iomart Group SWOT Analysis

Your Strategic Toolkit Starts Here

iomart Group stands out with robust UK cloud infrastructure, strong recurring revenue, and strategic M&A momentum, yet faces intense competition, margin pressure, and execution risks in scaling hybrid services; regulation and rising demand for secure managed hosting present clear growth levers. Purchase the full SWOT analysis to access a professionally formatted Word report and editable Excel model that transform these insights into actionable strategy and investment decisions.

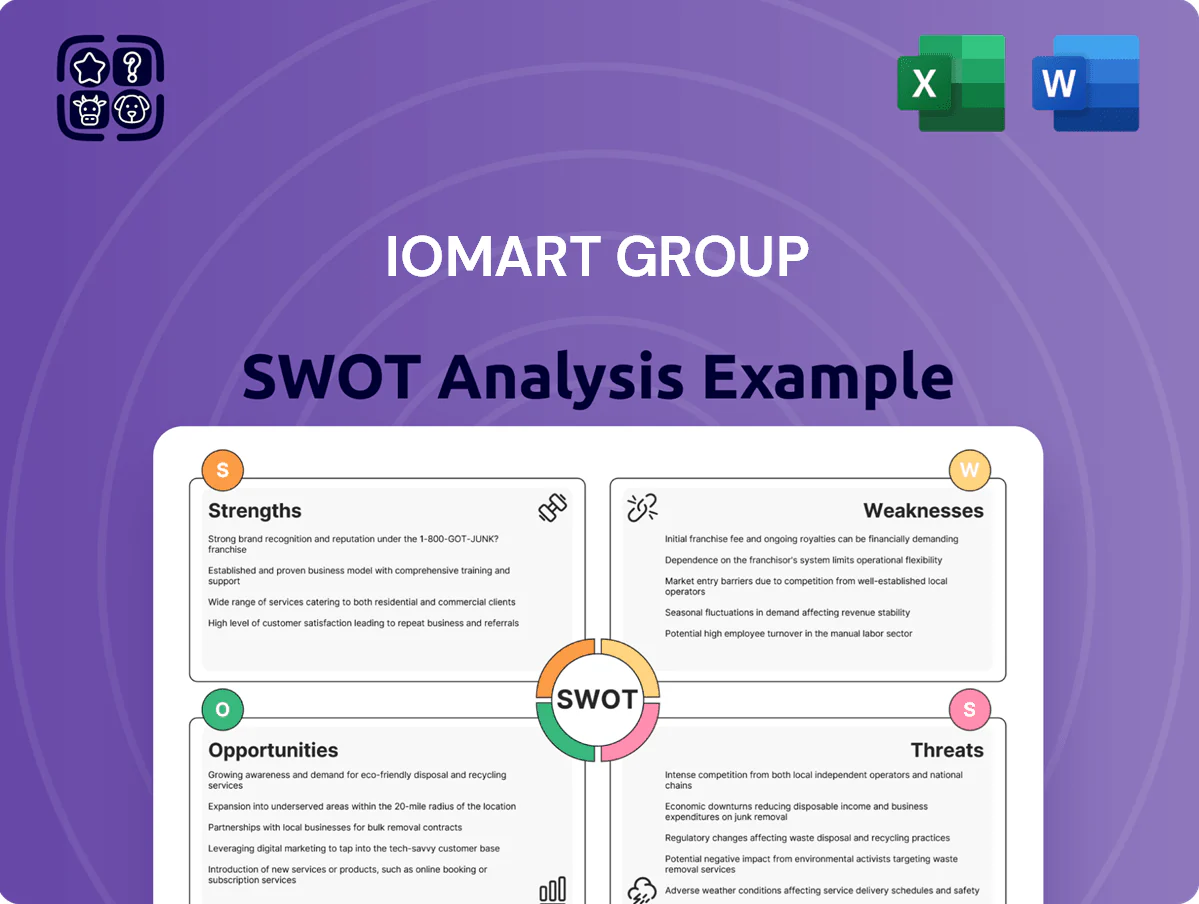

Strengths

Extensive UK Data Center Footprint

iomart Group owns and operates a broad UK data‑centre estate—17 sites as of FY2024—giving low latency and clear data sovereignty for UK clients, key for public sector and finance customers.

Controlling physical infrastructure lets iomart enforce stricter security and deliver industry‑leading uptime; its 2024 average availability exceeded 99.99% across the estate.

Ownership also improves long‑term costs: capitalized sites reduce recurring lease expense, helping gross margin resilience—iomart reported 2024 adjusted EBITDA margin of ~26%.

High Proportion of Recurring Revenue

A core strength is that iomart Group plc reported 86% recurring revenue in FY2024 (year to March 31, 2024), giving strong visibility and financial stability.

Most clients are on multi-year cloud and managed-service contracts, sustaining steady cash flow through economic cycles and lowering churn risk.

This predictability lets management plan capex and strategic investments; FY2024 net cash of £22m aided funding for growth initiatives.

Comprehensive Hybrid Cloud Portfolio

iomart Group offers a versatile portfolio across public, private, and hybrid cloud, serving 1,800+ customers and supporting over 40 data centres as of FY2024, which lets them meet diverse client needs. By acting as a single point of contact for colocation, connectivity, and managed security, they simplify the IT supply chain for mid-market enterprises. This end-to-end capability helped drive 2024 revenue of £183.6m and 12% adjusted EBITDA margin, making them a preferred partner for complex digital transformations.

Robust Customer Retention and Loyalty

iomart Group shows strong customer retention driven by a high-touch service model and technical support, with reported revenue retention above 90% in FY2024 and average client tenure of 5+ years, lowering acquisition costs and stabilising ARR.

Long-standing clients have migrated through multiple tech cycles under iomart’s guidance, enabling effective cross-sell: cybersecurity and managed services grew 18% YoY in 2024, boosting gross margin.

- Revenue retention >90% (FY2024)

- Average client tenure 5+ years

- Cybersecurity/managed services +18% YoY (2024)

- Improved gross margin via cross-sell

Strong Financial Position and Cash Generation

iomart Group maintained strong cash generation in FY2024, reporting adjusted operating cash flow of £64.1m and net debt of £176.3m as of 31 Dec 2024, supporting a 2024 interim dividend and targeted M&A.

This liquidity funds capex for data-center upgrades—capital expenditure was £45.8m in 2024—keeping infrastructure competitive in a capital-intensive market.

- Operating cash flow: £64.1m (FY2024)

- Net debt: £176.3m (31 Dec 2024)

- Capex: £45.8m (FY2024)

- Continued dividends and M&A funded

iomart: 17 UK data centres, £183.6m revenue, 86% recurring & £64.1m cash flow

iomart’s strengths: 17 UK data centres (FY2024), 86% recurring revenue, £183.6m revenue and £64.1m operating cash flow (FY2024), 99.99%+ estate availability, >90% revenue retention, 1,800+ customers, capex £45.8m (2024), net cash £22m (Mar 31, 2024) and net debt £176.3m (Dec 31, 2024).

| Metric | Value |

|---|---|

| Data centres | 17 (FY2024) |

| Revenue | £183.6m (FY2024) |

| Recurring rev | 86% (FY2024) |

| Op cash flow | £64.1m (FY2024) |

What is included in the product

Provides a concise SWOT overview of iomart Group, highlighting its cloud and managed hosting strengths, operational weaknesses, market growth opportunities, and external threats from competition, cybersecurity risks, and regulatory changes.

Provides a concise iomart Group SWOT matrix for quick strategic alignment and stakeholder-ready summaries, ideal for executives needing a clear snapshot of competitive position and risks.

Weaknesses

Geographical Concentration in the UK

The majority of iomart Group plc’s 2024 revenue—about 82% of £162.4m reported for the year to 31 March 2024—derives from the UK, concentrating physical data centres and staff domestically and raising exposure to UK GDP swings and sector-specific regulation.

Despite small international contracts, a UK downturn or local regulatory changes (data residency, energy) could hit margins and utilization rates more than competitors with broader footprints.

Structural limits—high capex for new data centres and complex local compliance—make diversifying revenue internationally slow and costly, keeping overseas sales below 20% of group turnover.

Exposure to Volatile Energy Costs

As a data center operator, iomart Group is highly sensitive to electricity price swings; UK wholesale power rose ~75% in 2021–22 and averaged £140/MWh in winter 2022, showing how costs can spike and hit margins.

The firm uses hedging and long-term supply contracts to soften volatility, but sustained high prices in 2022–23 still compressed EBITDA margins across the sector by 3–6 percentage points.

Raising customer prices risks churn: industry surveys show 28% of enterprise clients cite cost as a top switching reason, limiting iomart’s ability to fully pass through increased energy costs.

Reliance on M&A for Growth

A significant share of iomart Group plc’s growth has come from acquisitions—iomart completed 17 deals between 2018–2024, boosting revenue but making organic CAGR weaker at ~6% vs. reported revenue growth of ~12% in some years.

This reliance raises integration risks: mismatched cultures, legacy systems, and diverse tech stacks have driven post-deal costs and delayed synergies in past transactions.

If suitable targets slow or integrations fail, iomart’s group growth could stall and margins may compress; 2024 adjusted EBITDA margin was 18.2%, so a small revenue setback notably impacts earnings.

Lower Brand Awareness than Hyperscalers

iomart has notably lower brand recognition than hyperscalers like Amazon Web Services (AWS) and Microsoft Azure, which together held about 62% of global cloud market share in 2024 (Synergy Research Group).

This weaker awareness makes winning large enterprise deals harder: many C-suite buyers prefer household names for perceived brand safety and global reach, pushing iomart to offer discounts or extra SLAs.

iomart therefore spends proportionally more on targeted marketing and sales to compete—its FY2024 UK-focused revenue of £97.8m highlights regional strength but limited global scale versus hyperscalers.

- 62%: AWS+Azure global cloud share (2024)

- £97.8m: iomart FY2024 revenue

- Higher per-account marketing spend vs global peers

Infrastructure Maintenance Requirements

Owning a large network of physical data centres forces iomart Group to commit heavy, ongoing capital reinvestment to avoid technology obsolescence; UK data‑centre capex for listed operators averaged ~15–25% of revenue in 2023, and iomart reported £29.1m capex in FY2024 (year to Mar 31, 2024).

Hardware refresh cycles are shortening and cooling advances demand new investment, so iomart must spend to keep PUE (power usage effectiveness) competitive—industry leaders target PUE ≤1.2.

If capital allocation lags, service quality, latency and energy efficiency will worsen, raising churn risk and operating costs.

- £29.1m capex FY2024

- UK operator capex ~15–25% revenue (2023)

- Target PUE ≤1.2 to stay competitive

- Underinvestment raises churn, costs

iomart: UK‑centric cloud under reinvestment and M&A strain vs AWS/Azure dominance

iomart is UK‑concentrated (82% of £162.4m revenue, FY to 31 Mar 2024), exposing it to local GDP, regulation, and energy shocks; capex (£29.1m FY2024) and short hardware cycles raise reinvestment strain; heavy M&A (17 deals 2018–24) creates integration risk and lower organic CAGR (~6%); weaker brand vs AWS/Azure (62% share 2024) forces higher sales/discounting.

| Metric | Value |

|---|---|

| Group revenue (FY2024) | £162.4m |

| UK share | 82% |

| Capex (FY2024) | £29.1m |

| Deals 2018–24 | 17 |

| Organic CAGR | ~6% |

| AWS+Azure share (2024) | 62% |

Same Document Delivered

iomart Group SWOT Analysis

This is a real excerpt from the complete iomart Group SWOT analysis document—you’re viewing the exact file you’ll receive after purchase, professional and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

iomart Group stands out with robust UK cloud infrastructure, strong recurring revenue, and strategic M&A momentum, yet faces intense competition, margin pressure, and execution risks in scaling hybrid services; regulation and rising demand for secure managed hosting present clear growth levers. Purchase the full SWOT analysis to access a professionally formatted Word report and editable Excel model that transform these insights into actionable strategy and investment decisions.

Strengths

Extensive UK Data Center Footprint

iomart Group owns and operates a broad UK data‑centre estate—17 sites as of FY2024—giving low latency and clear data sovereignty for UK clients, key for public sector and finance customers.

Controlling physical infrastructure lets iomart enforce stricter security and deliver industry‑leading uptime; its 2024 average availability exceeded 99.99% across the estate.

Ownership also improves long‑term costs: capitalized sites reduce recurring lease expense, helping gross margin resilience—iomart reported 2024 adjusted EBITDA margin of ~26%.

High Proportion of Recurring Revenue

A core strength is that iomart Group plc reported 86% recurring revenue in FY2024 (year to March 31, 2024), giving strong visibility and financial stability.

Most clients are on multi-year cloud and managed-service contracts, sustaining steady cash flow through economic cycles and lowering churn risk.

This predictability lets management plan capex and strategic investments; FY2024 net cash of £22m aided funding for growth initiatives.

Comprehensive Hybrid Cloud Portfolio

iomart Group offers a versatile portfolio across public, private, and hybrid cloud, serving 1,800+ customers and supporting over 40 data centres as of FY2024, which lets them meet diverse client needs. By acting as a single point of contact for colocation, connectivity, and managed security, they simplify the IT supply chain for mid-market enterprises. This end-to-end capability helped drive 2024 revenue of £183.6m and 12% adjusted EBITDA margin, making them a preferred partner for complex digital transformations.

Robust Customer Retention and Loyalty

iomart Group shows strong customer retention driven by a high-touch service model and technical support, with reported revenue retention above 90% in FY2024 and average client tenure of 5+ years, lowering acquisition costs and stabilising ARR.

Long-standing clients have migrated through multiple tech cycles under iomart’s guidance, enabling effective cross-sell: cybersecurity and managed services grew 18% YoY in 2024, boosting gross margin.

- Revenue retention >90% (FY2024)

- Average client tenure 5+ years

- Cybersecurity/managed services +18% YoY (2024)

- Improved gross margin via cross-sell

Strong Financial Position and Cash Generation

iomart Group maintained strong cash generation in FY2024, reporting adjusted operating cash flow of £64.1m and net debt of £176.3m as of 31 Dec 2024, supporting a 2024 interim dividend and targeted M&A.

This liquidity funds capex for data-center upgrades—capital expenditure was £45.8m in 2024—keeping infrastructure competitive in a capital-intensive market.

- Operating cash flow: £64.1m (FY2024)

- Net debt: £176.3m (31 Dec 2024)

- Capex: £45.8m (FY2024)

- Continued dividends and M&A funded

iomart: 17 UK data centres, £183.6m revenue, 86% recurring & £64.1m cash flow

iomart’s strengths: 17 UK data centres (FY2024), 86% recurring revenue, £183.6m revenue and £64.1m operating cash flow (FY2024), 99.99%+ estate availability, >90% revenue retention, 1,800+ customers, capex £45.8m (2024), net cash £22m (Mar 31, 2024) and net debt £176.3m (Dec 31, 2024).

| Metric | Value |

|---|---|

| Data centres | 17 (FY2024) |

| Revenue | £183.6m (FY2024) |

| Recurring rev | 86% (FY2024) |

| Op cash flow | £64.1m (FY2024) |

What is included in the product

Provides a concise SWOT overview of iomart Group, highlighting its cloud and managed hosting strengths, operational weaknesses, market growth opportunities, and external threats from competition, cybersecurity risks, and regulatory changes.

Provides a concise iomart Group SWOT matrix for quick strategic alignment and stakeholder-ready summaries, ideal for executives needing a clear snapshot of competitive position and risks.

Weaknesses

Geographical Concentration in the UK

The majority of iomart Group plc’s 2024 revenue—about 82% of £162.4m reported for the year to 31 March 2024—derives from the UK, concentrating physical data centres and staff domestically and raising exposure to UK GDP swings and sector-specific regulation.

Despite small international contracts, a UK downturn or local regulatory changes (data residency, energy) could hit margins and utilization rates more than competitors with broader footprints.

Structural limits—high capex for new data centres and complex local compliance—make diversifying revenue internationally slow and costly, keeping overseas sales below 20% of group turnover.

Exposure to Volatile Energy Costs

As a data center operator, iomart Group is highly sensitive to electricity price swings; UK wholesale power rose ~75% in 2021–22 and averaged £140/MWh in winter 2022, showing how costs can spike and hit margins.

The firm uses hedging and long-term supply contracts to soften volatility, but sustained high prices in 2022–23 still compressed EBITDA margins across the sector by 3–6 percentage points.

Raising customer prices risks churn: industry surveys show 28% of enterprise clients cite cost as a top switching reason, limiting iomart’s ability to fully pass through increased energy costs.

Reliance on M&A for Growth

A significant share of iomart Group plc’s growth has come from acquisitions—iomart completed 17 deals between 2018–2024, boosting revenue but making organic CAGR weaker at ~6% vs. reported revenue growth of ~12% in some years.

This reliance raises integration risks: mismatched cultures, legacy systems, and diverse tech stacks have driven post-deal costs and delayed synergies in past transactions.

If suitable targets slow or integrations fail, iomart’s group growth could stall and margins may compress; 2024 adjusted EBITDA margin was 18.2%, so a small revenue setback notably impacts earnings.

Lower Brand Awareness than Hyperscalers

iomart has notably lower brand recognition than hyperscalers like Amazon Web Services (AWS) and Microsoft Azure, which together held about 62% of global cloud market share in 2024 (Synergy Research Group).

This weaker awareness makes winning large enterprise deals harder: many C-suite buyers prefer household names for perceived brand safety and global reach, pushing iomart to offer discounts or extra SLAs.

iomart therefore spends proportionally more on targeted marketing and sales to compete—its FY2024 UK-focused revenue of £97.8m highlights regional strength but limited global scale versus hyperscalers.

- 62%: AWS+Azure global cloud share (2024)

- £97.8m: iomart FY2024 revenue

- Higher per-account marketing spend vs global peers

Infrastructure Maintenance Requirements

Owning a large network of physical data centres forces iomart Group to commit heavy, ongoing capital reinvestment to avoid technology obsolescence; UK data‑centre capex for listed operators averaged ~15–25% of revenue in 2023, and iomart reported £29.1m capex in FY2024 (year to Mar 31, 2024).

Hardware refresh cycles are shortening and cooling advances demand new investment, so iomart must spend to keep PUE (power usage effectiveness) competitive—industry leaders target PUE ≤1.2.

If capital allocation lags, service quality, latency and energy efficiency will worsen, raising churn risk and operating costs.

- £29.1m capex FY2024

- UK operator capex ~15–25% revenue (2023)

- Target PUE ≤1.2 to stay competitive

- Underinvestment raises churn, costs

iomart: UK‑centric cloud under reinvestment and M&A strain vs AWS/Azure dominance

iomart is UK‑concentrated (82% of £162.4m revenue, FY to 31 Mar 2024), exposing it to local GDP, regulation, and energy shocks; capex (£29.1m FY2024) and short hardware cycles raise reinvestment strain; heavy M&A (17 deals 2018–24) creates integration risk and lower organic CAGR (~6%); weaker brand vs AWS/Azure (62% share 2024) forces higher sales/discounting.

| Metric | Value |

|---|---|

| Group revenue (FY2024) | £162.4m |

| UK share | 82% |

| Capex (FY2024) | £29.1m |

| Deals 2018–24 | 17 |

| Organic CAGR | ~6% |

| AWS+Azure share (2024) | 62% |

Same Document Delivered

iomart Group SWOT Analysis

This is a real excerpt from the complete iomart Group SWOT analysis document—you’re viewing the exact file you’ll receive after purchase, professional and ready to use.