Ipca PESTLE Analysis

Skip the Research. Get the Strategy.

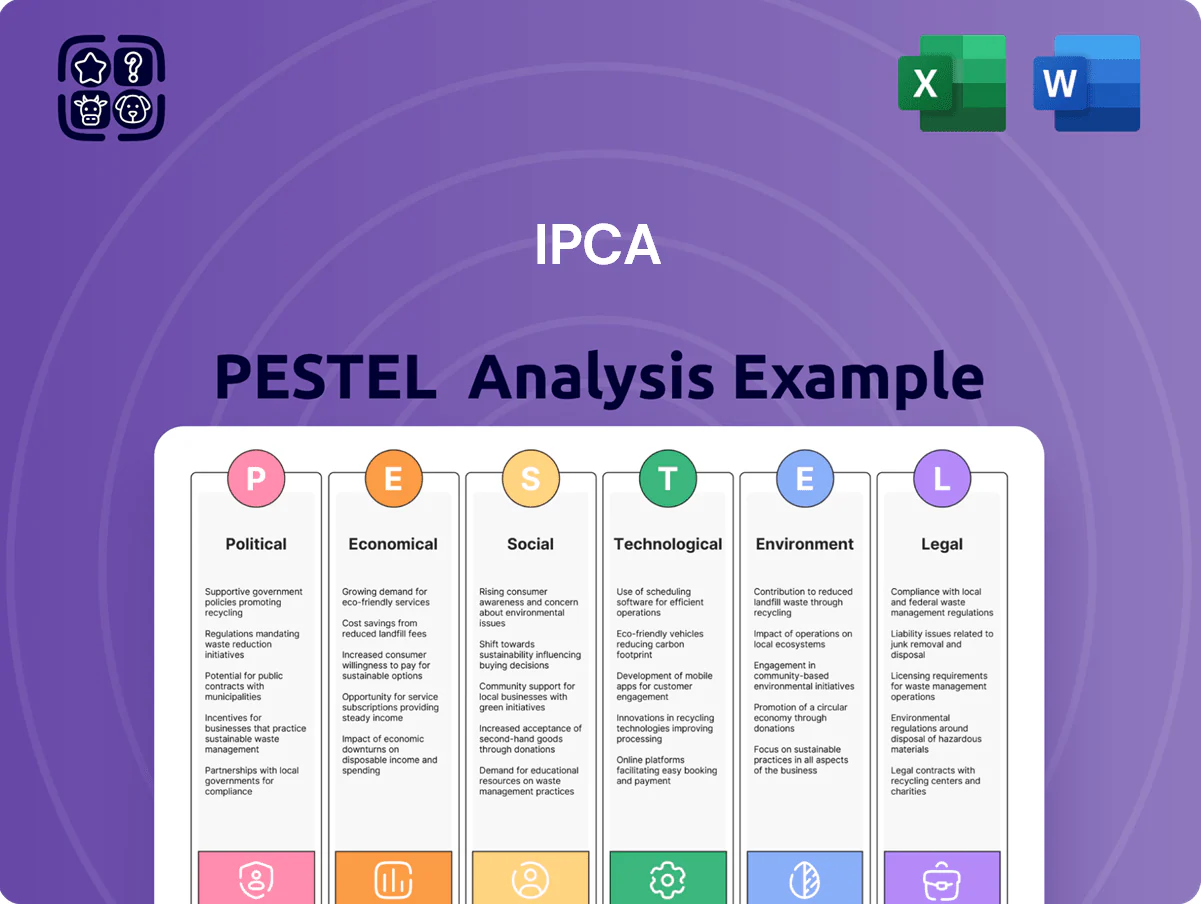

Unlock strategic clarity with our PESTLE Analysis of Ipca—uncover how political, economic, social, technological, legal, and environmental forces are shaping its growth and risk profile. Ideal for investors, consultants, and strategists, this concise yet powerful briefing highlights opportunities and threats you need to know. Purchase the full version to access the complete, editable report and make data-driven decisions with confidence.

Political factors

Government Healthcare Incentives

The Indian PLI scheme, allocating over INR 1.97 lakh crore across sectors, has catalyzed API capacity expansion; Ipca, qualifying for PLI-linked support, can leverage subsidies to scale API output—management guidance targets 15–20% capex-funded capacity growth through FY25–26. These incentives aim to cut import reliance (India imported ~70% of key starting materials in 2023) and could boost Ipca’s EBITDA margin by 150–300 bps if realized, so investors should track PLI disbursements and capex-to-subsidy recognition through 2026.

Geopolitical Trade Relations

Ipca’s exports accounted for about 58% of revenue in FY2024, making the firm sensitive to shifts in trade agreements and diplomatic ties with key markets in Africa, Europe and the Americas.

Political instability in parts of Africa and Latin America has previously caused supply disruptions and payment delays, notably impacting anti-malarial shipments that represent roughly 12% of export volumes.

The executive team prioritizes strategic market diversification—expanding EU tender participation and increasing presence in regulated US channels—to reduce concentration risk and cushion against bilateral trade disruptions.

Drug Price Control Regulations

The National Pharmaceutical Pricing Authority updated the National List of Essential Medicines in 2024, extending price caps that can affect Ipca's core formulations and compress gross margins—India's drug price controls covered over 300 medicines by 2024, directly impacting domestic revenue streams. Political emphasis on affordable healthcare has forced Indian generics firms to pursue higher volumes; Ipca reported 2024 domestic sales pressures with margins declining by mid-single digits year-on-year. Navigating NPPA ceilings is thus critical for Ipca to sustain FY2025 domestic profitability and retain market share.

Global Health Policy Alignment

As a major supplier of anti-malarial treatments, Ipca aligns strategies with WHO and global health funds; WHO procurement for artemisinin-based therapies accounted for about 40% of international institutional demand in 2024, affecting Ipca’s tender opportunities.

Shifts in donor funding—Global Fund disbursements fell 6% YoY to $3.5bn in 2024—can reduce procurement volumes for specialized meds, directly impacting Ipca’s institutional sales.

Maintaining strong relationships with intergovernmental organizations helps secure long-term contracts and a steady pipeline; institutional tenders represented roughly 22% of Ipca’s export revenues in FY2024.

- WHO/Global Fund policy changes drive tender volumes

- Global Fund 2024 disbursements ~$3.5bn (-6% YoY)

- WHO-sourced demand ≈40% of institutional anti-malarial procurement

- Institutional tenders ≈22% of Ipca export revenue FY2024

Regulatory Harmonization Efforts

Political moves toward harmonizing regulatory standards can shorten Ipca's drug approvals, potentially cutting time-to-market by months; WHO and ICH alignment efforts reached 18 guideline adoptions in 2024 impacting bioequivalence and GMP expectations.

India's participation in international forums (eg, ICH accession talks ongoing since 2021) lets Indian pharma shape global quality rules, aiding Ipca's exportability to EU and US markets where 2024 generics approvals rose 6%.

Such political alignment reduces multi-jurisdiction approval redundancies, enabling faster launch of off-patent generics across markets, supporting revenue scale-up—Indian generic exports were $25.5bn in FY2024.

- Harmonization shortens approval timelines

Policy boost cuts import risk but price caps and aid drop squeeze Ipca margins

Political support for domestic API capacity (PLI ≈INR1.97 lakh crore) and regulatory harmonization (18 ICH/WHO guidelines adopted in 2024) reduces import reliance (India imported ~70% of key starting materials in 2023) and shortens approvals, while NPPA price caps on 300+ medicines and falling donor flows (Global Fund ~$3.5bn in 2024, -6% YoY) create margin and tender-volume risks for Ipca.

| Metric | 2023–2024 |

|---|---|

| PLI allocation | INR1.97 lakh crore |

| Import reliance | ~70% |

| Ipca exports of rev | 58% (FY2024) |

| Institutional tenders rev | ≈22% (FY2024) |

| Global Fund disbursements | ~$3.5bn (-6% YoY) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ipca across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends for reliable, actionable insights.

Condenses Ipca's PESTLE into a concise, shareable brief that highlights regulatory, market and operational risks for quick decision-making and seamless inclusion in presentations or planning decks.

Economic factors

Currency Exchange Volatility

As an exporter to 100+ countries, Ipca is exposed to INR/USD and INR/EUR swings; a 5% rupee appreciation in 2024 would cut dollar-denominated realizations materially given exports constituted ~55% of revenue in FY2024 (₹2,760 crore exports). A weaker rupee in 2024–25 bolstered export margins, while management’s hedging reduced FX loss volatility to 0.8% of EBITDA in FY2024. Active foreign-currency debt management and forward contracts remain key to stabilise earnings.

Rising Input and Energy Costs

Global inflation raised input and energy costs, with India wholesale inflation averaging ~6.5% in 2024 and global oil prices up ~15% YoY, squeezing API margins as solvent and raw material costs rose ~10–20% for manufacturers.

Ipca faces limited pass-through power due to competitive generic pricing and price controls; FY2024 gross margin pressure was visible as EBITDA margin narrowed to ~13–14%.

Efficient supply-chain management and backward integration into key intermediates (reducing import dependence) remain critical levers to protect margins and offset a ~5–10% cost headwind.

Emerging Market Growth Potential

Economic expansion in emerging markets—GDP growth averaging 4.5–5.5% in 2024–25 across key regions like India, Southeast Asia and parts of Africa—is boosting disposable incomes and healthcare spend, with out-of-pocket health expenditure rising ~6–8% CAGR. Ipca is positioned to capture this via affordable branded generics, supported by emerging-market revenue contributing roughly 40–50% of its FY2024 sales. The focus on these regions buffers Ipca against low-single-digit growth in developed markets and underpins mid-single-digit overall company growth targets.

API Backward Integration Advantages

API backward integration lets Ipca control input costs and secure API supply, lowering COGS volatility; in FY2024 Ipca’s API segment contributed circa 28% of revenue, helping stabilize margins amid raw material inflation.

Producing APIs reduces reliance on Chinese suppliers—China accounted for about 60% of global generic API exports in 2023—mitigating price-shock risk and supply disruption exposure.

This structural edge supports Ipca’s competitiveness in the global generics market through 2026, sustaining pricing power and faster time-to-market for launches.

- API vertical integration → lower COGS, margin stability

- FY2024: API ~28% of revenue

- Reduces dependence on China (~60% share of global API exports in 2023)

- Enhances competitive positioning and launch speed through 2026

Interest Rate Environment

Fluctuations in domestic RBI policy rates and global rates (US 10-yr ~4.0% in Feb 2026) affect Ipca Laboratories’ borrowing costs for capital-intensive expansion; higher rates raise interest expense and can delay infrastructure upgrades or acquisitions.

Analysts track Ipca’s debt-to-equity (~0.25 FY2025) and interest coverage (~10x FY2025) to gauge resilience across cycles; rising rates would compress margins and slow investment.

- Higher RBI repo (2024–25 avg ~6.5%) raises loan costs

- Debt/equity ~0.25 (FY2025)

- Interest cover ~10x (FY2025)

Export-led margins hinge on FX hedges; API integration trims China risk, rates tested

Export FX exposure (exports ~55% of FY2024 revenue; ₹2,760 crore) and hedging (FX volatility ~0.8% of EBITDA FY2024) drive earnings sensitivity; API vertical integration (API ~28% of revenue FY2024) cuts COGS and reduces China reliance (~60% global API exports 2023). Higher rates (RBI repo ~6.5% 2024–25) affect borrowing; debt/equity ~0.25 and interest cover ~10x (FY2025).

| Metric | Value |

|---|---|

| Exports (% rev) | ~55% |

| Export ₹ | ₹2,760cr (FY2024) |

| API (% rev) | ~28% |

| China API share | ~60% (2023) |

| RBI repo | ~6.5% (2024–25) |

| D/E | ~0.25 (FY2025) |

| Interest cover | ~10x (FY2025) |

Preview the Actual Deliverable

Ipca PESTLE Analysis

The preview shown here is the exact Ipca PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the layout, content, and structure visible are identical to the downloadable file, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Ipca—uncover how political, economic, social, technological, legal, and environmental forces are shaping its growth and risk profile. Ideal for investors, consultants, and strategists, this concise yet powerful briefing highlights opportunities and threats you need to know. Purchase the full version to access the complete, editable report and make data-driven decisions with confidence.

Political factors

Government Healthcare Incentives

The Indian PLI scheme, allocating over INR 1.97 lakh crore across sectors, has catalyzed API capacity expansion; Ipca, qualifying for PLI-linked support, can leverage subsidies to scale API output—management guidance targets 15–20% capex-funded capacity growth through FY25–26. These incentives aim to cut import reliance (India imported ~70% of key starting materials in 2023) and could boost Ipca’s EBITDA margin by 150–300 bps if realized, so investors should track PLI disbursements and capex-to-subsidy recognition through 2026.

Geopolitical Trade Relations

Ipca’s exports accounted for about 58% of revenue in FY2024, making the firm sensitive to shifts in trade agreements and diplomatic ties with key markets in Africa, Europe and the Americas.

Political instability in parts of Africa and Latin America has previously caused supply disruptions and payment delays, notably impacting anti-malarial shipments that represent roughly 12% of export volumes.

The executive team prioritizes strategic market diversification—expanding EU tender participation and increasing presence in regulated US channels—to reduce concentration risk and cushion against bilateral trade disruptions.

Drug Price Control Regulations

The National Pharmaceutical Pricing Authority updated the National List of Essential Medicines in 2024, extending price caps that can affect Ipca's core formulations and compress gross margins—India's drug price controls covered over 300 medicines by 2024, directly impacting domestic revenue streams. Political emphasis on affordable healthcare has forced Indian generics firms to pursue higher volumes; Ipca reported 2024 domestic sales pressures with margins declining by mid-single digits year-on-year. Navigating NPPA ceilings is thus critical for Ipca to sustain FY2025 domestic profitability and retain market share.

Global Health Policy Alignment

As a major supplier of anti-malarial treatments, Ipca aligns strategies with WHO and global health funds; WHO procurement for artemisinin-based therapies accounted for about 40% of international institutional demand in 2024, affecting Ipca’s tender opportunities.

Shifts in donor funding—Global Fund disbursements fell 6% YoY to $3.5bn in 2024—can reduce procurement volumes for specialized meds, directly impacting Ipca’s institutional sales.

Maintaining strong relationships with intergovernmental organizations helps secure long-term contracts and a steady pipeline; institutional tenders represented roughly 22% of Ipca’s export revenues in FY2024.

- WHO/Global Fund policy changes drive tender volumes

- Global Fund 2024 disbursements ~$3.5bn (-6% YoY)

- WHO-sourced demand ≈40% of institutional anti-malarial procurement

- Institutional tenders ≈22% of Ipca export revenue FY2024

Regulatory Harmonization Efforts

Political moves toward harmonizing regulatory standards can shorten Ipca's drug approvals, potentially cutting time-to-market by months; WHO and ICH alignment efforts reached 18 guideline adoptions in 2024 impacting bioequivalence and GMP expectations.

India's participation in international forums (eg, ICH accession talks ongoing since 2021) lets Indian pharma shape global quality rules, aiding Ipca's exportability to EU and US markets where 2024 generics approvals rose 6%.

Such political alignment reduces multi-jurisdiction approval redundancies, enabling faster launch of off-patent generics across markets, supporting revenue scale-up—Indian generic exports were $25.5bn in FY2024.

- Harmonization shortens approval timelines

Policy boost cuts import risk but price caps and aid drop squeeze Ipca margins

Political support for domestic API capacity (PLI ≈INR1.97 lakh crore) and regulatory harmonization (18 ICH/WHO guidelines adopted in 2024) reduces import reliance (India imported ~70% of key starting materials in 2023) and shortens approvals, while NPPA price caps on 300+ medicines and falling donor flows (Global Fund ~$3.5bn in 2024, -6% YoY) create margin and tender-volume risks for Ipca.

| Metric | 2023–2024 |

|---|---|

| PLI allocation | INR1.97 lakh crore |

| Import reliance | ~70% |

| Ipca exports of rev | 58% (FY2024) |

| Institutional tenders rev | ≈22% (FY2024) |

| Global Fund disbursements | ~$3.5bn (-6% YoY) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ipca across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends for reliable, actionable insights.

Condenses Ipca's PESTLE into a concise, shareable brief that highlights regulatory, market and operational risks for quick decision-making and seamless inclusion in presentations or planning decks.

Economic factors

Currency Exchange Volatility

As an exporter to 100+ countries, Ipca is exposed to INR/USD and INR/EUR swings; a 5% rupee appreciation in 2024 would cut dollar-denominated realizations materially given exports constituted ~55% of revenue in FY2024 (₹2,760 crore exports). A weaker rupee in 2024–25 bolstered export margins, while management’s hedging reduced FX loss volatility to 0.8% of EBITDA in FY2024. Active foreign-currency debt management and forward contracts remain key to stabilise earnings.

Rising Input and Energy Costs

Global inflation raised input and energy costs, with India wholesale inflation averaging ~6.5% in 2024 and global oil prices up ~15% YoY, squeezing API margins as solvent and raw material costs rose ~10–20% for manufacturers.

Ipca faces limited pass-through power due to competitive generic pricing and price controls; FY2024 gross margin pressure was visible as EBITDA margin narrowed to ~13–14%.

Efficient supply-chain management and backward integration into key intermediates (reducing import dependence) remain critical levers to protect margins and offset a ~5–10% cost headwind.

Emerging Market Growth Potential

Economic expansion in emerging markets—GDP growth averaging 4.5–5.5% in 2024–25 across key regions like India, Southeast Asia and parts of Africa—is boosting disposable incomes and healthcare spend, with out-of-pocket health expenditure rising ~6–8% CAGR. Ipca is positioned to capture this via affordable branded generics, supported by emerging-market revenue contributing roughly 40–50% of its FY2024 sales. The focus on these regions buffers Ipca against low-single-digit growth in developed markets and underpins mid-single-digit overall company growth targets.

API Backward Integration Advantages

API backward integration lets Ipca control input costs and secure API supply, lowering COGS volatility; in FY2024 Ipca’s API segment contributed circa 28% of revenue, helping stabilize margins amid raw material inflation.

Producing APIs reduces reliance on Chinese suppliers—China accounted for about 60% of global generic API exports in 2023—mitigating price-shock risk and supply disruption exposure.

This structural edge supports Ipca’s competitiveness in the global generics market through 2026, sustaining pricing power and faster time-to-market for launches.

- API vertical integration → lower COGS, margin stability

- FY2024: API ~28% of revenue

- Reduces dependence on China (~60% share of global API exports in 2023)

- Enhances competitive positioning and launch speed through 2026

Interest Rate Environment

Fluctuations in domestic RBI policy rates and global rates (US 10-yr ~4.0% in Feb 2026) affect Ipca Laboratories’ borrowing costs for capital-intensive expansion; higher rates raise interest expense and can delay infrastructure upgrades or acquisitions.

Analysts track Ipca’s debt-to-equity (~0.25 FY2025) and interest coverage (~10x FY2025) to gauge resilience across cycles; rising rates would compress margins and slow investment.

- Higher RBI repo (2024–25 avg ~6.5%) raises loan costs

- Debt/equity ~0.25 (FY2025)

- Interest cover ~10x (FY2025)

Export-led margins hinge on FX hedges; API integration trims China risk, rates tested

Export FX exposure (exports ~55% of FY2024 revenue; ₹2,760 crore) and hedging (FX volatility ~0.8% of EBITDA FY2024) drive earnings sensitivity; API vertical integration (API ~28% of revenue FY2024) cuts COGS and reduces China reliance (~60% global API exports 2023). Higher rates (RBI repo ~6.5% 2024–25) affect borrowing; debt/equity ~0.25 and interest cover ~10x (FY2025).

| Metric | Value |

|---|---|

| Exports (% rev) | ~55% |

| Export ₹ | ₹2,760cr (FY2024) |

| API (% rev) | ~28% |

| China API share | ~60% (2023) |

| RBI repo | ~6.5% (2024–25) |

| D/E | ~0.25 (FY2025) |

| Interest cover | ~10x (FY2025) |

Preview the Actual Deliverable

Ipca PESTLE Analysis

The preview shown here is the exact Ipca PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the layout, content, and structure visible are identical to the downloadable file, with no placeholders or surprises.