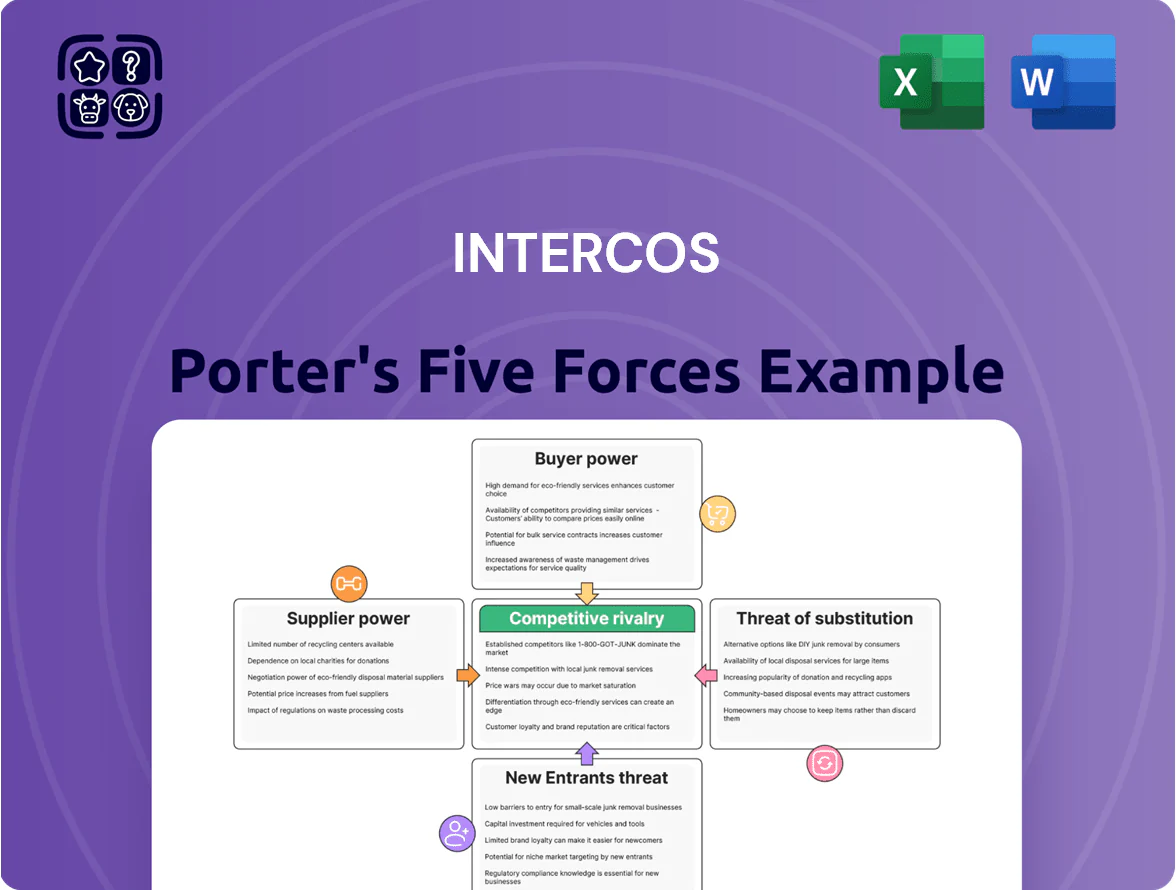

Intercos Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Intercos operates in a niche cosmetics-manufacturing market where supplier concentration and technical know-how raise entry barriers, while brand-driven buyer power and growing private-label demand intensify competition.

Regulatory complexity and raw-material volatility pose meaningful risks, yet Intercos’s R&D and scale offer defensive advantages against substitutes and rivals.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Intercos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Intercos depends on a complex supplier network for high‑grade pigments, actives, and sustainable compounds; scarcity of certified organic and ethically sourced inputs by late 2025 raised specialized suppliers’ leverage, with certified-supply shortfall estimated at ~18% industry-wide in 2024–25.

Intercos’s scale gives buying power—procurement spend exceeded €700m in 2024—but strict technical specs for prestige beauty shrink viable suppliers to a handful per ingredient, sustaining supplier bargaining power.

Energy and Logistics Cost Sensitivity

The cosmetics manufacturing is energy-intensive, so Intercos faces direct exposure to utility and logistics pricing; electricity can account for 6–12% of COGS in contract-manufacturing and diesel/logistics fuel added ~3–5% in 2024 for EU plants.

By end-2025 EU green-energy mandates and carbon pricing raised premiums for carbon-neutral power and logistics by ~15–25%, boosting supplier bargaining power for renewables and low-emission carriers.

These costs are hard to avoid, so Intercos secures multi-year fixed or indexed contracts (3–7 years typical) to smooth input-price volatility and protect margins.

Supplier Consolidation in the Chemical Industry

Ongoing mergers and acquisitions among global chemical distributors cut active suppliers by about 22% from 2018–2024, raising supplier concentration and squeezing Intercos’s bargaining leverage.

Fewer suppliers mean Intercos can’t easily play vendors off each other for price or terms, pressuring gross margins—raw material spend was 28% of sales in 2024.

To secure supply and innovation, Intercos must invest in deep strategic partnerships and long‑term contracts for priority access to patented molecules and formulations.

Sustainability and Compliance Standards

Suppliers compliant with ESG and REACH standards command premiums; studies show ESG-compliant chemical suppliers fetched 5–12% higher margins in 2024, narrowing Intercos’s vendor choices as brands demand full supply-chain transparency by 2025.

This shrinks Intercos’s pool to an estimated 30–40% of current vendors, raising supplier leverage and input-cost volatility because compliant suppliers have already invested in traceability and green processes.

- ESG/REACH-compliant suppliers: +5–12% pricing power

- Estimated compliant vendor pool for Intercos by 2025: 30–40%

- Higher supplier leverage increases input-cost volatility

Technological Integration with Key Vendors

Intercos co-develops formulations with primary chemical suppliers, creating deep technical interdependence that raises supplier switching costs and risks; re-testing and regulatory re-filing can take 6–12 months and cost €0.5–2.0 million per SKU, so suppliers hold strong leverage in negotiations.

Key vendors therefore capture bargaining power via R&D roles, access to proprietary chemistries, and supply continuity; estimates show top 3 suppliers can influence pricing on ~40–60% of strategic SKUs.

- Co-development raises switching cost: €0.5–2.0M and 6–12 months per SKU

- Technical interdependence concentrates leverage with key vendors

- Top 3 suppliers affect pricing on ~40–60% of strategic SKUs

Supplier strain: €700m procurement, 18% certified shortfall, top‑3 control 40–60%

Suppliers hold elevated leverage: certified inputs shortfall ~18% (2024–25) and compliant vendors only 30–40% of pool by 2025; procurement €700m (2024) but supplier concentration rose 22% (2018–24). Switching costs per SKU €0.5–2.0m and 6–12 months; top‑3 suppliers influence 40–60% of strategic SKUs; energy/logistics added ~9% to COGS in 2024.

| Metric | Value |

|---|---|

| Procurement (2024) | €700m |

| Certified supply shortfall | ~18% |

| Compliant vendor pool (2025) | 30–40% |

| Supplier concentration change (2018–24) | +22% |

| Switch cost per SKU | €0.5–2.0m; 6–12m |

| Top‑3 supplier influence | 40–60% SKUs |

| Energy/logistics COGS impact (2024) | ~9% |

What is included in the product

Tailored Porter's Five Forces analysis for Intercos that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its cosmetics manufacturing position.

Intercos Porter's Five Forces condensed into a single, slide-ready sheet—quickly gauge supplier, buyer, competitor, entrant, and substitute pressures to support fast, informed strategic moves.

Customers Bargaining Power

Concentration of Global Beauty Giants

A significant share of Intercos revenue—about 60% in 2024—comes from a handful of multinational beauty conglomerates, giving those clients strong bargaining power; they regularly extract sub-3% margin concessions, longer payment terms (90+ days), and exclusivity on formulations. These giants’ scale lets them demand R&D cost-sharing and priority production slots, squeezing Intercos’s EBITDA margin down from 11% in 2022 to roughly 8–9% by end-2025.

Rise of High-Growth Indie Brands

The rise of high-growth indie and influencer-led beauty brands has diversified Intercos’s customer mix, reducing reliance on global majors; by 2024 indie brands accounted for ~22% of global new product launches in prestige beauty, easing major clients’ leverage.

These small brands often lack R&D and full-service manufacturing, increasing dependence on Intercos’s end-to-end capabilities; Intercos reported ~38% of new client contracts in 2023 were full-service deals with indies.

Still, lower order volumes limit individual bargaining power—typical indie SKU runs are 5k–20k units versus >100k for prestige houses—so price and terms remain tilted toward larger established clients.

Low Switching Costs for Standard Formulations

Intercos’ strength in premium innovation contrasts with commodity formulations where switching costs are low; price-sensitive buyers can shift to contract manufacturers like Cosmax or Kolmar—Cosmax reported KRW 2.1 trillion revenue in 2024—pressuring margins on basic SKUs.

In 2024, top 20 retailers accounted for ~45% of global beauty sales, so major brands can reallocate volumes quickly; Intercos must keep investing in patented tech and bespoke R&D to protect loyalty and sustain ~12–15% gross margins on premium lines.

Demand for Rapid Innovation Cycles

Customers in 2025 demand shorter lead times and monthly product drops to match social media cycles, pushing Intercos to fast-track R&D and absorb inventory risk—Intercos reported a 12% YoY rise in bespoke short-run orders in 2024.

This customer-driven cadence gives buyers bargaining power in B2B terms because they can shift volumes rapidly and demand price concessions or priority, increasing Intercos’ working capital and R&D burn.

- Shorter lead times: monthly launches vs. quarterly

- 2024: 12% YoY rise in short-run orders

- Impact: higher working capital and R&D costs

Transparency and Ethical Sourcing Mandates

Prestige customers now require verifiable sustainability and ethical labor proof across supply chains; 68% of global luxury consumers (Bain, 2024) say this influences purchases, so Intercos must meet strict audits and traceability standards to keep top-brand contracts.

Missing certifications risks immediate loss of high-value accounts—luxury OEM deals often exceed €50m annually—so compliance directly protects revenue and margins.

- 68% luxury buyers value sustainability (Bain 2024)

- Top-brand contracts >€50m/yr at stake

- Audits, traceability, certifications required

Beauty giants tighten margins; indies lift demand—short runs, sustainability drive power

Major beauty conglomerates (60% revenue, 2024) hold strong leverage—sub-3% price cuts, 90+ day terms—pushing Intercos EBITDA toward 8–9% by 2025; indies (22% new launches, 2024) reduce concentration but lack scale, raising full-service demand (38% new contracts, 2023). Short-run orders rose 12% YoY (2024), sustainability audits (68% luxury buyers, Bain 2024) and commodity competition (Cosmax KRW 2.1T, 2024) keep buyer power high.

| Metric | Value |

|---|---|

| Top client share | 60% (2024) |

| Indie share new launches | 22% (2024) |

| Full-service indie deals | 38% (2023) |

| Short-run order growth | 12% YoY (2024) |

| Cosmax rev | KRW 2.1T (2024) |

Full Version Awaits

Intercos Porter's Five Forces Analysis

This preview shows the exact Intercos Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups. The document displayed is fully formatted and ready for download the moment you buy. You’re viewing the final, professionally written file that will be available to you instantly with no further setup required.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Intercos operates in a niche cosmetics-manufacturing market where supplier concentration and technical know-how raise entry barriers, while brand-driven buyer power and growing private-label demand intensify competition.

Regulatory complexity and raw-material volatility pose meaningful risks, yet Intercos’s R&D and scale offer defensive advantages against substitutes and rivals.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Intercos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Intercos depends on a complex supplier network for high‑grade pigments, actives, and sustainable compounds; scarcity of certified organic and ethically sourced inputs by late 2025 raised specialized suppliers’ leverage, with certified-supply shortfall estimated at ~18% industry-wide in 2024–25.

Intercos’s scale gives buying power—procurement spend exceeded €700m in 2024—but strict technical specs for prestige beauty shrink viable suppliers to a handful per ingredient, sustaining supplier bargaining power.

Energy and Logistics Cost Sensitivity

The cosmetics manufacturing is energy-intensive, so Intercos faces direct exposure to utility and logistics pricing; electricity can account for 6–12% of COGS in contract-manufacturing and diesel/logistics fuel added ~3–5% in 2024 for EU plants.

By end-2025 EU green-energy mandates and carbon pricing raised premiums for carbon-neutral power and logistics by ~15–25%, boosting supplier bargaining power for renewables and low-emission carriers.

These costs are hard to avoid, so Intercos secures multi-year fixed or indexed contracts (3–7 years typical) to smooth input-price volatility and protect margins.

Supplier Consolidation in the Chemical Industry

Ongoing mergers and acquisitions among global chemical distributors cut active suppliers by about 22% from 2018–2024, raising supplier concentration and squeezing Intercos’s bargaining leverage.

Fewer suppliers mean Intercos can’t easily play vendors off each other for price or terms, pressuring gross margins—raw material spend was 28% of sales in 2024.

To secure supply and innovation, Intercos must invest in deep strategic partnerships and long‑term contracts for priority access to patented molecules and formulations.

Sustainability and Compliance Standards

Suppliers compliant with ESG and REACH standards command premiums; studies show ESG-compliant chemical suppliers fetched 5–12% higher margins in 2024, narrowing Intercos’s vendor choices as brands demand full supply-chain transparency by 2025.

This shrinks Intercos’s pool to an estimated 30–40% of current vendors, raising supplier leverage and input-cost volatility because compliant suppliers have already invested in traceability and green processes.

- ESG/REACH-compliant suppliers: +5–12% pricing power

- Estimated compliant vendor pool for Intercos by 2025: 30–40%

- Higher supplier leverage increases input-cost volatility

Technological Integration with Key Vendors

Intercos co-develops formulations with primary chemical suppliers, creating deep technical interdependence that raises supplier switching costs and risks; re-testing and regulatory re-filing can take 6–12 months and cost €0.5–2.0 million per SKU, so suppliers hold strong leverage in negotiations.

Key vendors therefore capture bargaining power via R&D roles, access to proprietary chemistries, and supply continuity; estimates show top 3 suppliers can influence pricing on ~40–60% of strategic SKUs.

- Co-development raises switching cost: €0.5–2.0M and 6–12 months per SKU

- Technical interdependence concentrates leverage with key vendors

- Top 3 suppliers affect pricing on ~40–60% of strategic SKUs

Supplier strain: €700m procurement, 18% certified shortfall, top‑3 control 40–60%

Suppliers hold elevated leverage: certified inputs shortfall ~18% (2024–25) and compliant vendors only 30–40% of pool by 2025; procurement €700m (2024) but supplier concentration rose 22% (2018–24). Switching costs per SKU €0.5–2.0m and 6–12 months; top‑3 suppliers influence 40–60% of strategic SKUs; energy/logistics added ~9% to COGS in 2024.

| Metric | Value |

|---|---|

| Procurement (2024) | €700m |

| Certified supply shortfall | ~18% |

| Compliant vendor pool (2025) | 30–40% |

| Supplier concentration change (2018–24) | +22% |

| Switch cost per SKU | €0.5–2.0m; 6–12m |

| Top‑3 supplier influence | 40–60% SKUs |

| Energy/logistics COGS impact (2024) | ~9% |

What is included in the product

Tailored Porter's Five Forces analysis for Intercos that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its cosmetics manufacturing position.

Intercos Porter's Five Forces condensed into a single, slide-ready sheet—quickly gauge supplier, buyer, competitor, entrant, and substitute pressures to support fast, informed strategic moves.

Customers Bargaining Power

Concentration of Global Beauty Giants

A significant share of Intercos revenue—about 60% in 2024—comes from a handful of multinational beauty conglomerates, giving those clients strong bargaining power; they regularly extract sub-3% margin concessions, longer payment terms (90+ days), and exclusivity on formulations. These giants’ scale lets them demand R&D cost-sharing and priority production slots, squeezing Intercos’s EBITDA margin down from 11% in 2022 to roughly 8–9% by end-2025.

Rise of High-Growth Indie Brands

The rise of high-growth indie and influencer-led beauty brands has diversified Intercos’s customer mix, reducing reliance on global majors; by 2024 indie brands accounted for ~22% of global new product launches in prestige beauty, easing major clients’ leverage.

These small brands often lack R&D and full-service manufacturing, increasing dependence on Intercos’s end-to-end capabilities; Intercos reported ~38% of new client contracts in 2023 were full-service deals with indies.

Still, lower order volumes limit individual bargaining power—typical indie SKU runs are 5k–20k units versus >100k for prestige houses—so price and terms remain tilted toward larger established clients.

Low Switching Costs for Standard Formulations

Intercos’ strength in premium innovation contrasts with commodity formulations where switching costs are low; price-sensitive buyers can shift to contract manufacturers like Cosmax or Kolmar—Cosmax reported KRW 2.1 trillion revenue in 2024—pressuring margins on basic SKUs.

In 2024, top 20 retailers accounted for ~45% of global beauty sales, so major brands can reallocate volumes quickly; Intercos must keep investing in patented tech and bespoke R&D to protect loyalty and sustain ~12–15% gross margins on premium lines.

Demand for Rapid Innovation Cycles

Customers in 2025 demand shorter lead times and monthly product drops to match social media cycles, pushing Intercos to fast-track R&D and absorb inventory risk—Intercos reported a 12% YoY rise in bespoke short-run orders in 2024.

This customer-driven cadence gives buyers bargaining power in B2B terms because they can shift volumes rapidly and demand price concessions or priority, increasing Intercos’ working capital and R&D burn.

- Shorter lead times: monthly launches vs. quarterly

- 2024: 12% YoY rise in short-run orders

- Impact: higher working capital and R&D costs

Transparency and Ethical Sourcing Mandates

Prestige customers now require verifiable sustainability and ethical labor proof across supply chains; 68% of global luxury consumers (Bain, 2024) say this influences purchases, so Intercos must meet strict audits and traceability standards to keep top-brand contracts.

Missing certifications risks immediate loss of high-value accounts—luxury OEM deals often exceed €50m annually—so compliance directly protects revenue and margins.

- 68% luxury buyers value sustainability (Bain 2024)

- Top-brand contracts >€50m/yr at stake

- Audits, traceability, certifications required

Beauty giants tighten margins; indies lift demand—short runs, sustainability drive power

Major beauty conglomerates (60% revenue, 2024) hold strong leverage—sub-3% price cuts, 90+ day terms—pushing Intercos EBITDA toward 8–9% by 2025; indies (22% new launches, 2024) reduce concentration but lack scale, raising full-service demand (38% new contracts, 2023). Short-run orders rose 12% YoY (2024), sustainability audits (68% luxury buyers, Bain 2024) and commodity competition (Cosmax KRW 2.1T, 2024) keep buyer power high.

| Metric | Value |

|---|---|

| Top client share | 60% (2024) |

| Indie share new launches | 22% (2024) |

| Full-service indie deals | 38% (2023) |

| Short-run order growth | 12% YoY (2024) |

| Cosmax rev | KRW 2.1T (2024) |

Full Version Awaits

Intercos Porter's Five Forces Analysis

This preview shows the exact Intercos Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups. The document displayed is fully formatted and ready for download the moment you buy. You’re viewing the final, professionally written file that will be available to you instantly with no further setup required.