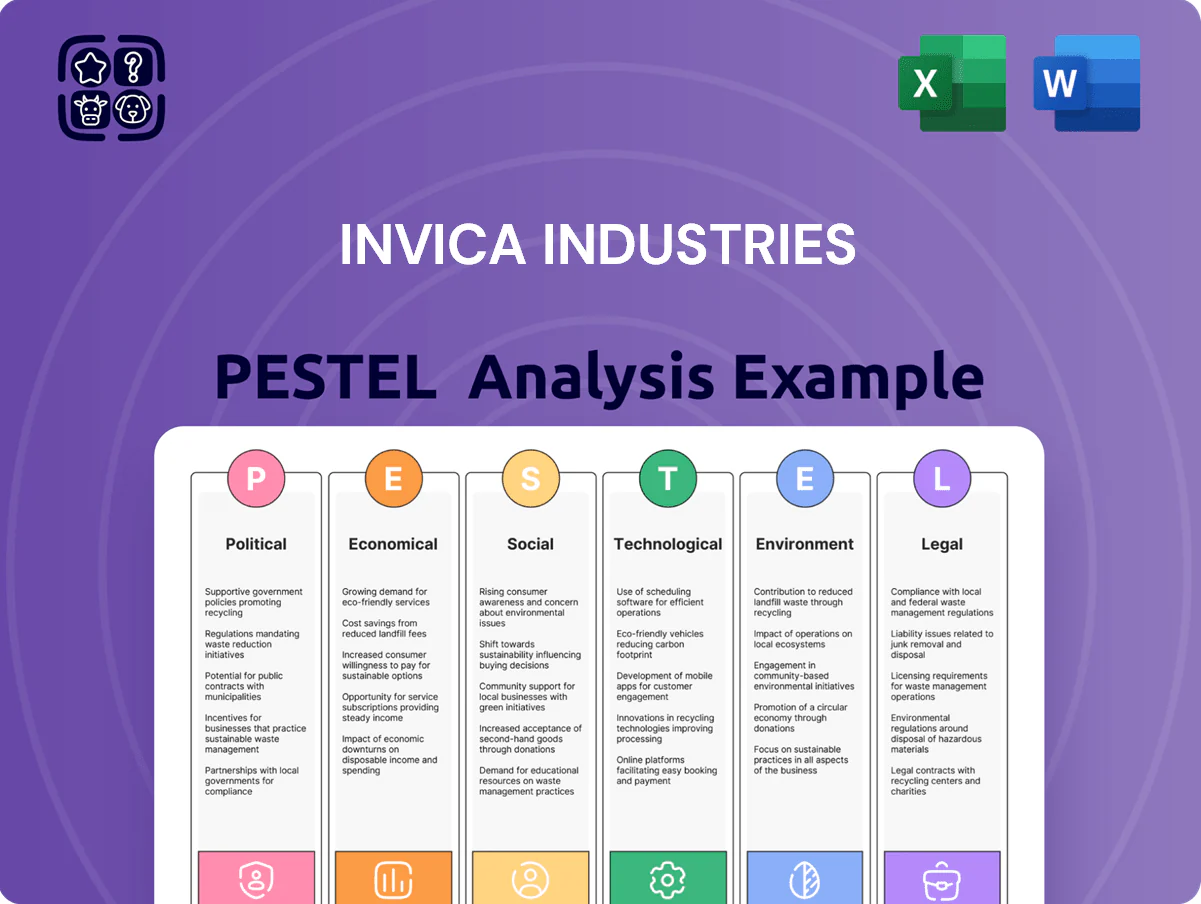

Invica Industries PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, supply-chain dynamics, and emerging technologies are reshaping Invica Industries' competitive landscape—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter strategy and investment decisions; purchase the full PESTLE analysis for a complete, actionable breakdown you can apply immediately.

Political factors

Global Trade Tariffs and Protectionism

Major economies' tariffs on steel and aluminum—US Section 232 duties (25% steel, 10% aluminum) and EU safeguard measures—raise Invica Industries' raw material costs, with global steel prices up ~15% in 2024 (avg $720/ton) versus 2023, squeezing margins.

As governments favor domestic producers, import duties can force price hikes for end-users or cut gross margin; Invica reported 2024 input-cost sensitivity of ~6% of revenue.

Diversifying suppliers across Asia, South America, and Europe is critical to hedge against abrupt policy shifts in top metal exporters like China, India, and Brazil.

Geopolitical Stability in Mining Regions

Political unrest in major non-ferrous ore regions like Peru and Zambia has in past years caused supply disruptions that pushed copper spot prices up 18% in 2024, highlighting risk to Invica Industries’ brass and copper sourcing.

Invica must continuously monitor political indicators across its primary hubs—Peru, Chile, Zambia—to safeguard a steady flow for industrial clients and preserve contract fulfillment.

Regional stability is essential to avoid force majeure triggers that could jeopardize long-term supply agreements and the company’s reliability as a key supplier.

Government Infrastructure Spending Initiatives

National programs to modernize infrastructure and expand renewable grids—backed by recent US Infrastructure Investment and Jobs Act allocations of ~$1.2 trillion through 2031 and EU green deal funding of €300 billion for 2024–27—drive steel, copper and aluminum demand, directly boosting Invica Industries’ ferrous/non-ferrous sales; aligning procurement and production to government fiscal cycles enables pursuit of multi-year public contracts often worth tens-to-hundreds of millions, securing volume and margin stability.

Export Control Regulations

Stringent export controls on critical minerals and recycled metal scrap—e.g., Indonesia’s 2023 nickel ore export limits and EU dual-use listings—shrink global supply of high-quality secondary materials, pushing prices up (nickel scrap prices rose ~18% in 2024) and raising sourcing costs for traders like Invica Industries.

Governments impose these measures to protect domestic industrial security, forcing trading firms into alternative markets or complex licensing; global trade compliance breaches can trigger fines exceeding millions of dollars and supply-chain disruptions.

Invica must continuously update trade-compliance protocols, invest in licensing capabilities, and monitor regulations across major markets (EU, US, China, Indonesia) to preserve its trusted intermediary status and avoid regulatory penalties.

- Export controls reduce available secondary material and inflate prices (~18% nickel scrap increase in 2024)

- Licensing complexity and sanctions risk can lead to multi-million-dollar fines

- Continuous compliance across EU, US, China, Indonesia required to maintain market access

Bilateral Trade Agreements

The signing of recent bilateral agreements—such as India–UAE CEPA (effective 2022) and ASEAN trade updates—reduces tariffs by up to 10–20% for industrial goods, granting Invica Industries preferential access to markets growing at 4–6% CAGR and lowering cross‑border admin costs by an estimated 8–12%.

Leveraging these frameworks can expand Invica’s footprint across 12+ emerging markets and enable competitive pricing that could improve export margins by 1–3 percentage points.

- Preferential tariffs: 10–20% reductions

- Market growth: 4–6% CAGR in targeted regions

- Admin cost savings: ~8–12%

- Potential export margin uplift: 1–3 pp

Geo-risk hikes input costs 6% of revenue; infrastructure & trade deals boost margins

Political risks—tariffs (US Section 232), export controls (Indonesia 2023), and unrest in Peru/Zambia—raised 2024 input costs ~6% of revenue; steel avg $720/ton (+15%), copper +18%, nickel scrap +18%. Infrastructure spending (US ~$1.2T thru 2031, EU €300B 2024–27) boosts demand; trade pacts (India–UAE CEPA) cut tariffs 10–20%, aiding 1–3pp export margin gains.

| Metric | 2024 |

|---|---|

| Steel price | $720/ton (+15%) |

| Copper | +18% |

| Nickel scrap | +18% |

| Input cost sensitivity | ~6% rev |

What is included in the product

Explores how external macro-environmental factors uniquely affect Invica Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify threats, opportunities, and strategic actions tailored to the company’s industry and region.

A concise, shareable PESTLE snapshot of Invica Industries that’s visually segmented for quick interpretation, easily dropped into presentations or planning sessions to streamline external risk discussions and team alignment.

Economic factors

Commodity Price Volatility

Fluctuations in global metal prices on the London Metal Exchange—copper down ~12% in 2024 from 2023 average and aluminum volatility ±18% YTD—directly affect Invica Industries' inventory valuation and pricing strategies, forcing mark-to-market adjustments and working capital swings. Rapid swings necessitate hedging: as of 2025 many peers report 60–80% coverage via forwards/options to shield margins. A flexible pricing model tied to LME indices is vital to preserve margins while staying competitive for price-sensitive industrial buyers.

Global Inflationary Pressures

Rising global inflation—headline CPI averaging 4.7% in advanced economies and energy price inflation near 15% in 2024—pushes up smelting energy costs, raw material and freight rates across the metal supply chain, raising Invica Industries’ input costs by an estimated 6–9% year-on-year.

The firm must balance passing costs to customers in heavy industry, construction and automotive without eroding demand; historical price elasticity in these sectors suggests limited tolerance for sustained price hikes above 5%.

Tracking core inflation (core CPI ~3.6% in 2024) enables Invica to model future cost trajectories, adjust procurement hedges and revise budgets to protect margins and sustain profitability.

Currency Exchange Rate Fluctuations

As an international trader, Invica Industries faces FX exposure that affected gross margins in 2024 when a 7% depreciation of the local currency vs USD raised COGS by roughly 4–6%, per company trade mix estimates; a 2025 IMF projection of 3–5% annual FX volatility increases this risk. Implementing forward contracts, FX options and multi-currency accounts can stabilize cash flow and hedge against market swings.

Industrial Production Growth Rates

Industrial production growth directly drives demand for copper, aluminum and steel; global manufacturing output fell 1.2% YoY in 2024, risking inventory buildup and lower trading volumes for Invica Industries.

Strong 2023–25 industrialization in India and Southeast Asia (manufacturing PMI averages >52) offers robust demand for raw materials across automotive, electronics and heavy machinery.

- 2024 global IP -1.2% YoY

- India/Southeast Asia PMI >52 (2023–25)

- Slowdown → inventory surplus, lower volumes

- Rapid industrialization → increased raw-material demand

Interest Rate Impact on Inventory Financing

High interest rates raise capital costs for maintaining large ferrous and non-ferrous inventories; global lending rates averaged 4.8% in 2025 vs 2.3% in 2021, squeezing margins in capital-intensive metal trading.

Invica Industries’ financing capacity and supply‑chain expansion hinge on monetary policy; tighter credit can slow growth and elevate short-term borrowing costs.

To preserve a healthy debt‑to‑equity ratio, Invica must optimize working capital, use inventory financing tools and negotiate lower-cost supply credit.

- Higher rates increase carrying costs and reduce ROIC

- Average metal trader leverage rose to ~2.1x in 2024

- Use of receivables financing and supplier credit mitigates rate impact

Input-cost shock: metal volatility, weaker demand, FX and rates squeeze margins

Metal price volatility (LME copper -12% in 2024; aluminum ±18% YTD) and 2024 global IP -1.2% cut margins and volumes; inflation (global CPI ~4.7%) raised input costs ~6–9%; FX swings (local currency -7% vs USD in 2024) increased COGS ~4–6%; higher rates (avg lending 4.8% in 2025) lift inventory carrying costs—hedging, flexible pricing and inventory financing are essential.

| Metric | 2024/2025 |

|---|---|

| LME copper | -12% (2024) |

| Aluminum volatility | ±18% YTD |

| Global IP | -1.2% YoY (2024) |

| Global CPI | 4.7% (2024) |

| FX move | Local -7% vs USD (2024) |

| Avg lending rate | 4.8% (2025) |

Preview Before You Purchase

Invica Industries PESTLE Analysis

The preview shown here is the exact Invica Industries PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The content and structure visible in the preview are the same file you’ll download immediately after payment. Everything displayed here is part of the final, professionally structured product.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, supply-chain dynamics, and emerging technologies are reshaping Invica Industries' competitive landscape—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter strategy and investment decisions; purchase the full PESTLE analysis for a complete, actionable breakdown you can apply immediately.

Political factors

Global Trade Tariffs and Protectionism

Major economies' tariffs on steel and aluminum—US Section 232 duties (25% steel, 10% aluminum) and EU safeguard measures—raise Invica Industries' raw material costs, with global steel prices up ~15% in 2024 (avg $720/ton) versus 2023, squeezing margins.

As governments favor domestic producers, import duties can force price hikes for end-users or cut gross margin; Invica reported 2024 input-cost sensitivity of ~6% of revenue.

Diversifying suppliers across Asia, South America, and Europe is critical to hedge against abrupt policy shifts in top metal exporters like China, India, and Brazil.

Geopolitical Stability in Mining Regions

Political unrest in major non-ferrous ore regions like Peru and Zambia has in past years caused supply disruptions that pushed copper spot prices up 18% in 2024, highlighting risk to Invica Industries’ brass and copper sourcing.

Invica must continuously monitor political indicators across its primary hubs—Peru, Chile, Zambia—to safeguard a steady flow for industrial clients and preserve contract fulfillment.

Regional stability is essential to avoid force majeure triggers that could jeopardize long-term supply agreements and the company’s reliability as a key supplier.

Government Infrastructure Spending Initiatives

National programs to modernize infrastructure and expand renewable grids—backed by recent US Infrastructure Investment and Jobs Act allocations of ~$1.2 trillion through 2031 and EU green deal funding of €300 billion for 2024–27—drive steel, copper and aluminum demand, directly boosting Invica Industries’ ferrous/non-ferrous sales; aligning procurement and production to government fiscal cycles enables pursuit of multi-year public contracts often worth tens-to-hundreds of millions, securing volume and margin stability.

Export Control Regulations

Stringent export controls on critical minerals and recycled metal scrap—e.g., Indonesia’s 2023 nickel ore export limits and EU dual-use listings—shrink global supply of high-quality secondary materials, pushing prices up (nickel scrap prices rose ~18% in 2024) and raising sourcing costs for traders like Invica Industries.

Governments impose these measures to protect domestic industrial security, forcing trading firms into alternative markets or complex licensing; global trade compliance breaches can trigger fines exceeding millions of dollars and supply-chain disruptions.

Invica must continuously update trade-compliance protocols, invest in licensing capabilities, and monitor regulations across major markets (EU, US, China, Indonesia) to preserve its trusted intermediary status and avoid regulatory penalties.

- Export controls reduce available secondary material and inflate prices (~18% nickel scrap increase in 2024)

- Licensing complexity and sanctions risk can lead to multi-million-dollar fines

- Continuous compliance across EU, US, China, Indonesia required to maintain market access

Bilateral Trade Agreements

The signing of recent bilateral agreements—such as India–UAE CEPA (effective 2022) and ASEAN trade updates—reduces tariffs by up to 10–20% for industrial goods, granting Invica Industries preferential access to markets growing at 4–6% CAGR and lowering cross‑border admin costs by an estimated 8–12%.

Leveraging these frameworks can expand Invica’s footprint across 12+ emerging markets and enable competitive pricing that could improve export margins by 1–3 percentage points.

- Preferential tariffs: 10–20% reductions

- Market growth: 4–6% CAGR in targeted regions

- Admin cost savings: ~8–12%

- Potential export margin uplift: 1–3 pp

Geo-risk hikes input costs 6% of revenue; infrastructure & trade deals boost margins

Political risks—tariffs (US Section 232), export controls (Indonesia 2023), and unrest in Peru/Zambia—raised 2024 input costs ~6% of revenue; steel avg $720/ton (+15%), copper +18%, nickel scrap +18%. Infrastructure spending (US ~$1.2T thru 2031, EU €300B 2024–27) boosts demand; trade pacts (India–UAE CEPA) cut tariffs 10–20%, aiding 1–3pp export margin gains.

| Metric | 2024 |

|---|---|

| Steel price | $720/ton (+15%) |

| Copper | +18% |

| Nickel scrap | +18% |

| Input cost sensitivity | ~6% rev |

What is included in the product

Explores how external macro-environmental factors uniquely affect Invica Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify threats, opportunities, and strategic actions tailored to the company’s industry and region.

A concise, shareable PESTLE snapshot of Invica Industries that’s visually segmented for quick interpretation, easily dropped into presentations or planning sessions to streamline external risk discussions and team alignment.

Economic factors

Commodity Price Volatility

Fluctuations in global metal prices on the London Metal Exchange—copper down ~12% in 2024 from 2023 average and aluminum volatility ±18% YTD—directly affect Invica Industries' inventory valuation and pricing strategies, forcing mark-to-market adjustments and working capital swings. Rapid swings necessitate hedging: as of 2025 many peers report 60–80% coverage via forwards/options to shield margins. A flexible pricing model tied to LME indices is vital to preserve margins while staying competitive for price-sensitive industrial buyers.

Global Inflationary Pressures

Rising global inflation—headline CPI averaging 4.7% in advanced economies and energy price inflation near 15% in 2024—pushes up smelting energy costs, raw material and freight rates across the metal supply chain, raising Invica Industries’ input costs by an estimated 6–9% year-on-year.

The firm must balance passing costs to customers in heavy industry, construction and automotive without eroding demand; historical price elasticity in these sectors suggests limited tolerance for sustained price hikes above 5%.

Tracking core inflation (core CPI ~3.6% in 2024) enables Invica to model future cost trajectories, adjust procurement hedges and revise budgets to protect margins and sustain profitability.

Currency Exchange Rate Fluctuations

As an international trader, Invica Industries faces FX exposure that affected gross margins in 2024 when a 7% depreciation of the local currency vs USD raised COGS by roughly 4–6%, per company trade mix estimates; a 2025 IMF projection of 3–5% annual FX volatility increases this risk. Implementing forward contracts, FX options and multi-currency accounts can stabilize cash flow and hedge against market swings.

Industrial Production Growth Rates

Industrial production growth directly drives demand for copper, aluminum and steel; global manufacturing output fell 1.2% YoY in 2024, risking inventory buildup and lower trading volumes for Invica Industries.

Strong 2023–25 industrialization in India and Southeast Asia (manufacturing PMI averages >52) offers robust demand for raw materials across automotive, electronics and heavy machinery.

- 2024 global IP -1.2% YoY

- India/Southeast Asia PMI >52 (2023–25)

- Slowdown → inventory surplus, lower volumes

- Rapid industrialization → increased raw-material demand

Interest Rate Impact on Inventory Financing

High interest rates raise capital costs for maintaining large ferrous and non-ferrous inventories; global lending rates averaged 4.8% in 2025 vs 2.3% in 2021, squeezing margins in capital-intensive metal trading.

Invica Industries’ financing capacity and supply‑chain expansion hinge on monetary policy; tighter credit can slow growth and elevate short-term borrowing costs.

To preserve a healthy debt‑to‑equity ratio, Invica must optimize working capital, use inventory financing tools and negotiate lower-cost supply credit.

- Higher rates increase carrying costs and reduce ROIC

- Average metal trader leverage rose to ~2.1x in 2024

- Use of receivables financing and supplier credit mitigates rate impact

Input-cost shock: metal volatility, weaker demand, FX and rates squeeze margins

Metal price volatility (LME copper -12% in 2024; aluminum ±18% YTD) and 2024 global IP -1.2% cut margins and volumes; inflation (global CPI ~4.7%) raised input costs ~6–9%; FX swings (local currency -7% vs USD in 2024) increased COGS ~4–6%; higher rates (avg lending 4.8% in 2025) lift inventory carrying costs—hedging, flexible pricing and inventory financing are essential.

| Metric | 2024/2025 |

|---|---|

| LME copper | -12% (2024) |

| Aluminum volatility | ±18% YTD |

| Global IP | -1.2% YoY (2024) |

| Global CPI | 4.7% (2024) |

| FX move | Local -7% vs USD (2024) |

| Avg lending rate | 4.8% (2025) |

Preview Before You Purchase

Invica Industries PESTLE Analysis

The preview shown here is the exact Invica Industries PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The content and structure visible in the preview are the same file you’ll download immediately after payment. Everything displayed here is part of the final, professionally structured product.