Interzero Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

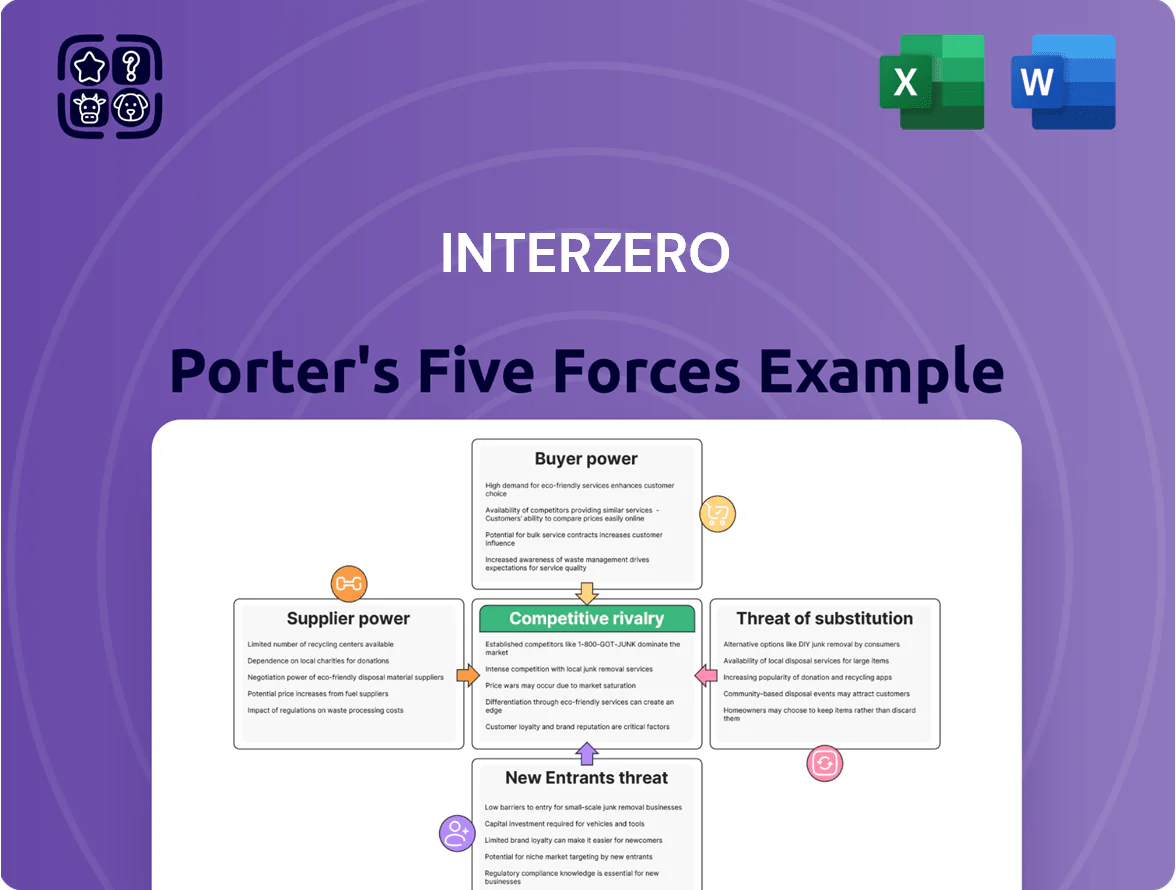

Interzero faces moderate supplier leverage, rising buyer expectations, and evolving substitute threats amid regulatory shifts and circular-economy opportunities; competitive rivalry is intensifying as players scale services and tech. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Interzero’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of waste sources

The vast majority of Interzero’s waste suppliers—over 90%—are small, fragmented generators such as retail shops and light industry sites, so no single supplier can push prices materially; this fragmentation keeps supplier-side bargaining weak. As of 2024 Interzero handled ~12 million tonnes of municipal and commercial waste across Europe, which bolsters its leverage in negotiating collection fees and long-term contracts.

Dependence on specialized logistics providers

Interzero handles large volumes but depends on specialized haulers for heavy waste; in 2024 transport accounted for about 12% of waste-to-recycling direct costs in Europe, so carriers matter.

Fuel price swings (diesel rose ~18% in 2022–23) and driver shortages—EU vacancy rate 4.5% for logistics in 2023—give providers short-term leverage at renewals.

Interzero limits risk by using a broad partner network—over 50 certified carriers in Germany by 2024—avoiding single-supplier dependence.

Technology and sorting equipment vendors

Technology and sorting equipment vendors have moderate bargaining power: only about 8–10 global high-tech providers supply proprietary optical and AI-driven sorters required for >95% purity targets in secondary materials, so switching costs are high.

Interzero’s 2024 capex of ~€120m and 1.2 Mtpa processing scale secure volume discounts and multi-year service contracts, letting Interzero negotiate lower lifetime costs and spare-parts access despite supplier concentration.

Scarcity of high-quality plastic streams

Scarcity of high-quality plastic streams has raised supplier leverage: by Q3 2025 demand for clean, easily recyclable plastic rose ~30% after EU Packaging and Packaging Waste Regulation updates, pushing prices for pre-sorted feedstock up ~18% year-over-year.

Interzero secures long-term contracts with industrial partners (multi-year deals covering ~40–60% of input volumes) to lock quality and hedge spot-price volatility.

- Demand up ~30% by Q3 2025

- Feedstock prices +18% YoY

- Interzero long-term contracts cover ~40–60% inputs

- Contracts reduce supply volatility and quality risk

Regulatory influence on municipal supply

Interzero scales vs rising feedstock & plastic demand—risk tempered by long-term contracts

Supplier power is mixed: fragmented small waste generators keep pressure low, but municipal tenders (7–15 yrs, ~70% household waste) and scarce high-quality plastic (+30% demand by Q3 2025, feedstock +18% YoY) raise leverage; transport and sorter vendors exert moderate power; Interzero’s scale (~12 Mt handled 2024, €120m capex, 1.2 Mtpa) and 40–60% long-term input contracts reduce risk.

| Metric | Value |

|---|---|

| Waste handled (2024) | ~12 Mt |

| Capex (2024) | €120m |

| Long-term input cover | 40–60% |

| High-quality plastic demand (Q3 2025) | +30% |

| Feedstock price YoY | +18% |

What is included in the product

Comprehensive Porter's Five Forces analysis for Interzero that uncovers competitive drivers, supplier/buyer power, barriers to entry, substitutes, and emerging threats with strategic implications for pricing and market positioning.

Concise Porter's Five Forces snapshot for Interzero—quickly spot competitive pressures and strategic levers to relieve pain points in procurement, pricing, and market entry decisions.

Customers Bargaining Power

Strict corporate sustainability mandates

By end-2025, strict ESG and circular-economy rules force 72% of S&P 500 firms to report scope 3 and recycled-content metrics, raising demand for Interzero’s certified secondary raw materials and recycling services; this dependence lowers customer price sensitivity as 58% of surveyed corporates (2024 Deloitte) say they’ll pay premiums for guaranteed compliance. Large clients often accept 5–12% higher costs to avoid regulatory fines and supply-chain disruption.

Volume-based negotiation from large retailers

Standardization of secondary raw materials

As recycled plastics and metals become global commodities—EU secondary plastic prices fell ~12% in 2024 to €620/ton—industrial buyers can easily switch recyclers if secondary-material pricing lags, boosting customer bargaining power.

Interzero counters this by selling high-purity grades tailored to manufacturers; in 2024 its specialty-output premium averaged €140/ton above commodity grades, preserving loyalty and reducing price-driven churn.

Switching costs for integrated circular services

Interzero embeds consulting, waste audits, and tailored recycling systems into client supply chains, creating high switching costs since rivals would need a full process overhaul; studies show integrated waste service contracts retain clients 30–45% longer than standalone collections (2024 EU waste services report).

This deep integration reduces customer bargaining power over time, as termination risks operational disruption and potential €0.5–2.5M implementation costs for mid-size manufacturers (2023 vendor case studies).

- Integrated services = high switching cost

- Client retention +30–45% (2024 EU report)

- Exit cost €0.5–2.5M for mid-size firms (2023 cases)

- Bargaining power weakens over contract life

Regulatory pressure for recycled content

New EU and German laws since 2024 mandate minimum recycled content in packaging (EU Packaging Regulation proposal: 30% for certain plastics by 2030), boosting demand for Interzero’s secondary materials and shifting bargaining power toward suppliers of recycled feedstock.

Manufacturers legally must buy recycled inputs, keeping volumes steady even in downturns; recycling rates rose 6.5% in 2024, and Interzero reported a 12% revenue increase in 2024 from recycled-material sales.

- Mandatory recycled content: ~30% target by 2030

- 2024 recycling volumes +6.5%

- Interzero recycled sales +12% in 2024

- Manufacturers face limited alternatives due to legal requirements

Retailer power meets premium: Interzero boosts retention + margins amid 2030 recycling push

Customers hold moderate-to-high bargaining power: large retailers supply 60%+ waste volumes and run €5–20m tenders, pushing fees down, while regulation (30% recycled-content target by 2030) and 72% of S&P500 reporting needs increase willingness to pay premiums; Interzero’s integrated services, specialty-grade premium €140/ton (2024) and client retention +30–45% blunt price pressure.

| Metric | Value |

|---|---|

| Retailers’ share of waste volumes | 60%+ |

| Avg contract size | €5–20m |

| EU recycled-content target (proposal) | ~30% by 2030 |

| Interzero specialty premium | €140/ton (2024) |

| Client retention lift | +30–45% (2024 EU report) |

What You See Is What You Get

Interzero Porter's Five Forces Analysis

This preview shows the exact Interzero Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Interzero faces moderate supplier leverage, rising buyer expectations, and evolving substitute threats amid regulatory shifts and circular-economy opportunities; competitive rivalry is intensifying as players scale services and tech. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Interzero’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of waste sources

The vast majority of Interzero’s waste suppliers—over 90%—are small, fragmented generators such as retail shops and light industry sites, so no single supplier can push prices materially; this fragmentation keeps supplier-side bargaining weak. As of 2024 Interzero handled ~12 million tonnes of municipal and commercial waste across Europe, which bolsters its leverage in negotiating collection fees and long-term contracts.

Dependence on specialized logistics providers

Interzero handles large volumes but depends on specialized haulers for heavy waste; in 2024 transport accounted for about 12% of waste-to-recycling direct costs in Europe, so carriers matter.

Fuel price swings (diesel rose ~18% in 2022–23) and driver shortages—EU vacancy rate 4.5% for logistics in 2023—give providers short-term leverage at renewals.

Interzero limits risk by using a broad partner network—over 50 certified carriers in Germany by 2024—avoiding single-supplier dependence.

Technology and sorting equipment vendors

Technology and sorting equipment vendors have moderate bargaining power: only about 8–10 global high-tech providers supply proprietary optical and AI-driven sorters required for >95% purity targets in secondary materials, so switching costs are high.

Interzero’s 2024 capex of ~€120m and 1.2 Mtpa processing scale secure volume discounts and multi-year service contracts, letting Interzero negotiate lower lifetime costs and spare-parts access despite supplier concentration.

Scarcity of high-quality plastic streams

Scarcity of high-quality plastic streams has raised supplier leverage: by Q3 2025 demand for clean, easily recyclable plastic rose ~30% after EU Packaging and Packaging Waste Regulation updates, pushing prices for pre-sorted feedstock up ~18% year-over-year.

Interzero secures long-term contracts with industrial partners (multi-year deals covering ~40–60% of input volumes) to lock quality and hedge spot-price volatility.

- Demand up ~30% by Q3 2025

- Feedstock prices +18% YoY

- Interzero long-term contracts cover ~40–60% inputs

- Contracts reduce supply volatility and quality risk

Regulatory influence on municipal supply

Interzero scales vs rising feedstock & plastic demand—risk tempered by long-term contracts

Supplier power is mixed: fragmented small waste generators keep pressure low, but municipal tenders (7–15 yrs, ~70% household waste) and scarce high-quality plastic (+30% demand by Q3 2025, feedstock +18% YoY) raise leverage; transport and sorter vendors exert moderate power; Interzero’s scale (~12 Mt handled 2024, €120m capex, 1.2 Mtpa) and 40–60% long-term input contracts reduce risk.

| Metric | Value |

|---|---|

| Waste handled (2024) | ~12 Mt |

| Capex (2024) | €120m |

| Long-term input cover | 40–60% |

| High-quality plastic demand (Q3 2025) | +30% |

| Feedstock price YoY | +18% |

What is included in the product

Comprehensive Porter's Five Forces analysis for Interzero that uncovers competitive drivers, supplier/buyer power, barriers to entry, substitutes, and emerging threats with strategic implications for pricing and market positioning.

Concise Porter's Five Forces snapshot for Interzero—quickly spot competitive pressures and strategic levers to relieve pain points in procurement, pricing, and market entry decisions.

Customers Bargaining Power

Strict corporate sustainability mandates

By end-2025, strict ESG and circular-economy rules force 72% of S&P 500 firms to report scope 3 and recycled-content metrics, raising demand for Interzero’s certified secondary raw materials and recycling services; this dependence lowers customer price sensitivity as 58% of surveyed corporates (2024 Deloitte) say they’ll pay premiums for guaranteed compliance. Large clients often accept 5–12% higher costs to avoid regulatory fines and supply-chain disruption.

Volume-based negotiation from large retailers

Standardization of secondary raw materials

As recycled plastics and metals become global commodities—EU secondary plastic prices fell ~12% in 2024 to €620/ton—industrial buyers can easily switch recyclers if secondary-material pricing lags, boosting customer bargaining power.

Interzero counters this by selling high-purity grades tailored to manufacturers; in 2024 its specialty-output premium averaged €140/ton above commodity grades, preserving loyalty and reducing price-driven churn.

Switching costs for integrated circular services

Interzero embeds consulting, waste audits, and tailored recycling systems into client supply chains, creating high switching costs since rivals would need a full process overhaul; studies show integrated waste service contracts retain clients 30–45% longer than standalone collections (2024 EU waste services report).

This deep integration reduces customer bargaining power over time, as termination risks operational disruption and potential €0.5–2.5M implementation costs for mid-size manufacturers (2023 vendor case studies).

- Integrated services = high switching cost

- Client retention +30–45% (2024 EU report)

- Exit cost €0.5–2.5M for mid-size firms (2023 cases)

- Bargaining power weakens over contract life

Regulatory pressure for recycled content

New EU and German laws since 2024 mandate minimum recycled content in packaging (EU Packaging Regulation proposal: 30% for certain plastics by 2030), boosting demand for Interzero’s secondary materials and shifting bargaining power toward suppliers of recycled feedstock.

Manufacturers legally must buy recycled inputs, keeping volumes steady even in downturns; recycling rates rose 6.5% in 2024, and Interzero reported a 12% revenue increase in 2024 from recycled-material sales.

- Mandatory recycled content: ~30% target by 2030

- 2024 recycling volumes +6.5%

- Interzero recycled sales +12% in 2024

- Manufacturers face limited alternatives due to legal requirements

Retailer power meets premium: Interzero boosts retention + margins amid 2030 recycling push

Customers hold moderate-to-high bargaining power: large retailers supply 60%+ waste volumes and run €5–20m tenders, pushing fees down, while regulation (30% recycled-content target by 2030) and 72% of S&P500 reporting needs increase willingness to pay premiums; Interzero’s integrated services, specialty-grade premium €140/ton (2024) and client retention +30–45% blunt price pressure.

| Metric | Value |

|---|---|

| Retailers’ share of waste volumes | 60%+ |

| Avg contract size | €5–20m |

| EU recycled-content target (proposal) | ~30% by 2030 |

| Interzero specialty premium | €140/ton (2024) |

| Client retention lift | +30–45% (2024 EU report) |

What You See Is What You Get

Interzero Porter's Five Forces Analysis

This preview shows the exact Interzero Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for download.