Indian Oil Porter's Five Forces Analysis

From Overview to Strategy Blueprint

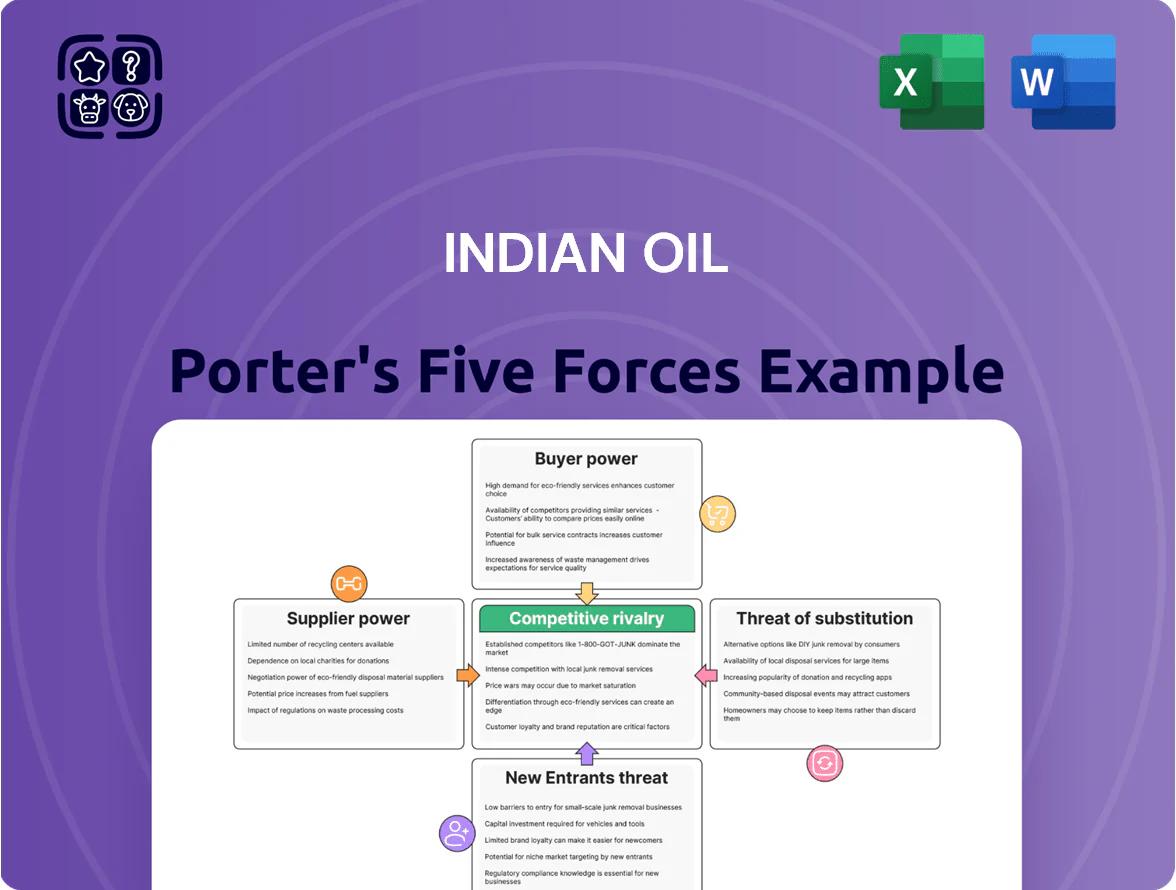

Indian Oil faces moderate buyer power, stable supplier relationships, high barriers for new entrants, intense rivalry among incumbents, and growing substitution risks from renewables and EVs; strategic positioning hinges on scale, refinery complexity, and retail network strengths. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Indian Oil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Crude Oil Imports from OPEC Plus

Indian Oil depends on overseas crude for roughly 80% of its feedstock, so OPEC Plus production cuts and pricing moves sharply affect refinery margins and import bill.

By end-2025, geopolitical strains kept crude volatility high—Brent averaged ~88 USD/bbl in 2025 H1—boosting supplier leverage and input cost risk for Indian Oil.

Indian Oil counters with diversified sourcing across West Africa, Russia, and the Middle East and long-term contracts covering about 40–50% of imports, lowering but not removing supplier power.

Influence of Domestic Upstream Producers

Volatility in Global Energy Markets

Supplier power rises sharply in global energy shortages: spot crude surged 65% in 2022–23 and hit $120/bbl in Oct 2023, forcing refiners to buy at peak prices. Indian Oil (IOCL), as India’s largest refiner, must secure feedstock to meet 35% of national fuel demand, so traders can dictate terms during crises. By late 2025, a multi-currency trade shift (INR, USD, RMB) added FX complexity, raising procurement hedging costs by ~4–6%.

Strategic Partnerships for Technology and Infrastructure

Suppliers of specialized refining tech and green-energy infrastructure hold strong leverage over Indian Oil due to niche expertise and scarce global suppliers; carbon-capture and advanced-biofuel tech are concentrated among a few firms, raising dependency as IOCL targets net-zero by 2046.

High switching costs, integration complexity, and long validation cycles—often $100m+ per complex project—bolster supplier power and limit IOCL’s bargaining flexibility.

- Few global suppliers for CCUS and biofuels

- Net-zero by 2046 increases tech spend

- Per-project capex often exceeds $100m

- High switching costs and long validation times

Transition to Green Feedstock Suppliers

Supplier base is shifting to farmers and small bioenergy firms as India targets 20% ethanol blend by 2025 and expands compressed biogas; this fragments supply and appears low-power initially.

Cooperatives and state-set MSP/floor prices for crops (e.g., sugarcane, maize) can raise input costs—Indian Oil reported 2024 ethanol procurement of ~3.2 bn litres, exposing margins to feedstock pricing.

Indian Oil must build supplier aggregation, forward contracts, and blending hubs to control logistics and price volatility or margin erosion.

- 2025 ethanol target: 20% nationwide

- Indian Oil 2024 ethanol buy: ~3.2 billion litres

- Risk: MSP/floor prices and cooperative bargaining

- Mitigation: aggregation, forward contracts, blending hubs

Imports, OPEC+ Risk and Tech Capex Keep Suppliers Powerful

Suppliers hold moderate-to-high power: ~80% imported crude (Brent ~88 USD/bbl H1 2025) raises vulnerability to OPEC+ moves, while 20–25% domestic supply (ONGC ~67 USD/bbl FY2024) offers limited relief; long-term contracts cover ~40–50% imports. Tech and CCUS vendors exert high leverage—projects often >$100m—while ethanol (IOCL ~3.2 bn L in 2024) shifts some power to farmers and MSPs.

| Metric | Value |

|---|---|

| Imported crude share | ~80% |

| Domestic share | 20–25% |

| Brent H1 2025 | ~88 USD/bbl |

| ONGC FY2024 transfer | ~67 USD/bbl |

| Long-term cover | 40–50% imports |

| IOCL ethanol 2024 | ~3.2 bn litres |

| Typical tech project capex | >$100m |

What is included in the product

Tailored exclusively for Indian Oil, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its pricing and profitability.

Concise Porter's Five Forces for Indian Oil—one-sheet view to rapidly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Retail Price Sensitivity and Government Regulation

Individual motorists have low bargaining power but strong collective clout via price sensitivity and voting pressure; a 2024 IPSOS survey showed 68% of Indians cite fuel prices as a top household concern, pressuring policy.

The Indian government routinely caps or delays retail fuel hikes—e.g., central and state taxes kept pump prices below parity during late‑2022 crude spikes—acting as a consumer proxy.

That intervention prevents Indian Oil from instantly passing Brent rises (Brent averaged $85/b in 2024) to consumers, squeezing short‑term gross margins; Indian Oil reported a GRM (gross refining margin) hit of Rs 12bn in Q3 2024 from delayed pass‑through.

Bulk Industrial Buyer Negotiation Strength

Expansion of Choice in the Lubricant Segment

In India’s lubricants and specialty chemicals market, over 60 brands compete, including domestic names and multinationals like Shell and BP, giving customers wide choice; brand loyalty helps but switching costs are low, so buyers shift on price or performance.

Indian Oil reported lubricants revenue of INR 16.4 billion in FY2024, so it must keep high marketing spend and R&D—industry average ad/R&D intensity ~3–4%—to retain share in this contested segment.

Impact of Digital Payment and Loyalty Programs

The rise of digital ecosystems lets customers compare fuel prices and earn rewards via apps, shifting choice to value-added services, convenience, and loyalty points; 2024 data show ~59% of Indian petrol buyers use mobile wallets or UPI at stations, raising switching risk.

Indian Oil’s retention hinges on app engagement and outlet service quality; Indian Oil One app had 12.4 million downloads by Dec 2024, but conversion to repeat-fill rate must improve to cut churn.

- 59% mobile payment adoption (2024)

- Indian Oil One: 12.4M downloads (Dec 2024)

- Customers pick digital rewards+convenience over location

- Retention tied to app engagement and outlet service

Rise of Alternative Fuel Options for Consumers

The rise of EV charging (over 1.3 million public chargers in India by Dec 2025 forecast) and a 9% CAGR in CNG vehicle registrations since 2020 gives customers clear exit options from petrol/diesel.

As infrastructure matures through 2025, Indian Oil faces higher risk of outright customer loss, pushing it to expand into EV charging, CNG, and renewable fuels to remain a total energy provider.

- 1.3M public EV chargers by Dec 2025 (forecast)

- 9% CAGR CNG vehicle registrations since 2020

- Indian Oil must scale charging, CNG, renewables

Price‑sensitive motorists vs. powerful industrial buyers: digital shift raises switch risk

Customers have mixed bargaining power: individual motorists show low direct leverage but high price sensitivity (68% cite fuel prices as top concern, IPSOS 2024), while large industrial buyers (top 10 ≈15% sales) and lubricant buyers (60+ brands; IOCL lubes revenue INR 16.4bn FY2024) extract discounts; digital adoption (59% mobile payments, IO One 12.4M downloads Dec 2024) and EV/CNG growth raise switch risk.

| Metric | Value |

|---|---|

| Fuel concern (IPSOS 2024) | 68% |

| Mobile payments (2024) | 59% |

| IOCL lubes rev FY2024 | INR 16.4bn |

| IO One downloads Dec 2024 | 12.4M |

| Top-10 buyers share | ≈15% |

What You See Is What You Get

Indian Oil Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Indian Oil you’ll receive immediately after purchase—no surprises, no placeholders. It includes the full competitive assessment of supplier power, buyer power, threat of new entrants, threat of substitutes, and industry rivalry, fully formatted and ready to use. Once you buy, you’ll get instant access to this identical document for download and application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Indian Oil faces moderate buyer power, stable supplier relationships, high barriers for new entrants, intense rivalry among incumbents, and growing substitution risks from renewables and EVs; strategic positioning hinges on scale, refinery complexity, and retail network strengths. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Indian Oil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Crude Oil Imports from OPEC Plus

Indian Oil depends on overseas crude for roughly 80% of its feedstock, so OPEC Plus production cuts and pricing moves sharply affect refinery margins and import bill.

By end-2025, geopolitical strains kept crude volatility high—Brent averaged ~88 USD/bbl in 2025 H1—boosting supplier leverage and input cost risk for Indian Oil.

Indian Oil counters with diversified sourcing across West Africa, Russia, and the Middle East and long-term contracts covering about 40–50% of imports, lowering but not removing supplier power.

Influence of Domestic Upstream Producers

Volatility in Global Energy Markets

Supplier power rises sharply in global energy shortages: spot crude surged 65% in 2022–23 and hit $120/bbl in Oct 2023, forcing refiners to buy at peak prices. Indian Oil (IOCL), as India’s largest refiner, must secure feedstock to meet 35% of national fuel demand, so traders can dictate terms during crises. By late 2025, a multi-currency trade shift (INR, USD, RMB) added FX complexity, raising procurement hedging costs by ~4–6%.

Strategic Partnerships for Technology and Infrastructure

Suppliers of specialized refining tech and green-energy infrastructure hold strong leverage over Indian Oil due to niche expertise and scarce global suppliers; carbon-capture and advanced-biofuel tech are concentrated among a few firms, raising dependency as IOCL targets net-zero by 2046.

High switching costs, integration complexity, and long validation cycles—often $100m+ per complex project—bolster supplier power and limit IOCL’s bargaining flexibility.

- Few global suppliers for CCUS and biofuels

- Net-zero by 2046 increases tech spend

- Per-project capex often exceeds $100m

- High switching costs and long validation times

Transition to Green Feedstock Suppliers

Supplier base is shifting to farmers and small bioenergy firms as India targets 20% ethanol blend by 2025 and expands compressed biogas; this fragments supply and appears low-power initially.

Cooperatives and state-set MSP/floor prices for crops (e.g., sugarcane, maize) can raise input costs—Indian Oil reported 2024 ethanol procurement of ~3.2 bn litres, exposing margins to feedstock pricing.

Indian Oil must build supplier aggregation, forward contracts, and blending hubs to control logistics and price volatility or margin erosion.

- 2025 ethanol target: 20% nationwide

- Indian Oil 2024 ethanol buy: ~3.2 billion litres

- Risk: MSP/floor prices and cooperative bargaining

- Mitigation: aggregation, forward contracts, blending hubs

Imports, OPEC+ Risk and Tech Capex Keep Suppliers Powerful

Suppliers hold moderate-to-high power: ~80% imported crude (Brent ~88 USD/bbl H1 2025) raises vulnerability to OPEC+ moves, while 20–25% domestic supply (ONGC ~67 USD/bbl FY2024) offers limited relief; long-term contracts cover ~40–50% imports. Tech and CCUS vendors exert high leverage—projects often >$100m—while ethanol (IOCL ~3.2 bn L in 2024) shifts some power to farmers and MSPs.

| Metric | Value |

|---|---|

| Imported crude share | ~80% |

| Domestic share | 20–25% |

| Brent H1 2025 | ~88 USD/bbl |

| ONGC FY2024 transfer | ~67 USD/bbl |

| Long-term cover | 40–50% imports |

| IOCL ethanol 2024 | ~3.2 bn litres |

| Typical tech project capex | >$100m |

What is included in the product

Tailored exclusively for Indian Oil, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its pricing and profitability.

Concise Porter's Five Forces for Indian Oil—one-sheet view to rapidly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Retail Price Sensitivity and Government Regulation

Individual motorists have low bargaining power but strong collective clout via price sensitivity and voting pressure; a 2024 IPSOS survey showed 68% of Indians cite fuel prices as a top household concern, pressuring policy.

The Indian government routinely caps or delays retail fuel hikes—e.g., central and state taxes kept pump prices below parity during late‑2022 crude spikes—acting as a consumer proxy.

That intervention prevents Indian Oil from instantly passing Brent rises (Brent averaged $85/b in 2024) to consumers, squeezing short‑term gross margins; Indian Oil reported a GRM (gross refining margin) hit of Rs 12bn in Q3 2024 from delayed pass‑through.

Bulk Industrial Buyer Negotiation Strength

Expansion of Choice in the Lubricant Segment

In India’s lubricants and specialty chemicals market, over 60 brands compete, including domestic names and multinationals like Shell and BP, giving customers wide choice; brand loyalty helps but switching costs are low, so buyers shift on price or performance.

Indian Oil reported lubricants revenue of INR 16.4 billion in FY2024, so it must keep high marketing spend and R&D—industry average ad/R&D intensity ~3–4%—to retain share in this contested segment.

Impact of Digital Payment and Loyalty Programs

The rise of digital ecosystems lets customers compare fuel prices and earn rewards via apps, shifting choice to value-added services, convenience, and loyalty points; 2024 data show ~59% of Indian petrol buyers use mobile wallets or UPI at stations, raising switching risk.

Indian Oil’s retention hinges on app engagement and outlet service quality; Indian Oil One app had 12.4 million downloads by Dec 2024, but conversion to repeat-fill rate must improve to cut churn.

- 59% mobile payment adoption (2024)

- Indian Oil One: 12.4M downloads (Dec 2024)

- Customers pick digital rewards+convenience over location

- Retention tied to app engagement and outlet service

Rise of Alternative Fuel Options for Consumers

The rise of EV charging (over 1.3 million public chargers in India by Dec 2025 forecast) and a 9% CAGR in CNG vehicle registrations since 2020 gives customers clear exit options from petrol/diesel.

As infrastructure matures through 2025, Indian Oil faces higher risk of outright customer loss, pushing it to expand into EV charging, CNG, and renewable fuels to remain a total energy provider.

- 1.3M public EV chargers by Dec 2025 (forecast)

- 9% CAGR CNG vehicle registrations since 2020

- Indian Oil must scale charging, CNG, renewables

Price‑sensitive motorists vs. powerful industrial buyers: digital shift raises switch risk

Customers have mixed bargaining power: individual motorists show low direct leverage but high price sensitivity (68% cite fuel prices as top concern, IPSOS 2024), while large industrial buyers (top 10 ≈15% sales) and lubricant buyers (60+ brands; IOCL lubes revenue INR 16.4bn FY2024) extract discounts; digital adoption (59% mobile payments, IO One 12.4M downloads Dec 2024) and EV/CNG growth raise switch risk.

| Metric | Value |

|---|---|

| Fuel concern (IPSOS 2024) | 68% |

| Mobile payments (2024) | 59% |

| IOCL lubes rev FY2024 | INR 16.4bn |

| IO One downloads Dec 2024 | 12.4M |

| Top-10 buyers share | ≈15% |

What You See Is What You Get

Indian Oil Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Indian Oil you’ll receive immediately after purchase—no surprises, no placeholders. It includes the full competitive assessment of supplier power, buyer power, threat of new entrants, threat of substitutes, and industry rivalry, fully formatted and ready to use. Once you buy, you’ll get instant access to this identical document for download and application.