Intrepid Potash Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

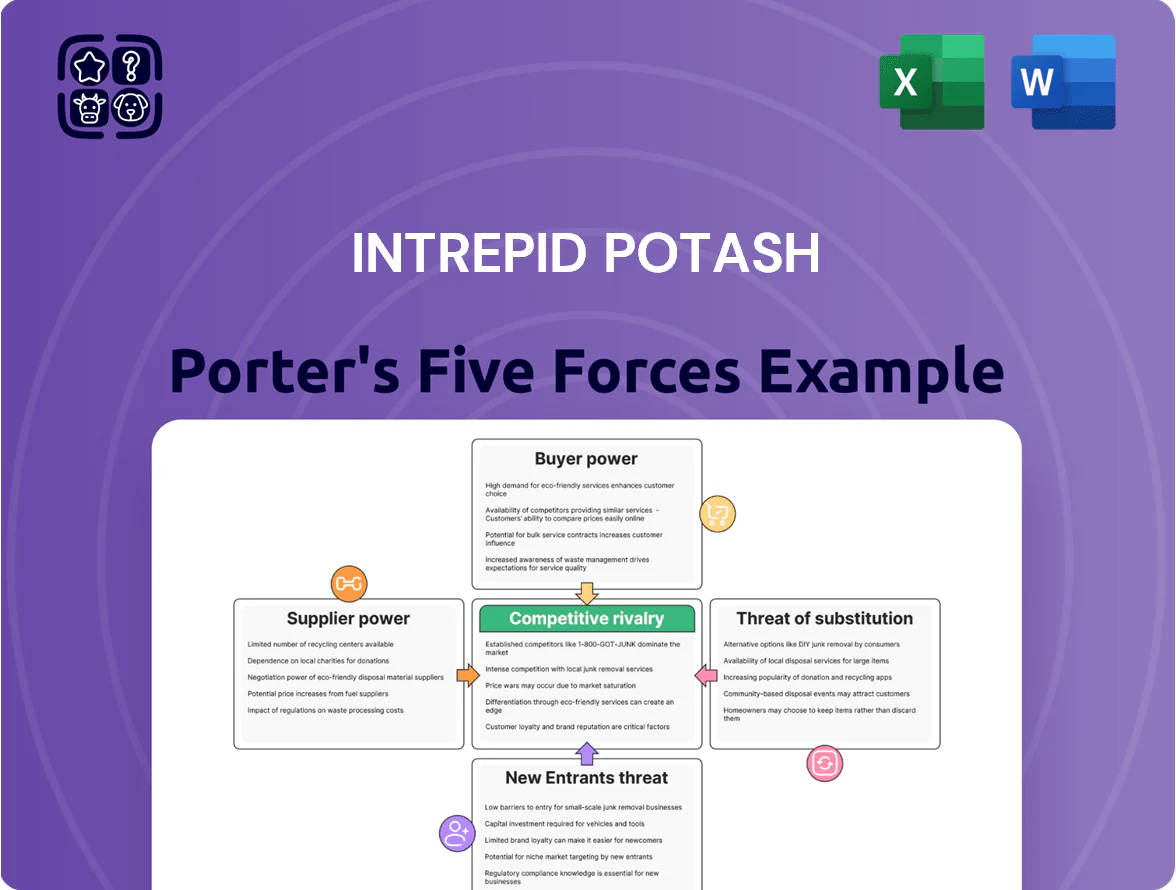

Intrepid Potash faces moderated buyer power and significant commodity price sensitivity, while supplier concentration and regulatory hurdles shape its margins—competitive rivalry remains intense among global fertilizer producers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Intrepid Potash’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy and Utility Dependency

Intrepid Potash depends on natural gas and grid electricity for solar evaporation and mining; in 2024 energy accounted for ~18% of operating costs, and US natural gas Henry Hub averaged $3.53/MMBtu in 2024, limiting cost control.

Global commodity-driven price swings give utility suppliers leverage; with few industrial-scale alternatives, supplier power raises input cost volatility and margin risk—energy spikes in 2022 raised operating margins by ~5 percentage points.

Specialized Mining Equipment Availability

The procurement of specialized heavy machinery and solar evaporation tech for Intrepid Potash faces concentrated supply: roughly 4–6 global vendors dominate high-capacity evaporators and mining rigs, giving suppliers pricing leverage and control over 9–18 month lead times; a single major vendor delay in 2024 forced a US potash producer to defer 20–30% of planned output, showing how supply disruption can raise capex by 10–25% and push production schedules back months.

Labor Market Dynamics

Operating solely in the United States, Intrepid Potash faces domestic labor swings; US Bureau of Labor Statistics data (Dec 2025) shows mining employment down 1.2% year-over-year, tightening skilled labor supply for potash operations.

Specialized potash mining skills give workers moderate bargaining power: wage growth for mining engineers averaged 4.5% in 2024, and Intrepid’s 2024 payroll was 28% of operating costs, raising sensitivity to wage hikes.

Competition from US mining and energy firms—where median mining engineer pay hit $107,000 in 2024—boosts talent mobility and increases recruitment costs, pressuring margins during tight labor markets.

Raw Material and Chemical Inputs

Intrepid produces brine but buys specialized reagents for magnesium chloride and salt processing; global chemical producers are concentrated, letting suppliers push prices—US specialty chemical margins rose to 16.8% in 2024 (ICIS), raising input cost risk for miners.

Supply concentration and limited substitutes make Intrepid exposed to input-price shocks; a 10% reagent price rise could cut adjusted EBITDA by ~3–5% based on 2024 gross margins.

- Own brine reduces raw-salt risk

- Specialty chemicals from consolidated suppliers

- 2024 specialty-chemical margin 16.8% (ICIS)

- 10% reagent price hike → ~3–5% EBITDA hit

Logistics and Transportation Providers

Intrepid Potash relies heavily on rail and trucking to move ~2–4 million tons of potash annually from Utah and New Mexico; Class I railroads act as regional monopolies, allowing freight-rate increases that squeezed margins—rail freight cost rises of ~6–9% in 2023–2024 raised per-ton transport expense materially vs. historical levels.

- ~2–4M tons shipped/year

- Rail rate hikes 6–9% (2023–24)

- Rail regional duopolies = pricing power

- Higher transport = lower gross margins

Supplier power squeezes margins: energy, reagents, rail hikes → 10% reagents = ~3–5% EBITDA

Suppliers hold moderate-to-high bargaining power: energy (18% of 2024 op costs; Henry Hub $3.53/MMBtu in 2024), concentrated reagent and equipment vendors, and regional rail duopolies raising transport costs (rail +6–9% 2023–24) increase input-price volatility and margin risk; a 10% reagent rise → ~3–5% adjusted EBITDA hit.

| Item | 2024 / Source |

|---|---|

| Energy share | ~18% op costs |

| Henry Hub | $3.53/MMBtu |

| Rail rate change | +6–9% (2023–24) |

| Reagent shock impact | 10% → ~3–5% EBITDA |

What is included in the product

Tailored Porter's Five Forces for Intrepid Potash, evaluating competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and strategic levers to protect margins and market position.

A concise Porter's Five Forces one-sheet for Intrepid Potash—quickly pinpoint competitive pressures and regulatory risks to streamline boardroom decisions.

Customers Bargaining Power

Consolidation of Agricultural Distributors

A large portion of Intrepid Potash sales flows through a handful of US agricultural cooperatives and retailers—Top 10 buyers account for roughly 45% of domestic potash purchases (USDA 2024)—giving them strong leverage to demand volume discounts and extended payment terms.

These buyers can switch suppliers quickly; spot price sensitivity rose after 2023 supply changes, pressuring Intrepid’s margins and forcing tighter contract pricing to retain volume.

Commodity Price Sensitivity

Primary buyers—farmers—have purchasing power tied to global crop prices and net farm income; U.S. net farm income fell 11% in 2024 to about $136 billion (USDA), so many delayed or cut fertilizer use, boosting buyer leverage. When corn and soybean futures slide (e.g., 2024 corn avg ~$4.50/bu), farmers shift to cheaper blends or cut rates, forcing Intrepid Potash to trim prices or offer credits to preserve volumes. This cyclical downturn clearly shifts bargaining power to buyers.

Industrial and Oilfield Demand

Customers in the oil and gas sector buy Intrepid Potash’s magnesium chloride and brine mainly for well completion and de-icing, so demand swings with energy prices—U.S. crude oil output rose ~2.5% in 2024, keeping demand volatile.

Industrial buyers have many suppliers and low switching costs, so they can shift volumes if Intrepid’s price is uncompetitive; spot brine/mag chloride prices fell ~8% in 2024 vs 2023.

That competition compresses margins: Intrepid reported non-agricultural sales represented ~18% of 2024 revenue, limiting its pricing power in this segment.

Low Switching Costs for Standardized Products

Potash and salt are commoditized; Intrepid Potash's products show minimal chemical or functional differentiation versus global peers, so buyers can substitute suppliers easily.

Low technical switching costs and simple logistics mean customers face little operational interruption when changing vendors, boosting buyer leverage.

In 2024 Intrepid sold ~1.1 million tonnes of potash equivalent; with global potash spot-market volatility ±15% in 2023–24, price competition raises buyer bargaining power.

- Commoditized product — low differentiation

- Minimal switching cost — easy substitution

- Low brand loyalty — stronger buyer leverage

- 2024 sales ~1.1 Mt potash eq; spot swings ±15%

Information Symmetry and Market Transparency

Global potash prices are publicly tracked on platforms like Argus and CRU; the benchmark average CFR Brazil potash price was about $360/tonne in Q4 2025, so buyers have clear negotiation anchors.

This transparency caps Intrepid Potash’s ability to charge premiums above market rates and lets large buyers leverage competing suppliers to push prices down.

- Benchmark price ~ $360/tonne (CFR Brazil, Q4 2025)

- High market transparency reduces premium potential

- Buyers pit producers to secure lowest price

Buyer Power Crushes Potash Margins: Top-10 ~45%, Intrepid 1.1Mt, ±15% spot swings

Buyers hold strong leverage: Top 10 buyers ~45% of US purchases (USDA 2024), product commoditized with low switching costs, and transparency (Argus/CRU) pins prices; Intrepid sold ~1.1 Mt potash eq in 2024 and non-ag sales ~18% revenue. Large buyers demand discounts, push tighter contract pricing, and shift volumes when crop prices or spot CFR benchmarks move (~±15% volatility 2023–24).

| Metric | 2024/2023 |

|---|---|

| Top-10 buyer share | ~45% |

| Intrepid sales | ~1.1 Mt potash eq (2024) |

| Non-ag revenue | ~18% |

| Spot volatility | ±15% (2023–24) |

Same Document Delivered

Intrepid Potash Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Intrepid Potash you'll receive upon purchase—no placeholders or mockups; fully formatted, professionally written, and ready for immediate download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Intrepid Potash faces moderated buyer power and significant commodity price sensitivity, while supplier concentration and regulatory hurdles shape its margins—competitive rivalry remains intense among global fertilizer producers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Intrepid Potash’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy and Utility Dependency

Intrepid Potash depends on natural gas and grid electricity for solar evaporation and mining; in 2024 energy accounted for ~18% of operating costs, and US natural gas Henry Hub averaged $3.53/MMBtu in 2024, limiting cost control.

Global commodity-driven price swings give utility suppliers leverage; with few industrial-scale alternatives, supplier power raises input cost volatility and margin risk—energy spikes in 2022 raised operating margins by ~5 percentage points.

Specialized Mining Equipment Availability

The procurement of specialized heavy machinery and solar evaporation tech for Intrepid Potash faces concentrated supply: roughly 4–6 global vendors dominate high-capacity evaporators and mining rigs, giving suppliers pricing leverage and control over 9–18 month lead times; a single major vendor delay in 2024 forced a US potash producer to defer 20–30% of planned output, showing how supply disruption can raise capex by 10–25% and push production schedules back months.

Labor Market Dynamics

Operating solely in the United States, Intrepid Potash faces domestic labor swings; US Bureau of Labor Statistics data (Dec 2025) shows mining employment down 1.2% year-over-year, tightening skilled labor supply for potash operations.

Specialized potash mining skills give workers moderate bargaining power: wage growth for mining engineers averaged 4.5% in 2024, and Intrepid’s 2024 payroll was 28% of operating costs, raising sensitivity to wage hikes.

Competition from US mining and energy firms—where median mining engineer pay hit $107,000 in 2024—boosts talent mobility and increases recruitment costs, pressuring margins during tight labor markets.

Raw Material and Chemical Inputs

Intrepid produces brine but buys specialized reagents for magnesium chloride and salt processing; global chemical producers are concentrated, letting suppliers push prices—US specialty chemical margins rose to 16.8% in 2024 (ICIS), raising input cost risk for miners.

Supply concentration and limited substitutes make Intrepid exposed to input-price shocks; a 10% reagent price rise could cut adjusted EBITDA by ~3–5% based on 2024 gross margins.

- Own brine reduces raw-salt risk

- Specialty chemicals from consolidated suppliers

- 2024 specialty-chemical margin 16.8% (ICIS)

- 10% reagent price hike → ~3–5% EBITDA hit

Logistics and Transportation Providers

Intrepid Potash relies heavily on rail and trucking to move ~2–4 million tons of potash annually from Utah and New Mexico; Class I railroads act as regional monopolies, allowing freight-rate increases that squeezed margins—rail freight cost rises of ~6–9% in 2023–2024 raised per-ton transport expense materially vs. historical levels.

- ~2–4M tons shipped/year

- Rail rate hikes 6–9% (2023–24)

- Rail regional duopolies = pricing power

- Higher transport = lower gross margins

Supplier power squeezes margins: energy, reagents, rail hikes → 10% reagents = ~3–5% EBITDA

Suppliers hold moderate-to-high bargaining power: energy (18% of 2024 op costs; Henry Hub $3.53/MMBtu in 2024), concentrated reagent and equipment vendors, and regional rail duopolies raising transport costs (rail +6–9% 2023–24) increase input-price volatility and margin risk; a 10% reagent rise → ~3–5% adjusted EBITDA hit.

| Item | 2024 / Source |

|---|---|

| Energy share | ~18% op costs |

| Henry Hub | $3.53/MMBtu |

| Rail rate change | +6–9% (2023–24) |

| Reagent shock impact | 10% → ~3–5% EBITDA |

What is included in the product

Tailored Porter's Five Forces for Intrepid Potash, evaluating competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and strategic levers to protect margins and market position.

A concise Porter's Five Forces one-sheet for Intrepid Potash—quickly pinpoint competitive pressures and regulatory risks to streamline boardroom decisions.

Customers Bargaining Power

Consolidation of Agricultural Distributors

A large portion of Intrepid Potash sales flows through a handful of US agricultural cooperatives and retailers—Top 10 buyers account for roughly 45% of domestic potash purchases (USDA 2024)—giving them strong leverage to demand volume discounts and extended payment terms.

These buyers can switch suppliers quickly; spot price sensitivity rose after 2023 supply changes, pressuring Intrepid’s margins and forcing tighter contract pricing to retain volume.

Commodity Price Sensitivity

Primary buyers—farmers—have purchasing power tied to global crop prices and net farm income; U.S. net farm income fell 11% in 2024 to about $136 billion (USDA), so many delayed or cut fertilizer use, boosting buyer leverage. When corn and soybean futures slide (e.g., 2024 corn avg ~$4.50/bu), farmers shift to cheaper blends or cut rates, forcing Intrepid Potash to trim prices or offer credits to preserve volumes. This cyclical downturn clearly shifts bargaining power to buyers.

Industrial and Oilfield Demand

Customers in the oil and gas sector buy Intrepid Potash’s magnesium chloride and brine mainly for well completion and de-icing, so demand swings with energy prices—U.S. crude oil output rose ~2.5% in 2024, keeping demand volatile.

Industrial buyers have many suppliers and low switching costs, so they can shift volumes if Intrepid’s price is uncompetitive; spot brine/mag chloride prices fell ~8% in 2024 vs 2023.

That competition compresses margins: Intrepid reported non-agricultural sales represented ~18% of 2024 revenue, limiting its pricing power in this segment.

Low Switching Costs for Standardized Products

Potash and salt are commoditized; Intrepid Potash's products show minimal chemical or functional differentiation versus global peers, so buyers can substitute suppliers easily.

Low technical switching costs and simple logistics mean customers face little operational interruption when changing vendors, boosting buyer leverage.

In 2024 Intrepid sold ~1.1 million tonnes of potash equivalent; with global potash spot-market volatility ±15% in 2023–24, price competition raises buyer bargaining power.

- Commoditized product — low differentiation

- Minimal switching cost — easy substitution

- Low brand loyalty — stronger buyer leverage

- 2024 sales ~1.1 Mt potash eq; spot swings ±15%

Information Symmetry and Market Transparency

Global potash prices are publicly tracked on platforms like Argus and CRU; the benchmark average CFR Brazil potash price was about $360/tonne in Q4 2025, so buyers have clear negotiation anchors.

This transparency caps Intrepid Potash’s ability to charge premiums above market rates and lets large buyers leverage competing suppliers to push prices down.

- Benchmark price ~ $360/tonne (CFR Brazil, Q4 2025)

- High market transparency reduces premium potential

- Buyers pit producers to secure lowest price

Buyer Power Crushes Potash Margins: Top-10 ~45%, Intrepid 1.1Mt, ±15% spot swings

Buyers hold strong leverage: Top 10 buyers ~45% of US purchases (USDA 2024), product commoditized with low switching costs, and transparency (Argus/CRU) pins prices; Intrepid sold ~1.1 Mt potash eq in 2024 and non-ag sales ~18% revenue. Large buyers demand discounts, push tighter contract pricing, and shift volumes when crop prices or spot CFR benchmarks move (~±15% volatility 2023–24).

| Metric | 2024/2023 |

|---|---|

| Top-10 buyer share | ~45% |

| Intrepid sales | ~1.1 Mt potash eq (2024) |

| Non-ag revenue | ~18% |

| Spot volatility | ±15% (2023–24) |

Same Document Delivered

Intrepid Potash Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Intrepid Potash you'll receive upon purchase—no placeholders or mockups; fully formatted, professionally written, and ready for immediate download and use.