Ionis Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Ionis faces nuanced competitive pressures—from specialized supplier leverage in biotech inputs to evolving threats from novel RNA-based therapies—impacting pricing power and R&D pacing; this snapshot highlights critical dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized Raw Material Providers

Ionis depends on specialized chemicals and phosphoramidites for oligonucleotide synthesis, but long-term contracts and multi-source agreements lower single-supplier risk; suppliers historically held moderate leverage given technical specs. As of late 2025, industry maturation raised qualified vendors to ~25 from ~15 in 2020, cutting supplier concentration and trimming estimated supply-cost volatility by ~8%.

Contract Manufacturing Organizations (CMOs)

Ionis relies on CMOs for large-scale antisense RNA production; in 2024 roughly 40–50% of its commercial manufacturing volume was outsourced, reflecting operational scale needs.

High technical requirements for RNA synthesis limit qualified CMOs to fewer than 15 global facilities with GMP RNA capability, creating moderate supplier power and concentration risk.

Ionis retains significant internal process knowledge and spent $120M on manufacturing R&D in 2024 to balance dependency and support tech transfer readiness.

Collaborative Research Partners

Academic labs and small biotechs supply Ionis with core IP and early-stage RNA-target discoveries, and in 2024 about 35% of Ionis’s pipeline originated from external collaborators, giving suppliers leverage via unique patents and data exclusivity.

Specialized Equipment Manufacturers

Specialized equipment makers command leverage for antisense work because PCR-grade synthesizers and GMP oligonucleotide scale-up rigs cost $1–5m and integrate deeply into workflows, making switching expensive and slow.

Still, many high-throughput screening (HTS) instruments are standardized; global HTS market was $3.2bn in 2024, diluting supplier power and enabling competitive sourcing.

- High switching cost: $1–5m per unit

- Integration risk: months of validation

- Mitigant: $3.2bn HTS market (2024)

- Net: moderate supplier power

Regulatory and Quality Compliance Services

Providers of clinical trial management and regulatory consulting are critical for navigating FDA and EMA rules; delays or quality lapses can add months and millions—median FDA review adds ~10 months, and Phase III delays cost $20–100M.

These suppliers have leverage since their performance affects approval speed and launch timing, but Ionis uses scale and a 2025 track record of 12 partnered trials to secure better pricing and timelines.

- Essential: regulatory expertise reduces approval risk

- High impact: approval delays cost $20–100M per Phase III

- Leverage: Ionis 12 partnered trials in 2025 improves negotiation

- Mitigation: reputation and scale lower supplier power

Growing CMO pool eases supplier power—outsourcing, $120M R&D & 35% external pipeline

Suppliers exert moderate power: qualified CMO/GMP RNA sites <15, specialized gear $1–5M/unit, but vendor pool grew (qualified vendors ~25 in 2025 vs ~15 in 2020) cutting supply-cost volatility ~8%; Ionis outsourced 40–50% manufacturing (2024), spent $120M on manufacturing R&D (2024), and sourced ~35% pipeline from external collaborators (2024), creating patent leverage.

| Metric | Value (Year) |

|---|---|

| Qualified CMOs (GMP RNA) | <15 (2025) |

| Qualified vendors | ~25 (2025) |

| Outsourced volume | 40–50% (2024) |

| Manufacturing R&D spend | $120M (2024) |

| Pipeline from external partners | ~35% (2024) |

| HTS market | $3.2B (2024) |

What is included in the product

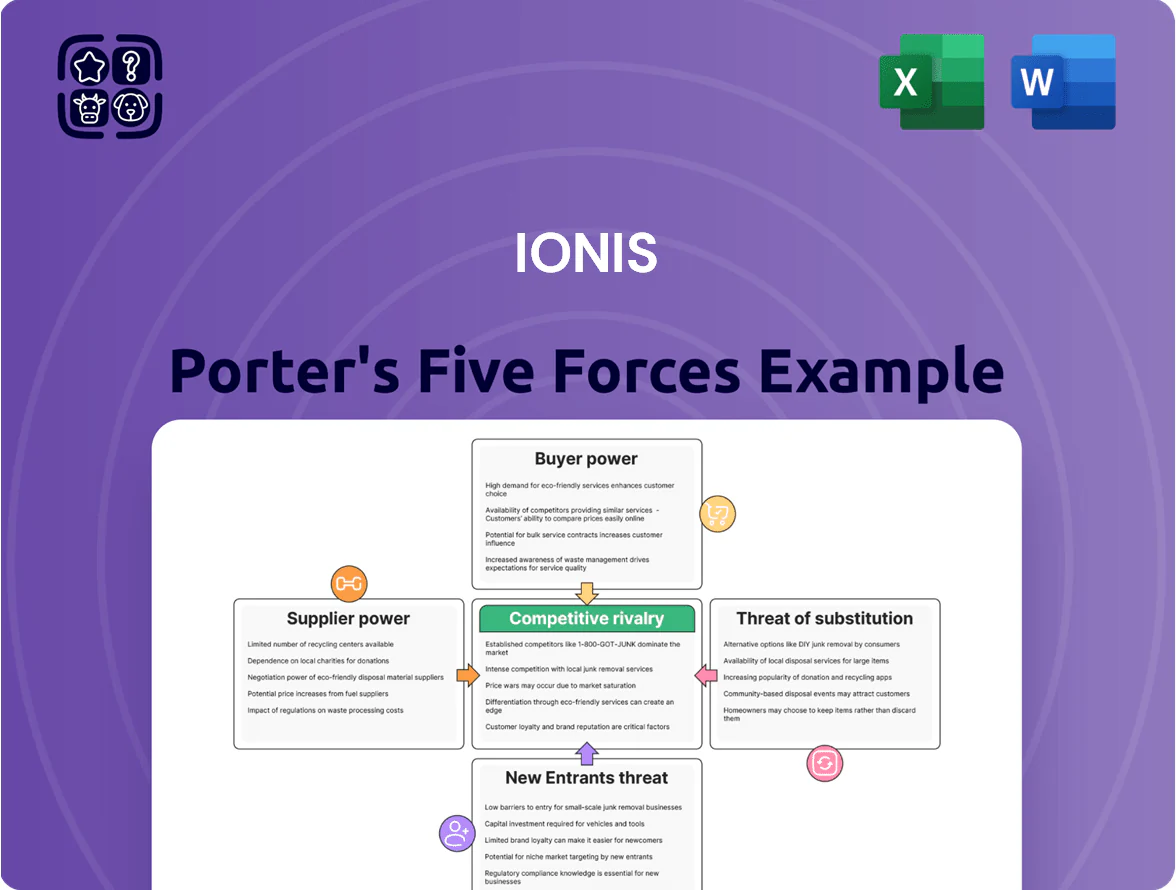

Concise Porter's Five Forces analysis tailored to Ionis, revealing competitive intensity, buyer and supplier power, entry barriers, and substitute threats with strategic implications for pricing, profitability, and growth.

Clear, one-sheet Porter's Five Forces for Ionis—instantly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Government and Private Payers

Insurance companies and national health systems are Ionis Therapeutics’s main buyers for its high-cost specialty drugs, and they push hard on price via value-based contracts and formulary exclusions; by 2024 payers negotiated rebates averaging 28–35% for novel RNA-targeted therapies.

Large Pharmaceutical Partners

Ionis routinely partners with pharma giants—Biogen, AstraZeneca, Roche—that control global distribution and marketing; these partners accounted for licensing and collaboration revenue of roughly $1.2 billion for Ionis in 2024, amplifying their leverage. Because they can prioritize Ionis assets across broad portfolios, they can demand tougher milestones, larger profit splits, and longer exclusivity terms, pressuring Ionis’s margin and negotiating position.

Specialty Pharmacies and Distributors

The small pool of specialty pharmacies and distributors—top 10 providers handle roughly 60–70% of RNA-drug cold-chain distribution in the US—gives them strong bargaining power over Ionis; they can demand higher service fees (premium of 5–12% typical) and extended payment terms (30–90 days), squeezing maker margins and complicating launch cash flows.

Patient Advocacy Groups

Patient advocacy groups shape adoption and reimbursement in rare disease; for example, Duchenne and SMA foundations helped secure access that drove nusinersen to >$1.5bn annual sales by 2020 and influenced payer coverage.

They are not direct buyers but their endorsements create market pull and regulatory pressure; Ionis must sustain partnerships to boost trial recruitment (rare-disease trials often need <200 patients) and payer dialogues.

- Advocacy drives payer decisions and access

- Endorsements boost uptake and pricing leverage

- Partnerships aid recruitment—trials often <200 pts

- Ionis needs ongoing engagement to secure commercial success

Health Technology Assessment (HTA) Bodies

- ICER: 2024 reports set value-based price ranges that shifted expected U.S. launch revenues by up to 30% for comparable rare-disease drugs.

- NICE: not-recommended decisions reduce UK patient access by >60% in first 2 years, per 2023 NHS data.

- Practical power: indirect but decisive—coverage hinges on HTA positive appraisal.

Payers, partners & distributors: squeezing RNA-drug margins with rebates, fees, and deals

Buyers—insurers, national health systems, and pharma partners—wield strong price and contract leverage: payers secured 28–35% rebates on novel RNA drugs by 2024, partners drove ~$1.2bn licensing revenue for Ionis in 2024 and can demand tougher milestones, and top 10 specialty distributors handle 60–70% of cold-chain volume charging 5–12% service premiums.

| Buyer | 2024/2023 Metric |

|---|---|

| Payer rebates | 28–35% |

| Partner revenue | $1.2bn (2024) |

| Top distributors’ share | 60–70% |

| Distribution premium | 5–12% |

What You See Is What You Get

Ionis Porter's Five Forces Analysis

This preview shows the exact Ionis Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

It contains the complete, professionally written assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry; once you buy, the same document is yours to download instantly.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Ionis faces nuanced competitive pressures—from specialized supplier leverage in biotech inputs to evolving threats from novel RNA-based therapies—impacting pricing power and R&D pacing; this snapshot highlights critical dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized Raw Material Providers

Ionis depends on specialized chemicals and phosphoramidites for oligonucleotide synthesis, but long-term contracts and multi-source agreements lower single-supplier risk; suppliers historically held moderate leverage given technical specs. As of late 2025, industry maturation raised qualified vendors to ~25 from ~15 in 2020, cutting supplier concentration and trimming estimated supply-cost volatility by ~8%.

Contract Manufacturing Organizations (CMOs)

Ionis relies on CMOs for large-scale antisense RNA production; in 2024 roughly 40–50% of its commercial manufacturing volume was outsourced, reflecting operational scale needs.

High technical requirements for RNA synthesis limit qualified CMOs to fewer than 15 global facilities with GMP RNA capability, creating moderate supplier power and concentration risk.

Ionis retains significant internal process knowledge and spent $120M on manufacturing R&D in 2024 to balance dependency and support tech transfer readiness.

Collaborative Research Partners

Academic labs and small biotechs supply Ionis with core IP and early-stage RNA-target discoveries, and in 2024 about 35% of Ionis’s pipeline originated from external collaborators, giving suppliers leverage via unique patents and data exclusivity.

Specialized Equipment Manufacturers

Specialized equipment makers command leverage for antisense work because PCR-grade synthesizers and GMP oligonucleotide scale-up rigs cost $1–5m and integrate deeply into workflows, making switching expensive and slow.

Still, many high-throughput screening (HTS) instruments are standardized; global HTS market was $3.2bn in 2024, diluting supplier power and enabling competitive sourcing.

- High switching cost: $1–5m per unit

- Integration risk: months of validation

- Mitigant: $3.2bn HTS market (2024)

- Net: moderate supplier power

Regulatory and Quality Compliance Services

Providers of clinical trial management and regulatory consulting are critical for navigating FDA and EMA rules; delays or quality lapses can add months and millions—median FDA review adds ~10 months, and Phase III delays cost $20–100M.

These suppliers have leverage since their performance affects approval speed and launch timing, but Ionis uses scale and a 2025 track record of 12 partnered trials to secure better pricing and timelines.

- Essential: regulatory expertise reduces approval risk

- High impact: approval delays cost $20–100M per Phase III

- Leverage: Ionis 12 partnered trials in 2025 improves negotiation

- Mitigation: reputation and scale lower supplier power

Growing CMO pool eases supplier power—outsourcing, $120M R&D & 35% external pipeline

Suppliers exert moderate power: qualified CMO/GMP RNA sites <15, specialized gear $1–5M/unit, but vendor pool grew (qualified vendors ~25 in 2025 vs ~15 in 2020) cutting supply-cost volatility ~8%; Ionis outsourced 40–50% manufacturing (2024), spent $120M on manufacturing R&D (2024), and sourced ~35% pipeline from external collaborators (2024), creating patent leverage.

| Metric | Value (Year) |

|---|---|

| Qualified CMOs (GMP RNA) | <15 (2025) |

| Qualified vendors | ~25 (2025) |

| Outsourced volume | 40–50% (2024) |

| Manufacturing R&D spend | $120M (2024) |

| Pipeline from external partners | ~35% (2024) |

| HTS market | $3.2B (2024) |

What is included in the product

Concise Porter's Five Forces analysis tailored to Ionis, revealing competitive intensity, buyer and supplier power, entry barriers, and substitute threats with strategic implications for pricing, profitability, and growth.

Clear, one-sheet Porter's Five Forces for Ionis—instantly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Government and Private Payers

Insurance companies and national health systems are Ionis Therapeutics’s main buyers for its high-cost specialty drugs, and they push hard on price via value-based contracts and formulary exclusions; by 2024 payers negotiated rebates averaging 28–35% for novel RNA-targeted therapies.

Large Pharmaceutical Partners

Ionis routinely partners with pharma giants—Biogen, AstraZeneca, Roche—that control global distribution and marketing; these partners accounted for licensing and collaboration revenue of roughly $1.2 billion for Ionis in 2024, amplifying their leverage. Because they can prioritize Ionis assets across broad portfolios, they can demand tougher milestones, larger profit splits, and longer exclusivity terms, pressuring Ionis’s margin and negotiating position.

Specialty Pharmacies and Distributors

The small pool of specialty pharmacies and distributors—top 10 providers handle roughly 60–70% of RNA-drug cold-chain distribution in the US—gives them strong bargaining power over Ionis; they can demand higher service fees (premium of 5–12% typical) and extended payment terms (30–90 days), squeezing maker margins and complicating launch cash flows.

Patient Advocacy Groups

Patient advocacy groups shape adoption and reimbursement in rare disease; for example, Duchenne and SMA foundations helped secure access that drove nusinersen to >$1.5bn annual sales by 2020 and influenced payer coverage.

They are not direct buyers but their endorsements create market pull and regulatory pressure; Ionis must sustain partnerships to boost trial recruitment (rare-disease trials often need <200 patients) and payer dialogues.

- Advocacy drives payer decisions and access

- Endorsements boost uptake and pricing leverage

- Partnerships aid recruitment—trials often <200 pts

- Ionis needs ongoing engagement to secure commercial success

Health Technology Assessment (HTA) Bodies

- ICER: 2024 reports set value-based price ranges that shifted expected U.S. launch revenues by up to 30% for comparable rare-disease drugs.

- NICE: not-recommended decisions reduce UK patient access by >60% in first 2 years, per 2023 NHS data.

- Practical power: indirect but decisive—coverage hinges on HTA positive appraisal.

Payers, partners & distributors: squeezing RNA-drug margins with rebates, fees, and deals

Buyers—insurers, national health systems, and pharma partners—wield strong price and contract leverage: payers secured 28–35% rebates on novel RNA drugs by 2024, partners drove ~$1.2bn licensing revenue for Ionis in 2024 and can demand tougher milestones, and top 10 specialty distributors handle 60–70% of cold-chain volume charging 5–12% service premiums.

| Buyer | 2024/2023 Metric |

|---|---|

| Payer rebates | 28–35% |

| Partner revenue | $1.2bn (2024) |

| Top distributors’ share | 60–70% |

| Distribution premium | 5–12% |

What You See Is What You Get

Ionis Porter's Five Forces Analysis

This preview shows the exact Ionis Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

It contains the complete, professionally written assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry; once you buy, the same document is yours to download instantly.