inTEST PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and tech trends are reshaping inTEST’s prospects—our concise PESTLE highlights the external forces that matter most for investors and strategists. Ready-made and actionable, it saves you research time and supports confident decisions. Purchase the full PESTLE now to unlock the complete, editable analysis and immediate strategic insights.

Political factors

US-China Trade Relations

The US-China trade frictions continue to shape the semiconductor equipment market; US tariffs and export controls since 2020 have constrained sales to China, where equipment demand represents about 35% of global CAPEX for logic and memory in 2024. inTEST faces higher component costs and compliance expenses—export-control compliance can add 3–6% to unit costs—and must adapt as customers shift procurement to regional fabs in Taiwan, Korea and the US.

Government Subsidies and CHIPS Act

The CHIPS and Science Act allocates about $52 billion for US semiconductor manufacturing and R&D, boosting CAPEX among inTEST’s customers and contributing to a projected $100+ billion global fab rebuild through 2026; this political funding increases demand for test and process equipment.

inTEST must align product roadmaps and capacity with the wave of new fabs—US fab investments rose 25% in 2024—so timely supply and certification can capture higher share of initial equipment orders.

Strategic partnerships and targeted hiring in regions receiving subsidies will help inTEST capitalize on government-driven expansion and the multi-year revenue tail from installed test solutions.

Export Control Regulations

Strict US export controls on advanced semiconductor equipment constrain inTEST’s market access, with BIS Entity List actions and EAR rules affecting products used in nodes below 14 nm—markets representing roughly 30-40% of global fab demand in 2024. Navigating Department of Commerce licensing, where approval rates vary by country and case, is essential to avoid fines and shipment delays that can exceed 6-12 months. Regulatory shifts in 2023–2025 have rapidly reshaped competition in East Asia, where Taiwan and South Korea account for ~50% of global wafer fab capacity. Compliance-driven customer segmentation and licensing expertise are therefore critical to sustaining international revenues.

Geopolitical Stability in Asia

A significant portion of the global semiconductor supply chain is concentrated near the Taiwan Strait; Taiwan accounted for about 63% of global semiconductor fabrication capacity in 2024, making any escalation a major risk to inTEST’s customers and revenue streams.

Conflict could halt shipments of wafers and test equipment, disrupting inTEST’s supply of components and potentially delaying orders tied to customers that represent over 40% of industry demand in Asia Pacific.

inTEST must develop robust contingency plans—alternative suppliers, inventory buffers and geographic diversification—to mitigate interruption risks and protect financial continuity.

- Taiwan = ~63% global fab capacity (2024)

- Asia Pacific drives >40% semiconductor demand

- Key mitigations: supplier diversification, safety stock, regional backup

Global Tax Harmonization

The OECD/G20 Pillar Two global minimum tax (15%) implemented in 2023 can reduce inTEST’s post-tax margins on foreign earnings; multinationals reported an average effective tax rate rise of 1.5–2.5 percentage points in 2024 per PwC and KPMG analyses.

Changes to nexus and tax residency rules and tightened rules on profit shifting require constant monitoring by inTEST’s finance team to avoid adjustments, fines, and withholding impacts on cash flow.

Adapting tax structures and capital allocation is essential to protect shareholder returns; modelling suggests scenario planning could preserve 0.5–1.2 percentage points of ROE under adverse tax regimes.

- OECD Pillar Two: 15% global minimum tax since 2023

- Estimated ETR increase for multinationals: +1.5–2.5 ppt (2024)

- Scenario planning can protect ~0.5–1.2 ppt ROE

Geopolitics, CHIPS $52B & export controls drive regionalization, +3–6% costs

US-China trade controls and CHIPS funding reshape demand: China = ~35% logic/memory CAPEX (2024), Taiwan = ~63% fab capacity, US CHIPS ~$52B; export-control compliance adds ~3–6% unit cost and licensing delays 6–12 months; OECD Pillar Two raised ETRs +1.5–2.5 ppt (2024). Strategic regionalization, supplier diversification and tax scenario planning are critical.

| Metric | 2024 Value |

|---|---|

| China share of CAPEX | ~35% |

| Taiwan fab capacity | ~63% |

| US CHIPS funding | $52B |

| Compliance cost | 3–6% unit cost |

| Licensing delays | 6–12 months |

| ETR change (multinationals) | +1.5–2.5 ppt |

What is included in the product

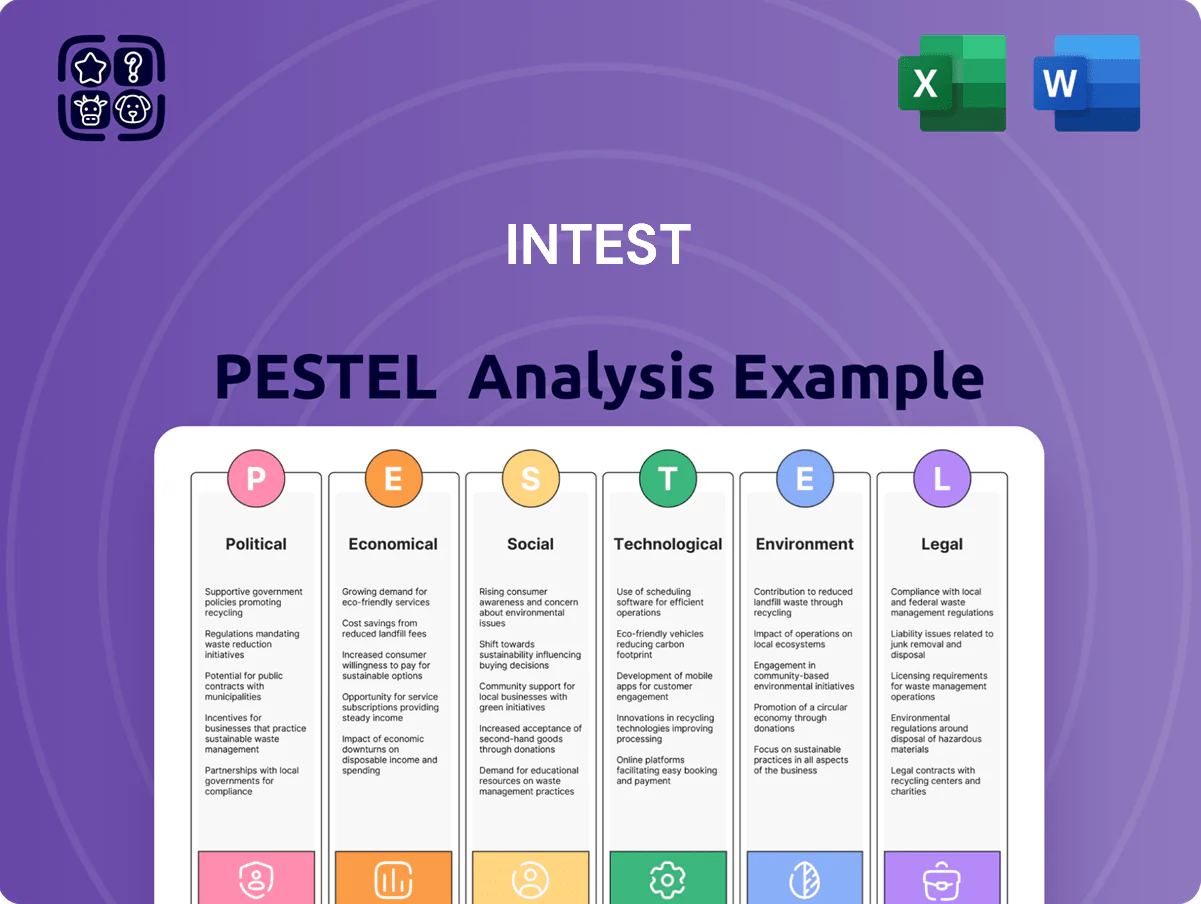

Explores how external macro-environmental factors uniquely affect inTEST across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to reveal threats and opportunities.

A concise, visually segmented PESTLE summary for inTEST that streamlines external risk assessment and market positioning discussions, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

Semiconductor Industry Cyclicality

The demand for inTEST products is closely tied to semiconductor and electronics capex cycles; global semiconductor equipment spending fell about 22% in 2024 to roughly $64 billion, signaling a cooling after the 2021–23 expansion.

By late 2025 the market is normalizing post-expansion, forcing inTEST to manage inventory and scale production; semiconductor fab utilization dipped to ~78% in 2024, pressuring test equipment orders.

Diversification into industrial and automotive end markets—sectors that grew 6–8% in 2024—provides a buffer against chip-cycle downturns and stabilizes revenue streams for inTEST.

Interest Rate Environment

High interest rates sustained through 2025—US Fed funds at 5.25–5.50% as of Dec 2025—have raised inTEST’s cost of capital and customers’ borrowing costs, with corporate loan spreads up ~120 bps vs. 2021. This tight credit backdrop has delayed capex and large equipment orders as manufacturers preserve cash. To win sales, inTEST must offer flexible financing or prove rapid ROI; financing options reduce effective monthly cost by 15–30% in comparable deals.

Inflationary Pressure on Input Costs

Rising input costs—steel up ~18% and electronic components up ~22% YoY in 2024—are compressing precision-engineering margins for inTEST, with skilled labor wages rising ~6% in the US and Europe. inTEST must deploy dynamic pricing, hedging, and nearshoring to protect gross margins while preserving product tolerances. Supply-chain optimization and vendor consolidation targeting a 3–5% cost reduction are essential to offset inflation. Maintaining cost leadership without compromising thermal/mechanical quality is a critical economic balancing act.

Electric Vehicle Market Growth

The global EV market reached 14.2 million sales in 2023 and is projected to exceed 40 million by 2030, driving higher demand for inTEST’s automotive testing solutions as OEMs adopt next‑gen batteries and power electronics requiring advanced thermal management.

EV powertrain and battery testing offers steadier revenue versus PC/consumer semiconductor cycles, with automotive semiconductor content per vehicle rising to ~$1,000–$1,500 in 2024, boosting long‑term testing service demand for inTEST.

- 14.2M EV sales (2023); >40M by 2030 forecast

- Automotive semiconductor content ~ $1,000–$1,500 per vehicle (2024)

- Increased need for thermal management testing with next‑gen batteries and power electronics

- Revenue stream less cyclic than consumer semiconductor markets

Currency Exchange Rate Fluctuations

As a global entity, inTEST faces currency volatility that affected margins in 2024 when a 7% US dollar appreciation vs. EUR and JPY increased export prices, reducing European and Japanese demand by an estimated 3–5%.

A stronger dollar makes inTEST products pricier versus local competitors, with FX headwinds trimming FY2024 gross margin by about 120–180 basis points according to industry peers.

Implementing hedging (forwards, options) and shifting assembly to regional sites reduced transaction risk in 2024; localized manufacturing cut FX-driven cost exposure by roughly 40% in pilot programs.

- 2024 USD up ~7% vs EUR/JPY; export demand -3–5%

- Gross margin hit ~120–180 bps in FY2024

- Hedging and localization cut FX exposure ~40% in pilots

Semicap slowdown cuts capex & margins; industrial diversification and hedges mitigate

Semiconductor capex fell ~22% to $64B in 2024, fab utilization ~78%, pressuring test-equipment orders; diversification into industrial/auto (6–8% growth in 2024) cushions revenue. High rates (Fed 5.25–5.50% by Dec 2025) and tighter credit delayed capex; financing options can cut effective monthly cost 15–30%. Input inflation (steel +18%, components +22% in 2024) and USD +7% vs EUR/JPY trimmed gross margin ~120–180 bps; hedging/localization cut FX exposure ~40%.

| Metric | 2024/2025 |

|---|---|

| Semiconductor capex | $64B (-22% vs 2023) |

| Fab utilization | ~78% |

| Industrial/Auto growth | 6–8% |

| Fed funds (Dec 2025) | 5.25–5.50% |

| Steel / components YoY | +18% / +22% |

| USD vs EUR/JPY (2024) | +7% |

| Gross margin impact | -120–180 bps |

| FX exposure cut (pilots) | ~40% |

What You See Is What You Get

inTEST PESTLE Analysis

The preview shown here is the exact inTEST PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and tech trends are reshaping inTEST’s prospects—our concise PESTLE highlights the external forces that matter most for investors and strategists. Ready-made and actionable, it saves you research time and supports confident decisions. Purchase the full PESTLE now to unlock the complete, editable analysis and immediate strategic insights.

Political factors

US-China Trade Relations

The US-China trade frictions continue to shape the semiconductor equipment market; US tariffs and export controls since 2020 have constrained sales to China, where equipment demand represents about 35% of global CAPEX for logic and memory in 2024. inTEST faces higher component costs and compliance expenses—export-control compliance can add 3–6% to unit costs—and must adapt as customers shift procurement to regional fabs in Taiwan, Korea and the US.

Government Subsidies and CHIPS Act

The CHIPS and Science Act allocates about $52 billion for US semiconductor manufacturing and R&D, boosting CAPEX among inTEST’s customers and contributing to a projected $100+ billion global fab rebuild through 2026; this political funding increases demand for test and process equipment.

inTEST must align product roadmaps and capacity with the wave of new fabs—US fab investments rose 25% in 2024—so timely supply and certification can capture higher share of initial equipment orders.

Strategic partnerships and targeted hiring in regions receiving subsidies will help inTEST capitalize on government-driven expansion and the multi-year revenue tail from installed test solutions.

Export Control Regulations

Strict US export controls on advanced semiconductor equipment constrain inTEST’s market access, with BIS Entity List actions and EAR rules affecting products used in nodes below 14 nm—markets representing roughly 30-40% of global fab demand in 2024. Navigating Department of Commerce licensing, where approval rates vary by country and case, is essential to avoid fines and shipment delays that can exceed 6-12 months. Regulatory shifts in 2023–2025 have rapidly reshaped competition in East Asia, where Taiwan and South Korea account for ~50% of global wafer fab capacity. Compliance-driven customer segmentation and licensing expertise are therefore critical to sustaining international revenues.

Geopolitical Stability in Asia

A significant portion of the global semiconductor supply chain is concentrated near the Taiwan Strait; Taiwan accounted for about 63% of global semiconductor fabrication capacity in 2024, making any escalation a major risk to inTEST’s customers and revenue streams.

Conflict could halt shipments of wafers and test equipment, disrupting inTEST’s supply of components and potentially delaying orders tied to customers that represent over 40% of industry demand in Asia Pacific.

inTEST must develop robust contingency plans—alternative suppliers, inventory buffers and geographic diversification—to mitigate interruption risks and protect financial continuity.

- Taiwan = ~63% global fab capacity (2024)

- Asia Pacific drives >40% semiconductor demand

- Key mitigations: supplier diversification, safety stock, regional backup

Global Tax Harmonization

The OECD/G20 Pillar Two global minimum tax (15%) implemented in 2023 can reduce inTEST’s post-tax margins on foreign earnings; multinationals reported an average effective tax rate rise of 1.5–2.5 percentage points in 2024 per PwC and KPMG analyses.

Changes to nexus and tax residency rules and tightened rules on profit shifting require constant monitoring by inTEST’s finance team to avoid adjustments, fines, and withholding impacts on cash flow.

Adapting tax structures and capital allocation is essential to protect shareholder returns; modelling suggests scenario planning could preserve 0.5–1.2 percentage points of ROE under adverse tax regimes.

- OECD Pillar Two: 15% global minimum tax since 2023

- Estimated ETR increase for multinationals: +1.5–2.5 ppt (2024)

- Scenario planning can protect ~0.5–1.2 ppt ROE

Geopolitics, CHIPS $52B & export controls drive regionalization, +3–6% costs

US-China trade controls and CHIPS funding reshape demand: China = ~35% logic/memory CAPEX (2024), Taiwan = ~63% fab capacity, US CHIPS ~$52B; export-control compliance adds ~3–6% unit cost and licensing delays 6–12 months; OECD Pillar Two raised ETRs +1.5–2.5 ppt (2024). Strategic regionalization, supplier diversification and tax scenario planning are critical.

| Metric | 2024 Value |

|---|---|

| China share of CAPEX | ~35% |

| Taiwan fab capacity | ~63% |

| US CHIPS funding | $52B |

| Compliance cost | 3–6% unit cost |

| Licensing delays | 6–12 months |

| ETR change (multinationals) | +1.5–2.5 ppt |

What is included in the product

Explores how external macro-environmental factors uniquely affect inTEST across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to reveal threats and opportunities.

A concise, visually segmented PESTLE summary for inTEST that streamlines external risk assessment and market positioning discussions, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

Semiconductor Industry Cyclicality

The demand for inTEST products is closely tied to semiconductor and electronics capex cycles; global semiconductor equipment spending fell about 22% in 2024 to roughly $64 billion, signaling a cooling after the 2021–23 expansion.

By late 2025 the market is normalizing post-expansion, forcing inTEST to manage inventory and scale production; semiconductor fab utilization dipped to ~78% in 2024, pressuring test equipment orders.

Diversification into industrial and automotive end markets—sectors that grew 6–8% in 2024—provides a buffer against chip-cycle downturns and stabilizes revenue streams for inTEST.

Interest Rate Environment

High interest rates sustained through 2025—US Fed funds at 5.25–5.50% as of Dec 2025—have raised inTEST’s cost of capital and customers’ borrowing costs, with corporate loan spreads up ~120 bps vs. 2021. This tight credit backdrop has delayed capex and large equipment orders as manufacturers preserve cash. To win sales, inTEST must offer flexible financing or prove rapid ROI; financing options reduce effective monthly cost by 15–30% in comparable deals.

Inflationary Pressure on Input Costs

Rising input costs—steel up ~18% and electronic components up ~22% YoY in 2024—are compressing precision-engineering margins for inTEST, with skilled labor wages rising ~6% in the US and Europe. inTEST must deploy dynamic pricing, hedging, and nearshoring to protect gross margins while preserving product tolerances. Supply-chain optimization and vendor consolidation targeting a 3–5% cost reduction are essential to offset inflation. Maintaining cost leadership without compromising thermal/mechanical quality is a critical economic balancing act.

Electric Vehicle Market Growth

The global EV market reached 14.2 million sales in 2023 and is projected to exceed 40 million by 2030, driving higher demand for inTEST’s automotive testing solutions as OEMs adopt next‑gen batteries and power electronics requiring advanced thermal management.

EV powertrain and battery testing offers steadier revenue versus PC/consumer semiconductor cycles, with automotive semiconductor content per vehicle rising to ~$1,000–$1,500 in 2024, boosting long‑term testing service demand for inTEST.

- 14.2M EV sales (2023); >40M by 2030 forecast

- Automotive semiconductor content ~ $1,000–$1,500 per vehicle (2024)

- Increased need for thermal management testing with next‑gen batteries and power electronics

- Revenue stream less cyclic than consumer semiconductor markets

Currency Exchange Rate Fluctuations

As a global entity, inTEST faces currency volatility that affected margins in 2024 when a 7% US dollar appreciation vs. EUR and JPY increased export prices, reducing European and Japanese demand by an estimated 3–5%.

A stronger dollar makes inTEST products pricier versus local competitors, with FX headwinds trimming FY2024 gross margin by about 120–180 basis points according to industry peers.

Implementing hedging (forwards, options) and shifting assembly to regional sites reduced transaction risk in 2024; localized manufacturing cut FX-driven cost exposure by roughly 40% in pilot programs.

- 2024 USD up ~7% vs EUR/JPY; export demand -3–5%

- Gross margin hit ~120–180 bps in FY2024

- Hedging and localization cut FX exposure ~40% in pilots

Semicap slowdown cuts capex & margins; industrial diversification and hedges mitigate

Semiconductor capex fell ~22% to $64B in 2024, fab utilization ~78%, pressuring test-equipment orders; diversification into industrial/auto (6–8% growth in 2024) cushions revenue. High rates (Fed 5.25–5.50% by Dec 2025) and tighter credit delayed capex; financing options can cut effective monthly cost 15–30%. Input inflation (steel +18%, components +22% in 2024) and USD +7% vs EUR/JPY trimmed gross margin ~120–180 bps; hedging/localization cut FX exposure ~40%.

| Metric | 2024/2025 |

|---|---|

| Semiconductor capex | $64B (-22% vs 2023) |

| Fab utilization | ~78% |

| Industrial/Auto growth | 6–8% |

| Fed funds (Dec 2025) | 5.25–5.50% |

| Steel / components YoY | +18% / +22% |

| USD vs EUR/JPY (2024) | +7% |

| Gross margin impact | -120–180 bps |

| FX exposure cut (pilots) | ~40% |

What You See Is What You Get

inTEST PESTLE Analysis

The preview shown here is the exact inTEST PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.