IR PESTLE Analysis

Skip the Research. Get the Strategy.

Our PESTLE Analysis of IR reveals how political shifts, economic trends, and technological advances are reshaping the company’s outlook—perfect for investors and strategists who need timely, actionable intelligence; buy the full, fully editable report to access deep-dive insights, risk ratings, and practical recommendations you can use immediately.

Political factors

Geopolitical Trade Volatility

The escalating US-China trade tensions have driven Ingersoll Rand to accelerate supply‑chain diversification, reducing exposure to China from an estimated 35% of parts sourcing in 2020 toward targeted regionalization; tariffs on industrial components—averaging 7–25% in recent US measures—push manufacturing closer to end markets to avoid cost spikes. Continuous monitoring of WTO, USMCA and RCEP developments is required to preserve global pricing competitiveness and protect 2025 gross margins, which averaged about 30% in 2024.

Infrastructure Spending Stimulus

Government initiatives like the US Infrastructure Investment and Jobs Act, which allocates 1.2 trillion USD (with 550 billion USD new spending) through 2026, create a multi-year demand floor for industrial flow and compression technologies, supporting sustained orders for water management and transport projects. These state-funded programs drive long-term capital expenditure—US public construction spending rose 6.1% in 2024—positioning Ingersoll Rand to capture increased procurement as countries prioritize domestic industrial resilience.

Defense and Security Spending

Rising NATO defense budgets—NATO members pledged a 4.5% real increase in 2024, with US defense spending at about $858B in 2024—boost demand for specialized power tools and material-handling systems used in maintenance and logistics.

Governments link stability to industrial capacity, offering incentives: EU’s 2024 Critical Raw Materials Act and €8B defense industrial funds drive onshore production of critical machinery.

These policies expand markets for high-reliability industrial solutions in military and security sectors, where contract values often exceed $50M per program and multi-year procurement pipelines improve revenue visibility.

Corporate Tax Policy Shifts

The 2024 global minimum tax (OECD Pillar Two) at 15% and recent U.S. proposal to raise effective rates shift net margins for Ingersoll Rand, which reported $14.5B revenue in 2024, making multinational tax strategy crucial to preserve profitability.

Political moves increasing corporate accountability force IR to manage transfer pricing, repatriation, and tax-efficient capital allocation across 30+ countries of operation.

Changes to R&D tax credits and depreciation schedules could swing EPS forecasts by several cents; sensitivity analyses show a 1% effective tax rate change can alter net income by roughly $30–40M for a company of IRs scale.

- Global minimum tax 15% (OECD Pillar Two)

- 2024 revenue $14.5B — tax strategy material to margins

- Operations in 30+ countries increase compliance complexity

- 1% ETR shift ≈ $30–40M net income impact

Energy Security Policies

Political moves for energy independence are driving investment into LNG and hydrogen; global LNG trade rose 6% to 400 Mt in 2024 and hydrogen project capacity reached 15 GW electrolyzer announcements by end-2025, boosting demand for specialized pumps and compressors.

Rising subsidies—EU committed €210 billion to clean energy 2024–27 and US IRA tax credits—expand buyers for the company’s technologies and lower customer CAPEX barriers.

Government support for CCS (global capacity target ~0.2 MtCO2/yr in 2024 with planned projects aiming >50 MtCO2 by 2030) widens markets for industrial flow solutions and retrofit services.

- 400 Mt LNG trade (2024); hydrogen electrolyzer capacity announcements 15 GW (2025)

- EU €210B clean energy funding 2024–27; US IRA tax incentives

- CCS planned capacity >50 MtCO2 by 2030 expanding retrofit demand

Geopolitics, taxes and subsidies Rewire Supply Chains — Boosting Pumps & Compressors Demand

Political risks and incentives reshape IR: trade tensions and tariffs drive supply‑chain regionalization (China parts share cut from ~35% in 2020); state infrastructure spend (US $1.2T act) and defense budget rises support demand; OECD 15% global minimum tax and 30+ country footprint make tax strategy material (2024 revenue $14.5B; 1% ETR ≈ $30–40M NI); clean‑energy subsidies (EU €210B, US IRA) expand market for pumps/compressors.

| Metric | 2024/25 Data |

|---|---|

| Revenue | $14.5B (2024) |

| China parts share | ~35% (2020) ↓ |

| OECD Pillar Two | 15% GMT (2024) |

| US Infra Act | $1.2T (through 2026) |

| EU clean funding | €210B (2024–27) |

What is included in the product

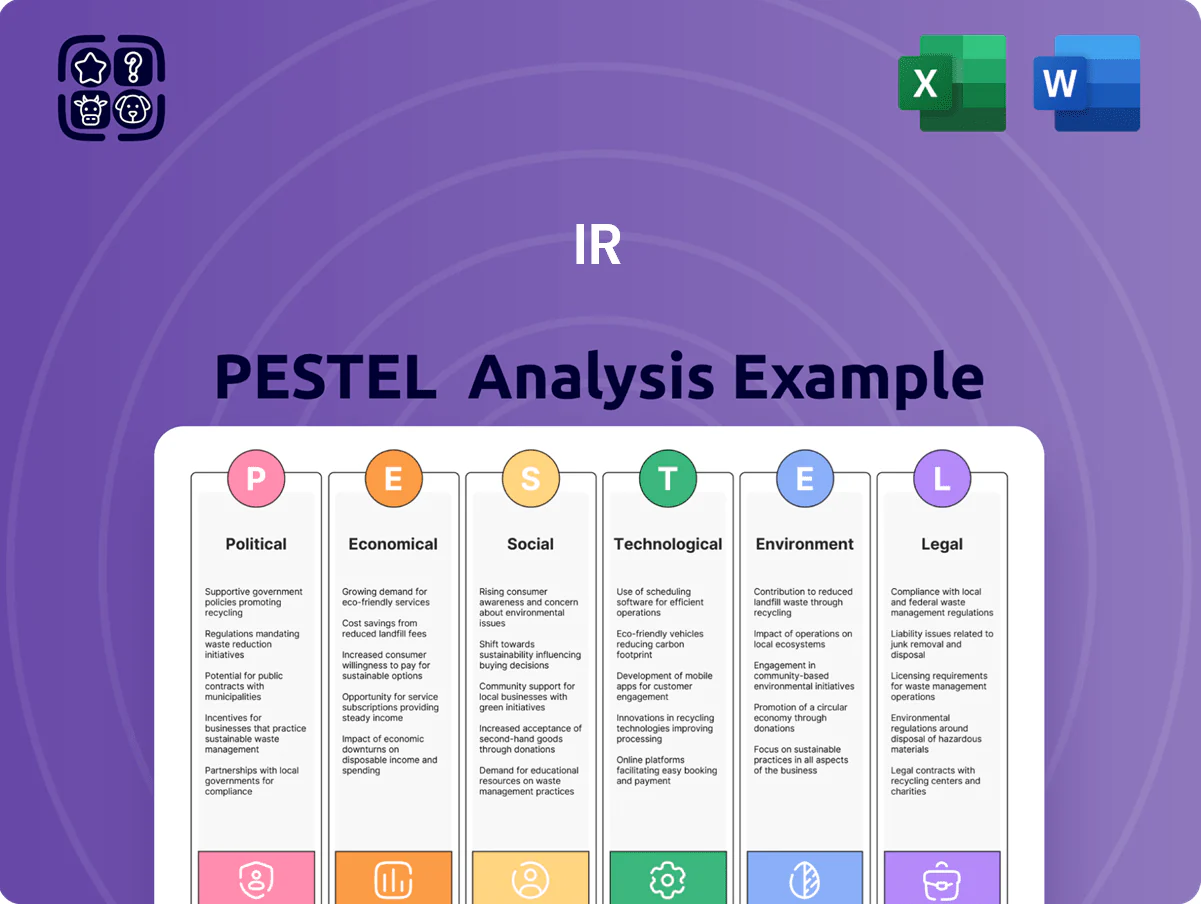

Explores how external macro-environmental factors uniquely affect the IR across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and forward-looking scenarios for executives, consultants, and entrepreneurs.

Summarizes the full IR PESTLE analysis into a concise, visually segmented brief that’s easy to drop into presentations, share across teams, and adapt with region- or business-specific notes for faster strategic alignment.

Economic factors

Global Interest Rate Environment

As central banks move down from 2022–2023 peak rates, global policy rates fell on average by ~150–200 bps through 2024–2025, stabilizing cost of capital for large industrial projects; 10-year U.S. Treasury yields averaged ~3.8% in 2025 versus ~4.2% in 2023. This easing encourages Ingersoll Rand customers to restart deferred CAPEX on air compressors and vacuum systems, with global industrial machinery orders rising ~6% y/y in 2024. Lower borrowing costs support higher sales volumes for high-ticket equipment across manufacturing, aiding order pipelines and margin recovery.

Industrial Inflation and Input Costs

Persistent volatility in steel, copper and aluminum—steel up ~18% YTD and copper +12% in 2025—compresses industrial margins, with global input costs rising ~9% year-over-year for manufacturers in 2024. Ingersoll Rand offsets inflation via dynamic pricing, hedging and lean manufacturing, reporting gross margin resilience near 31% in FY2024. Managing energy cost swings, where industrial electricity prices rose ~7% in 2024, remains key to safeguarding factory efficiency worldwide.

Currency Exchange Rate Fluctuations

The U.S. dollar’s 2024 appreciation—about 6% vs the euro and 4% vs the yen year-to-date—has reduced reported revenue by roughly the same magnitude for firms with euro/yen sales, eroding price competitiveness in Europe and Japan.

In 2023–24, several emerging markets saw currency drops of 10–30%, making exports costlier locally and depressing volume; such devaluations heighten demand volatility and margin pressure.

Active hedging is critical: by end-2024, global corporates increased FX forward and option usage by ~12% to mitigate P&L swings, protecting EBITDA from abrupt FX moves.

Labor Market Dynamics

The ongoing shortage of skilled labor in manufacturing has pushed average hourly wages up 5.8% YoY in the US manufacturing sector through 2024, raising unit labor costs and total production expenses for industrial equipment makers.

Heightened competition for technical talent is accelerating capital expenditure into automation—global industrial robotics installations rose 10% in 2024—allowing firms to sustain output without proportional headcount increases.

This shift increases demand for Ingersoll Rand’s ergonomic power tools, supporting higher individual productivity and reducing injury-related downtime; IR’s industrial tools segment grew mid-single digits in 2024, reflecting this trend.

- Wages +5.8% YoY (US manufacturing, 2024)

- Industrial robot installs +10% (2024)

- IR tools segment mid-single digit growth (2024)

Reshoring and Nearshoring Trends

Rising reshoring and nearshoring drive regional factory builds: US reshoring investments reached $500B in announced projects for 2023–2025, while EU industrial relocation spending grew ~12% YoY in 2024, boosting demand for production equipment in North America and Europe.

Regionalization shortens lead times and cuts logistics costs ~15–25%, lowering supply-chain disruption losses; this creates service and aftermarket revenue opportunities and reduces dependence on distant centralized hubs.

- US reshoring projects: $500B (2023–2025)

- EU relocation capex growth: ~12% YoY (2024)

- Logistics cost/time savings: ~15–25%

- Stronger aftermarket/service revenue potential in NA and EU

Policy cuts revive CAPEX amid input inflation, USD strength and automation surge

Lower policy rates (policy cuts ~150–200 bps through 2024–25) and 10y UST ~3.8% (2025) revive CAPEX; input inflation (steel +18%, copper +12% YTD 2025) and energy +7% (2024) squeeze margins; USD up ~6% vs EUR (2024) and EM currency drops 10–30% disrupt volumes; wages +5.8% (US mfg 2024) and robot installs +10% (2024) shift spend to automation, boosting IR tools mid-single-digit growth (2024).

| Metric | Value |

|---|---|

| Policy cuts | 150–200 bps (2024–25) |

| 10y UST | ~3.8% (2025) |

| Steel / Copper | +18% / +12% (2025 YTD) |

| Energy | +7% (2024) |

| USD vs EUR | +6% (2024) |

| Wages (US mfg) | +5.8% (2024) |

| Robot installs | +10% (2024) |

| IR tools growth | Mid-single digits (2024) |

Full Version Awaits

IR PESTLE Analysis

The preview shown here is the exact IR PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Our PESTLE Analysis of IR reveals how political shifts, economic trends, and technological advances are reshaping the company’s outlook—perfect for investors and strategists who need timely, actionable intelligence; buy the full, fully editable report to access deep-dive insights, risk ratings, and practical recommendations you can use immediately.

Political factors

Geopolitical Trade Volatility

The escalating US-China trade tensions have driven Ingersoll Rand to accelerate supply‑chain diversification, reducing exposure to China from an estimated 35% of parts sourcing in 2020 toward targeted regionalization; tariffs on industrial components—averaging 7–25% in recent US measures—push manufacturing closer to end markets to avoid cost spikes. Continuous monitoring of WTO, USMCA and RCEP developments is required to preserve global pricing competitiveness and protect 2025 gross margins, which averaged about 30% in 2024.

Infrastructure Spending Stimulus

Government initiatives like the US Infrastructure Investment and Jobs Act, which allocates 1.2 trillion USD (with 550 billion USD new spending) through 2026, create a multi-year demand floor for industrial flow and compression technologies, supporting sustained orders for water management and transport projects. These state-funded programs drive long-term capital expenditure—US public construction spending rose 6.1% in 2024—positioning Ingersoll Rand to capture increased procurement as countries prioritize domestic industrial resilience.

Defense and Security Spending

Rising NATO defense budgets—NATO members pledged a 4.5% real increase in 2024, with US defense spending at about $858B in 2024—boost demand for specialized power tools and material-handling systems used in maintenance and logistics.

Governments link stability to industrial capacity, offering incentives: EU’s 2024 Critical Raw Materials Act and €8B defense industrial funds drive onshore production of critical machinery.

These policies expand markets for high-reliability industrial solutions in military and security sectors, where contract values often exceed $50M per program and multi-year procurement pipelines improve revenue visibility.

Corporate Tax Policy Shifts

The 2024 global minimum tax (OECD Pillar Two) at 15% and recent U.S. proposal to raise effective rates shift net margins for Ingersoll Rand, which reported $14.5B revenue in 2024, making multinational tax strategy crucial to preserve profitability.

Political moves increasing corporate accountability force IR to manage transfer pricing, repatriation, and tax-efficient capital allocation across 30+ countries of operation.

Changes to R&D tax credits and depreciation schedules could swing EPS forecasts by several cents; sensitivity analyses show a 1% effective tax rate change can alter net income by roughly $30–40M for a company of IRs scale.

- Global minimum tax 15% (OECD Pillar Two)

- 2024 revenue $14.5B — tax strategy material to margins

- Operations in 30+ countries increase compliance complexity

- 1% ETR shift ≈ $30–40M net income impact

Energy Security Policies

Political moves for energy independence are driving investment into LNG and hydrogen; global LNG trade rose 6% to 400 Mt in 2024 and hydrogen project capacity reached 15 GW electrolyzer announcements by end-2025, boosting demand for specialized pumps and compressors.

Rising subsidies—EU committed €210 billion to clean energy 2024–27 and US IRA tax credits—expand buyers for the company’s technologies and lower customer CAPEX barriers.

Government support for CCS (global capacity target ~0.2 MtCO2/yr in 2024 with planned projects aiming >50 MtCO2 by 2030) widens markets for industrial flow solutions and retrofit services.

- 400 Mt LNG trade (2024); hydrogen electrolyzer capacity announcements 15 GW (2025)

- EU €210B clean energy funding 2024–27; US IRA tax incentives

- CCS planned capacity >50 MtCO2 by 2030 expanding retrofit demand

Geopolitics, taxes and subsidies Rewire Supply Chains — Boosting Pumps & Compressors Demand

Political risks and incentives reshape IR: trade tensions and tariffs drive supply‑chain regionalization (China parts share cut from ~35% in 2020); state infrastructure spend (US $1.2T act) and defense budget rises support demand; OECD 15% global minimum tax and 30+ country footprint make tax strategy material (2024 revenue $14.5B; 1% ETR ≈ $30–40M NI); clean‑energy subsidies (EU €210B, US IRA) expand market for pumps/compressors.

| Metric | 2024/25 Data |

|---|---|

| Revenue | $14.5B (2024) |

| China parts share | ~35% (2020) ↓ |

| OECD Pillar Two | 15% GMT (2024) |

| US Infra Act | $1.2T (through 2026) |

| EU clean funding | €210B (2024–27) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the IR across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and forward-looking scenarios for executives, consultants, and entrepreneurs.

Summarizes the full IR PESTLE analysis into a concise, visually segmented brief that’s easy to drop into presentations, share across teams, and adapt with region- or business-specific notes for faster strategic alignment.

Economic factors

Global Interest Rate Environment

As central banks move down from 2022–2023 peak rates, global policy rates fell on average by ~150–200 bps through 2024–2025, stabilizing cost of capital for large industrial projects; 10-year U.S. Treasury yields averaged ~3.8% in 2025 versus ~4.2% in 2023. This easing encourages Ingersoll Rand customers to restart deferred CAPEX on air compressors and vacuum systems, with global industrial machinery orders rising ~6% y/y in 2024. Lower borrowing costs support higher sales volumes for high-ticket equipment across manufacturing, aiding order pipelines and margin recovery.

Industrial Inflation and Input Costs

Persistent volatility in steel, copper and aluminum—steel up ~18% YTD and copper +12% in 2025—compresses industrial margins, with global input costs rising ~9% year-over-year for manufacturers in 2024. Ingersoll Rand offsets inflation via dynamic pricing, hedging and lean manufacturing, reporting gross margin resilience near 31% in FY2024. Managing energy cost swings, where industrial electricity prices rose ~7% in 2024, remains key to safeguarding factory efficiency worldwide.

Currency Exchange Rate Fluctuations

The U.S. dollar’s 2024 appreciation—about 6% vs the euro and 4% vs the yen year-to-date—has reduced reported revenue by roughly the same magnitude for firms with euro/yen sales, eroding price competitiveness in Europe and Japan.

In 2023–24, several emerging markets saw currency drops of 10–30%, making exports costlier locally and depressing volume; such devaluations heighten demand volatility and margin pressure.

Active hedging is critical: by end-2024, global corporates increased FX forward and option usage by ~12% to mitigate P&L swings, protecting EBITDA from abrupt FX moves.

Labor Market Dynamics

The ongoing shortage of skilled labor in manufacturing has pushed average hourly wages up 5.8% YoY in the US manufacturing sector through 2024, raising unit labor costs and total production expenses for industrial equipment makers.

Heightened competition for technical talent is accelerating capital expenditure into automation—global industrial robotics installations rose 10% in 2024—allowing firms to sustain output without proportional headcount increases.

This shift increases demand for Ingersoll Rand’s ergonomic power tools, supporting higher individual productivity and reducing injury-related downtime; IR’s industrial tools segment grew mid-single digits in 2024, reflecting this trend.

- Wages +5.8% YoY (US manufacturing, 2024)

- Industrial robot installs +10% (2024)

- IR tools segment mid-single digit growth (2024)

Reshoring and Nearshoring Trends

Rising reshoring and nearshoring drive regional factory builds: US reshoring investments reached $500B in announced projects for 2023–2025, while EU industrial relocation spending grew ~12% YoY in 2024, boosting demand for production equipment in North America and Europe.

Regionalization shortens lead times and cuts logistics costs ~15–25%, lowering supply-chain disruption losses; this creates service and aftermarket revenue opportunities and reduces dependence on distant centralized hubs.

- US reshoring projects: $500B (2023–2025)

- EU relocation capex growth: ~12% YoY (2024)

- Logistics cost/time savings: ~15–25%

- Stronger aftermarket/service revenue potential in NA and EU

Policy cuts revive CAPEX amid input inflation, USD strength and automation surge

Lower policy rates (policy cuts ~150–200 bps through 2024–25) and 10y UST ~3.8% (2025) revive CAPEX; input inflation (steel +18%, copper +12% YTD 2025) and energy +7% (2024) squeeze margins; USD up ~6% vs EUR (2024) and EM currency drops 10–30% disrupt volumes; wages +5.8% (US mfg 2024) and robot installs +10% (2024) shift spend to automation, boosting IR tools mid-single-digit growth (2024).

| Metric | Value |

|---|---|

| Policy cuts | 150–200 bps (2024–25) |

| 10y UST | ~3.8% (2025) |

| Steel / Copper | +18% / +12% (2025 YTD) |

| Energy | +7% (2024) |

| USD vs EUR | +6% (2024) |

| Wages (US mfg) | +5.8% (2024) |

| Robot installs | +10% (2024) |

| IR tools growth | Mid-single digits (2024) |

Full Version Awaits

IR PESTLE Analysis

The preview shown here is the exact IR PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.