Interfor PESTLE Analysis

Skip the Research. Get the Strategy.

Uncover how political shifts, market cycles, and sustainability trends are reshaping Interfor’s outlook with our targeted PESTLE Analysis—perfect for investors and strategists seeking actionable external insight. Purchase the full report to access detailed risks, growth drivers, and ready-to-use recommendations that will sharpen your decisions and save research time.

Political factors

US-Canada Softwood Lumber Dispute

The ongoing US-Canada softwood lumber dispute remains a primary political hurdle for Interfor, with US countervailing and anti-dumping duties on Canadian softwood varying between 6% and 20% in late 2025, driving margin pressure on US-bound shipments.

Interfor reported that US exports accounted for roughly 45% of its 2024 sales; duties and periodic retroactive assessments have raised landed costs by an estimated CAD 30–50/mbf on affected shipments.

These fluctuating tariffs force Interfor to pursue geographic diversification of assets and sales — including increased investment in US mills and Asian market expansion — to mitigate tariff-related financial risks and stabilize cash flows.

Government Housing Initiatives

Indigenous Land Rights and Sovereignty

In British Columbia, unresolved Indigenous land title claims and treaty negotiations directly affect timber harvest levels; BC reported Indigenous-led agreements reducing available Crown harvest by up to 10% in some regions by 2024, impacting companies like Interfor that rely on provincial licences.

Interfor must maintain long-term partnerships with First Nations—over 200 Indigenous communities in BC—securing fibre access through tenure transfers, revenue-sharing and joint ventures to stabilize supply and capital allocation.

Recent legal rulings and the BC Declaration on the Rights of Indigenous Peoples Act implementation (2019–2025) have prompted reclassifications of land-use and conservation areas, with estimated regional harvest volume reductions of 5–15% in disputed territories.

Carbon Pricing and Climate Policy

Government carbon taxes and emissions caps raise Interfor’s manufacturing costs; British Columbia’s 2024 carbon tax reached CA$70/tCO2e, while EU ETS prices averaged ~€90/t in 2024, implying material cost pressure across its mills and export markets.

Net-zero commitments by 2050 push stricter reporting and cap compliance—Interfor reported Scope 1+2 emissions of ~0.35 tCO2e/m3 in 2023, so regulatory tightening could require increased capital for fuel-switching and efficiency.

Policy incentives can benefit Interfor if timber gains recognition as low-carbon: lifecycle studies show cross-laminated timber can store ~0.9 tCO2e/m3, improving public procurement prospects and market share in low-carbon construction.

- Higher carbon prices (CA$70/t in BC; €90/t EU ETS) => increased operational costs

- Net-zero by 2050 => greater reporting/capex for emissions reduction (Interfor Scope 1+2 ~0.35 tCO2e/m3 in 2023)

- Opportunity: wood’s carbon storage (~0.9 tCO2e/m3 for CLT) boosts public procurement potential

Trade Protectionism and Global Relations

Broader geopolitical shifts and rising protectionism can disrupt flows of lumber and sawmill equipment; in 2024 tariffs and quotas contributed to a 7% decline in Canadian softwood lumber exports to the US and altered trade routes to Asia.

New export restrictions or changes to trade agreements reduce Interfor’s competitiveness in offshore markets such as China and Japan, where the company sold roughly 15% of volumes in 2023.

Political instability in key export regions increases logistics risk and revenue volatility; port disruptions or sanctions can add weeks to transit and raise costs by an estimated 3–5% per shipment.

- 2024 tariffs/quotas linked to 7% fall in Canada→US lumber flows

- ~15% of Interfor volumes exported to Asian markets in 2023

- Port disruptions can add 3–5% per-shipment cost and weeks of delay

Tariffs, taxes and US demand reshape Canadian lumber — 6–20% duties, CAD30–50/mbf impact

US-Canada softwood duties (6–20% in late 2025) and CAD30–50/mbf landed-cost hits; US sales ~45% of 2024 revenue; housing policies (US$65bn+ incentives 2024–25) lifted N.A. starts ~9–12% in 2024; BC Indigenous agreements cut regional Crown harvest 5–15%; BC carbon tax CA$70/t (2024) and EU ETS ~€90/t raise costs; exports to Asia ~15% of volumes (2023); 2024 tariffs cut Canada→US flows ~7%.

| Metric | Value |

|---|---|

| US sales (2024) | ~45% |

| Asia volumes (2023) | ~15% |

| Softwood duties (late 2025) | 6–20% |

| BC carbon tax (2024) | CA$70/t |

| EU ETS (2024) | ~€90/t |

| Canada→US flow change (2024) | -7% |

What is included in the product

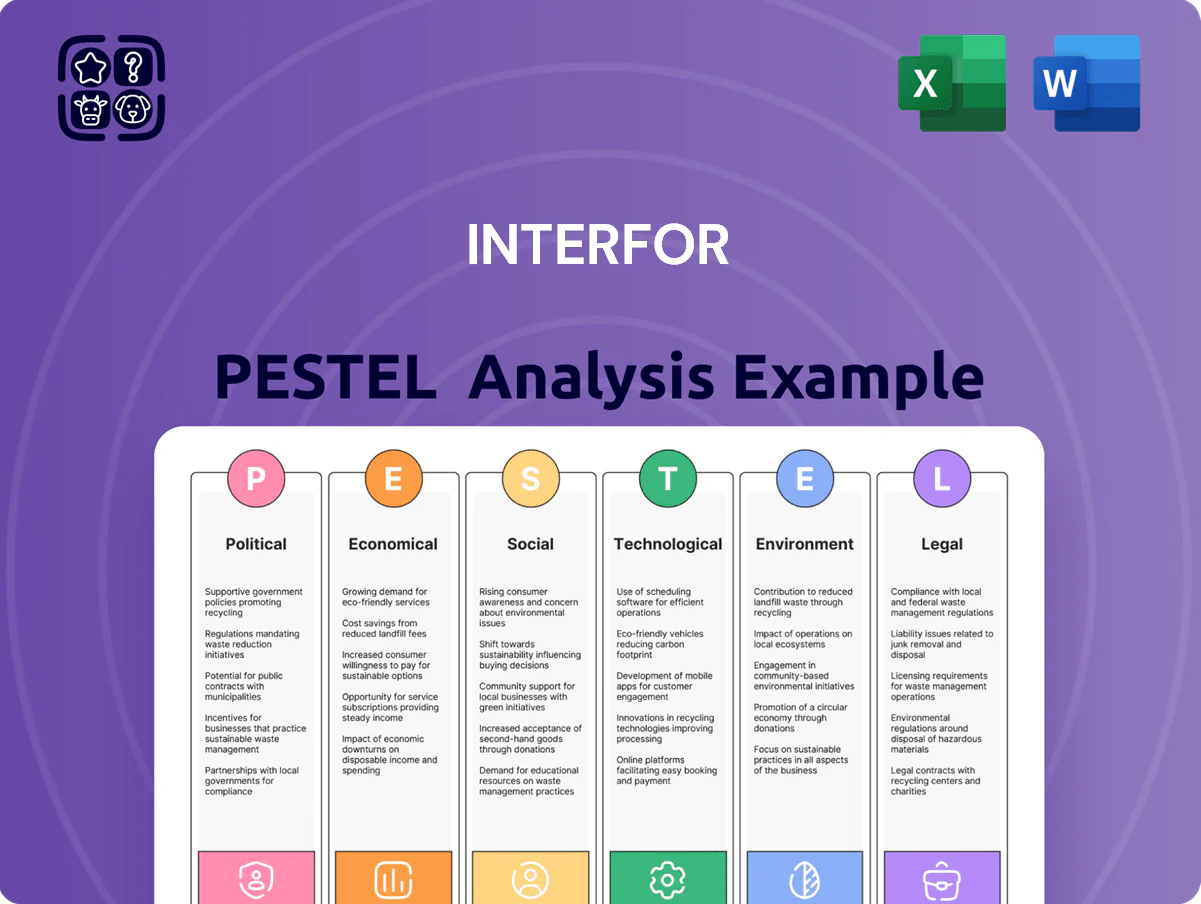

Explores how external macro-environmental factors uniquely affect Interfor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented PESTLE summary for Interfor that simplifies external risk analysis and can be dropped directly into presentations or strategy packs for quick cross-team alignment.

Economic factors

Interest Rates and Mortgage Affordability

Housing Market Dynamics

North American housing health—US existing-home inventory at a 2.6-month supply (Dec 2025) and median single-family home price up ~5% year-over-year—directly impacts Interfor’s lumber revenues and margins.

A persistent US single-family shortage—estimated 4.4 million-unit deficit by 2025—creates a structural floor for lumber demand despite cyclical swings.

Interfor’s planners monitor starts, permits and prices weekly to adjust production and inventory; housing starts of ~1.3M annualized (Q4 2025) guide mill utilization decisions.

Currency Exchange Rate Volatility

Interfor’s CAD/USD exposure is material: in 2024 the average CAD/USD rate was ~0.74, so a weaker CAD boosts Canadian lumber export competitiveness but raised reported costs on US$-denominated debt and CapEx; Interfor held roughly US$200–300m of foreign currency liabilities in recent filings, amplifying FX-driven EBITDA volatility. Financial analysts must model FX swings into quarterly earnings and cash-flow forecasts using sensitivity scenarios (±5–10%).

Labor Market Inflation

- Wage growth ~5.1% y/y (Canada, 2024)

- Rural CPI ~3–4% (2024)

- Peer EBITDA margins ~12–14% (2024)

Global Supply Chain and Logistics Costs

Rising transport costs—US rail rates up ~12% in 2024 and diesel averaging $4.10/gal in North America—directly pressure Interfor’s margins when shipping finished lumber by rail, truck, or ocean; ocean freight volatility (Shanghai–LA spot rates swinging 40% in 2024) raises per-unit delivered costs.

Logistical bottlenecks and port delays increased lead times by 10–20% in 2023–24, raising inventory and customer service costs; optimizing Interfor’s distribution network and modal mix is crucial to protect profitability amid fuel-price and freight-rate swings.

- Rail rate +12% (2024) impacts domestic costs

- Diesel ≈ $4.10/gal (2024) raises trucking expenses

- Ocean spot volatility ~±40% (2024) alters export margins

- Port delays ↑ lead times 10–20% (2023–24)

High rates crush lumber margins as US starts plunge, FX and costs squeeze 2024–25

High rates (5.25–5.50% in 2023–24) cut US housing starts ~25–30%, crushing SPF prices >40% from 2021 and squeezing Interfor margins; forecasts expect rate cuts H2 2025 to revive demand. CAD/USD ~0.74 in 2024, US$200–300m FX liabilities; wage growth ~5.1% and rural CPI 3–4% raised OPEX; rail +12% and diesel ~$4.10/gal lifted logistics costs.

| Metric | 2024–25 |

|---|---|

| US starts change | -25–30% |

| SPF price drop | >-40% vs 2021 |

| CAD/USD | ~0.74 |

| FX liabilities | US$200–300m |

| Wage growth (CA) | ~5.1% |

| Rail rates | +12% |

| Diesel | $4.10/gal |

What You See Is What You Get

Interfor PESTLE Analysis

The preview shown here is the exact Interfor PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Uncover how political shifts, market cycles, and sustainability trends are reshaping Interfor’s outlook with our targeted PESTLE Analysis—perfect for investors and strategists seeking actionable external insight. Purchase the full report to access detailed risks, growth drivers, and ready-to-use recommendations that will sharpen your decisions and save research time.

Political factors

US-Canada Softwood Lumber Dispute

The ongoing US-Canada softwood lumber dispute remains a primary political hurdle for Interfor, with US countervailing and anti-dumping duties on Canadian softwood varying between 6% and 20% in late 2025, driving margin pressure on US-bound shipments.

Interfor reported that US exports accounted for roughly 45% of its 2024 sales; duties and periodic retroactive assessments have raised landed costs by an estimated CAD 30–50/mbf on affected shipments.

These fluctuating tariffs force Interfor to pursue geographic diversification of assets and sales — including increased investment in US mills and Asian market expansion — to mitigate tariff-related financial risks and stabilize cash flows.

Government Housing Initiatives

Indigenous Land Rights and Sovereignty

In British Columbia, unresolved Indigenous land title claims and treaty negotiations directly affect timber harvest levels; BC reported Indigenous-led agreements reducing available Crown harvest by up to 10% in some regions by 2024, impacting companies like Interfor that rely on provincial licences.

Interfor must maintain long-term partnerships with First Nations—over 200 Indigenous communities in BC—securing fibre access through tenure transfers, revenue-sharing and joint ventures to stabilize supply and capital allocation.

Recent legal rulings and the BC Declaration on the Rights of Indigenous Peoples Act implementation (2019–2025) have prompted reclassifications of land-use and conservation areas, with estimated regional harvest volume reductions of 5–15% in disputed territories.

Carbon Pricing and Climate Policy

Government carbon taxes and emissions caps raise Interfor’s manufacturing costs; British Columbia’s 2024 carbon tax reached CA$70/tCO2e, while EU ETS prices averaged ~€90/t in 2024, implying material cost pressure across its mills and export markets.

Net-zero commitments by 2050 push stricter reporting and cap compliance—Interfor reported Scope 1+2 emissions of ~0.35 tCO2e/m3 in 2023, so regulatory tightening could require increased capital for fuel-switching and efficiency.

Policy incentives can benefit Interfor if timber gains recognition as low-carbon: lifecycle studies show cross-laminated timber can store ~0.9 tCO2e/m3, improving public procurement prospects and market share in low-carbon construction.

- Higher carbon prices (CA$70/t in BC; €90/t EU ETS) => increased operational costs

- Net-zero by 2050 => greater reporting/capex for emissions reduction (Interfor Scope 1+2 ~0.35 tCO2e/m3 in 2023)

- Opportunity: wood’s carbon storage (~0.9 tCO2e/m3 for CLT) boosts public procurement potential

Trade Protectionism and Global Relations

Broader geopolitical shifts and rising protectionism can disrupt flows of lumber and sawmill equipment; in 2024 tariffs and quotas contributed to a 7% decline in Canadian softwood lumber exports to the US and altered trade routes to Asia.

New export restrictions or changes to trade agreements reduce Interfor’s competitiveness in offshore markets such as China and Japan, where the company sold roughly 15% of volumes in 2023.

Political instability in key export regions increases logistics risk and revenue volatility; port disruptions or sanctions can add weeks to transit and raise costs by an estimated 3–5% per shipment.

- 2024 tariffs/quotas linked to 7% fall in Canada→US lumber flows

- ~15% of Interfor volumes exported to Asian markets in 2023

- Port disruptions can add 3–5% per-shipment cost and weeks of delay

Tariffs, taxes and US demand reshape Canadian lumber — 6–20% duties, CAD30–50/mbf impact

US-Canada softwood duties (6–20% in late 2025) and CAD30–50/mbf landed-cost hits; US sales ~45% of 2024 revenue; housing policies (US$65bn+ incentives 2024–25) lifted N.A. starts ~9–12% in 2024; BC Indigenous agreements cut regional Crown harvest 5–15%; BC carbon tax CA$70/t (2024) and EU ETS ~€90/t raise costs; exports to Asia ~15% of volumes (2023); 2024 tariffs cut Canada→US flows ~7%.

| Metric | Value |

|---|---|

| US sales (2024) | ~45% |

| Asia volumes (2023) | ~15% |

| Softwood duties (late 2025) | 6–20% |

| BC carbon tax (2024) | CA$70/t |

| EU ETS (2024) | ~€90/t |

| Canada→US flow change (2024) | -7% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Interfor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented PESTLE summary for Interfor that simplifies external risk analysis and can be dropped directly into presentations or strategy packs for quick cross-team alignment.

Economic factors

Interest Rates and Mortgage Affordability

Housing Market Dynamics

North American housing health—US existing-home inventory at a 2.6-month supply (Dec 2025) and median single-family home price up ~5% year-over-year—directly impacts Interfor’s lumber revenues and margins.

A persistent US single-family shortage—estimated 4.4 million-unit deficit by 2025—creates a structural floor for lumber demand despite cyclical swings.

Interfor’s planners monitor starts, permits and prices weekly to adjust production and inventory; housing starts of ~1.3M annualized (Q4 2025) guide mill utilization decisions.

Currency Exchange Rate Volatility

Interfor’s CAD/USD exposure is material: in 2024 the average CAD/USD rate was ~0.74, so a weaker CAD boosts Canadian lumber export competitiveness but raised reported costs on US$-denominated debt and CapEx; Interfor held roughly US$200–300m of foreign currency liabilities in recent filings, amplifying FX-driven EBITDA volatility. Financial analysts must model FX swings into quarterly earnings and cash-flow forecasts using sensitivity scenarios (±5–10%).

Labor Market Inflation

- Wage growth ~5.1% y/y (Canada, 2024)

- Rural CPI ~3–4% (2024)

- Peer EBITDA margins ~12–14% (2024)

Global Supply Chain and Logistics Costs

Rising transport costs—US rail rates up ~12% in 2024 and diesel averaging $4.10/gal in North America—directly pressure Interfor’s margins when shipping finished lumber by rail, truck, or ocean; ocean freight volatility (Shanghai–LA spot rates swinging 40% in 2024) raises per-unit delivered costs.

Logistical bottlenecks and port delays increased lead times by 10–20% in 2023–24, raising inventory and customer service costs; optimizing Interfor’s distribution network and modal mix is crucial to protect profitability amid fuel-price and freight-rate swings.

- Rail rate +12% (2024) impacts domestic costs

- Diesel ≈ $4.10/gal (2024) raises trucking expenses

- Ocean spot volatility ~±40% (2024) alters export margins

- Port delays ↑ lead times 10–20% (2023–24)

High rates crush lumber margins as US starts plunge, FX and costs squeeze 2024–25

High rates (5.25–5.50% in 2023–24) cut US housing starts ~25–30%, crushing SPF prices >40% from 2021 and squeezing Interfor margins; forecasts expect rate cuts H2 2025 to revive demand. CAD/USD ~0.74 in 2024, US$200–300m FX liabilities; wage growth ~5.1% and rural CPI 3–4% raised OPEX; rail +12% and diesel ~$4.10/gal lifted logistics costs.

| Metric | 2024–25 |

|---|---|

| US starts change | -25–30% |

| SPF price drop | >-40% vs 2021 |

| CAD/USD | ~0.74 |

| FX liabilities | US$200–300m |

| Wage growth (CA) | ~5.1% |

| Rail rates | +12% |

| Diesel | $4.10/gal |

What You See Is What You Get

Interfor PESTLE Analysis

The preview shown here is the exact Interfor PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or surprises.