Inwido SWOT Analysis

Your Strategic Toolkit Starts Here

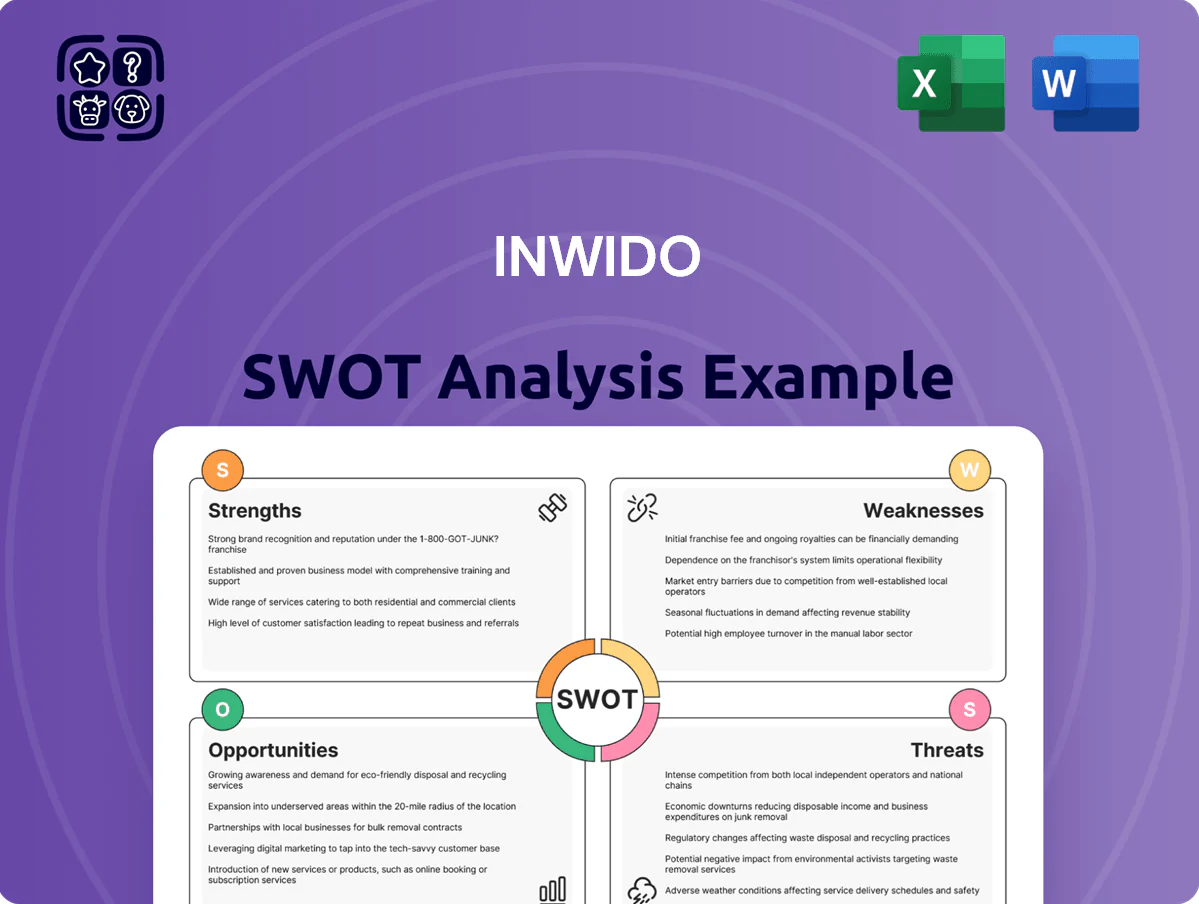

Inwido’s SWOT reveals its strengths in product diversification and strong Nordic market presence, tempered by supply-chain risks and competitive pressure; uncover strategic opportunities in sustainability-driven renovations and digital sales channels. Purchase the full SWOT analysis to access a professionally formatted, research-backed report with editable Word and Excel deliverables—ideal for investors, advisors, and strategic planners seeking actionable insights.

Strengths

Resilient Financial Performance and Profitability

Inwido showed resilient financial performance in 2025, keeping operating EBITA margins near 10.5–12.2% despite a severe European construction downturn. Full-year net sales reached SEK 9,002 million, up 2% from 2024, driven by tight cost control and value-based pricing. A solid balance sheet backs this resilience: net debt to operating EBITDA was 1.7x, well under the 2.5x target. These metrics signal durable profitability and financial flexibility.

Dominant Market Leadership in Northern Europe

As of late 2025, Inwido is Europe’s leading window and door group, holding number one in the Nordics and number two in the UK, with ~35 localized business units and c.€1.6bn revenue in 2024 supporting scale.

The decentralized model uses strong regional brands to keep close customer ties, drive a c.12% EBITDA margin in 2024, and capture purchasing benefits across markets.

Decentralized and Flexible Business Model

The company’s decentralized structure lets regional business units pivot quickly to demand and cost shifts, which in 2025 enabled Inwido to cut idle capacity by 18% and protect gross margin at 29.4% despite volatile order flow. This flexibility supported a 6% year-on-year production efficiency gain and limited inventory days to 42. The model also drives engagement: the 2025 employee satisfaction index hit 77% with a 92% response rate, up from 71% in 2024. These metrics show governance that balances local agility with group profitability.

Strategic Acquisition and Integration Capabilities

- Q4 2025: 3 acquisitions (AJM, Victorian House Window Group, +1)

- 2030 target: SEK 20bn turnover

- Post-acquisition revenue +SEK 200m run-rate (RM Snickerier, Fast Frame)

- EBITDA margin uplift ~150–250 bps from prior deals

Focus on Energy-Efficient and Sustainable Solutions

Inwido’s product mix centers on triple-glazed windows and doors, aligning it with EU decarbonization rules and boosting market access across Northern and Western Europe.

In 2025 Inwido cut energy use per unit and lowered greenhouse gas emissions by 15% vs 2022, improving sustainability KPIs and reducing regulatory risk.

This green focus attracts eco-minded consumers and supports pricing power as demand for high-performance glazing rises.

- 15% GHG cut vs 2022

- Triple-glazed focus: majority of portfolio

- Stronger regulatory alignment across EU

- Higher appeal to eco-conscious buyers

Inwido 2025: Resilient growth—SEK 9.0bn sales, ~11% EBITA, 3 deals, 15% GHG cut

Inwido delivered resilient 2025 results: SEK 9,002m sales (+2% vs 2024), operating EBITA margin ~11.0%, net debt/EBITDA 1.7x, and gross margin 29.4%; decentralised, #1 Nordics/#2 UK with ~35 units and c.€1.6bn 2024 revenue; 3 Q4 2025 acquisitions and prior deals added ~SEK 200m run-rate and +150–250bps EBITDA; 15% GHG cut vs 2022.

| Metric | 2025 |

|---|---|

| Net sales | SEK 9,002m |

| EBITA margin | ~11.0% |

| Net debt/EBITDA | 1.7x |

| Gross margin | 29.4% |

| Acquisitions Q4 | 3 |

| GHG reduction vs 2022 | 15% |

What is included in the product

Provides a concise SWOT overview of Inwido, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decisions.

Provides a clear, visual SWOT snapshot of Inwido to speed strategic alignment and decision-making across teams.

Weaknesses

Exposure to Cyclical Construction and Real Estate Markets

Inwido is highly exposed to cyclical construction and real estate markets; 2025 saw a severe downturn in residential and commercial building that hit new-build demand. The group grew organic sales 4% for full-year 2025 but suffered a 12% drop in organic order intake in Q4 2025, underscoring revenue volatility. Sensitivity to macro cycles, especially new-build, remains a structural weakness for cash flow predictability.

Regional Performance Disparity and Market Concentration

Regional performance is skewed: Scandinavia drove a 6% sales rise in late 2025 while Eastern Europe saw a 7% sales drop and margins slumped to 4.1%, widening group variance.

Relying on a few core markets—notably Finland and Sweden—raises exposure: a localized downturn could cut group sales and EBITDA markedly.

At year-end 2025, Scandinavia accounted for roughly 60% of operating profit, underscoring concentration risk and limited diversification.

Declining Order Backlog and Low Visibility

By end-2025 Inwido’s order backlog fell 9% to SEK 2,272m, signaling weaker consumer demand and delayed project starts; this aligns with lower Nordic housing permits in 2025 (down ~6% y/y).

Management reports low visibility for 2026 demand, making production planning and inventory control harder and raising the risk of stock mismatches.

A shrinking backlog reduces revenue forecasting accuracy and may cause underutilized capacity and higher per-unit costs if recovery stalls.

Vulnerability to Currency Fluctuations and FX Headwinds

Inwido, reporting in Swedish krona, saw 2025 earnings hit by FX volatility: a stronger SEK versus 2024 and swings in GBP and EUR trimmed reported net sales by roughly 3.5–4.2 percentage points and shaved ~150–220 bps off operating margin in FY2025.

These currency moves are beyond management control and can hide real operational gains when consolidated into SEK financials.

- Estimated sales FX drag: 3.5–4.2%

- Estimated margin impact: 150–220 bps

- Key drivers: stronger SEK, GBP/EUR fluctuations

Challenges in the e-Commerce Segment Growth

Despite margin improvements, Inwido's e-Commerce sales fell 1% in Q4 2025 as cautious online consumers cut back on big-ticket purchases, limiting volume recovery.

Structural cost measures raised segment EBIT margin by about 120 basis points in 2025, but inconsistent order volumes prevent full leverage of digital investment.

This weakness caps Inwido's ability to capture digital market share in building materials, where online penetration rose to ~18% in 2025 but high-ticket conversion lagged.

- Q4 2025 e-Commerce sales -1%

- EBIT margin improvement ~+120 bps in 2025

- Online building-materials penetration ~18% (2025)

- High-ticket conversion below category average

Nordic exposure, FX pain and weak orders dent 2025 growth and margins

Concentration in Nordic markets and sensitivity to new-build cycles cut revenue visibility; FY2025 backlog fell 9% to SEK 2,272m and Q4 order intake dropped 12%. FX headwinds (stronger SEK) trimmed reported sales by ~3.5–4.2% and shaved ~150–220 bps off operating margin in 2025. Regional mix: Scandinavia generated ~60% of operating profit in 2025 while Eastern Europe sales fell 7% and margins hit 4.1%. e‑commerce growth lagged (Q4 2025 −1%), limiting digital leverage.

| Metric | 2025 |

|---|---|

| Order backlog | SEK 2,272m (−9% y/y) |

| Q4 order intake | −12% y/y |

| FX sales drag | 3.5–4.2ppt |

| Operating margin hit | −150–220 bps |

| Scandinavia share of OP | ~60% |

| Eastern Europe sales | −7% (margins 4.1%) |

| e‑commerce Q4 | −1% |

Full Version Awaits

Inwido SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Inwido’s SWOT reveals its strengths in product diversification and strong Nordic market presence, tempered by supply-chain risks and competitive pressure; uncover strategic opportunities in sustainability-driven renovations and digital sales channels. Purchase the full SWOT analysis to access a professionally formatted, research-backed report with editable Word and Excel deliverables—ideal for investors, advisors, and strategic planners seeking actionable insights.

Strengths

Resilient Financial Performance and Profitability

Inwido showed resilient financial performance in 2025, keeping operating EBITA margins near 10.5–12.2% despite a severe European construction downturn. Full-year net sales reached SEK 9,002 million, up 2% from 2024, driven by tight cost control and value-based pricing. A solid balance sheet backs this resilience: net debt to operating EBITDA was 1.7x, well under the 2.5x target. These metrics signal durable profitability and financial flexibility.

Dominant Market Leadership in Northern Europe

As of late 2025, Inwido is Europe’s leading window and door group, holding number one in the Nordics and number two in the UK, with ~35 localized business units and c.€1.6bn revenue in 2024 supporting scale.

The decentralized model uses strong regional brands to keep close customer ties, drive a c.12% EBITDA margin in 2024, and capture purchasing benefits across markets.

Decentralized and Flexible Business Model

The company’s decentralized structure lets regional business units pivot quickly to demand and cost shifts, which in 2025 enabled Inwido to cut idle capacity by 18% and protect gross margin at 29.4% despite volatile order flow. This flexibility supported a 6% year-on-year production efficiency gain and limited inventory days to 42. The model also drives engagement: the 2025 employee satisfaction index hit 77% with a 92% response rate, up from 71% in 2024. These metrics show governance that balances local agility with group profitability.

Strategic Acquisition and Integration Capabilities

- Q4 2025: 3 acquisitions (AJM, Victorian House Window Group, +1)

- 2030 target: SEK 20bn turnover

- Post-acquisition revenue +SEK 200m run-rate (RM Snickerier, Fast Frame)

- EBITDA margin uplift ~150–250 bps from prior deals

Focus on Energy-Efficient and Sustainable Solutions

Inwido’s product mix centers on triple-glazed windows and doors, aligning it with EU decarbonization rules and boosting market access across Northern and Western Europe.

In 2025 Inwido cut energy use per unit and lowered greenhouse gas emissions by 15% vs 2022, improving sustainability KPIs and reducing regulatory risk.

This green focus attracts eco-minded consumers and supports pricing power as demand for high-performance glazing rises.

- 15% GHG cut vs 2022

- Triple-glazed focus: majority of portfolio

- Stronger regulatory alignment across EU

- Higher appeal to eco-conscious buyers

Inwido 2025: Resilient growth—SEK 9.0bn sales, ~11% EBITA, 3 deals, 15% GHG cut

Inwido delivered resilient 2025 results: SEK 9,002m sales (+2% vs 2024), operating EBITA margin ~11.0%, net debt/EBITDA 1.7x, and gross margin 29.4%; decentralised, #1 Nordics/#2 UK with ~35 units and c.€1.6bn 2024 revenue; 3 Q4 2025 acquisitions and prior deals added ~SEK 200m run-rate and +150–250bps EBITDA; 15% GHG cut vs 2022.

| Metric | 2025 |

|---|---|

| Net sales | SEK 9,002m |

| EBITA margin | ~11.0% |

| Net debt/EBITDA | 1.7x |

| Gross margin | 29.4% |

| Acquisitions Q4 | 3 |

| GHG reduction vs 2022 | 15% |

What is included in the product

Provides a concise SWOT overview of Inwido, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decisions.

Provides a clear, visual SWOT snapshot of Inwido to speed strategic alignment and decision-making across teams.

Weaknesses

Exposure to Cyclical Construction and Real Estate Markets

Inwido is highly exposed to cyclical construction and real estate markets; 2025 saw a severe downturn in residential and commercial building that hit new-build demand. The group grew organic sales 4% for full-year 2025 but suffered a 12% drop in organic order intake in Q4 2025, underscoring revenue volatility. Sensitivity to macro cycles, especially new-build, remains a structural weakness for cash flow predictability.

Regional Performance Disparity and Market Concentration

Regional performance is skewed: Scandinavia drove a 6% sales rise in late 2025 while Eastern Europe saw a 7% sales drop and margins slumped to 4.1%, widening group variance.

Relying on a few core markets—notably Finland and Sweden—raises exposure: a localized downturn could cut group sales and EBITDA markedly.

At year-end 2025, Scandinavia accounted for roughly 60% of operating profit, underscoring concentration risk and limited diversification.

Declining Order Backlog and Low Visibility

By end-2025 Inwido’s order backlog fell 9% to SEK 2,272m, signaling weaker consumer demand and delayed project starts; this aligns with lower Nordic housing permits in 2025 (down ~6% y/y).

Management reports low visibility for 2026 demand, making production planning and inventory control harder and raising the risk of stock mismatches.

A shrinking backlog reduces revenue forecasting accuracy and may cause underutilized capacity and higher per-unit costs if recovery stalls.

Vulnerability to Currency Fluctuations and FX Headwinds

Inwido, reporting in Swedish krona, saw 2025 earnings hit by FX volatility: a stronger SEK versus 2024 and swings in GBP and EUR trimmed reported net sales by roughly 3.5–4.2 percentage points and shaved ~150–220 bps off operating margin in FY2025.

These currency moves are beyond management control and can hide real operational gains when consolidated into SEK financials.

- Estimated sales FX drag: 3.5–4.2%

- Estimated margin impact: 150–220 bps

- Key drivers: stronger SEK, GBP/EUR fluctuations

Challenges in the e-Commerce Segment Growth

Despite margin improvements, Inwido's e-Commerce sales fell 1% in Q4 2025 as cautious online consumers cut back on big-ticket purchases, limiting volume recovery.

Structural cost measures raised segment EBIT margin by about 120 basis points in 2025, but inconsistent order volumes prevent full leverage of digital investment.

This weakness caps Inwido's ability to capture digital market share in building materials, where online penetration rose to ~18% in 2025 but high-ticket conversion lagged.

- Q4 2025 e-Commerce sales -1%

- EBIT margin improvement ~+120 bps in 2025

- Online building-materials penetration ~18% (2025)

- High-ticket conversion below category average

Nordic exposure, FX pain and weak orders dent 2025 growth and margins

Concentration in Nordic markets and sensitivity to new-build cycles cut revenue visibility; FY2025 backlog fell 9% to SEK 2,272m and Q4 order intake dropped 12%. FX headwinds (stronger SEK) trimmed reported sales by ~3.5–4.2% and shaved ~150–220 bps off operating margin in 2025. Regional mix: Scandinavia generated ~60% of operating profit in 2025 while Eastern Europe sales fell 7% and margins hit 4.1%. e‑commerce growth lagged (Q4 2025 −1%), limiting digital leverage.

| Metric | 2025 |

|---|---|

| Order backlog | SEK 2,272m (−9% y/y) |

| Q4 order intake | −12% y/y |

| FX sales drag | 3.5–4.2ppt |

| Operating margin hit | −150–220 bps |

| Scandinavia share of OP | ~60% |

| Eastern Europe sales | −7% (margins 4.1%) |

| e‑commerce Q4 | −1% |

Full Version Awaits

Inwido SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout.