Wealth Investors

As Inter&Co scales, professional and wealth investors demand expert tools and access to alternatives; globally HNW individuals held $87.5 trillion in 2024, so losing a handful can shift millions to rivals like XP or BTG Pactual.

Catering to pros forces product depth—advanced analytics, direct listings, private equity access—while keeping onboarding simple for novices; conversion and retention hinge on feature parity with incumbents.

- HNW pool: $87.5T (2024)

- Churn risk: large capital moves to XP/BTG

- Need: analytics + diverse assets

- Design: simple onboarding, expert depth

Brazilian customers force banks to match zero fees & 12% APYs or lose volumes

Customers hold strong bargaining power: Pix handled ~11.5B monthly txns in 2025 and 58% of Brazilians compare fees, so price sensitivity and instant switching force Inter&Co to match zero-fee offers and competitive APYs (neo-banks advertised up to 12% in 2025) or lose volumes.

| Metric | 2024–25 |

|---|---|

| Pix monthly txns | ~11.5B (2025) |

| Fee comparison | 58% users (2025) |

| Zero-fee preference | 65% (2025) |

| Neo-bank APY | up to 12% (2025) |

| Online review reach | viral complaint ~100k+ people hrs |

Preview the Actual Deliverable

Inter&Co Porter's Five Forces Analysis

This preview shows the exact Inter&Co Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders or mockups—fully formatted, professionally written, and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Inter&Co’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threats from entrants and substitutes, and how these forces shape margins and strategy.

Suppliers Bargaining Power

Cloud Infrastructure and Technology Providers

Inter&Co depends on major cloud providers such as Amazon Web Services (AWS) for uptime and scalability; AWS had 32% global IaaS market share in 2024, underscoring concentrated supplier power.

That concentration gives suppliers moderate leverage on pricing and SLAs, as top three providers held ~66% of cloud market in 2024, affecting contract terms.

Inter&Co’s multi-cloud strategy and ability to shift workloads limits lock-in, cutting outage risk and negotiating leverage—migration tools reduced multi-cloud switch costs by an estimated 15–25% in recent case studies.

Financial Market Infrastructure and Regulators

The Central Bank of Brazil and B3 provide the regulatory and technical rails Inter&Co depends on, setting capital rules, settlement windows, and PIX/TEF protocols; in 2024 the Central Bank’s Basel III capital buffer guidance raised minimum CET1 targets by ~1.0 percentage point for large banks, which raises funding costs for intermediated digital products.

Payment Network Rails

Global networks Visa and Mastercard supply the rails for Inter&Co’s debit and credit cards, giving them high supplier power because of near-universal acceptance and PCI DSS-level security that a single bank can’t match.

Inter&Co must negotiate interchange fees—Visa and Mastercard set global averages around 1.2–2.5% for consumer cards in 2024—so margin pressure is constant and switching costs are high.

Specialized Tech Talent and Human Capital

The supply of senior software engineers, data scientists, and cybersecurity experts is a strategic bottleneck for Inter&Co; Brazil produced ~70,000 new ICT graduates in 2023 but demand from fintechs keeps vacancy rates above 8% in São Paulo as of 2024.

These specialists command higher pay and remote-friendly terms—senior engineers in Brazil earned median R$240k in 2024—giving suppliers strong bargaining power over compensation and benefits.

Inter&Co must invest in employer brand, continuous learning, and equity/bonus schemes to retain talent crucial for its Super App roadmap and to avoid 15–25% annual tech attrition seen in regional fintechs.

- Brazil: ~70,000 ICT grads (2023)

- São Paulo tech vacancy rate >8% (2024)

- Senior engineer median pay R$240k (2024)

- Tech attrition 15–25% in regional fintechs

- Actions: employer brand, training, equity

Third-Party Marketplace Merchants

The Inter Shop ecosystem relies on thousands of retail partners; small merchants hold little leverage, but large anchors and brands (top 100 merchants representing ~40% of GMV in 2024) can demand higher cashback or integration priority.

Keeping a diverse merchant mix lets Inter&Co cap commissions (average take-rate 8% in 2024) and preserve consumer choice, so loss of a major brand could raise costs and reduce user retention.

- Top 100 merchants ≈ 40% GMV (2024)

- Average take-rate 8% (2024)

- Small merchants = low leverage

- Anchor brands = negotiation power

Suppliers wield strong leverage: cloud, card nets, regulators, talent, top merchants

Suppliers exert moderate-to-strong power: cloud (AWS 32% IaaS 2024; top3 ≈66%), card networks set interchange (1.2–2.5% 2024), regulators raise CET1 ~+1.0pp (2024), talent shortage (Brazil 70k ICT grads 2023; SP vacancy >8% 2024; senior pay R$240k 2024) and top 100 merchants ≈40% GMV concentrate bargaining.

| Supplier | Key metric (2023–24) |

|---|---|

| Cloud | AWS 32% IaaS; top3 ≈66% |

| Card nets | Interchange 1.2–2.5% |

| Regulator | CET1 +1.0pp (2024 guidance) |

| Talent | 70k grads; SP vacancy >8%; R$240k med pay |

| Merchants | Top100 ≈40% GMV; take-rate 8% |

What is included in the product

Tailored exclusively for Inter&Co, this Porter's Five Forces analysis uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and disruptive threats with strategic commentary and industry-backed insights.

Concise one-sheet Porter's Five Forces summary that clarifies competitive pressures instantly, with customizable force levels and a ready-to-use spider chart for fast inclusion in pitch decks or executive reports.

Customers Bargaining Power

Low Switching Costs in Digital Banking

Open Finance and Pix let Brazilian users move funds almost instantly; by 2025 Pix processes ~11.5 billion monthly transactions, so Inter&Co must keep service high to avoid churn.

Account opening/closure times dropped to minutes with APIs and instant transfers, giving customers leverage to demand better rates and features.

High Sensitivity to Fees and Interest Rates

Brazilian retail customers show high price sensitivity, with 58% using comparison platforms for fees and 65% favoring zero-fee accounts as of 2025, forcing banks to match zero-fee offers to retain volumes. Deposit APY comparisons drive flows—digital wallets and neo-banks advertise up to 12% annual yield on short-term products in 2025—so Inter&Co cannot raise rates without losing customers. Credit-cost sensitivity is high: average household compares APRs across 3+ apps before borrowing, limiting Inter&Co’s pricing power. Inter&Co must therefore chase operational efficiency to sustain margins while offering competitive rates and near-zero fees.

Access to Real-Time Information and Reviews

Modern users post on social media and review sites; 92% of consumers consult online reviews before buying and a single viral complaint can reach 100,000+ people in hours. This transparency gives customers collective power—repeated outages or poor support can cut net promoter score and lower retention by 15–30%. Inter&Co must prioritize UX, real-time monitoring, and proactive communication to contain reputational risk.

Demand for Integrated Super App Functionality

Customers now expect one app for banking, shopping, and investments, and 62% of US digital consumers in 2024 said they'd switch to platforms offering integrated financial services (McKinsey, 2024), forcing Inter&Co to rapidly add verticals to retain users.

This puts power with customers: they consolidate their financial life where utility is highest, so Inter&Co must prioritize cross-product UX, partner deals, and M&A to avoid churn and revenue loss.

- 62% of US digital consumers want integrated services

- Integrated users spend 2.5x more on-platform (2024 industry avg)

- Failure to integrate raises churn risk and opens room for specialist apps

Sophistication of Professional and Wealth Investors

As Inter&Co scales, professional and wealth investors demand expert tools and access to alternatives; globally HNW individuals held $87.5 trillion in 2024, so losing a handful can shift millions to rivals like XP or BTG Pactual.

Catering to pros forces product depth—advanced analytics, direct listings, private equity access—while keeping onboarding simple for novices; conversion and retention hinge on feature parity with incumbents.

- HNW pool: $87.5T (2024)

- Churn risk: large capital moves to XP/BTG

- Need: analytics + diverse assets

- Design: simple onboarding, expert depth

Brazilian customers force banks to match zero fees & 12% APYs or lose volumes

Customers hold strong bargaining power: Pix handled ~11.5B monthly txns in 2025 and 58% of Brazilians compare fees, so price sensitivity and instant switching force Inter&Co to match zero-fee offers and competitive APYs (neo-banks advertised up to 12% in 2025) or lose volumes.

| Metric | 2024–25 |

|---|---|

| Pix monthly txns | ~11.5B (2025) |

| Fee comparison | 58% users (2025) |

| Zero-fee preference | 65% (2025) |

| Neo-bank APY | up to 12% (2025) |

| Online review reach | viral complaint ~100k+ people hrs |

Preview the Actual Deliverable

Inter&Co Porter's Five Forces Analysis

This preview shows the exact Inter&Co Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders or mockups—fully formatted, professionally written, and ready for download and use the moment you buy.